new plant commissioned in July 24. 60% growth in capacity due to green filed. later there will be brownfield. I can see a clear cut way to growth. for last 4 quarters they were operating at peak capacity now growth will come bcz their products are very superior… I guess that’s the reason.

2 Likes

Presentation before AGM:

3 Likes

Anyone tracking the latest updates on this company - please shed your insights on this stock? Seems like solid consolidation in last 7 months and at support now technically.

From CRISIL Ratings report dated 30-Apr-2024:

- The group has established its position pan-India as a market leader in the ramming mass manufacturing segment, with superior product quality resulting in higher-than-average realizations.

- The group exports to over 30 countries with volume growth of 19 % in fiscal 2024

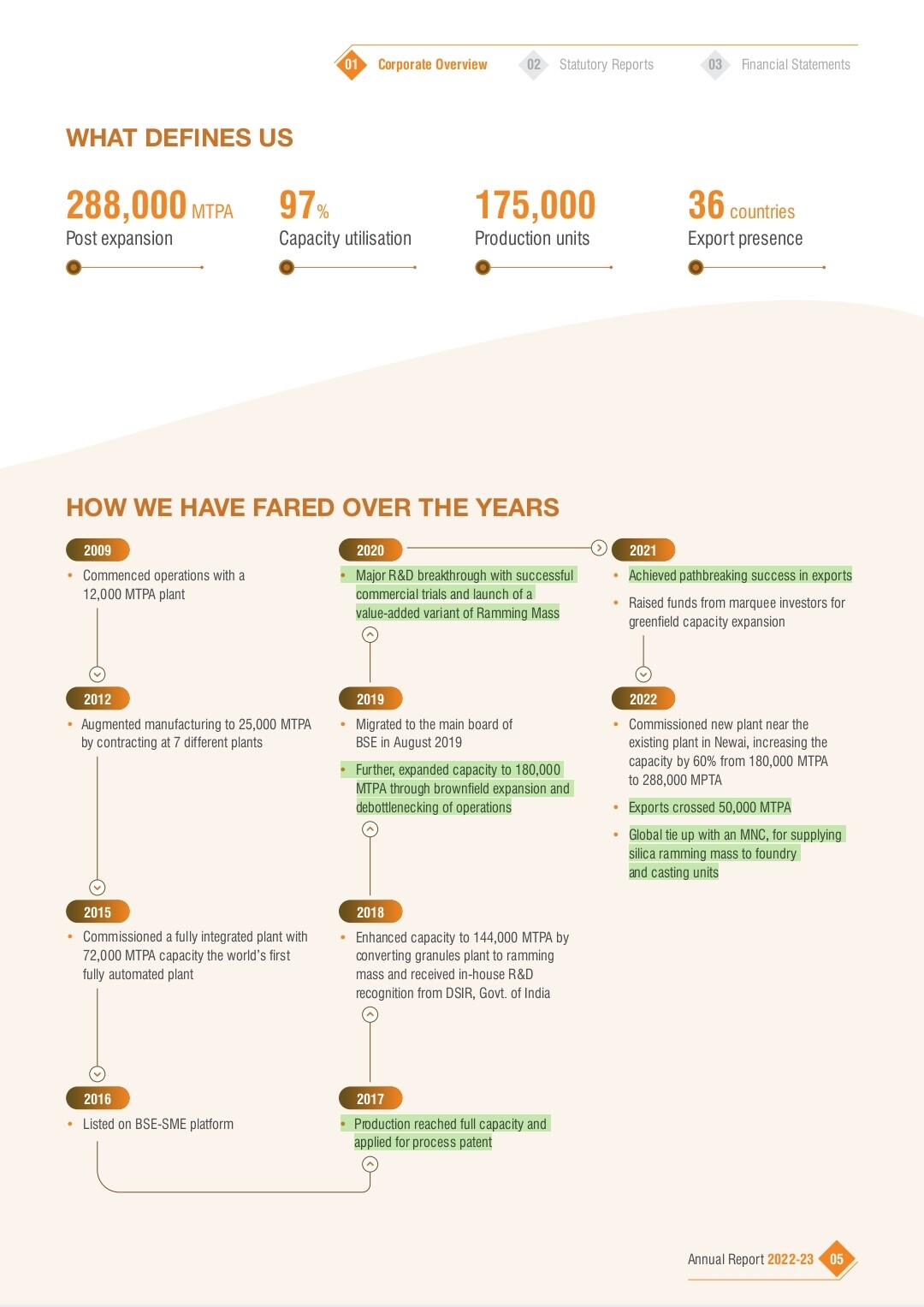

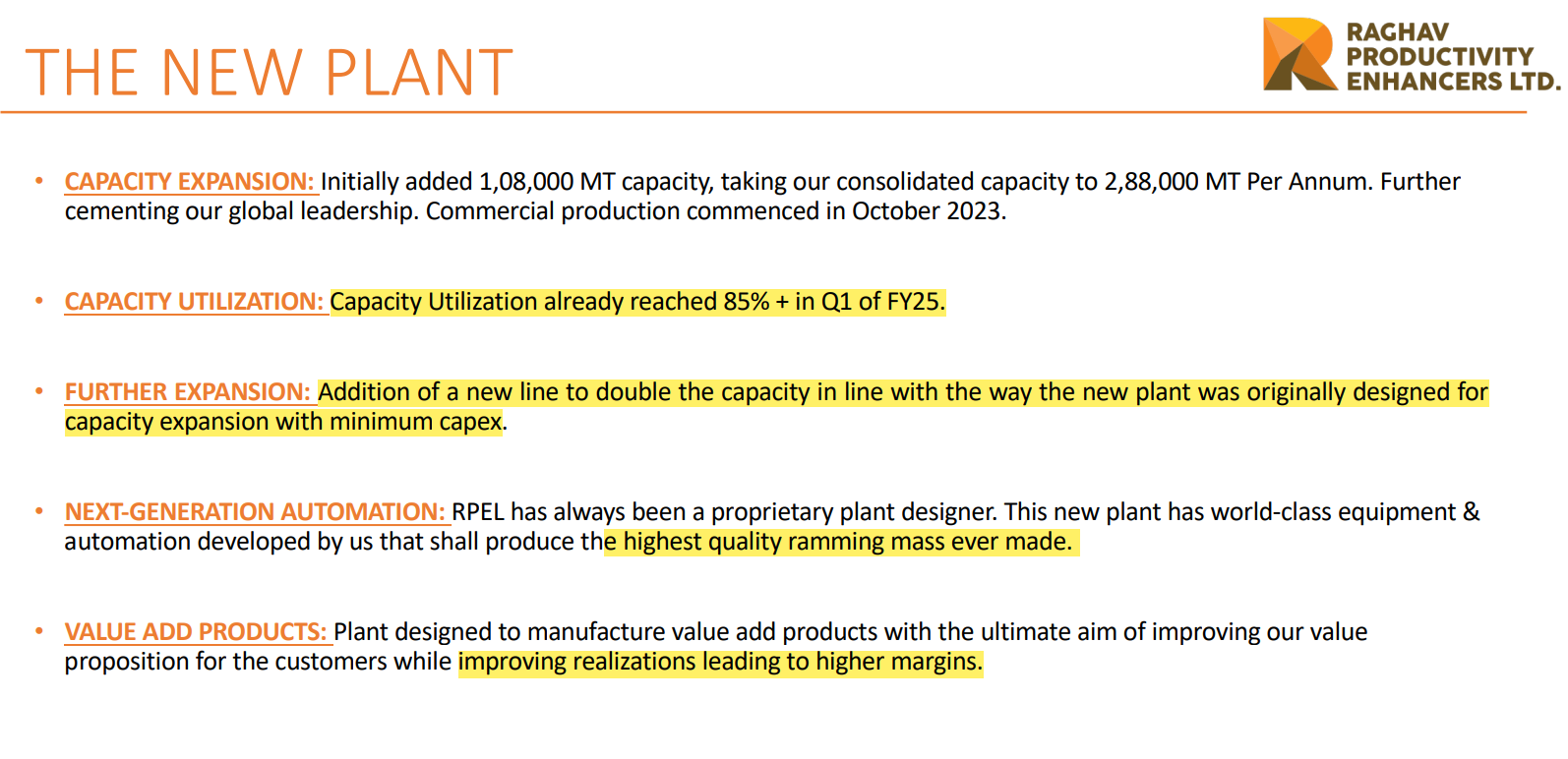

- The group expanded its production capacity to 2,88,000 MT per annum from 1,80,000 MT per annum in October 2023.

- Return on capital employed was estimated at 26 % in fiscal 2024 on the back of high economies of scale. Operating margin was also steady and is likely above 28-29 % in fiscal 2024

- Limited external debt

- No major capex expected over the medium term

- Despite expectation of volumetric growth of 5-6 % in fiscal 2024, turnover was estimated to be slightly lower at Rs 125-130 crore compared to Rs. 137.4 crore in fiscal 2023 due to lower freight revenue

- Competition from a large number of unorganized players in the industry

3 Likes

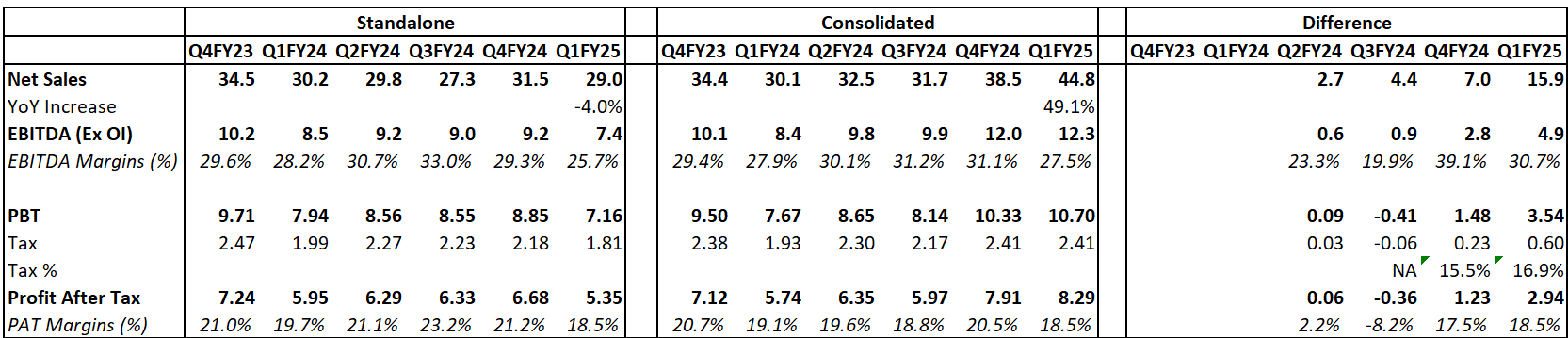

One thing which to be noted is that the new capex which they have done is under a 100% owned subsidiary. Although the difference can be because of other subsidiaries too, but the primary delta seems to be from the new plant which was commissioned in October 2023.

The fact is very well known that the new plant is very efficient in terms of production and also has better quality of ramming mass.

By comparing the numbers (consol (-) standalone), it might be seem like the new plant is doing very well! Q1 is typically a weaker qtr for the company, but still the new plant might be doing 30% EBITDA margins. I will be little skeptical to reach to conclusion very quickly that they might have done 39% EBITDA margins in Q4, but this is definitely interesting.

Happy to be corrected if this logic is flawed.

