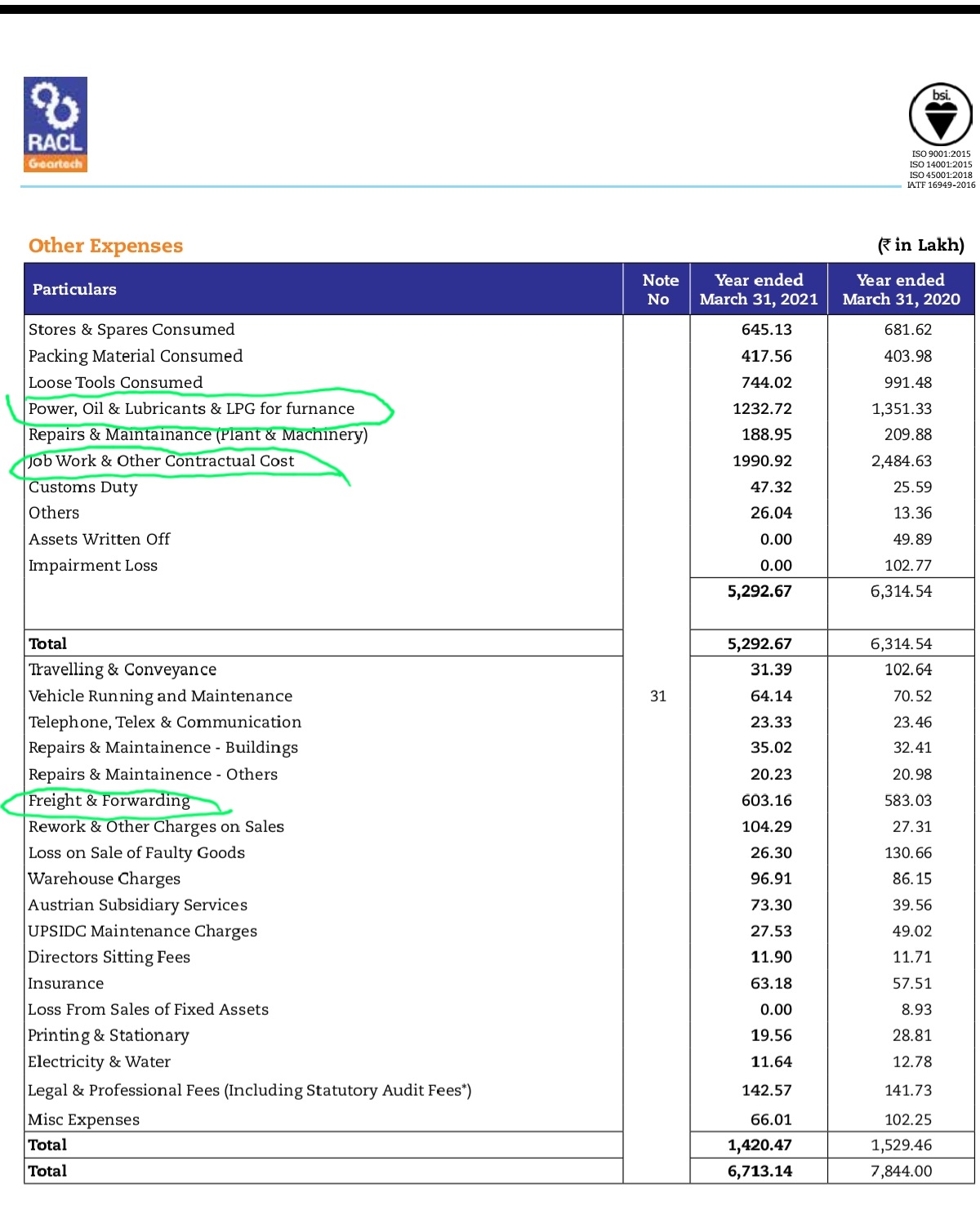

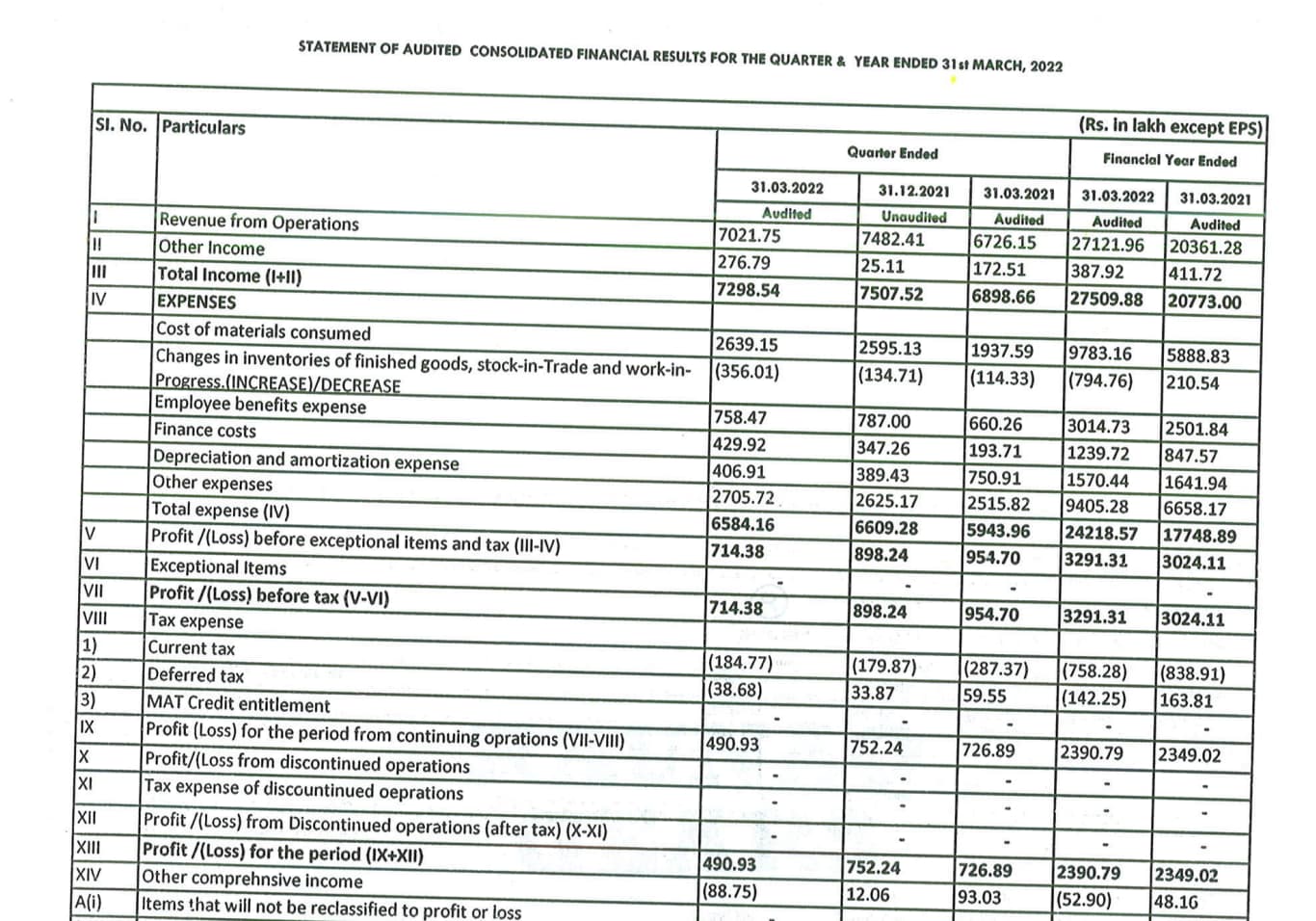

Looks decent number for Q3 overall, on margin pressure front given Other expenses are the party pooper, it would be apt to see what RACL definition of same is and which are bigger components,

Three major components make up for 60% + for other exp per AR 21 as highlighted. Power and freight are common suspects per other mfg heavy commentaries. Job work is another major one for RACL.

