Sahil smaller steel companies disappeared in last bust post GFC in 2008. IFs are relics of past and I don’t think anyone I know is keen on putting it. EAF is the future.

9 Likes

There were some interesting case studies from Harvard Business School with regard to Induction Furnaces/EAF (called mini mills) vs traditional blast furnaces. By recycling scrap instead of the traditional BF steel making process, mini mills are able to ably compete in low grade steel applications at a fraction of the capex of blast furnaces. In addition, they are also far more environmentally friendly since use of coal is far lower since you are just using the same carbon instead of creating new carbon via coke. My guess is, with climate change on everybodys agenda now, the share of IFs/EAFs will continue to go up with time; especially in developing economies. Of course, a large outlier is China whose 90% capacity installed of steel is via the Blast Furnace route and who accounts for 50% of the worlds production. Hoping India does not follow the same route.

I would add 2 further levers:

4) Increasing share of exports: as a country we have an absolute advantage with regard to quality of quartz. The company is trying hard to open up export markets in Africa, Bangladesh, etc where a large portion of steelmaking capacity will come via the IF route due to capital constraints.

5) Targetting adjacencies: You touched upon these; but ramming mass for the foundry market (which the company seems to be targetting now) and future opportunities in anything that uses a furnace process: ceramics, glass, etc.

3 Likes

One of the key unknowns about this co is how the induction furnace route has been performing over the years. Whether the capacities are growing or not? Is induction furnace dying or growing?

Luckily. there seems to be an association for induction furnaces called:

https://www.aaiifa.org/

They publish a monthly newsletter. news letters are accessible here:

https://www.aaiifa.org/newsletter-2022.php

Few key takeaways from 2022 news letters that i read:

- Induction Furnace industry has been contributing very significantly in the overall production of steel in

the country, both in quantitative terms and as percentage of total steel production. - Crude steel production through induction Furnace route has been continuously increasing from about 4.3 MT (16%) to 22.6 MT (32%) in 2010-11 and finally to 33 MT (30%) in 2019-20.

- Contribution of the Induction Furnace sector is likely to be significant in years to come in making available quality steel at competitive price to the consumers in different geographical locations in

the country. - Since, it has a number of advantages such as low investment cost, land intensive as compared to

integrated steel producer, agility to produce various profiles of steel within a short time span, low operating Cost, providing greater opportunity of employment in rural areas to prevent unnecessary migration of people towards Metropolitan city etc., Moreover, the main advantage of the

induction furnace is a clean, energy-efficient and well-controllable melting process compared to

most other means of metal melting. Only air pollution occurs and no water or noise pollution

takes place in induction furnace, therefore, a special thrust is required to be given to look in to the barriers - Unlike other large steel producers, the Indian steel industry is also characterized by the presence of a large number of small and medium steel producers who utilize sponge iron, melting scrap and non-coking coal (EAF/IF route) for steelmaking. There are 285 sponge iron producers that use iron ore/ pellets and non-coking coal/gas providing feedstock for steel production; 39 electric arc furnaces & 858 induction furnaces that use sponge iron and/or melting scrap to produce semi-finished steel

- It is estimated that present demand for scrap is around 30MT which translates to roughly 20-25%

scrap usage overall. Since about 55% steel is produced through EAF and IF, this usage is low. The scrap usage is low due to no availability of quality scrap and high-power tariff because of which some

hot metal is used in EAF also. The scrap requirement as worked out is 65MT in 2030-31. This will work out to 22% scrap usage overall. Scrap arising within steel industry (domestic scrap) could be around 25MT. Hence, 40MT has to be made available through collection and recycling and imports.

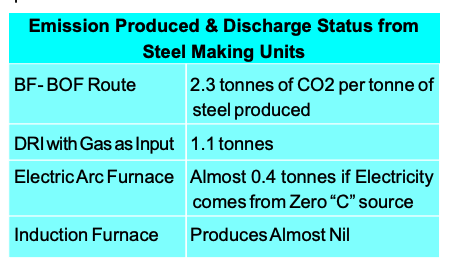

This clearly shows us the better environmental nature of IF & EAF steel making route.

