The company has faced headwinds in the last couple of years. Street expectation of reducing debt in good times was not met. Instead the company went for new capacity in specialty chemical side. To reduce some extent of cyclicality. Let’s see how it plays out. Does remain a risky play due to high debt. As was in 2014.

I’m a fan of Dr Stock’s analysis, and avid reader of his blog…but after spending some time in the market I soon realized what Mohnish made more sense in terms of investing.

What Mohnish said repeatedly is that “great businesses and great investments are different things”, you need to decide whether you want to earn great returns or want to be an investor of great businesses.

Your mind shall have clarity.

I’m sharing this as not about Rain (Anyways I think Rain has a pathetic business model), but just sharing in general what I learned by being in the market (although I’m not an expert)

Looking at their cash flows, I’m least concerned about their debt levels(Anyways debt interest cost are low mostly 5-7%).

What I’m most concerned about is environmental issues they might face at different parts of the world.

Rain has a pathetic business model where they need some universal conditions to align exactly at the same time to get great revenues & OPM’s.

Steel industry shall do great ( Raw material for CTP comes from here)

Refineries shall do great ( Raw material for CPC comes from here)

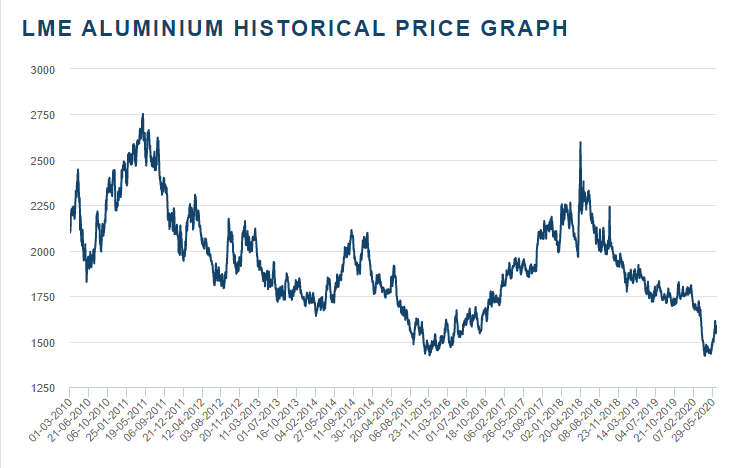

Aluminium industry shall do great ( End product is used there)

When all these 3 conditions satisfy stock will go over the roof.

probably by the time 2024-25 when you think about great future of the company, mostly I would be out of it.

Haha the way you started regards Rain has a pathetic business model I did not expect you to end with it being 20 percent of your portfolio . Do you see the environmental factors aligning and hence bought or are you waiting for an exit at higher levels?

Btw I’ve read that Rain is trying hard to leave the cyclical nature of their business by doing the following

Increasing margins of their chemical business(above 25 percent of revenue)

Increasing margins of cement business (approx 7 percent of their revenue)

And lastly for their main business they want to remove cyclicality by decreasing their dependence on the price fluctuations of GPC by using ACP Which they can produce on their own hence removing all cyclicality. I must confess I’m not and expert in this field so I’ve no idea if Itll work but I trust the management and I’m sure they want to leave cyclicality more than us. So if they do indeed do all of this then this a sleeping giant that the market just hasn’t noticed.

Disc: starting an SIP due to money being tied up in other investments

All the segments they work in are cyclical(CPC,CTP, Pathlic Anhydrous, Naptha, cement etc), I think what management is doing is more of a diversification.

"The company has also launched a new product called anhydrous carbon pellets (ACP), which is at par with the quality of GPC. The calcined version of ACP offers some unique advantages to anode producers like lower power consumption. Due to this advantage, some of the headwinds in the domestic CPC business can be compensated through ACP, which doesn’t faces challenges of import ban/quota and can be made from the refinery products available in India.

Hence, the company plans to commission two ACP plants at a total cost of USD 27 million, one each at India (capacity: 250,000 tonne) and another in the US (200,000 tonne). Its India ACP plant is expected to be commissioned by H2 2020, while the one in USA is expected to start operations in Q2 2020.

Initially, the company plans to sell a blend of ACP and CPC to aluminium smelters, which would offer better quality than a CPC-only product. In fact, the company has already imported the first shipment of ACP produced on a small-scale at a US pilot plant and the product acceptance would be tested in coming days."

Note that: These plants are on hold until next year due to Corona. So there LL still be some time where this stock could be range bound. I want to accumulate it over this year and next.

