There is no gross margin compression QoQ, they have passed on any QoQ cost increases. I don’t think expecting YoY flat gross margins is realistic at this point. Agree that the company will feel the heat of increased RM prices and European demand depression for sometime. Banking on the company’s deep relationship with OEMs for margin preservation.

2 Likes

Why has depreciation dropped despite an increase in fixed assets - have they changed depreciation policy?

Thanks for your point.

QoQ and YoY operating margins are indeed compressed. But, gross margin has remained flat as you indicate. So RM cost increases are being passed on, apparently. What explains the opm

compression then?

Either way, market has already started bashing RACL. In an up market, it is down 10%…

1 Like

Operating deleverage. Higher operating costs without higher sales. its N small things. see other expenses, see finance costs. Microcaps have a volatile execution cycle. One cannot expect QoQ or even YoY growth in a B2B microcap. Key question is whether something fundamental changed which impacted industry structure? fact that GM is same (or has actually expanded a little bit QoQ) shows that competitive positioning is same. My wild guess: Export orders got delayed which resulted in deleverage (could be one of N things: Europe crisis, temp suppression of demand, container shortage)

We will find out in concall. My probabilistic guess is that structural disruption has not happened, & thus this is a buying opportunity. Good news & good valuations generally do not co-occur. Have added a little bit today.

Depreciation drop can be due to many things. We can ask in concall but to my mind its an irrelevant detail.

Disc: Largest position by CMP, im biased.

12 Likes

If you go through Cashflow Statement, there is one more detail there which is not discussed in notes to accounts - profit/loss arising from sale of assets

Combining this with depreciation one, it seems they dont have good disclosures or accounting practices

1 Like

The Primary reason that I sold out of RACL is the inability of the promoter to raise any more equity capital due to their already very low holding - they would not want further dilution. Given its highly capital intensive business model and long cash conversion cycle with mid-tier RoCEs of 18-20%, growth from internal accruals is also limited.

RACL only grows in spurts by piling on debt - typically upto 1.5x of their book value, then scaling up and deleveraging. This was great when the interest cycle was turning down. Now with global interest rates rising, it is hitting their bottomline.

If the promoters had more equity they could have done a QIP to fund more growth given that the company has been rerated substantially. Personally would re-enter this closer to a 3x price to book.

22 Likes

That’s a very nice observation on RACL’s growth characteristics, thanks for sharing. A few comments.

About promoter holding - the promoter holds about 37% of the company. The reason minority shareholders want a high promoter holding is to ensure the promoter works in our interest and has enough skin in the game. However promoter holding % is not necessarily the right criteria to judge skin in the game. The right criteria is “What % of promoter net worth is made up by the promoter’s holdings in a particular company”. Seen this way, Gurcharan Singh must be one of the most aligned promoters, because given his history (employee to promoter), presumably all his wealth will be linked to his shareholdings in RACL. So promoter dilution from 37% should not be a cause for concern for minority shareholders because even at 25-30% levels, Mr. Singh will continue to have substantial skin in the game.

As far as promoter’s willingness to further dilute his stake is concerned, I think he will do it if makes sense. But I don’t think equity financing makes sense for RACL. Cost of debt right now seems to be around 11% p.a. and it should be comfortably below cost of equity financing, so the question of dilution does not arise immediately anyway. Even if he dilutes 5% of his stake (That’s already too much and he won’t do it), he will only have raised 28Crs at CMP. Assuming Q4 results were normal, he would have raised 5Crs higher, which is not really material. If he had diluted at ATH, he would have raised a further 5Crs, again not really material given that RACL’s last 2 years capex run rate has been 50Crs+.

