Here i have tried to compile important data from past Annual Reports. ARs are more than enough to know about the sector and company. I have used bold and underlined fonts to attract the attention on specified points which were told in past and management walked the talk. Market for their legacy product that is Ramming mass have been more than doubled in past 4 years but company could not double its revenue though they have captured market but still a lot of scope present. I like the vision of the management and how have they planned it beforehand there could have been some timing issue in execution or due to pandemic and all but what i have observed that they have not changed the path.

A commodity company making high 20+ margin is superb and making commodity in to product is phenomenon. Product is in demand and they have expanded multiple times and expanded capacity exponentially is also commendable. Their focus on new revenue stream that too high margin low volume and backed by solid research will be gamechanger. Significant part of their revenue was from steel trading but they have closed it and focused on core, this is also a sign of a good management.

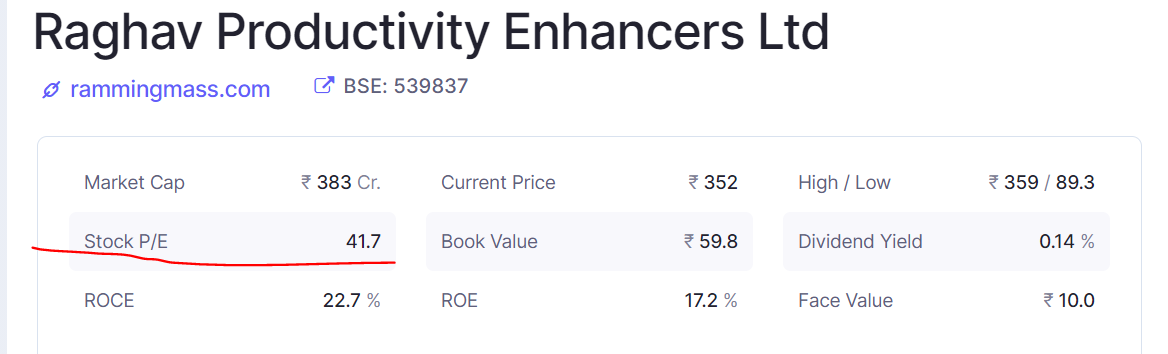

All Of it are from Annual Report

The quality of AR written is great no need to dig more just reads their AR and u will get most of their plans and activity.

UNDERSTANDING QUARTZ POWDER

Quartz is a silica-based mineral extracted as large stones from mines. These stones are processed into various sizes having different silica purity content. Quartz powder with a silica purity of 96-98% is called ramming mass and is widely used in the steel industry as a refractory material in lining of the inner surface of coreless induction furnaces for melting scrap, sponge and pig iron. Quartz powder with higher silica purity is used in glass and ceramics industries, while quartz powder with highest purity is used in the manufacture of ophthalmic lens and solar industry.

AR FY15-16

Fixed asset section mentions about Three car AUDI (2012) , Hundai(2015) and Mercdeze(2016)

AR FY16-17

The quality of AR written is great no need to dig more just reads their AR and u will get most of their plans and activity.

RAGHAV RAMMING MASS LIMITED has emerged as a productivity enhancement partner for the steel industry, and is moving towards being the same for glass and ceramics industry. The premium quality quartz powder, including its flagship quartz ramming mass, adds a significant value to its users with distinct and clearly visible enhancement in Return on Investment (ROI) for its customers. Compared to other players with a “commodity mindset”, RRML provides differentiated solutions with its bespoke products, each customized and tailor-made for specific industry and application need. RRML is changing its name and is revamping its brand identity to reflect its focus and philosophy that is aligned with this positioning as the preferred and recognized PRODUCTIVITY ENHANCEMENT PARTNER that delivers.

Company is moving up the Quartz Powder value chain, displaying formidable thought-leadership. It is all set to expand its presence into newer industries and applications.

Strong Export Potential

The Induction Furnace process is widely used in countries of the Middle East and Africa, which present a promising opportunity for export of Ramming Mass.

GST to benefit organized players The implementation of GST is expected to benefit the organized players in the Ramming Mass

only one in India and amongst the very few in the world to use state-of-the-art automated technology along with ball milling process for ramming mass production. Recognized for the quality of its products that has a proven capability of enhancing steel manufacturing productivity, the Company is amongst the most trusted players globally in this field. The Company is taking ahead this expertise by extending its product portfolio to High Purity Quartz Powder (HPQ) and Tundish Boards.

Steel Ramming mass market size- 450 crore in 2015

70% Unorganized in 2015

scaling capacities

In January 2015, we operationalized our Newai plant which enabled us to scale our ramming mass production capacity from a mere 15,000 TPA to 144,000 TPA compared. With nearly 11 times growth, our total production capacity stands at 159,000 TPA, which is nearly one-third of the industry’s demand of 5,65,640 TPA in 2015. This massive capacity addition shall allow us to capitalise on the rising demand, cater to untapped demand from eastern states and grab market share from the unorganized sector.