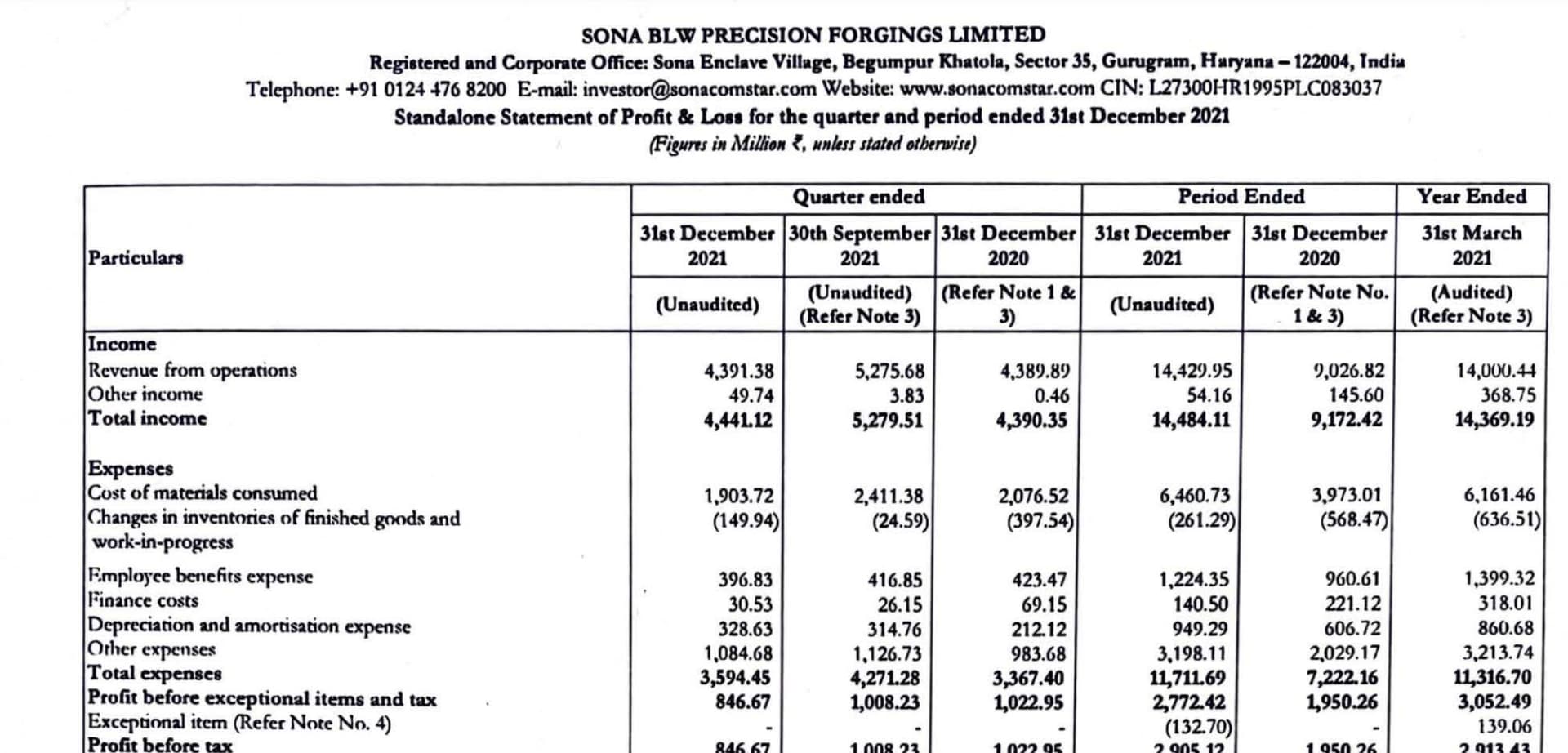

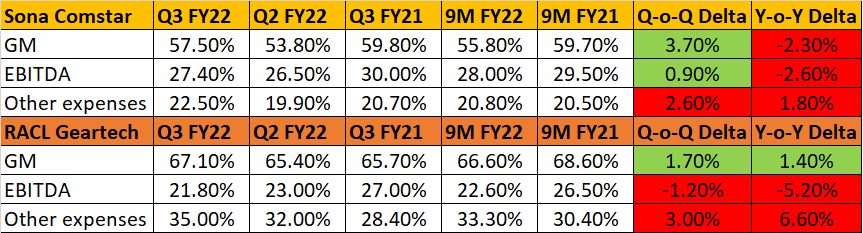

Revenue growth was impressive for RACL y-o-y and q-o-q no doubt. But something has gone wrong with Other expenses in this quarter. Detailed margin comparison of RACL and Sona below