8. The iron and steel industry is responsible for 11% of global carbon dioxide (CO2) emissions and will need to change rapidly to align with the world’s climate goals Steel production from induction furnace saves about 62% of the energy compared to the conventional steel making units significantly reducing carbon dioxide emissions.

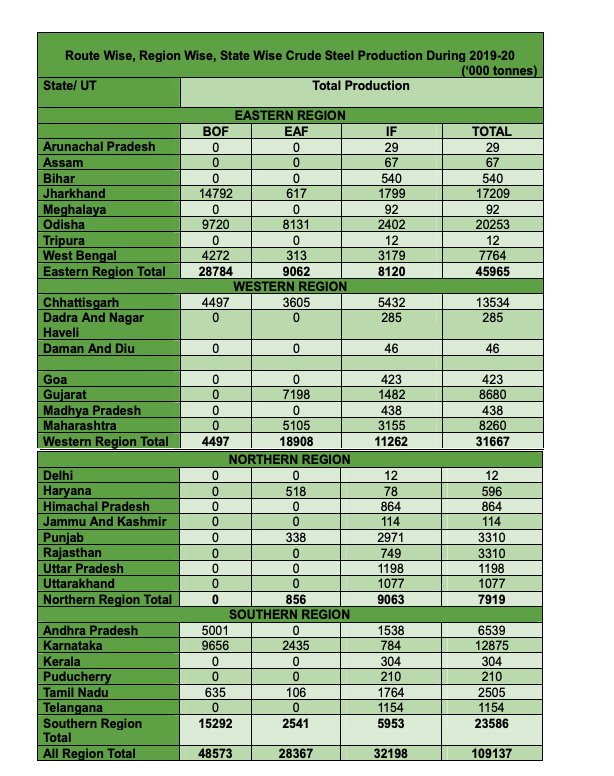

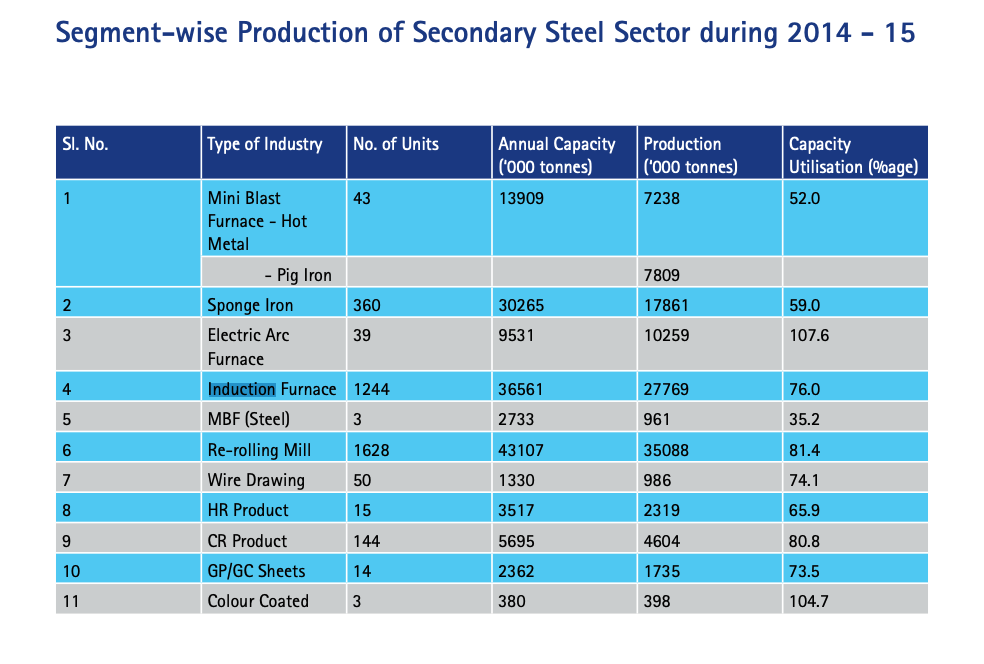

9. Detailed breakdown of IF steel production by region & state:

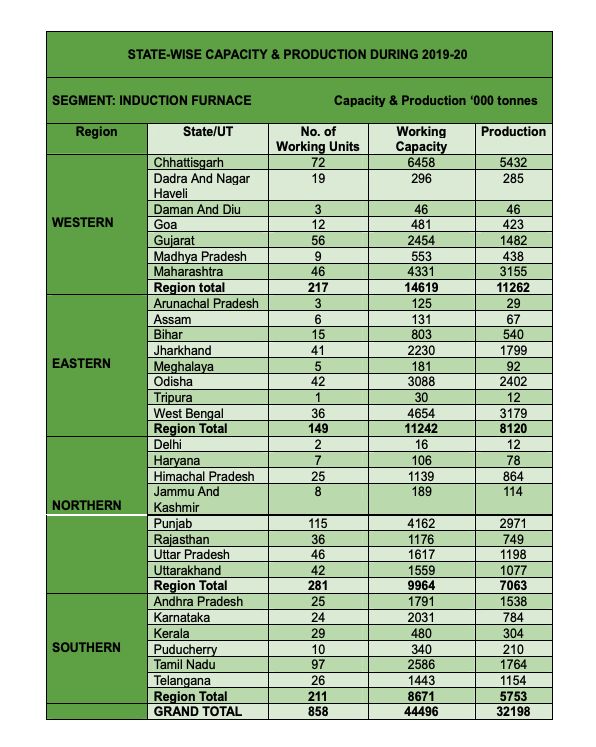

10. Detailed IF capacity utilisation:

Here are some other interesting stats from ficci steel report:

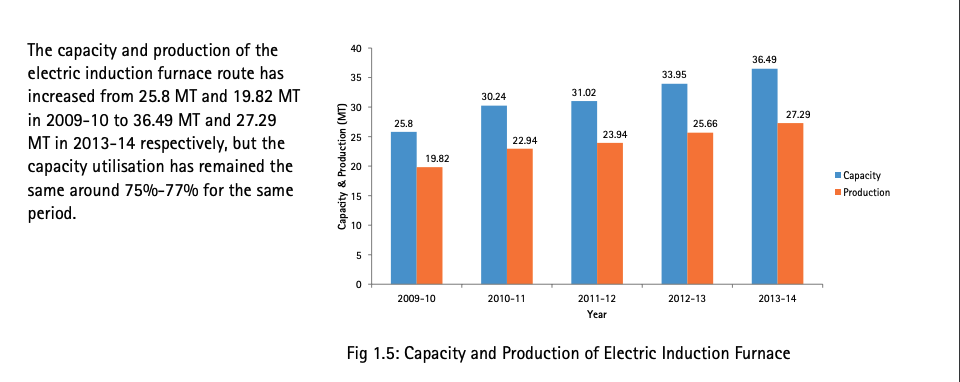

- Electric induction furnace capacity & production:

- capacity & production in FY15 (so that we can contrast with 2020 numbers in table above)

One can watch this 4 hour annual national conference of all indian induction furnace association as well if one is so inclined:

Disc: Invested, biased

4 Likes

Sahil bhai all these things may not be the reasons for Nemish shah and other prominent name to make entry to it. The reason could be its capability of producing high purity Silica quartz to be used in specialized glass manufacturing and solar cell wafer’s raw material. If we can relate its R&D effort and other commentary by management to these assumption then this can become big.

Disc: No holding just observing

1 Like

Raghav annual report came out today.

