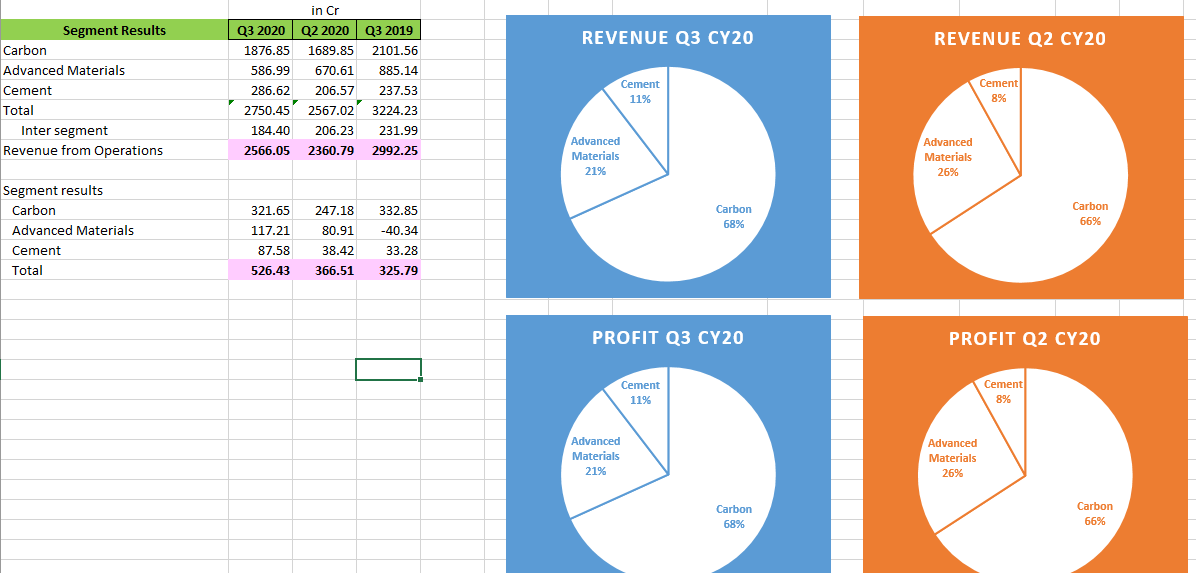

avg. blended realization was low for Carbon (-18%) - overall lower demand from various industry segments like Aluminium, Carbon Black, Construction and Graphite industries.

volumes for advanced segment were down by (-15%), but realization was up by ~3% (customer mix changes)- overall customers were impacted by Covid & shutdown

Cement revenue increased by 21%

higher realization in engineered prodcuts and Resins thus higher increase YoY

Hurrican Laura at Lake Charles, LA - shut down from Aug 23rd to partial prod resumed, 100% by 1st week of Nov

Lock down in india impacted - all plants shut down in march 2020.; phase resumption from April. Volumes across groups impacted gross margins.

ACP clearance by Supreme court is the only pending piece - all other clearneces have been obtained including raw material imports.

Aluminium prices have started growing up. Market share of company excluding china is at 10% globally.

lower margin facility in Netherlands shutdown is adding value.

Despite fall in volumes in Advanced Materials segment, EBITDA has improved due to:

lower raw material prices,

shutdown of lower-margin facility in the Netherlands coupled with appreciation of Euro against INR