7 Likes

3 Likes

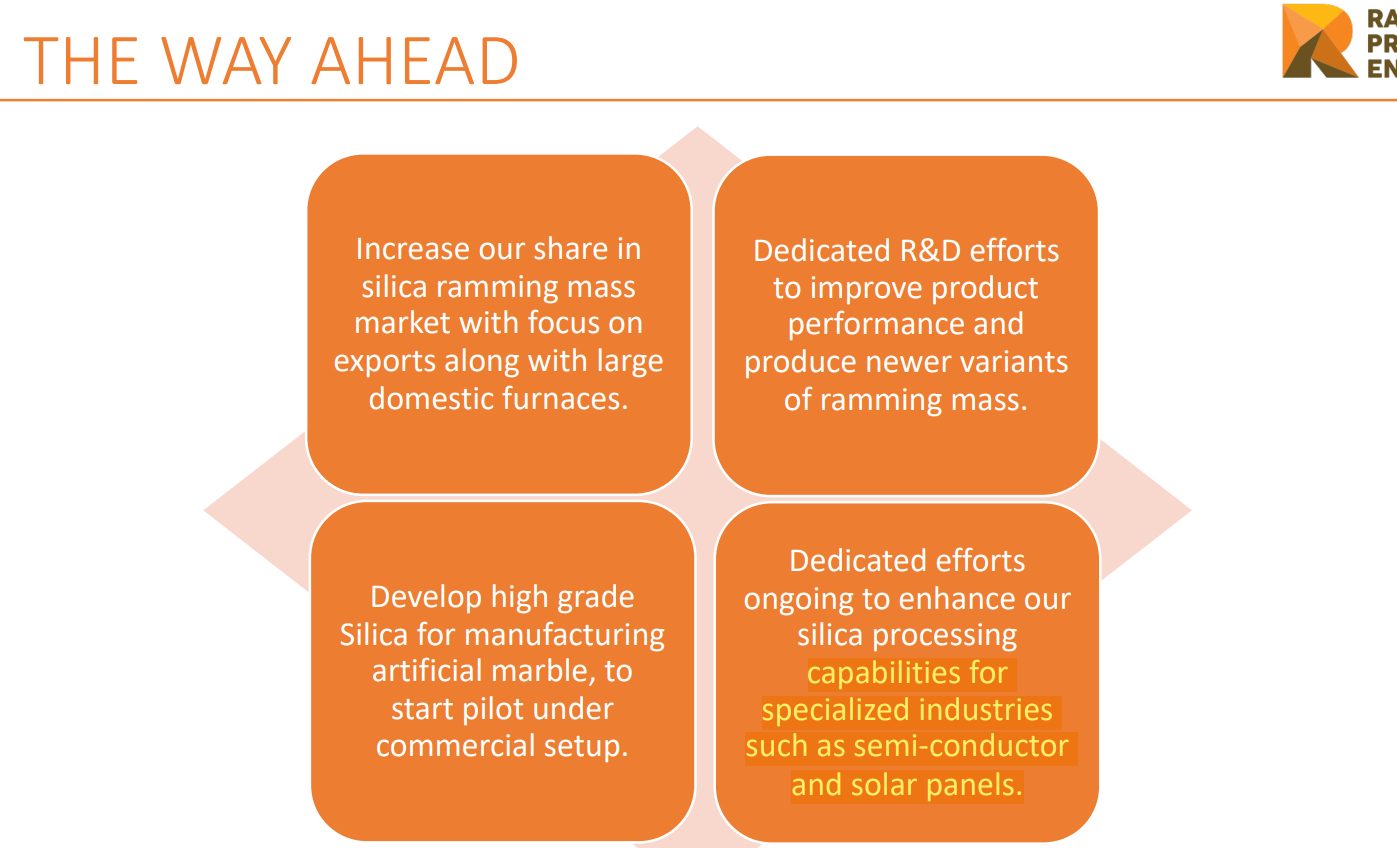

In a TV Interview with CNBC, Raghav Mentioned that ‘Artificial marble and Semi-conductors is some of the newer diversification company is looking at given they have access to one of the highest qualities of Silica in India’.