I have made some notes in a sheet format tried to categorize each point as being important for

X:Y:Z

where X: short term, medium term, long term

Y: period: p: present, pa: past, f: future

Z: biz: general business details, tg: topline growth, mo: moats, om: operating margins, tam: total addressable market

| page in pdf | metadata (timeline:tense:classification) | Key Insight |

|---|---|---|

| 4 | lt:p:mo | commenced business with a product that was considered a low-value-addition, geographically restricted commodity. Our relentless r&d efforts culminated in customised products & better processes. |

| 4 | lt:f:tg | Whether by developing new, value-added products for non-steel applications like foundries, etc. to expanding capacities to exploring newer markets and strengthening footprint in global markets |

| 5 | lt:p:mo | largest silica ramming mass producer in the world. We are a Jaipur-based company engaged in the production of highest quality silica ramming mass |

| 5 | lt:p:ca | 180000 MTPA production capacity on Mar-31 2022. 108000 MTPA capaciy to be added in FY23. Total proposed capacity: 288000 MTPA |

| 6 | lt:p:mo | Plant located in Newai (Raj), home to one of the densest quartz in the world, which is the primary raw material.Advanced technology with best-in-class production processes, operates the world’s only automated plant with VSI-based crushing process which provides customized product delivery capabilities |

| 10 | mt:pa:tg | Our exports grew 61.6% compared to the previous year, despite the global container crisis, sea freight challenges, and political instability. Our on-time deliveries and product quality spoke for itself and soon we began to receive enquiries from other clients too |

| 10 | lt:f:tg | Our high-value ramming mass for foundries has seen green shoots of acceptance in the market. We are increasing penetration in non-steel markets such as foundries, quartz slab, and other refractory products. This, I believe, will result in huge business growth and profitability |

| 12 | lt:f:tg | The new plant is expected to commence trial production by October 2022, which is in line with the project schedule. |

| 13 | lt:f:om | Further, we are also eyeing opportunities in segments beyond steel and have started developing products for foundry and quartz slab markets. These products, I believe, attract significantly higher margins and profitability |

| 14 | lt:p:tg | exports: 4500 MT in fy18, 7800 MT in FY19, 13000 MT in FY20, 16500 MT in fy21, 26600 in FY22 |

| 17 | lt:f:tg | Our unique advantage is at the heart of our increasing market share as customers perceive our product as a value enhancer when they consider its holistic cost-effectiveness |

| 17 | lt:p:mo | Latest automation technology with the state-of-the-art production process. Ability to provide customized products to end-user for maxium productivity. |

| 17 | lt:p:mo | We have an in-house research and development laboratory, which is the only one government-approved facility available in India. Through this lab, we assess specific requirements of our clients and develop customised ramming mass solutions, test and offer them to customers |

| 18 | lt:p:mo | Why customers use rpel : Increase in the sustainability of ramming mass in Induction Furnace (IF), as it can take a higher number of heating cycles (25% higher than conventional). It can offer sufficient heat with a lower proportion of scrap in total raw material resulting in a decrease in the overall cost of raw material. It reduces the peak electrical load demand by 25% as the number of start-ups are less compared to conventional ramming mass |

| 18 | lt:p:mo | Our customer relationships have been established over a period of time as a result of proper client handling and providing quality products. |

| 19 | lt:p:tam | Total domestic silica ramming mass demand stood at around 2034 KT for FY 2021-22. 70% comes from steel. 6% ceramics, 7% cement, 5% glass, 4% chemicals, 3% non ferrous metals. the weighted average demand for silica ramming mass in different industries is expected to grow at a CAGR of around 5-5.5% over the next 5 years |

| 20 | lt:f:tg | We are looking to penetrate the foundry and quartz processing markets. We are also developing certain high value-added refractory items like tundish board, castables, etc. evolving from our expertise in furnace operations |