In addition to this, in 2016, we again made investments towards adding new manufacturing facilities (High Purity Quartz Powder and Tundish Boards) that shall enable us to diversify our offerings to new industry while enhancing our revenues and profitability margins. These units are likely to get operationalized in August 2017

High Purity Quartz Powder (HPQ) 72,000 MTPA Artificial marble, glass and ceramics

Tundish boards 7,200 MTPA Steel industry

The total consumption of quartz powder in other industries is estimated at ~20% of the total consumption. Accordingly, the size of total domestic quartz powder industry in India is estimated at ` 13.2bn

Expenditure on R & D: Nil

AR FY17-18

The implementation of GST has been a game changer for the ramming mass industry, especially for organised players like us. We are convinced it will unlock massive and multiple opportunities. It will enable us to reduce pricing gap with the unorganized players by taking advantage of tax credits, which in turn will enhance our competitiveness. Besides, it will make the entire nation one single market and thus bring in more efficiency in logistics movement across our pan-India markets. This pricing and logistics movement advantage will multiply our overall proposition manifold.

We have increased market share, expanded into newer markets of east and south, won new customers, increased our exports as well as launched new products.

During the year, many ramming mass manufacturers had to shut down due to environmental issues. I would like to emphasis here that our plant is fully compliant to all environmental norms and is regarded as a model plant in the industry

Volume 46188 MT to 71242 MT

The freight cost is very high from Jaipur to the eastern region, and increased our price by as much as 60 per cent. Yet, in spite of substantially higher price, our products are preferred by customers due to the extra-ordinary results and productivity-enhancement benefits accruing to customers. Using RPEL products and solutions, customers are getting more than 50 per cent extra lining life and even after factoring in procurement at 60 per cent higher cost, our ramming mass is not just free for them but adds significantly to their profitability.

Our total operational capacity is 1,20,000 tonnes. In the last quarter of FY2018, we reached 80% capacity utilisation. With rising demand and growth in the ramming mass industry, we are also utilizing our granules infrastructure to produce ramming mass. This increases our capacity by another 60,000 tonnes annually. In addition, we also have scope for brownfield expansion in the future at the same site located at Newai.

We are using our free cash flows to retire debts and are committed to become debt-free in FY2019. We are extremely prudent in our working capital allocation, ensuring every decision is based on the right balance of generating both growth as well as ROI. Our focus is not just growth at any cost, but delivering profitable and quality growth, and keep improving the quality of earnings. We also changed our product name from ramming mass to Induction Lining Solutions to showcase the shift from product to solutions. Our in-house R&D Centre has been recognised by Department of Scientific and Industrial Research (DSIR) under the Ministry of Science and Technology of the Government of India. This makes us one of the only 1,800 companies in India having this recognition and the only one in our industry.

We have hired industry-leading consultants to guide us in our continuous effort to institutionalize excellence. Data-scientists are helping with high-end data analytics to enable deeper insights that will sharpen our strategy. We have launched an organization-wide ESOP scheme to retain and attract top talent**.(could not see any ESOPs Till FY 19-20)**

Price of Premix Ramming mass has been constant for the last 3 years – ` 5,500

We have increased our exports by 65% from 2017 to 7% of our total sales. And we aim to take exports to 15-20% of our total revenue in next 3 years.

Case Study on a 25 MT Induction Furnace Getting 25% More Heats.

Total Savings by using our ramming mass are more than ` 2.5 Crores per annum for 25 MT Induction Furnance

Buying from licenses mines also ensures a steady supply of quality raw materials. As we expand our presence further in east, south and central Indian markets, we will continue to de-risk our sales.

The Company has started new unit at Newai for production of Tundish Board which is made from waste generated from the Ramming mass plant as well as accessories for tundish board - garpack, garseal, radex, sleve nozzle filing compound and other-items used in Continuous Casting in Steel Plants. Our Company has received official recognition to the In-house Research and Development (R&D) from Department of Scientific and Industrial Research (DSIR), Ministry of Science and Technology, Government of India, The Company’s vision is to maintain leadership through consistent quality improvements in manufacturing of Silica Ramming mass and developing more quartz variants.

-

Refractory product manufacturing services 74.52 % of revenue

-

Trading of Steels products 25.48% of revenue

So company is also doing steel trading. That can also be seen from account notes for revenue breakup.

RESEARCH & DEVELOPMENT: a) Specific areas in which R & D is proposed to be carried out by the Company: The R & D activities of the Company have been directed towards improvement in the quality of ramming mass and tundish board, as well as to develop new products using quartz powder which is used in various industries like glass, ceramics, solar, semi-conductor etc. Continuous efforts have been made to achieve our goals.

b) Benefits derived: By virtue of our R & D activities, the Company has been able to improve the quality of its products, cost reduction, increased customer satisfaction, reduction of wastage and has improved environmental conditions, The recognition of our in-house R&D Centre is due to the tremendous efforts we have made by continuously investing in R&D and has significantly improved the quality which provides ‘MORE WITH LESS’ i.e. Steel Plants consume less ramming mass and get more productivity of steel by using our premium product which is developed through state-of-the-art technology.

c) Future plan of action: Our efforts are focused towards further increasing the quality and efficiency of making Ramming Mass & Tundish board as well as creating a viable process of making quartz powder for glass & ceramics industry.