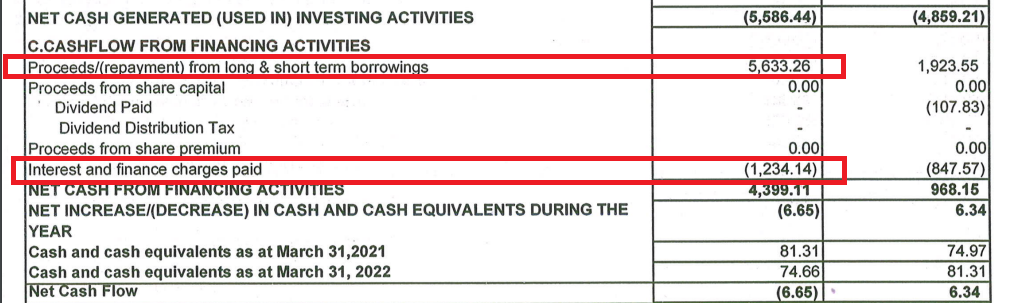

This year’s entire capex of 57Crs was funded by debt. Fixed asset turnover right now is 1.5x. Fixed asset turnover during 2016-2020 (Before the aggressive capex started), was 1.9-2x. Therefore, RACL is sitting on about 30% operating leverage which will start delivering soon. Assuming another year of heavy capex of ~50Crs funded entirely by debt, the D/E ratio will be 1.6x and Interest coverage ratio will hover around 4x. Those values are high and low respectively, but still not in crisis zone. If things don’t improve in another year’s time, the balance sheet situation may get concerning.

Mr. Singh has repeatedly referred to the close relationship RACL has with its European OEMs. He has hinted that the OEMs take care of RACL and will increase margins if the company is under stress. It looks like they have already helped by absorbing higher prices (Gross margins flat QoQ) but going forward can they also help their supplier out by releasing payments early and helping reduce receivables which have spiked this Q?

Key monitorable in the upcoming call for me would be twofold

- The commentary on European OEMs - How badly has their demand been affected by the war in Ukraine? Have they cutback on any production and is that likely to impact RACL?

- Will the original capex plan be on track to deliver 500Cr revenue by FY25 or will it be re-thought in the new context?

If these questions are satisfactorily and positively answered, I think extrapolating this quarter’s results into a larger crisis for the company will be premature.

I completely agree that in terms of share prices, RACL may stay at these levels for some time to come. For short term market participants, exiting on the escalation of Ukraine war would have been a good strategy. For long term holders looking to hold through to 2025, is there a breakdown in thesis yet? Don’t think so. Concall commentary and one more quarter results should tell us the way forward.

33 Likes

It’s not really a question of time horizon. IMHO, a leveraged auto ancillary with middling return ratios at 12x EV EBITDA and 5x P/B with its balance sheet at risk in the middle of a rising interest rate environment is not even in the top 10 of my buying list - especially given the sort of bargains that the last 6 months of corrections have thrown up. Of course, RACL could prove me wrong by delivering 25 percent+ EBITDA margins again - but I would rather see the proof of performance than sit on hope.

13 Likes

What attracted me to this company is its ability to generate 20% operating margin in auto component industry. Once I started digging deep, I was pleasantly surprised to notice their customer list of BMW and Kubota. Growing business with such marquee customers is never going to be easy and not going to happen overnight. Its not going to be smooth 20%+ YoY growth . In one year, it may grow 40% and then next year, sale may not grow at all. That’s the “nature of the beast”

Promoter comes across as a conservative true blue engineer, which I am happy about. Periods like now, provides opportunity to test once conviction and I am happy to add more during such stock price crashes.

Disclosure - invested for last 8+ months and added more in this week :- ![]()

17 Likes

ac86dd85-75fc-4d1d-8bec-e0c4daa2770b.pdf (256.5 KB)

Highest Monthly sale of 28.58 Crores for the Month of May’22

5 Likes

Thats a really interesting take, thanks for sharing.

Do you think once the expended capex starts producing revenue and hopefully the cash flow increases, the promoters can go the preferential route to increase the equity capital?

Concall on 24th.