While both have grown on gross margins and suffered on other expenses Q-o-Q, Sona has managed to cover the other expenses increase with its GM increase. RACL hasn’t been able to do that.

I hope there is a concall, Management needs to be queried on this sharp other expenses increase. Seems like they haven’t been able to pass on increased power/oil/freight costs to their customers this quarter. Stock probably over-reacted today. Concall should clarify.

Questions i am Planning to ask if given a chance in concall:

Hi,

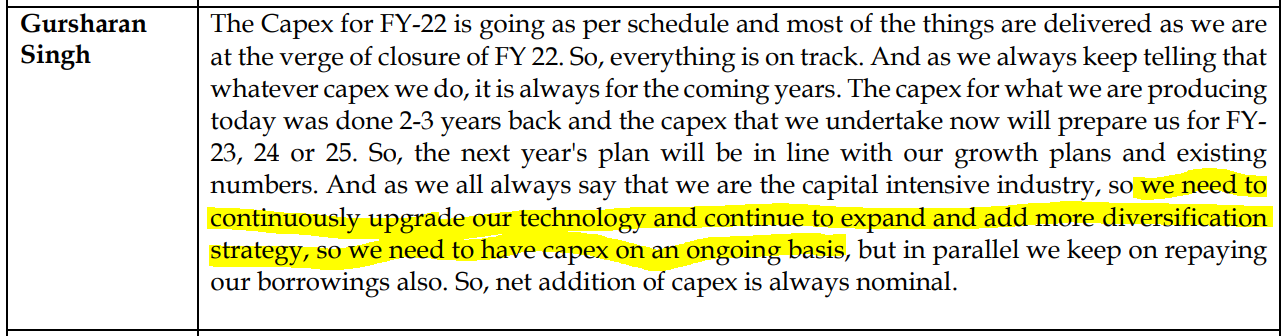

We had undertaken a 50cr capex in fy21 & were going to understand 50 cr capex in fy22. How have these capexes progressed? When do we envision for commercial revenue to start flowing from our fy21 capex & our fy22 capex?

How has the commercial launch of BMW ce04 (for which we provide gears) proceeded for us? Do we see significant traction for that product in the end market?

If we look at our 9Mfy22 operating margin it has been in the 21-22% operating margin range whereas it used to be around 25-26% in fy21 sep20 to mar-21. What has led to this downward pressure on our margins? To what extent are our margins affected by logistics costs/ shipping costs & to what extent are they affected by raw material or commodity inflation? Are we able to pass on these price increases to our customers?

Hi, who are competitions OF RACL Geartech? On screener it showing Amara Raja, which in battery company. Is there any company who makes gear other them Sona Comstar?

11.03.2022 (FY22Q3 concall notes)

• Input cost inflation + freight cost + higher gas prices lead to shrinkage in EBITDA margins. Higher other expenses was mostly due to high gas prices. Also in Q3FY21 prototyping contribution was higher which led to high margins last year

• Will try to maintain 20-23% EBITDA margins

• Net debt has increased by 16 cr. over Q2

• Semi-conductor shortage had much lesser impact on their customers until now

• Ongoing capex of 50 cr. is close to fully spent

• Electric vehicles (EVs):

