BMW has a partnership with TVS, the BMW G 310 R and G 310 GS are built in partnership with TVS. Is TVS also a customer of RACL? If not, may open doors for them. Apache is one of the highest selling premium bikes in India.

4 Likes

Q2 concall notes have been very well captured by VPers,

Stock rerating has been pretty swift after three consecutive qtr earnings and valuations are at 3X sales and 25X EBDITA on TTM basis - upper band for Auto ancillary, recent breakout above 600 after few months of consolidation is also a healthy sign on technical charts.

Some additional points

- MD called out Mr Chand/Motherson sumi as role model - multi countries- multi plants - thousand of employees - ambitious mgmt and quality of execution for microcap is healthy sign for us.

- There are reasons to believe that they may do beyond 500 cr mark by 2025, they called out buffer as part of strategy to cushion downside risks, thesis below

- their Qtrly runrate as of now is 70 cr /qtr, annualized 280-300 Cr from existing Customer or core biz in FY 22( normal year case)

- 50+ cr Capex done recently to deliver 1.4X I.e. 70 -80 cr type top up -

- FY 23 - 380 to 400 cr from above components

- a normal 20% growth in above itself takes us above 500 cr mark in FY 25

Additional Upside triggers

- Kubota-escorts will be adding meaningful business - MD admission of being aware of deal and meeting with Kubota folks during deal visits and finalization

- EV can add to meaningful upside, BMW scale up and any new contracts from local in progress discussions ( usually they win once they call out has been a trend)

- Newer biz will be 25% of top line by 25 that is 125 cr per current projections of 500 cr( from 2 large accounts added)

Above 3 could add anywhere north of 200-250 Cr , ( pure speculation based on data points ), can adjust for some risks/buffers.

Though they have delivered higher margins in recent quarters but they weren’t willing to commit on sustainability, given supply chain and logistics/RM cost improvement, hopefully they won’t venture far off and no reasons to believe high volatility as of now.

Was bit surprising to see no institutional participation in calls yet, retail dominance was visible.

Invested and added in recent breakout

25 Likes

Both being RACL customers( BMW more so on EV), this could be an interesting opportunity in coming years.

3 Likes

Analysts and sources close to the companies have said that it’s a win-win for the partners. For BMW TVS facility offers low cost and high quality manufacturing solution for India and global markets, for TVS the tie-up augurs well and it is looking to accelerate the premium segment with few more new launches to improve profitability as these products come with high margins .