Questions I would like to ask Management

1. Demand and receivables - With the war in Ukraine having intensified, is the company seeing any short to medium term impact on any customer orders? Are any customers cancelling or postponing previously logged in orders? Why have customer receivables increased significantly this FY - are customers delaying payments? Given the challenging cash flow situation, is it possible leverage RACL’s long term relationships to get customers to pay faster?

2. Capex - What’s the expected capex plan in FY23? How much more capex is needed to have sufficient capacity to meet the 500Cr target revenue? Is the management still confident of reaching INR 500 Cr topline by FY25 or is there a change in plan?

3. Capital structure - What is the plan for the capital structure of the company in the next 1-3 years? Given that the latest Qtr EBITDA Coverage ratio is down to 3X, does the management see any challenges in meeting its debt obligations? What will be the impact in Crs on the company’s annual interest costs given the rate hikes by Indian banks? Is there any guidance on target debt levels in the coming years?

11 Likes

Also…do we see demand from customers softening…owing to the rate hikes n eventual lower liquidity in the western world?

1 Like

-

For the past 6 quarters, our quarterly revenue have been in the 60-70cr bracket. When can we expect our quarterly revenues to cross this range to register 80-90 cr revenue runrate?

-

Some quarters ago, we had presented the % of revenues that we might get from EV & engine-agnostic parts. Given recent wins of BMW scooter, & a large domestic EV customer, what is our estimate for what % of our revenue could come from EV parts in FY23 & FY24?

-

In last concall we mentioned a large domestic passenger vehicle we are finalizing. engine agnostic steering & chassis parts. 90% probability it should come. Any updates on that customer & whether we were able to bag them eventually?

9 Likes

first model will be i3, sports sedan.

Considering, RACL has relations with BMW and has received orders for BMW 2w EV CE04 and RACL had highlighted its aspirations for premium passenger cars in EV

“RACL is gearing up fully to get ready for the future & we are diversifying into the Chassis component

and providing drive train solutions to the EVs. We have already invested capital expenditure for new

projects and futuristic technologies to enter into the Premium Passenger Car segment through one

of the largest players in the market.” Src : annual report

Any scope that RACL has got orders for this EV model of BMW ?

5 Likes

Questions and Answers :

Q4FY22 Concall notes :

% of revenue from EV and engine agnostic parts :

FY22 : 2% as EV contribution.

FY23 : >5%

FY24 : > 6%

Diversified in steering/chasis parts : also engine agnostic parts. Not dependent on type of vehicle.

We got the client/project awarded to us (discussed in Q3FY22) : Global PV player.

FY25 : 500 crores very confident on achieving.

Margins in Q4FY22 hit : Geopolitical situation from January onwards. That quarter, disturbed, input cost increased, volatility in market. 1 month no clarity, short term volatility, things have settled down and we are back to growth trajectory.

As a business strategy, we don’t want any customer > 25%. When dependence goes big, business is never stable, always volatility.

If we want to grow 25% top-line growth, we need 1 big customer. Every 2-3 years, we added Big customer, we nurture them and grow.

50% of revenues come from Europe, interest rates hike : Is there slowdown ?

There are few numbers, which are going beyond my imagination, we are getting very good demand. We are in premium luxury segment, demand is growing despite recession. Rich guys have good cash flows, our product goes to Europe (customers supply to globe not confined to Europe).

Receivables days high.

89 days is very healthy, it has reduced from 98 days. Until customer received good in factory, he will not pay. India to Europe logistics takes time since we are far from seaport, inland transit times are high.

When it leaves my gate to their gate, it takes 73 days.

Technically I get within 15 days. OEM are paying always on time.

Government is focussing on Delhi Mumbai freight corridor, it will reduce our transit 7 days.

Capex plan for 500 crores target :

FY23 : 50 crores. FY22 also : 50 crores

Gear industry is high capex industry. We are also upgrading our technology.

With interest rates increasing, capex funding source?

Interest are hardening. We get good rates because of our credit profile. We are getting interest rates just at MCLR no premium. Additional capex : debt since weak CFO and low cash/balance.