This info I believe was private before this, but mgmt has now said it over public forum and I believe this is the reason there was a pop of 15% on that day.

These are at only R&D stage as of now, there is no material developments as of now.

Rest of the interview was basically a summary of annual reports of last 2-3 yrs - same stuff nothing different.

6 Likes

Some data compilation I had done a while back…

IF vs EAF vs BF split (RPEL).xlsx (17.3 KB)

Disc - no holdings

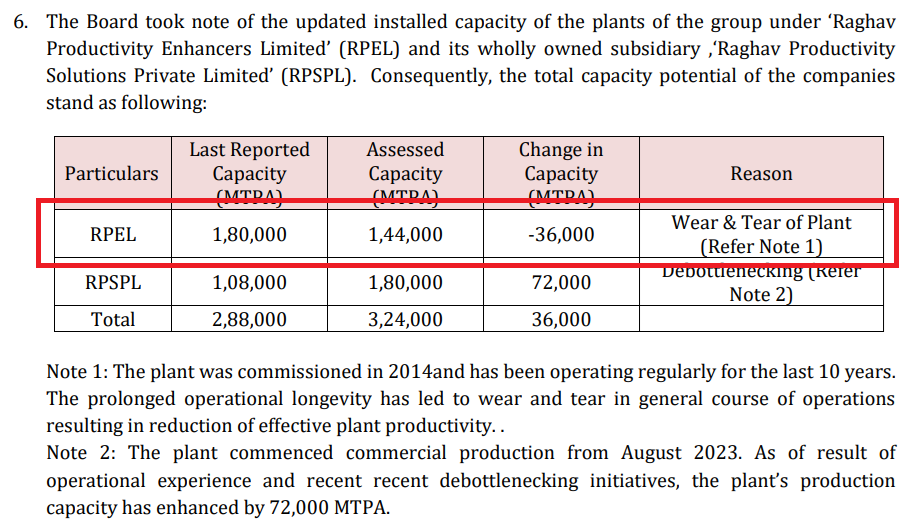

Plant capacity downgraded by 20 % due to wear & tear after just 10 years of operation - a rather strange kind of disclosure if only because I have not seen anyone else do it so far.

4 Likes

good point, a drop in 1 to 4% will be noticed but 20% drop and no action at all means, someone is not managing operations really well. and NOT reporting it to management in a way that requires materially significant disclosure.

4 Likes

Any idea of when the bonus shares will be credited?

Raghav Productivity Enhancers ended the year FY25 on a strong note, with sales growing 50 % from Rs.133 crore in FY24 to Rs.200 crore in FY25. PBT increased 37 % and PAT increased 42 %. The new plant which had gone on stream during the year operated at a utilization of around 45 % while the old plant operated at nearly 95 to 100 %. There was a slight dip in the margins on account of an increase in raw material costs and higher freight. However, EBIDTA per MT was maintained at about Rs.2100 which the management says, is “in line with the company’s long term business model”. Cash flows remained strong with CFO jumping from Rs.20 crore to Rs.39 crore for the year. Balance Sheet remains debt free. The current capacity provides scope for another 50 % increase in EBIDTA I think, after which the company will need to hike capacities further. Q1 FY26 results were also strong with sales growing at 30 % and PBT up 39 %.

Though ramming mass is a refractory product, Raghav has consistently clocked significantly higher margins that the refractory majors.

Compared to the above, traditional refractory players have operated at 40 % range.

The reason for this may be that Raghav’s products are used in Induction Furnaces, which are primarily used by small and secondary steel plants, unlike the above two who cater to the Tatas & Jindals of the world and have higher bargaining power.