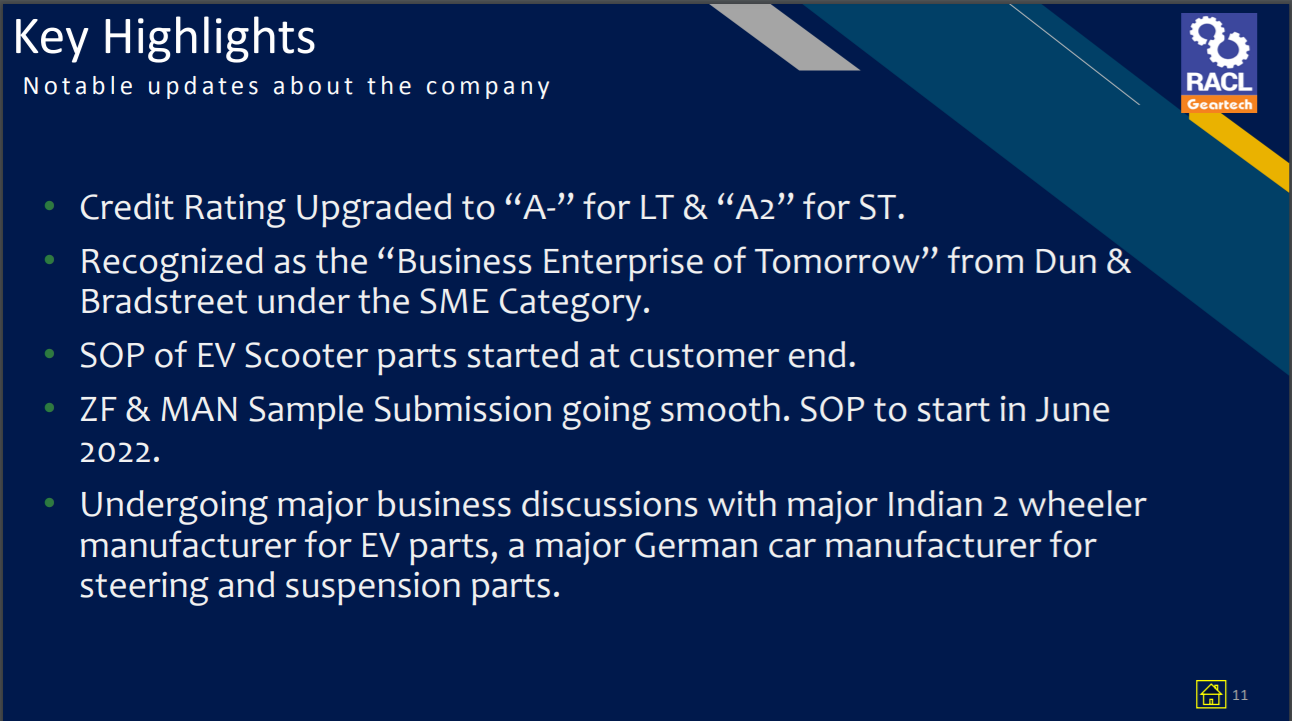

In the presentation last week, they said this:

The major indian 2 wheeler manufacturer for EV parts mentioned in the last point could well be TVS (just specuating here as they are an existing customer) !!

This new development from the long-standing partnership could definitely be an interesting opportunity for RACL going ahead ![]()

19 Likes

This is also an accounting misnomer that RACL does which overstates their debtor days. Most exporting cos (like PI) record Letter of Credits as contingent liabilities and discounted LCs are immediately credited to bank accounts. RACL doesn’t do that and only records the funds lying in its bank against discounted LCs once the end customer makes a payment to their bank.

1 Like

Management discussed this at length in the concall. Please read them all.

1 Like

As auto industry is cyclic in nature, can we expect racl to maintain it’s sales growth in bit long term like say 5-10yrs, as they r into agri segment & luxury bike segment both sales can be cyclical , management is good & it’s a turn around story no doubt but in bit longer term I want to clear my doubts whether with down cycles can it maintain sales growth, also put some light into client concentration & peers competition

1 Like

Hi All,

I got introduced to RACL Geartech via @sahil_vi Tweets. I went through the entire VP thread today. Would like to thank Sahil and all the other contributors for adding such rich data and commentary on the company here. Getting up to speed for a new investor like me becomes much easier thanks to the efforts made by you all!

You asked Management in the last concall about how they are able to deliver better quality than customer needs (25 ppm vs 100 ppm). I think you were trying to understand whether company has an identifiable moat in terms of quality.

My reading of Mr. Singh’s answer was that it seemed quite generic - he talked about taking care of people (But nothing about hiring new talent) and having best technology (But without going into any specifics). To me, his answer doesn’t project very high barriers to entry for new competition. I know in past concalls he has mentioned that long client relationships and past record of delivery are RACL’s biggest moat and he does not see any auto-ancillary entering RACL’s space soon, but I guess I am trying to look for factual evidences of moats in addition to trust on Management commentary (And Mr. Singh has certainly earned the right to be trusted with the kind of turnaround he has enabled for the company). I think understanding the barrier to entry for RACL is important as the entire investing thesis in RACL rests on its ability to sustain its niche clientele and high OPMs. Unlike Sona Comstar, RACL plays in a niche segment and RACL management does not guide for aggressive EV tailwinds or a very large order book, so growth will be relatively slow (Beyond 500 Cr topline) and sustenance of OPM will be a large part of the investment thesis I guess.

It would be great to hear your views on the following therefore:

-

What moats according to you does RACL truly possess and how easy/difficult would it be for an existing Indian auto-ancillary to eat into RACL’s pie of niche clientele in 2W/ATV/tractors etc.?