This year we will borrow 40 crores and pay off 10 crores. Our old debt at higher and hence new debt at lower cost.

Hence Interest as % is going down.

Prior FY17 : Asset turnover close to 1.8-2x. We started operations in 1990. All equipments obsolete, we upgraded/replacement then, then turn looked lower, since it was not utilized. Asset turnover of FY21/22, we have improved from 1.47 to 1.52x. it will gradually increase and go back to 2 levels (benchmark)

Product development :

We have a team of engineers. Team ~30 odd engineers only for this.

Geopolitical risk around European borders is always there.

Gas shortage leading to customer product halt? : They are still importing gas from Russia. At ground level, Germany operating at good level with Russian gas.

We believe in sustainable growth. We outweigh risk:reward and dont try to challenge this equation. In given situation, our ambition : 20-25% sustainable growth considering our base, beyond that we would have inorganic growth.

We have started to receive RFPs for FY25/FY26.

Steering/Chasis Parts : This is new product in automotive field itself, margins are good, less competitive intensity. Premium and complex product.

BMW : i3 sports sedan. Cant comment due to confidentiality.

Our 2nd generation is also gearing up for next leg of growth.

We dont do any capex unless business lined up with us. We never invest on anticipation.

Invested

23 Likes

Notes

- FY22: 186cr exports, 70cr domestic. 56% go to europe, 46% to india/asia

- Inventory days: 75 to 67, receivables from 98 to 89, 67 to 57 for payables, CCD: 106 to 99 days.

- FY22: 2% from EV, 5% in FY23, 6% in FY24, diversified into chassis & suspension & steering systems. EV + suspension will go to 16% not dependent on type of vehicle.

- Large global passenger vehicle chassis & steering parts that we talked about in last Q, OEM we are able to bag.

- If you look at it, we have grown 20-25% in each year except covid, can grow 20-25% even on top of FY25 target of 500cr revenues.

- Have been able to pass price hikes. Will go back to pre-Q4 margins in next few quarters.

- We dont want any client to be > 20% of our revenues.

- Europe recession: Forget decline, we are getting increased numbers from our customers. We are not into commodity segment, we are into premium luxury segment. Demand is growing in this segment. Good cashflow in upper strata of society. Although our parts go to europe, but the end product is sold all over the world. There can be some volatility due to chip shortage etc, availability of RM (particularly electronic components), otherwise demand is grow. No recessionary situation, forecasts from customers are very optimistic for near future

- Shipping times are very high. We are 2k KM from seaport. In-land transit times are high. SHipping times are high Our ports are not mechanized. Historically when product leaves my gate, and reaches customer gate is 72 days. In 89 days im getting payment. Delhi-mumbai freight corridor etc if it happens, If the on-land transit time reduces, then it will automatically reduce our receivable days by that many.

- Gear manufacturing is high capex product. High tech product. Upgrading tech, preparing for EV & suspensions.

- Will do 50cr capex in FY23.

- Capital structure: Interest rates are hardening, interest coverage is pretty good, older debts were higher rate, were BBB rated earlier, but now we are A- rated, so getting better interest rates now.

- Before FY17 asset turns were 1.8. Now it is 1.5. We had to do lot of capex in 2017 onward to modernize our equipment. Coming years gradually itll increase & go back to older levels of 1.8-2

- Product development team: 30 engineers only working on product development, team can develop products without inputs from CMD.

- Risks: Geopolitical risk is biggest risk to all world not only RACL. Forward trading can take speculatively nickel prices from 23k $/ton to 108k$/ton. This is purely due to speculation. In Commodity, speculation really hits manuacturers

- 75-80% of biz is premium luxury segment, 20-25% is more commoditized.

- Germany is still importing gas from russia. Germany, france etc are importing lot more gas from russia.