Higher margins allow surplus cash to be deployed for other purposes, and the management says efforts are on to improve performance of existing products and advancing silica processing capabilities to serve high-growth industries like semiconductors and engineered marbles. During the year RPEL secured a patent for silica ramming mass manufacturing process, a first globally.

The company is expanding into promising new sectors such as the foundry market within the refractory industry and exploring emerging industries where quartz is used, like engineered marble and semiconductors. These are even higher margin segments than the existing ones.

During FY25, the company appointed Mr. Bharat Tank as the new Sales President. Mr. Bharat is an industry veteran with more than 35 years of experience. I guess his focus would be growing the export markets, such as Europe where 40 % of steel is produced through the Induction Furnace route (where silica ramming mass is used).

No major capex was done during the year or is planned in near future as the capacity set up in FY24 awaits full utilization. However, de-bottlenecking and other enhancements increased capacity by another 90,000 MT.

India is the world’s second largest producer of quartz, and Rajasthan where the company’s plants are located is blessed with abundant quartzite reserves, which is the main raw material for silica ramming mass production. The company has long term arrangements with suppliers for its requirements and does not plan to integrate backwards by acquiring own mines. But given that freight is an important component of the company’s overall cost structure, I feel RPEL would benefit by setting up its next plant in South or East India. States like Andhra Pradesh & Tamil Nadu also have abundant quartz reserves and serving export markets would be easier from the South. A large part of the domestic market located in Eastern part of India would also be closer.

RPEL’s products are used in steel plants using the Induction Furnace (IF) route, which is the fastest growing segment within the steel industry. Steel production through the IF route is expected to grow by 7 % CAGR till 2028. In FY2024-25, Induction furnace contributed 38 % of India’s 145 MT total crude steel output, up from 32 % the year earlier. Last year, the entire growth of the steel industry came from the Induction Furnace route, says the management.