| 23 | lt:p:biz | Ramming mass is created by mixing powder and granules sourced from crushing of quartz stone (quartzite) and boron oxide. This mixture has strong thermal stability, corrosion resistance and wear resistance, making it ideal for downstream use in coreless induction furnaces and for melting scrap. Ramming mass is used as for lining of induction surface. According to the Ministry of Steel, India produces 33% of its steel through the induction furnace route. |

| 23 | lt:p:biz | The average silica ramming mass consumption per tonne of steel production is estimated at 28-30 Kg. Although the steel industry is cyclical, ramming mass business is not cyclical because it is a low-cost item. However, ramming mass plays a crucial role in the steel manufacturing process |

| 23 | lt:p:mo | The silica ramming mass industry is highly unorganised, and is spread across central and north India, with large production plants located in these geographies with an average plant capacity of 10KTPA and 15 KTPA respectively. |

| 23 | lt:f:tam | Demand for silica Ramming mass 2118 KT in fy23, supply 2070 KT, 2233 in fy24, supply 2157, 2354 KT in fy25, supply 2248 KT. |

| 23 | lt:p:tg | ramming mass exports from india have been growing at CAGR of 26%. 21 KT exports in FY20. This means RPEL did 66% of exports in FY20 from india.majority of these exports go to the Middle East, South Asia, Africa and South America owing to rapid infrastructure developments in these region. |

| 25 | lt:p:om | Worked towards developing higher value-added products which yield significantly higher margin. Higher contribution from high margin products aids business profitability and gives an edge over competition |

| 25 | lt:p:tg | In 2021-22 the Company earned 41.06% revenues from export sales, thereby insulating business revenue to some extent from fluctuations in the Indian economy |

| 135 | lt:p:om | See note 31. The freight expenses are up 3x from 8cr to 24cr. I believe this has artificially deflated true profitability of the business which could come out more prominently in FY23 as freight rates normalize (not to pre-covid but compared to FY22 rates). True P/E for raghav could be closer to 18-20 rather than 28-30. We will learn with time how accurate my estimates are. |

Disclaimer: Invested, biased

18 Likes

Hi @sahil_vi , I want to understand how you see the business of ramming mass in comparison to graphite electrodes or refectories, as they are also very much depend on steel industry.

1 Like

What could be the reasons for doing the 100% expansion via a subsidiary? Why not within parent company itself?

1 Like

Tax benefits

Refer This Is How Manufacturers Can Grab 15% Corporate Tax Benefit, According To Experts

4 Likes

Thank you so much for research and post like this company thanks bro ।request you to post again if you visit plant and any other plant

Is this a cyclical industry in nature ? because it serve to steel industry.

THANK YOU SO MUCH।

2 Likes

This is going to be the next Rajratan Global Wire ![]()

Latest interview of mgmt

https://twitter.com/aditya942000/status/1589511639820562434?t=6S-K_eE8ji-1l5aztntdQw&s=19

6 Likes

Thank girjeev ji nice information share about rpel

2 Likes

Management interview https://twitter.com/ETNowSwadesh/status/1612326081398468608?s=20&t=N8gJsu1JZHAnlA7Fj0s2mA

2 Likes

mgmt interview on q4fy23 result and outlook.

https://twitter.com/ETNOWlive/status/1650723676621533185?s=20

Disclosure: not invested

4 Likes

Hello,

I have been reading up on the Company. Had some Questions around the World Market Size here, Given the Company is going to largely focus on Exports, the Market Size becomes important to guage the Growth longevity.

I have run some calculations which says it is around 45000 Crores. Wanted to know if anyone has any views here.

3 Likes

The market size is big enough for them to grow for coming many years. Even they have market share to gain in India too.

Q1 results are not so good…

1 Like

Those who are saying this quarter result is bad.

Also the new plant commissioned has gone live. so operating leverage is on the cards going ahead.

1 Like

Massive jump in share prices today! Any specific reason for the same?

1 Like