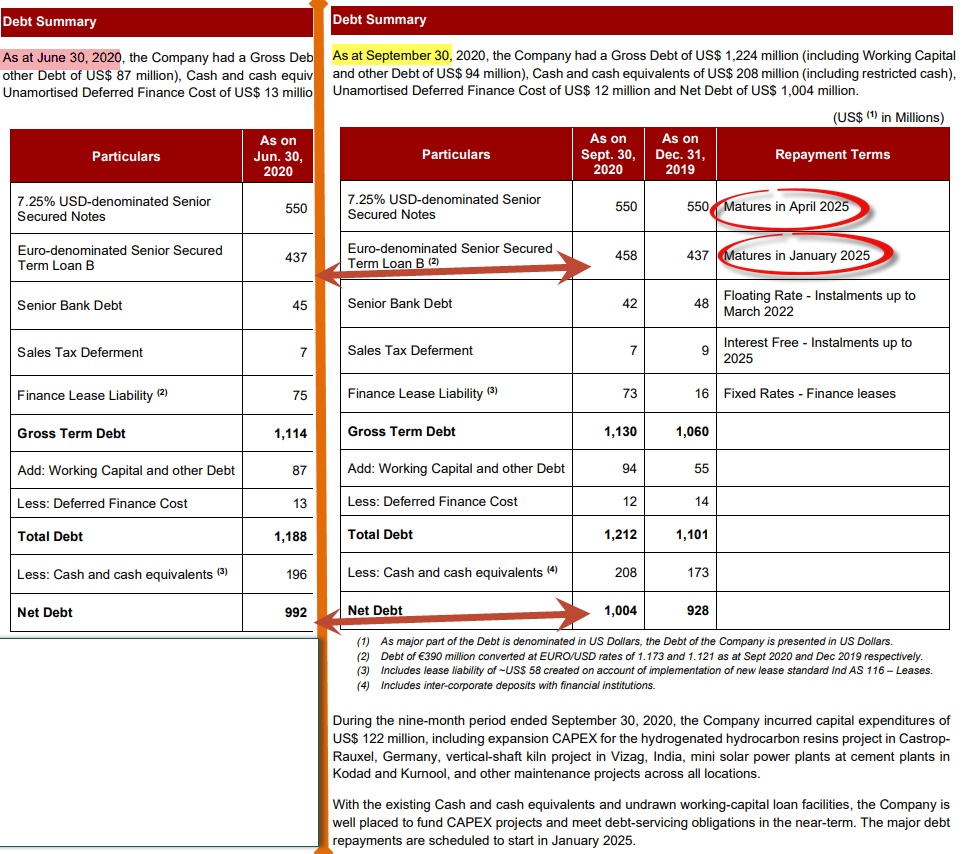

@ganeshrpl - Thanks for the summary of Conf call. Was there a word on conf call regarding the debt repayments in coming quarters as debt indeed increased in last quarter

also, note that mgmt. has stated that apart from the current capex in HHCR, Germany plant and Vertical shaft in Vizag, there is no planned major capex (apart from the regular yearly maintenance capex of 60-70). So all the CF that is going to come in, they can technically start paying back the debt. Note, a few of these debts are not due until 2025, but they have a clause wherein they cant pre-pay until 2022; if they do, they have to pay a penalty.

For further mgmt. commentary listen to call (2mins on this topic) at around 25-26mins. Rain Industries Earnings Call for Q3CY20 - YouTube

Been invested for 2 years. It looks like great value (the high debt looks manageable) now, like it did then.

My question to the knowledgeable:

Is Rain industries also a possible play on the very long term EV adoption story? I ask, because Electric vehicles will use more aluminum, and Rain Industries’ business depends on Aluminum demand.

Growth in aluminium does not translate into growth in stock price. What really creates value is whether that growth is profitable. If there is enough supply then no one makes money. Try to answer why should rain benefit and why others cannot compete or raise capacities if needed.

Not really a play on EV. not eve a play on aluminium price. Basically, its 80% EBITDA depends on Carbon products EBITDA margin which range between $30/ton the low side, $140/t on the higher side. Pure cyclical where we should buy when margins are lower and sell when they rise too high to be sustainable or even before that. Another play could have been delevaring- however, management has clearly ruled it out. They love debt and not at all keen to bring down debt.

Currently, its Annyhydrous Carbon material will lead to structurally lower costs/ higher volumes and there will be a big one time benefit and better Carbon margins.

Certainly undervalued i feel. Its trying to get its into resins as management feels its better to experiment with cash rather than deleverage.

Multiple subsidiaries and operations across the globe will always make it trade very cheap on valuation.

Disc: Not invested

Conglomerates always trade at a huge discount. Look cheap but they arent. Rain has three buisinesses with operations across geographies

They can never bring cash back to India from overseas as they have many subsidiries and it will be tax inefficient.

Developed markets hardly have growth. Such commodity businesses should be set up in low wage countries. So growth is much lower in Rain. Infact, in their Carbon Products, they have not expanded since many years. Equity is all about growth for me- they lack business opportunities. hence experimenting with resins as they never want to pay off debt.

Overall, complexity of business, lack of growth prospects and tax inefficiency will always lead to lower multiple. This is my view. I had bought the stock in 2016 and sold off in two years. Since then tracking it actively.

Rain sells its two Subsidiaries, RUTGERS Polymers Limited, Canada and Handy Chemicals (U.S.A.) Limited for an aggregate cash consideration of Rs. 6,374 Million

Market has liked this real initiative to repay debt, reinforcing their previous promise.

Quoting from their Announcement -

As part of its strategy to achieve sustainable growth, create value for all stakeholders and

reduce debt, the Company has decided to divest the stake in these two non-strategic subsidiary

companies, which are engaged in manufacturing and distribution of Polynaphthalene

Sulfonates, under Product-Group Naphthalene Derivates, in Advanced Materials business

segment.

The consideration received from the sale of above two subsidiaries will be utilized for

repayment of debt and other general corporate needs of the Company.

There is a paywall on the article. Below are the main highlights:

Deleveraging … Getting 9% of debt out for small part of business that contributes only 3% of current profits signals positive intent to pare down debt quicker.

Rising CPC and CTP prices which contribute to 2/3 of revenue augur well - CPC prices in China are up by 60% in past 6 months. However spreads rose by 35% only as raw material prices are also increasing. Analysts expect raw material supply to improve which would boost margins.

In Europe and the US Rain enjoys much higher margins than Chinese peers. -CTP prices are up by 30% in the past six months with stable margins. - Aluminium capacities worldwide are operating at multi-year high utilisations.

Analysts expect CY 21 EBITDA at 2500 cr . current company enterprise valuation is 4.8 times one year forward EBITDA compared to 11 times at its peak valuation in 2018 - given business prospects and ability to strengthen the balance sheet the stock is expected to continue its current price momentum.

I dont know if these are accurate, but have a look at this:

Graph indicates, Pet coke (6.5% sulphur). It’s not CPC is it?.. Pet Coke is the raw material to produce Calcined Pet Coke which has much less sulphur (I think).

The Indian prices of Pet Coke is at par with 2018 looks like.

I am not sure how these two prices from the 2 links correlate.