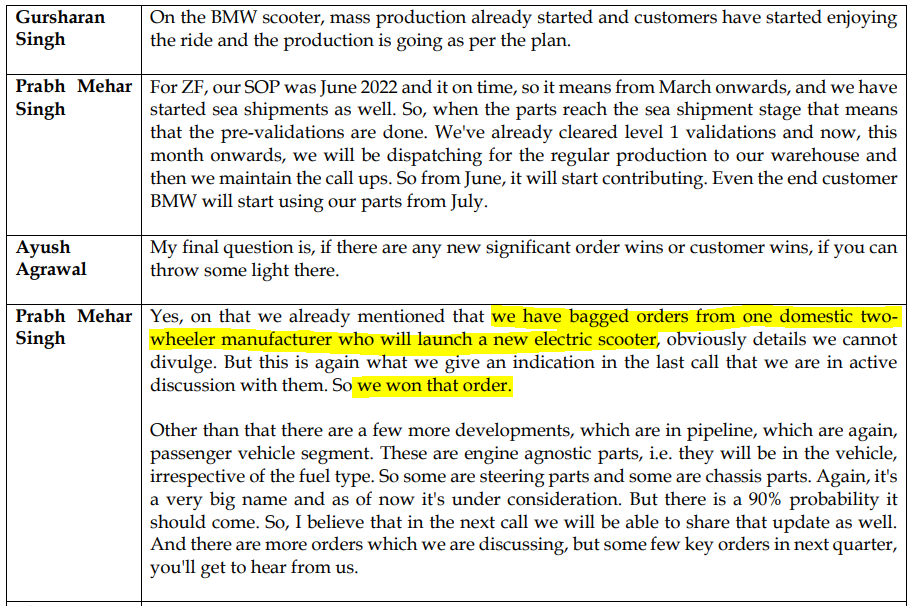

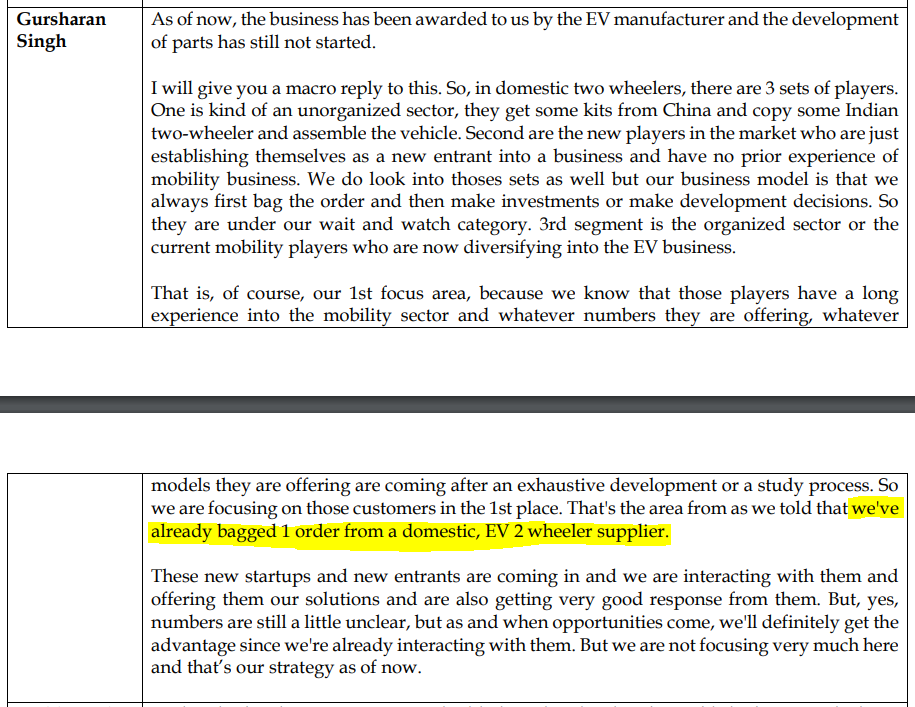

o Got a new order from a domestic 2-wheeler manufacturer (incumbent) that will make EV scooters (under confidentiality)

• ZF: SOP is in June 2022, have started sea shipments in March 2022. Cleared level 1 validations and will be dispatching to RACL’s warehouse in Europe

• In domestic segment, main focus is on large incumbent companies followed by newer companies who are starting up in the EV segment. However, the main focus is on getting business from incumbents