Expenditure on R & D:

(a) Capital (if any) : ` 636.63 Lacs

(b) Recurring R&D Expenditure : ` 27.63 Lacs

© Total R & D Expenditure as a Percentage of total turnover : 13.96%

The number of permanent employees on the rolls of the company as on 31st March 2018: 74

AR FY18-19

Today, we are leading from the front by being the only large-scale and organised ramming mass player in India. We have successfully shifted the mindset for Ramming Mass from “commodity-driven” to “solution-driven”, and have established ourselves as a recognised brand.

2.16Lakh Metric Tonnes Per Annum Our Production Capacity

10% Largest Market Share in the Industry

51% growth107575 MT only Ramming Mass given in AR

Export (MT)

FY 15-16 915

FY16-17 2,765

FY17-18 4,540

FY18-19 7,843

Our value proposition, strong and established brand and excellent customer service is helping us build new customers – locally and globally. By capturing India’s Eastern market, we are being less dependent on a specific geography. Besides catering to pan-India steel manufacturers, we export to over 20 countries worldwide.

VISION or ACTION PLAN

FY18-19 Forayed into the foundry industry

FY19-20 Venturing into exports in the global foundry industry

FY 20-21 Plans to foray into high purity quartz manufacturing

10 Billion Size of ramming mass market in India in 2019 market more than doubled in 4 years and also market share increased.

We have moved our focus from low-value to high-value manufacturing. We are achieving this by catering to large and quality-conscious players manufacturing with high value orders.

gradually we have exited completely from trading owing to the lack of any value-add from this business.

We are exploring the significant and ever-growing opportunities in the foundry segment. India has one of the world’s largest foundry industry, most of whom are extremely quality conscious. With our technical collaboration with JWK AB Sweden, we have developed a product which is suitable for the foundry industry.

The collaboration has equipped us to create the material best suited for use in Small Induction Furnaces, Melting Cast Iron and SG Iron for production of foundry products. The material enables these furnaces get maximum life, better than they were getting through imported Ramming Mass from Sweden, USA and Spain, manufactured by large refractory companies. Import substitute

SL No Name & Description of main products/services NIC Code of the Product /service % to total turnover of the company

1 Refractory Product manufacturing services 74.52 %

2 Trading of Steel Products 25.48%

Expenditure on R & D:

(a) Capital (if any) : 0.00

(b) Recurring R&D Expenditure : ` 164.85 Lakhs

© Total R & D Expenditure as a Percentage of total turnover : 2.92%

The number of permanent employees on the rolls of the company as on 31st March 2019: 99

AR FY19-20

Energy Efficiency Award 2019 & Certificate of Recognition for being the world’s largest manufacturer of ramming mass by AIIFA

Asia’s Most Trusted Ramming Mass Brand

Best SME 2019 Award

RPEL increased its exports volume by 66.17% in 2019-20 ( Volume 13000MT so realization in export are almost double from Indian Market as revenue from export is 12 crore)

Over the last few years, RPEL made a decisive investment of FY17 to 20 10.52 crore in research & development

The Company marketed 130655 MT of ramming mass products during the year under review, a 20.67% growth over the previous year. (Though realization are down in domestic market From 4900 RS/MT to 4700 RS/MT calculated after subtracting export value and volume from calculation)

FY 20-21 Venturing into exports in the global foundry industry

RPEL is the only ramming mass Company in India to position itself as an all-India player

RPEL intends to broadbase its product portfolio. The Company intends to extend to the manufacture of foundry grade ramming mass, which enjoys higher realisations and could help reduce the Company’s risk from an excessive dependence on the induction furnace-centric steel sector

RPEL intends to manufacture high purity quartz powder used in the manufacture of artificial marble, a large addressable market.

RPEL intends to engage with global distribution partners who market products to steel companies the world over, strengthening its pan-global market access without proprietary investments

The Company is the largest ramming mass manufacturer in India, its installed capacity at least 50% higher than its nearest competitor.

20% minimum premium generated by the Raghav brand over competing alternatives, 2019-20

Refractory Product manufacturing services 100.00% So Stopped all other trading activity.

Expenditure on R&D:

(a) Capital (if any) : 0.00

(b) Recurring R&D Expenditure : 222.39 Lacs

© Total R & D Expenditure as a : 3.35% Percentage of total turnover

The number of permanent employees on the rolls of the company as on 31st March 2020: 108

Future plan of action: Our efforts are focused towards further increasing the quality and efficiency of making Ramming Mass & Tundish board as well as creating a viable process of making quartz powder for glass & ceramics industry

Disc: No holdings