Thanks @jitenp for the reply. What are your views on the aluminium cycle both from demand perspective (auto, aerospace) and supply perspective (from China)?

It seems that almunium demand is going to be impacted severly with less air planes requirement by airlines and less auto/EV sales.

Company is able to generate enough cash flow even during the downturn, so its not going out of business for sure, that’s the reason for high allocation.

I saw this Youtube video where Mohnish is talking about Rain and Suntek.

Here’s what I feel about this company and also Mohnish’s holding POV:

Pros:

As Mohnish mentions, this company is owned and operated by a Maverik who will stop at nothing to optimize the operations, not only reducing, but converting dangerous waste SO2 emissions into useful byproducts which can be sold in the market. He will create ingenious in-house developed products like Anhydrous Carbon Pellets which remove dependence on GPC.

Mohnish also mentions something very fascinating about the Debt and its structure: The company has not put down any collateral for the loan, meaning, if the business fails and there is no debt repayment, the company does not really lose anything else from any of the other businesses. So Rain takes a giant 1B$ loan, tries to make a business work (which imo has 90% chances of working). If it does fail (10% chance), then the company loses revenue from this stream, but still has the rest of its businesses intact since there is no collateral for the loan.

The loan was taken by raising money via international bonds, getting Meryl lynch and Goldman to underwrite such huge bond issues demonstrates the power of the operating business for Rain.

The biggest pro which Mohnish referred to and which I can also agree with is the severe under-valuation of Rain. A company with Sales of 12k INR in a trough year is available at a market cap of 2600 crores. I think the only risk analysis to be done here is whether they can cover their interest payments. The fact that global interest rates are going down is good for Rain. They can potentially refinance their debt at even lower rates now (current rates are around 5-7% as someone else mentioned) which could reduce the debt risk even more. Current interest coverage ratio is 2.36 which seems like a medium comfortable place to be in. The TTM Operating Cash flow is 1,569 cr for a 2400 cr market cap company. This is what Mohnish refers to as a P/E of 1 buy.

Cons:

Mohnish, for all his bullishness on Rain had actually reduced his position in Rain. This does not necessarily mean that he does not believe in the company, merely that he found a better use for his money (better investment). His holding went down from 9.99% to 8.17% that it is now.

A lot of investors have said that “avoid companies that are too over-leveraged and you are going to be fine”. This is in general very sound advice. Is rain the exception that proves the rule? I don’t know.

As many others have said, Rain finds itself in a cyclical business. But one thing I have come to appreciate over the years is that almost all businesses are cyclical. Even banking, often touted as a secular growth story, is a cyclical business. Have a look at ICICI bank or axis bank earnings and you’ll see what I’m saying. Pharma? cyclical. All businesses where the input or the output is considered to be a commodity are cyclicals. That does not mean that they do not make for good investments. Having said that, would I hold Rain for 10 years? probably not.

All in all I would urge folks to go over Mohnish’s interview as well as other informative valuepickr threads such as the ART of valuation and Towards a capital allocation framework. Rain industries in my mind is a Type B business with great management and debt risks that has high probability of returning 5-6x the capital (at least) in 2 years. That is the way I would treat it.

Note: The management seems to try and convert it into a Type A business with increasing value added products, and so forth.

Disc: Not invested yet, but plan to add a small 5% position over next few months, specially post Q2 results (rain industries creates its AR aligned with calendar years) where revenue and profits would fall dramatically.

He has distributed his holdings into more funds so he hasn’t reduced it but moved some of them to other funds[Dhandho funds] resulting in less than 1% holding in those funds and hence not coming in shareholding pattern.

Thanks for the clarification, I wasn’t aware about this can you please provide some trustworthy reporting of this so that I can modify my original post?

Also is there a way to track dhando funds holdings over time? For his pabrai funds, I utilize this website called trendlyne.com to find current holdings and historic levels over the past.

Ok but if dhando funds holds less than 1% then there has been some trimming in the position since pabrai funds holds 8.17% and he started off with 9.9%. is that not correct?

I don’t think he was at 9.99 to be exact. Probably at 9.61% if i remember correctly. There might be minor differences here and there but I won’t worry about that too much.

Hi, I was looking at Rain Industries on Screener. Company has market cap of 2556 cr. But it has operating profit of 1569 cr and net profit of 429 cr. Interestingly Cash and equivalent is 1169 cr. It means company is available at huge discount with Price to book value of 0.5. What do you think about valuation and risk apart from Aluminum price not going up in near future?

I think interestingly you missed the debt part of company.

No doubt other points are correct. But I feel you should check finance costs and repayments coming up till 2025.