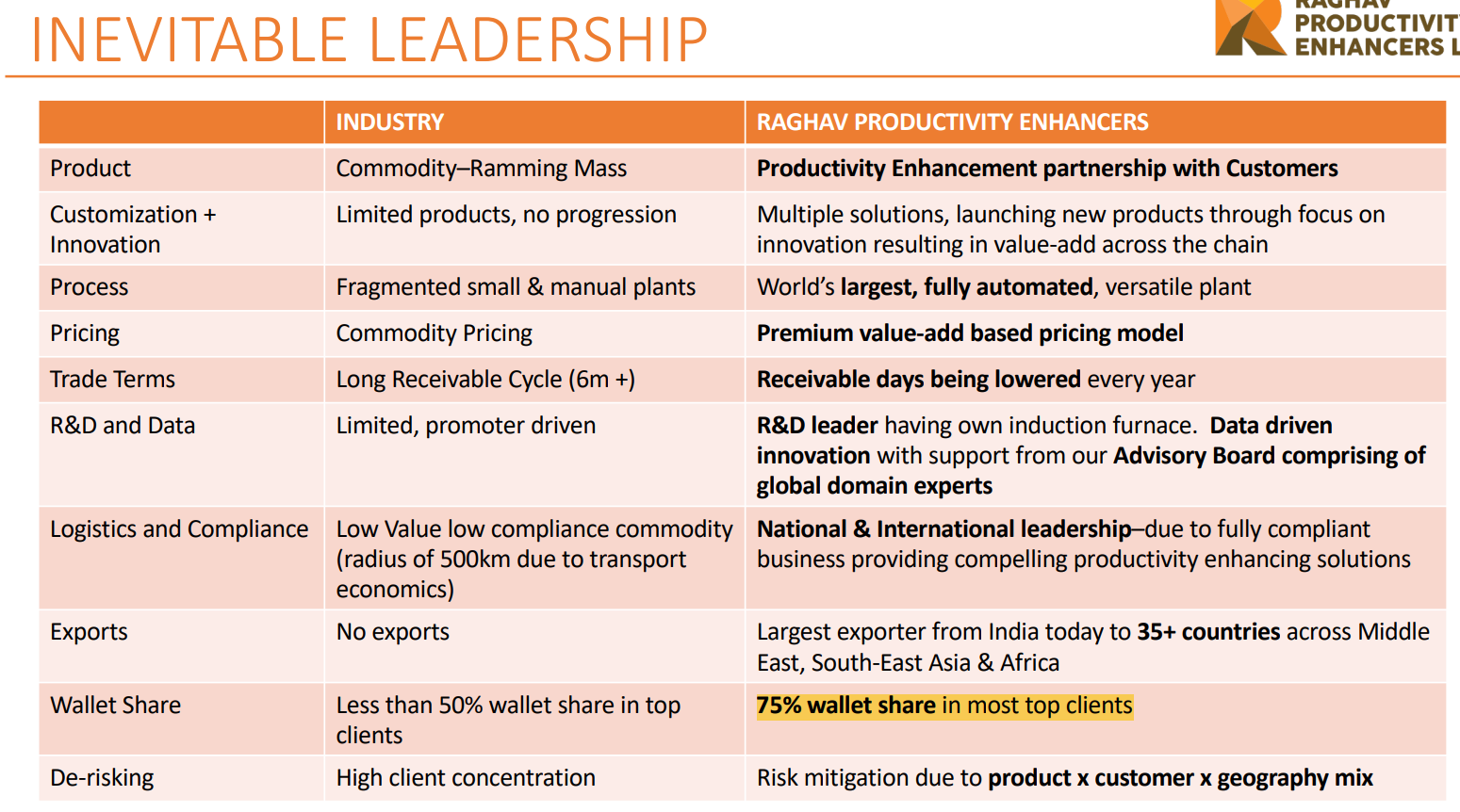

Approximately 30 kg of silica ramming mass is required for every ton of steel produced (via IF), and RPEL claims around 12 % market share of Indian market. This puts the domestic market size at around Rs.800 crore. This is small enough to keep the multinational majors out of the market, while providing growth opportunities to Raghav. But the real kicker can come if the company’s R&D leads to something concreate which expands the TAM significantly. At the AGM, the management said RPEL has 75 % wallet share of its top customers, and all (i.e. many of) their customers are adding capacities, which assures RPEL of steady “double digit” growth for the next few years.

In Quality Investing, one of the best investment books I have read, Lawrence Cunningham writes that the structure of a company’s industry is critical to its potential as a quality investment. Refractories lend themselves to such a favorable structure, as I have noted in multiple posts under the RHI Magnesita thread. It is often misunderstood as a commodity, but it neither displays the price volatility of commodities not their capital intensity. The cost of ramming mass is just 0.2 % of the cost of producing steel, but it plays a vital role in the production process. This is the moat the business has, and if your product works better than the competitors, the customers will happily pay a significant premium to buy from you. RPEL says it sells its products at a premium of 150 % in the domestic market and 2 to 4 times in the export market over rival producers, most of whom are from the unorganized sector.

(Disc: Holding)

11 Likes

Thanks for the detailed write-up.

This pretty much sums up the industry and the company alike.

Though, I’m studying a newly listed company Monolithisch India Ltd in the same business as RPEL albeit with much smaller capacity (growing too) but larger aspiration.

Any light you may throw on Monolithisch India Ltd?

2 Likes

Yes, I saw that Monoolithisch is in the same line of business as Raghav. I read its DRHP but haven’t gone beyond that. I think they would enjoy the same business characteristics what Raghav enjoys. They are located closer to India’s steel belt, which works well when it comes to being closer to the customer. On the other hand, Rajasthan is widely regarded as having India’s best quality Quartz reserves with high silicon dioxide content and low levels of impurities, so Raghav has an advantage in terms of raw material sourcing.

5 Likes

1 Like