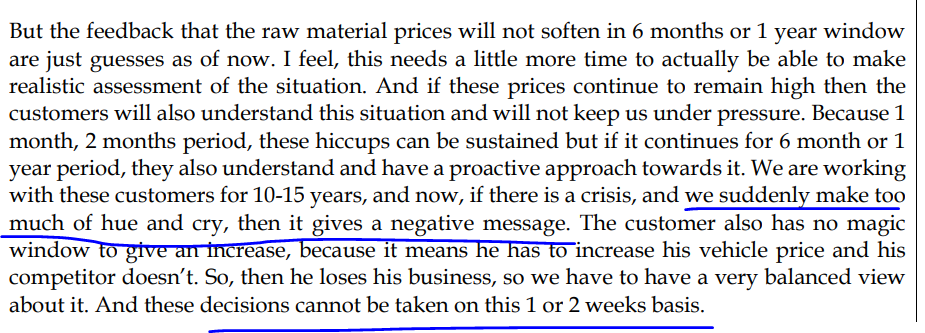

• There is no systematic trend in raw material price spurts

• Focus on lower payable days as they can get better pricing thereby increasing margins. Working capital costs are much lower than the margin benefit it brings

• Hiring: Hire freshers out of colleges, have a 2-year training program on the shop floor

Disclosure: Invested (position size here, no transactions in last 30 days)

