The number 532.64 in your screenshot tallies with an item “Advance Taxes” in their FY 2020 AR. Page # 146

Some form of a prepaid tax exp perhaps?

The number 532.64 in your screenshot tallies with an item “Advance Taxes” in their FY 2020 AR. Page # 146

Some form of a prepaid tax exp perhaps?

That explains it!

I went back and searched all statements for last 10 years and tallied cash flow statements. So till 2017 they weren’t paying advance taxes (I am not really sure why, maybe some regime change). Till 2017 all cash flow statements were prepared with Profit Before Tax and then Tax paid was deducted from the CFO to arrive at Net CFO.

For 2018 they only paid less than 2 lakhs in advance taxes and CF statements changed to Profit After Tax with Direct Taxes being added back to CFO to arrive at Net CFO.

For 2019 and 2020 they paid significant advance taxes and as such they are being added back to CFO since these are technically advance payments to arrive at Net CFO.

The figures of 532.64 is advance tax paid in 2020 and 300.78 advance taxes paid in 2019.

I have also emailed the company just to be double sure of this logic. Will update if they come back with an answer, but I am sure its the advance tax treatment that’s been changed since 2018 onwards.

Email Sent to Investor Relations

Already discussed above.

The mgt. said that competitors of clients does not usually have same supplier. This means the way to grow is to increase wallet share of existing clients or enter new segments. While this may not matter to RACL now because of their small size, but what about the bigger players in the space? The reusability of process design in the industry must be low then (assuming peers in same segment have similar products). So the SKUs of bigger players must be huge then as they have to cater to many different segments as a constraint not as a diversification tactic to scale up. Will be glad if any senior member can corroborate this hypothesis.

Disc - Tracking position, likely to add

This point stands out for me in terms of how the company is operating. This is also how Amazon Web Services has grown to offer a vast array of services while maintaining utility. When you work backwards from your existing customers and build based on their needs/problems, you end up, usually, with sustainable growth. This works much, much better than when you have a solution in search of a problem (like blockchain in most cases).

Thanks for the summary, Sahil!

Disc: Invested

Have a question here.

Usually the companies show bill discounting as contingent liabilities in their financial statemets but recognise the bill discounting receipts immediately. In Q3 concall, RACL mentioned that because of prudent accounting norms, they’re not following this treatment and instead knocking off receivables once intra-bank settlement has taken place.

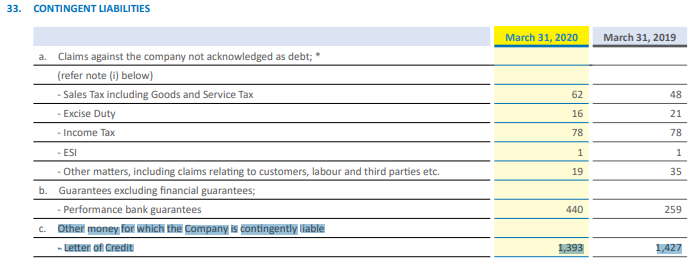

If that is the case, is the Company understating its true cash balances? Eg: part of the receivables may already have been converted to cash via bill discounting but due to outstanding obligation to bank (in case customer doesn’t pay their own bank the necessary dues), RACL isn’t recognising it as balance received?

I checked the annual report for FY 2019-20 and they indeed do not report bill discounting in their CLs (see extract below).

See extract from PI Industries (export dominant) for reference:-

Someone may have to clarify regarding the true bank balance of RACL in this case.

RACL has all the characteristics of CRAMS. What is impressive about this company is, they spent 7 years to strengthen their technology base, this investment would go long way in providing value for money for their customers

Lessons learnt from from yesterdays call: There will not be bargain power when you deal with multi billion dollar companies, the way to make money is better quality, repeatability and timely delivery. These characteristics improve reliability resulting repeated orders and introduction in new products (models). IMO, Specialty chemicals and Pharma companies doing CRAMS would have the same dynamics, high reliable vendors get repeat orders like Navin and Suven

Q4 Investor presentation

racl-q4-investor-presentation.pdf (1012.5 KB)

Yesterday’s concall recording - audio is not embedding properly, so can just click on it

Disc: Invested

Cash on RACL definitely needs some investigation and they should be putting out notes in AR to clarify some of the accounting rules they are following.

Having said that, understating cash is a better problem to have than overstating cash. If they reply to my earlier email, I will ask them this as a follow up question.

I have tried looking at other gear manufacturers like Shanti gears, Bharat gears and elecon engineering. RACL has better return ratios that them and seem to be doing better than them. But they manufacture bigger size gears also which are used for industrial gears. So in my opinion they have better longevity than RACL which is more focused on automotive gears and are always under the threat of EV’s even if they are able to manufacture the gears for them.The bigger size industrial gears require different set of machines . It would not be easy for them to shift to industrial in case the auto ones dry up.

We are sometime away fro EV for commercial vehicles (trucks, dumpers, caterpillar type machines), where the power and the torque transmitted through the gears is much larger. We dont see customers in that segment(Kubota could be an exception)…Like discussions earlier the number of gears in an electric car is going to reduce.

Why should i invest in this and not in Sona Comstar. From screener. For RACL- 3 year sales growth-14%, profit growth 44%, ROE 3 yrs-22%, OPM-25.6%, for Sona- 3 yr sales growth-37%, 3 year profit growth-51%, roe- 3 yr-27%, all the ratios look similar and receivable days for both are around 3 months. I could not get past data for Sona but for RACL FCF for past 5 years has been negligible. Is the whole gear business a gruesome business?