- Want growth to be sustainable. 20-25-30% is an ambitious organic growth rate. Prabh & his team are gearing for the future

- Customers have long term vision. Development team is working for FY 24-25-26

- Started getting RFQs for FY25-26

- BMW i3 sports sedan from china. We are bound by confidentiality, cannot speak about anything. We are aware about this.

- Chassis components are premium, complex products, good margins.

- 15% of growth out of 27% growth from new projects from existing customers, 6% growth from existing projects, 2-3% growth from new clients like ZF.

- CF moto is a JV KTM & CF motors china. That customer was added in past 2 years. ZF & ambient trucks was added in past 2 years.

- Capex: goes to infra creation, funding new projects, funding existing projects

Disc: Invested, biased

32 Likes

Got an opportunity to ask these questions and Mr. Singh was patient enough to answer these.

1. Demand and receivables - With the war in Ukraine having intensified, is the company seeing any short to medium term impact on any customer orders? Are any customers cancelling or postponing previously logged in orders? Why have customer receivables increased significantly this FY - are customers delaying payments? Given the challenging cash flow situation, is it possible leverage RACL’s long term relationships to get customers to pay faster?

As per company there is no demand slowdown from Europe in spite of recessionary fears, gas shortages and the war. On receivables, they can’t do better than present numbers as they are constrained by door-to-door shipping times from RACL factory to customer warehouse (Receivable days may decrease by ~7 days when Delhi-Mumbai freight corridor is up and running)

2. Capex - What’s the expected capex plan in FY23? How much more capex is needed to have sufficient capacity to meet the 500Cr target revenue? Is the management still confident of reaching INR 500 Cr topline by FY25 or is there a change in plan?

Capex will be ~50Crs for FY23, debt funded. From what I could understand, capex will continue in the coming years and fixed asset turnover will hover around present number of 1.5x and may settle at 2x in the long term. Management is confident of achieving 500Cr topline in FY25, no change in guidance on that front. Target revenue for FY23 ~345-350 Cr (Surprised to hear such a precise guidance!)

3. Capital structure - What is the plan for the capital structure of the company in the next 1-3 years? Given that the latest Qtr EBITDA Coverage ratio is down to 3X, does the management see any challenges in meeting its debt obligations? What will be the impact in Crs on the company’s annual interest costs given the rate hikes by Indian banks? Is there any guidance on target debt levels in the coming years?

In answer to my question, Mr. Singh said that in FY22 40Cr LT debt was taken whereas 30Cr LT debt was retired. However, net-net, there was 56Cr debt addition last year as can be seen below. Interest rates on loans for the company have reduced compared to before due to credit re-rating from BBB to A-. However, he acknowledged that interest costs will go up a little due to interest rates hardening.

Overall, as an investor the call was satisfactory. But I am not really comfortable with the balance sheet situation. Debt will keep increasing with interest rates also hardening putting more pressure on the balance sheet. Operating cash flow generation in FY23 will be a key monitorable for me, that’s the only way leverage can be reduced a little.

Will keep allocations at moderate levels due to balance sheet position. Will monitor Q-o-Q and increase allocation when gross margins/cash flow increases.

28 Likes

Racl concall june 2022

1…Geography

52% @ Europe,

46% @ India and Asia Pacific and

2% @ USA

2…Financials

A…Debt-Equity Ratio rose from 1.00 to 1.25

B…Cash Conversion Days have also dropped from 106 days to 99 days in this financial year.

C…Low ebita

=Unfortunately the Geo-Political situation started deteriorating globally from January, 2022 and precisely there was big blast in February, 2022. So, that quarter was disturbed due to the sudden increase in input costs and volatility in the market and things went bad to worse. For the 1st month, there was no clarity and that created short term volatility.

= Also, the disruptions due to the said geo-political scenario and Europe, not only impacted RACL but all the component manufacturers that were mainly dependent on Europe. More so, the impact was not on account of the market, rather due to the volatility to the input cost price.

= But now, issues have settled down and we have made all the corrections and in the coming quarters, we will be back to our old normal.