-

Basis Management commentary, new orders and Capex plans underway, it seems that RACL may be able to achieve the stated goal of 500 Cr topline (+/- 10%) with 20%+ OPM by FY25. Do you think there are capabilities present already or being built at RACL that can take the 500 Cr topline to 1000 Cr @ the same OPMs in a further 3 years time from FY25?

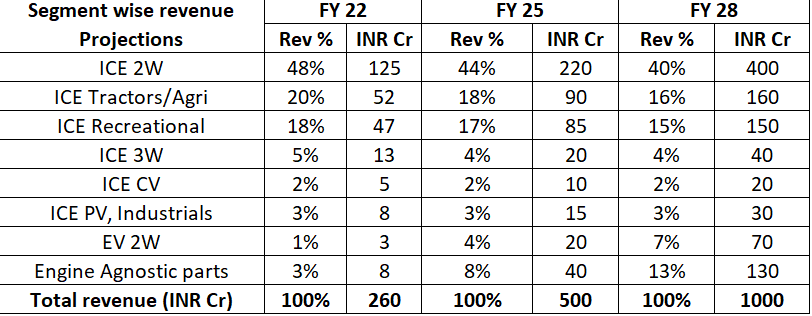

A projection of current segmental revenue and segmental revenue 3 and 6 years out might look like this (Basis management guidance; I have extrapolated EV and Engine agnostic revenue components from FY25 to FY28, assumptions may not be accurate, please correct me in case they aren’t).

Now, basis Mr. Singh’s comment that per kit motorcycle revenue for RACL is ~INR 10.5k right now, in order to do 470Cr INR of 2W revenue in FY28, company would have to sell ~3.73 Lakh 2W kits (By 2026, have assumed kit cos will be ~INR 12.6k based on 3% yearly inflation). Is this number 3.73 Lakhs achievable considering the niche luxury bikes market RACL plays in. Maybe @msandip can comment basis his extensive deep dives into client numbers. The same concern would be present in the other niche segment of Recreational vehicles. Is there enough demand to sustain a 3X jump in revenues for RACL? I would assume this concern would not be present in the other

segments like tractors/PV/CV as enough demand should be there.

Critically, if such numbers can’t be driven from the luxury segment for 2W and Recreational, what kind of OPM impairment are we looking at to serve more affordable 2W segments?

