If we start with PBT, then Working Capital changes (changes in current assets/ liabilities) which are also part of cash flow from operations is also adjusted accordingly due to advance taxes/ tax liabilities being in nature of current assets/liabilities.

If we start with PAT, then it is not the case and thus the net impact is same in both cases.

In your eg, for instance, if we start with PBT then we have basically made an adjustment to PAT in nature of adding back taxes -and this adjustment must have a double entry nature which is that advance tax asset is reduced by way of adjustment in cash flow workings but;

if we start with PAT then no adjustment is made to profit (ie we have not added back taxes) and hence advance tax is not reduced, and hence increase in assets to account of increase in advance taxes is there in changes in WC in cash flow from operations and this has impact of reducing the cash flow.

You can refer my earlier post as well (although it may be confusing - it is mere presentation, no impact on cash flow from operations imo)

disc : not invested, possibility exists that I may be wrong

This calculation seems wrong, should come around 500 Cr.

Anyway, taken FCF is also wrong because, not all EBITDA is OCF and not all OCF is then FCF as the company is doing capex.

Also, DCF works mostly for mature companies as their business models are well defined and operating parameters do not vary much. For companies of size like RACL, rely on other simpler valuation methods.

Thanks Simrat for helping. Actually this post had me believing that we’re supposed to take the EBIDTA as FCF, because taking 3 yrs avg Free Cash Flow was giving me an intrinsic value which was way off from the current market price. However taking EBIDTA gave me a number closer to the current market price.

What other valuation methods do you use other than PE and PEG? Currently RACL is trading at a PE of 33, do you feel that it’s fairly valued? I feel that given it’s growth potential, 33 isn’t too expensive.

What @Simrat said is right, But if you still want to calculate free cash to firm (FCF) in the correct way from Net Income, you can use the Formula that is : FCF = NI (-) Non cash charges [Depreciation/ amortization] (-/+) Increase/Decrease in Working Capital (-) Capital Expenditure.

There are also other ways to calculate FCF from CFO and EBITDA. Again the DCF models are not very suitable for companies like RACL which have growing or more volatile cash flows.

-It is subjective technique and valuation by different people varies widely

-WHAT PETER LYNCH SAYS ABOUT FUTURE CASH FLOW AND DCF?

=As per peter lynch, how one can predict future of company and future cash flow?

=Peter lynch relies on PE and PEG ratio for valuation

=He further says, rather predicting future cash flow, one can study company’s future growth triggers like expansion, capex, new market, new products etc.

=He says, if one does not rely on future profit and cash flow, one will never buy stocks at high PE

-In one interview, Ramdeo agrawal of motilal oswal said, DCF is difficult method of valuation with high chances of errors.

So, if these legends find it difficult, how can we rely on our future calculations.

RATHER,

=Study past years performance and future growth triggers

=BUY STOCKS AT REASONABLE P/E AND NEVER BUY STOCKS WITH HIGH PE RATIO

DCF method is flawed, except that it is better than all the other methods. All other methods try to guess the information that would be produced by DCF then why not do actual DCF.

Just one example:

Using reverse DCF when one assigns a PE after 3-5 years. On what basis does one arrive at the future PE. People say look for similar companies. Picking another company as similar is another guess. So when one tries to use simpler method one relies on very broad assumptions which can have big variation valuation.

The idea of DCF is really to get over complexity of multiple time series numbers (growth, hurdle) which cannot be intuitively calculated using one’s broad judgement - unless one is a good mathematician.

I don’t expect any impact as 1. RACL supplies to premium bikes which has no direct correlation with economy 2. Majority of those premium bikes get exported outside Germany

RACL didn’t impacted even post covid, so their OEM are immune to recession as the section of clients they cater they are likely to get unaffected by recession, also market discount this factor prior to the actual situation,

Enough land for taking revenue 3x then need to hunt for land.

Logistic time for europe has reduced by 22 days (inventory was a bit higher due to earlier logistic time being 22 days higher at 72, now 50. Inventory will reduce now)

For ZF- Capacity shortfall. Demand is for 120% Capacity right now.

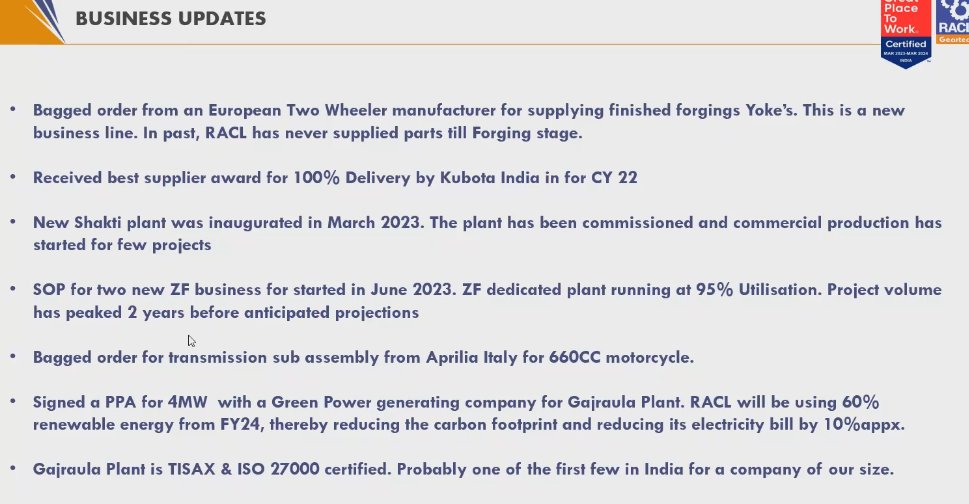

Entered into Yoke Forgings for existing customer, This would completely new domain for RACL Geartech.