3…EV

=For FY 21-22, we had a little over 2% of EV Participation which will now

increase this year to 4-5% and eventually it will increase around 6%, in the next year also.

4…New products

=Apart from EV, we have also diversified into, Chassis & Suspension parts also, which are not dependent upon, EV, Fuel or Hybrid, they have common application for

all the platforms.

= In the coming years, our EV and Suspension will grow more than 16% of our revenue and it will be not dependent on type of vehicle and this way we are preparing for the future.

5…Steering and chassis parts

=This product, for which mass production has already started, is a new product in the automotive field itself. Margins are looking good and impressive but since it has come into

mainstream production, very recently.

= So, let the production stabilize as, when we start the production initially, there are always teething troubles and then are always certain successes

and failures and challenges. Our estimations are that this product will give us good margins, but, let us wait for some more time that the production gets smoother. Then we’ll be able to have a clearer picture.

=This is a premium product and very complex. Of course, the margins are better, but you will also see that it is a competitive world and customers also know how to squeeze the suppliers,

so we have to draw a balance. But, you can also understand that why we are selecting these kind of products because there is no crowd of suppliers in this. We have put our best foot

forward and we will get the advantage of this.

6…New customer addition

=If we have to add 20-25% year on year growth to our top line, then our plan is to add a big customer in every one or two years, so that we can add 5-10-15% from it and every year the customer organically grows 2-3% with us so that in aggregate, we grow by 20-25%.

=So, if you see our past history, every 2-3 years we added a new, big customer, then we nurture them and bring them to a sustainable level so that they also are confident with us and we are also to confident with them and then we start adding new customers.

=We added new customer ZF in a big way past 2 years. So, that customer has still not added much to the revenue in the previous year, it will start adding to the revenue from this year.

=MAN Trucks was a new customer

and CF Moto is basically KTM. They have formed a joint venture in China and that was also added in last 2 years and it has already started adding to the revenue from last year.

7…A large global passenger

vehicle customer was being finalized for some engine agnostic steering and chassis part with a probability that the business could come to us.

=We have begged the new business, but due to confidentiality reasons, we cannot divulge much information.

8…Roadmap

=Our roadmap in earlier concalls, that by FY 2024-25, we plan to

become a Rs. 500 Crore Company. This road map was chalked out around 2-3 years back anat that time, it looked very aggressive and over optimistic.

=But now as we are nearing FY

2024-25, we are very confident that we shall be able to achieve it.

9…Vision

=BMW and all such customers, give us a business, they will not give us a business for tomorrow, they’ll give this business for after 3 years as they have a longer gestation period.

= At our operational level, we are discussing FY 21-22 and FY 22-23, but our development team is working for FY 24-25 and FY 25-26 with our customers.

10…Capex

=We did around 50 crore of capex last year and this year we plan to do another 50 Crore, so just a breakup of, how this 50 Crore was spent. A total of 100 Crore capex is a huge capex .

=Partly it goes to creating infrastructure, then it goes to partly to fund the new project and partly

goes to funding of our existing projects. Broadly, around 35% goes to our production activities and all the production machines.

=Capex has to be done very judiciously and have to spend money on where we need equipment precisely. And we have always shared that we will never make any capex until we have very clear business lined up for us. We always invest when we get the business. You may take it as a conservative approach or you may take it as a strategic approach, but we always believe that, it is always better to create a fully integrated and flexible setup, so then when the customer comes, you have that technology to produce sample parts, but for the

capacity expansion, but will invest only when it gives us an order

11…growth

= I will say whether you grow by 2% or 100%, it should be sustainable, because any short term growth will not lead any business to success.