Leaving aside valuations, Sona has a product profile which includes electrical drives,motors and controller systems which go into an ev. They can make all the gears that RACL makes. They also make differential assemblies which are used in rear drive vehicles . They are also making complete E drive units which is an assembly of gears and which can connect the electrical motor to the output/wheels. Better value proposition to a customer which includes the electrical and mechanical systems.

In have gone through the concalls and have gone through their product profile and customers. Have given another view. Would like to hear a counter view from a person who understands this technically. I am not saying iam 100% correct but i stand by what i have written.

This topic is temporarily closed for at least 4 hours due to a large number of community flags.

This topic was automatically opened after 32 hours.

There are six major alternative of power drive configuration …

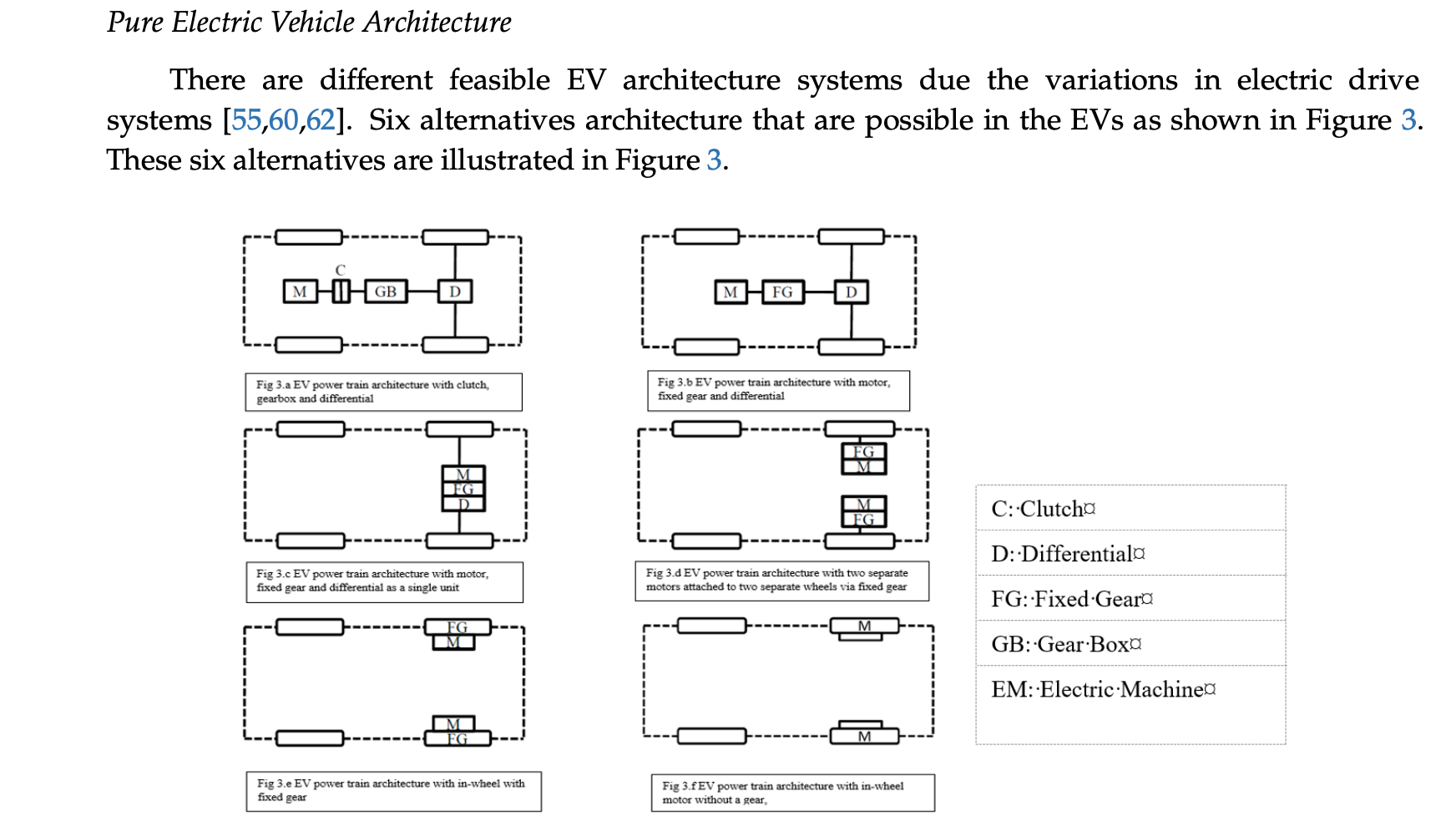

In 3a both transmission and differential gear system are required , in 3b , 3c , 3d etc gear component keeps on reducing

while in 3 e and 3f design power drive system it is nearly gear less

It is too early to understand how transmission system will evolve … but it is declining industry and hence ZF etc are outsourcing big time to smaller players …

Ultimately it would evolve to a system where all the wheels are connected to individual motors with a electronic differential where the speeds of the wheels are varied by the electronic differential system. There will be no gear box or the differential gears.

Surprisingly amount spent on R&D is zero…!

disc: invested sub 100 levles

Dinesh bhai… look at the CFO and CFI last 3 yrs… Gross Block has always gone up…

this is a execution company with strong capabilities : there is no capital WIP as well… they import machinery from Germany etc and do the value add job work for the clients.

R&D is less relevant today given the size

EV in CV is 5-10 years away… and the mkt will not go binary here… for RACL with less than 100mn top line there is enough to do for the decade…

The challenge will be capabilities to execute higher end… maintaining costs and margins…

Employee skill sets and work capital/ funds…

These are more relevant…

Dis: invested sub 100 levels.

please read the concall notes I have posted. R&D spend is not 0. Product R&D spend is 0, but process R&D spend is at least 15% of all employee expenses.

{kind=link}