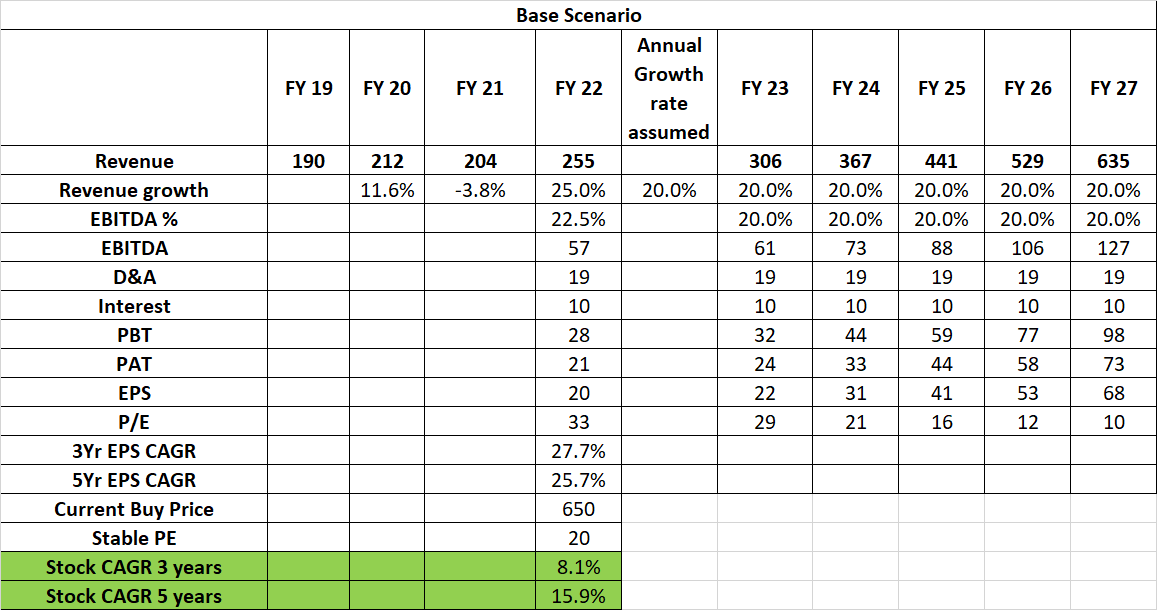

These are some key questions that I am looking forward to discovering the answers to along with the VP community. I discovered this company recently and will take a starter position soon. As per my calculations, even if we miss Management guidance by a significant margin for FY 25 (440 Cr FY25 revenues @ 20% OPM) and stock suffers a de-rating from current PE to 20x (Implying 1.5-2x P/S, which seems a safe P/S for an auto-ancillary without the premium clientele and margins of RACL), it has the potential to return 8% and 16% CAGR returns for a 3 and 5 year horizon. So investing at current prices seems like a safe option with no capital impairment risks but with great upside potential. Would love for some of you experienced folks to take a look at this and poke holes in it.

Happy New Year to you all! Wish RACL Geartech continues its wonderful turnaround journey and continues to create wealth for all shareholders ![]()

18 Likes

Just my two cents, please ignore if it is not enough.

- MOAT is overrated ! especially for an auto ancillary company , SonaComstar and Mothersonsumi command a premium bcos of their scalability and being aggressive , To add to that comstar has a good portfolio of parts supplying to EV vehicles mftrs.

RACL is neither aggressive nor do they have ambitious plans. Infact they expand only if the client asks for new SKUs and if the new SKUs demands expensive machinery, I believe in the past their customer have sourced or financed it for RACL (if my memory serves right)

- Their capex is already completed POCs are done and samples are approved , no more capex is needed , its a play of brining operational efficiency and reaping the benefits of established relations

What I have invested in RACL is for the management, they are not flashy could have gained more mileage by throwing around their clients name like BMW, Kuboto,KTM … they never do that .

I didn’t expect a phenomenal movement in the stock price but I would never say NO if that happens.

ITS all abt process and culture both are intangible, rest, all the stats you can find on concalls and other reports.

Culture eats strategy for breakfast ! yeah, investor just don’t invest for the culture alone, I know that , but yeah the numbers are not bad either ![]()

10 Likes

I am not really the one who would identify moats as such in any business…but yes…there are evidences we can sometimes find that make a certain business special…

so here are my 2 cents of those “evidences”

-

BMW and KTM are rival companies and yet both have the same supplier…that speaks volumes about the supplier

-

The customer stickyness is there for sure…Kubota was one of their first customers and not only has it stuck all along the way…but even brought in ESCORTS with the new JV with them

-

When a big Auto company (like say BMW) choses a vendor for it to supply for the next 10 years…the price is not the only consideration in their minds…the bigger consideration is…

WILL THIS SUPPLIER BE AROUND AFTER 10 YRS??

WILL THIS BUSINESS BE SUSTAINABLE IN THE NEXT 10 years??

I think…a company like BMW chosing them as a supplier actually makes our work as an investor easier….as they have a better connect with the company and they find the business good enough to be around for the next 10 years…or whatever is the length of the supply contract…

These few points and a bit more….which i discussed with Jay Shankarpure samvad on his youtube channel….

from time stamp….22:20 to 26:40

hope that helps ![]()

25 Likes

The stock has seen quite a steep run-up in the past year or so, and trades at a P/E somewhere in the mid/high 20s.

Would love to know the thoughts on current valuations of the stock by senior members on the forum (inviting @ayushmit especially)

While I have no doubt that this is a good business, but a microcap trading at these valuations is making me a little uncomfortable.