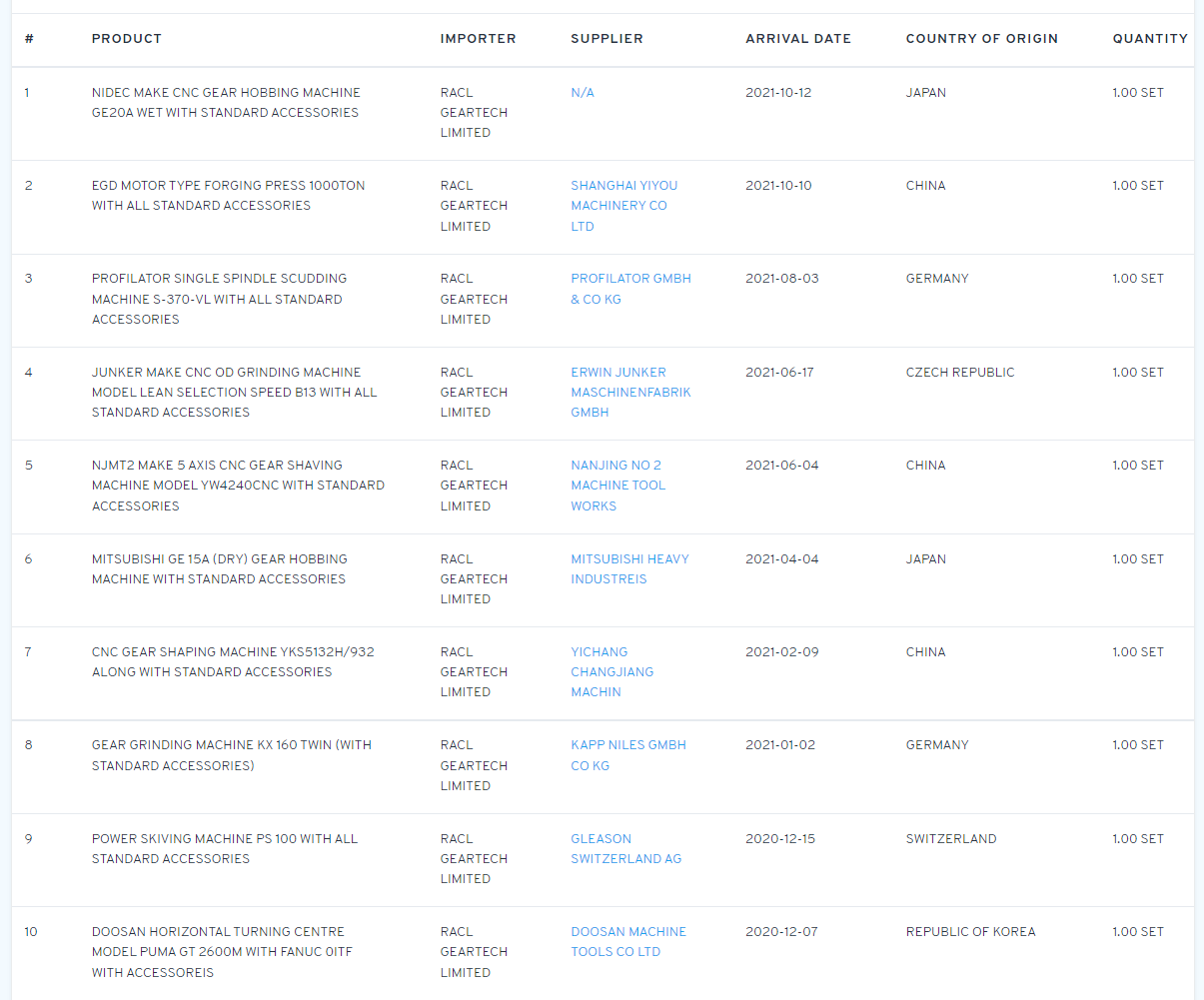

RACL continuously working on the technology upgradation and process improvement. Here is the list of machines/tools imported recently by RACL for capex / process improvemnt:

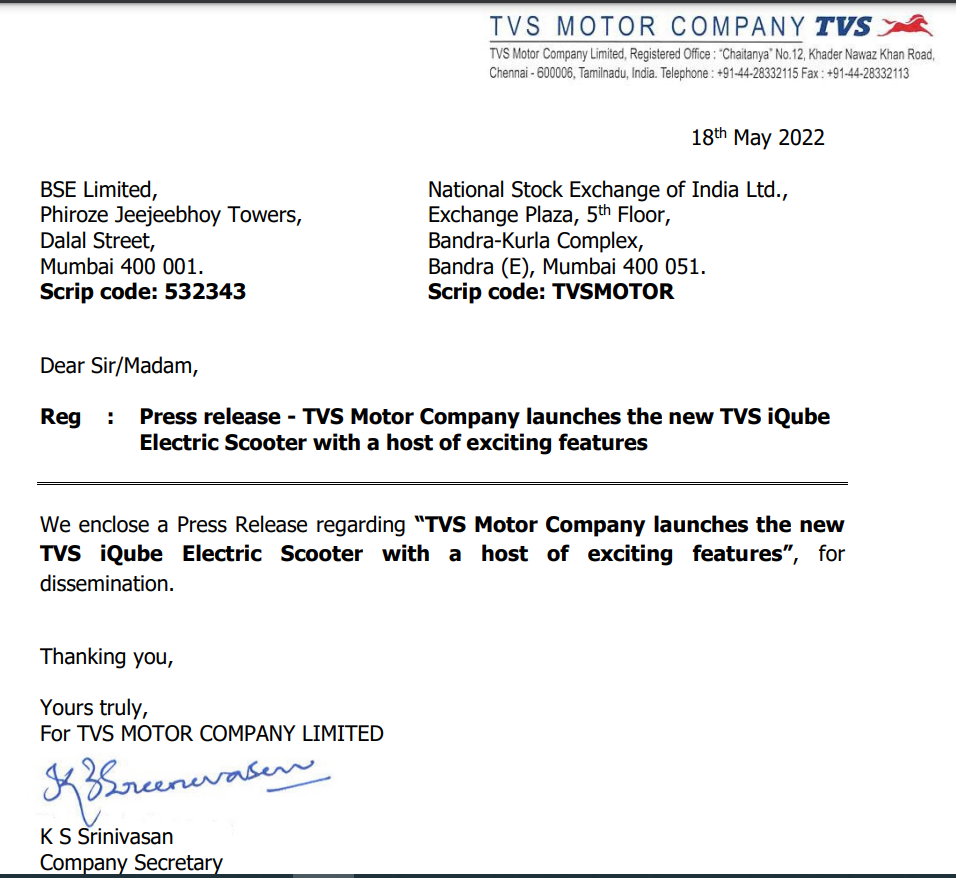

TVS launched their flagship EV Scooter iQube yesterday. My speculation is that RACL has got this order. In last concall management clearly said that they won an order from a domestic major 2-wheeler player for their “new electric scooter”. TVS iQube was initially launched (only one variant) 2 year back, but they were working to upgrade that and now launched in a new avatar in 3 variant with lot of features added and will focus now to grab the market share. So far, their ev sales were miniscule comparing to market leaders:

TVS has been RACL’s client since long, and recently no other EV scooter launch in sight from any major auto player to my knowledge. Management has given enough hint in the last con call also:

We can only confirm it during the next investors call, this is a pure speculation till then. If this becomes true and TVS can grab a good share of market going forward, this can be a good revenue generator for RACL.

Disc: Invested from lower levels and biased, this is not any recomendation to buy/sell.

HOLGER KLEIN – Head (India, APAC) ZF Group on focus on Indian operations & increasing sourcing

“As part of our Refresh India strategy plan, we aim to double our component sourcing from India to €2 billion. We doubled down on India several years back and we have seen a 20% CAGR, as we aim to quadruple our business in the country in the coming decade to about €3 billion.

We have 3 subsidiaries, 4 JV partners & 8 engg centers, with over 13000 employees in India. There is a clear roadmap to accelerate localization & use India for sourcing and development capabilities for the global markets. We learnt it a hard way over the last few years to diversify the supply chain amid disruption. Today one doesn’t want to be too dependent on one source, in this India gains.”

Top line stagnant, significant margin compressions. RACL-g was considered akin to the specialty chemical mfg- why could they not pass on input cost increases? In the domestic market, auto stocks are back in favor and so are auto-anc. RACL Europe exposure is also a weighing factor.

RACL had a good run up so far. A few more quarters of high inflation will really be a trying time for RACL. On balance, expect stock to Drop.

DISCLOSURE position at 570, will look to exit and get back in at lower levels if I notice

top line growth.

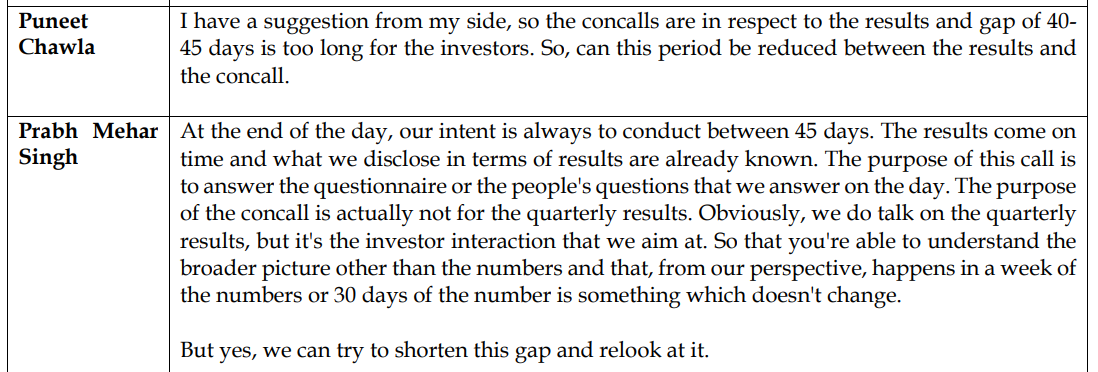

i think thats why they deferred the results for couple of week to avoid that long lag, which was pointed out in the previous concall as well…hopefully we will have call within this week itself…good time for long guys to accumulate it

Invested and biased

Last call i requested specifically to avoid time lag between results and call

Mgmt answer was more on the lines of --dont think short term

Another question was on passing cost to customer

Mgmt wanted to take a big picture and dont want to go to customer every few weeks/months

They believe if costs has increased, it will follow some time lag with renewal of contracts

Disc-- Exited with Dec Quarter results which also showed margin compression

Expect few more months of pain in margin–confcall may help us to understand current scenario