= Our ambition to grow 25% average year on year, is a very sustainable growth

=Beyond that, then the way out is that either we have some inorganic growth by mergers and acquisitions. But by creating your own facility, creating your own infrastructure, getting your own building, getting your own product model, then we have to invest a lot and it’s not only the money, the human

resources also, your technical competence

=Let the time come and our next generation is also preparing for the future. Let’s see if there are some bigger opportunities and there are any alternate methods of growth, we’ll

do that also. But right now our focus is on growing the way we are growing on 20-25-30%year on year

12…Customer concentration

=We always try that none of our customers should be more than 20-25%. When the dependence increases, the business

does not remain stable and there is always a level of volatility. Let’s say, you are dependent on a particular customer, say, 50-60% and something wrong happens to that customer, in that case, you get very badly impacted. Therefore, this strategy acts as a limiting factor, that even if that customer hits by 50% so net loss to us will not be more than 10-15%. For us, this strategy is doing very well, and we have tried and practiced it for the last 10-15 years and we found that this business model works.

=We have also seen our peers that they are dependent on a single customer by 60%-70%-80%, but when that customer fluctuates, then the ripples are much bigger on those suppliers. Whereas in our case, this is a safeguard, which we have adopted strategically. So, we never had this ambition to go beyond 25% of our revenue to any single customer.

13…Product development

Q=I’d like to ask that, are you involved in the product development or your team can do product development without your involvement at all?

Ans=We have a full-fledged team of engineers. Our product development team, as on today, has

30 odd engineers, working only on product development and the team is very capable. We only have to add value and we have a dedicated team doing it.

14…Slow down/war effect

Q=50% of our revenues come from Europe and with the war situation and

the interest rate hikes, going on, how do you see customer demand right now?

Ans=Everything is on track and in fact forget decline, we are getting increased numbers from our

customers. The reason is that we are not into the commodity segment, we are into the premium luxury segment

15…Luxury segment

Q…What percentage of the portfolio would you say is fairly resistant to the economic conditions because the end customer is the super-rich.

Ans…Almost 75-80% of business goes to premium and luxury segment and 25% goes to thecommodity segment.

=So, these business are not very prone to shorter hiccups. But, yes, if anything bigger happens, it will have an impact.

16…Asset turnover ratio

=As already mention that gear manufacturing is capital intensive industry and we can’t really

get very high number of Asset Turnover, but 2 should be our benchmark and we are

gradually moving towards that

Q= I notice that the fixed asset turnover for the company was closer to 2x, right now it is I think around 1.5x and we are going to do more capex. So, do you think that we will go back to that closer to 2 x or the nature of the business, the technologies that we are getting into, will bring the asset turnover down to this level 1.5x

or is there some operating leverage waiting to play out in the coming years

Ans=Your observations right, prior to 2017 our asset turnover was better. The reason is that, we

started operations in 1990 and there was a time when all our equipments became obsolete and we had to invest very heavily to change all those obsolete technologies to newer

technologies. So, that replacement costs were also adding to the assets which will not contributing much towards increase of the top line, but actually it was being utilized to

upgrade our technologies and replace the obsolete technology. And if you really compare our asset turnover ratio of FY 21-21, you see we have already improved from 1.47 to 1.52, and

then coming years, it will gradually increase.

17…Capital structure

=We did not generate much

operating cash flow last year and cash balance is also not there. So this incremental capex will have to be debt funded

18…Working capital management

=Our receivables in absolute numbers might have increased, but if you see receivable in number of days has reduced.

=Previously it was 98 days, now it has come to 89 and 89 days is a

very healthy receivable because until customer receives goods in his factory, he cannot pay me.

=Unfortunately, logistic time from India to European destination is very high because 1st of all, we are far from the seaport, almost 2000 kilometers away. So, the inland transit times

are higher and then the shipping time is very high because our ports are not so mechanizedthat the goods move very fast. As per our historical data, when the product leaves my gate

and it reaches my customers, it is around 70 to 72 Days and in 89 days, I’m getting the payment.

= So, technically the goods enter the gate and within 15 days, I get the money from them. So, nothing can be planned the better than this, except the Government improves our

infrastructure and there is a lot of focus on them, particularly, this Delhi-Mumbai freight corridor

Disc…invested

My latest portfolio

16 Likes

19 Likes