Just as a comparison, Suprajit Engineering (another auto ancillary player but much bigger than RACL) is trading at a P/E ~30

Disc: Hold both of the above mentioned stocks, not a recommendation.

RACL is my largest holding, forms ~20% of PF, has been a 5.5x for me from my avg. buy price and a 10x from when I started buying

4 Likes

my two cents:

- exit when you hv had your enough… PE re ratings are always difficult to ascertain… dont seek for justification… time horizons, entry price pts and port weights are different for everyone… so its relative…

- capital is limited… if you hv another opportunity wherein you think you can get more returns… consider accoddingly…

all the best

1 Like

Trading at market cap of 700cr+ is underrated as Institution will not take any position till it crosses certain level, if they create entry will make upper circuit & exit it will lower, so they will stay away, may be PMS holders personal holding may be there, as it’s into niche segment, inflation & corona immune we have experienced, as the segment it belongs to the level where price is not a concern for the end customer, as big brands tie up with this small cap & sticky ness is obvious as they have been for decades with them, as promoter point of view from a plant head to entrepreneur journey has been a roller coaster, turned around story in India doesn’t fit well but this is an exception, valuation is justified my point of view, D/E is bit higher but has a reason for that , will watch closely how they add more capacity with adding more brands.

2 Likes

BMW Motorrad has published a press release today with the sales details of entire 2021 and what is in store in 2022, they have seen growth everywhere in 2021 and expect to go even stronger in 2022:

For me, the highlights are these ![]() as a proud RACL Shareholder:

as a proud RACL Shareholder:

Looking ahead at 2022.

Markus Schramm, Head of BMW Motorrad: “I look forward to 2022 with great confidence as we start the year with what is sure to be the strongest product offering ever. Our four cruiser models from the BMW R 18 model family are entering their first full year of sales together. In addition, in the first few months of 2022 alone, the market launches of the all-electric BMW CE 04 and our four superior 6-cylinder models K 1600 GT/GTL/B and Grand America, which have been further improved in all respects, are absolute highlights in our range and will generate a further sales drive in the first half of the year. We also have a lot planned for the second half of 2022, so our customers and fans are in store for a number of surprises.”

24 Likes

Quarterly results…exchange time 6.35 PM today

awaiting seasoned @msandip to comment on the results…1st glance, not the result that will set the price on fire mode…and of course, we can wait for the concall

2 Likes

Just a guesstimate on what could have gone by :

Inflationary pressure is well known, so impact on margins was known.

Growth could have been better but hearing out concalls of export focussed companies, container issues have not yet been resolved completely impacting dispatches and other expenses reflect the same (increased container charges in my opinion).

2 Likes

Look closely.

- Gross margins are stable to a little bit better.

- Operating margins are lower. This was to be expected on 2 counts : new capacity is ready but it takes time to validate & ramp up utilisation. But operating costs won’t be 0 in the mean while. Reflecting in depreciation, employee costs.

- Other expenses are where all the pain is. Imo this would largely be on account of freight costs. Will and should ask in concall.

I think this is a good set of results. Gross margins are good. Which indicates ability to pass on price increase (or maybe they didn’t suffer rm price volatility).

Key trigger here would be significant ramp up of new capex. Have to check latest timeline with management. I think last time timeline indicated was q1 fy23 or q2 fy23.

Disc : invested, biased.

16 Likes

Agree @sahil_vi.

Revenue of 75Cr has been best ever in its history, maintiaining the gross margin as well. Other expenses has been increased by 4Cr than last quarter and add to that the increased finance cost of 1Cr due to increased debt for capex. These 5 Cr would have been added directly to bottomline, but this pain is worth taking anticipating the upcoming ramp up of capex cycle.

If we consider 75Cr quarterly revenue run rate, RACL has already reached 300Cr revenue target, I guess they are well on track to achieve 500Cr revenue target by 2025.

Disc: Invested and biased, not a recommendation.

18 Likes

The “Other Expenses” have increased by 4+ Cr. This is the elephant in the room (on a 7.5 Cr. PAT). We need to get clarity on this header during the conf call.