@sensaptarishi and I were discussing Punjab chemicals as an interesting stock idea in the agchem space. I will summarize my understanding of the company and we can see if there are others interested in collaborating.

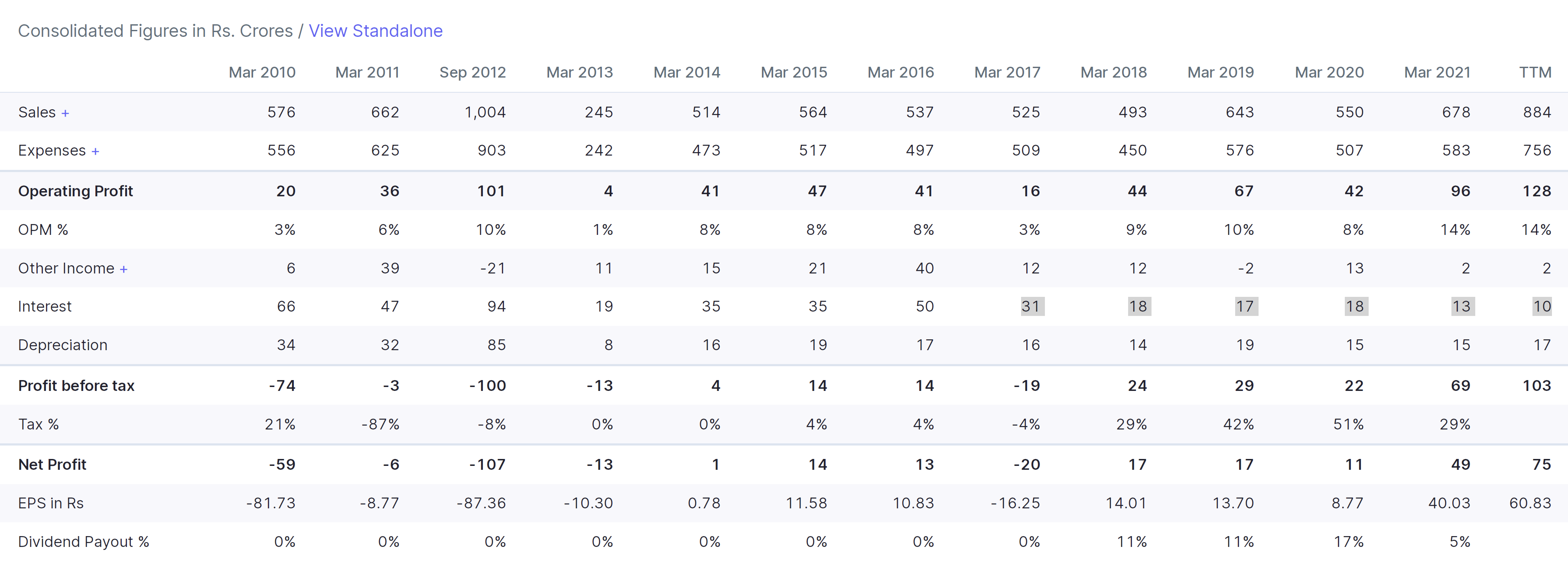

History: Company went on an aggressive debt funded acquisition spree in 2003-08 to acquire marketing capabilities in agrichemicals in developed markets. This backfired in 2008 when there was a global slowdown and one of their factories had a large fire event, leading them to default on their debt obligations. Things started changing around 2016 when there was a change in their business model, from marketing pesticides on their own to manufacturing active ingredients (or technicals) for other companies (mostly UPL at that time). A lot of noncore assets (offices, leased factory, etc.) were divested and promoters lent money (through ICDs) to company for settling their debt.

This started reflecting in financials where interest costs decreased from peak of 50 cr. in FY16 to 13 cr. in FY21, and margins approached double digits.

In 2019, they had a fire incident in their main agchem facility in Derabassi facility which led to muted FY20 numbers. Performance improved in FY21 and margins expanded to 14%. FY22 has been a bumper year so far, where sales has grown by 30%+ and margins have approached 15%.

I will now summarize my understanding of the company’s operations. They have three main business divisions

- Agrichemical technical manufacturing (60-65% of sales)

- Intermediate manufacturing (~20% of sales)

- Industrial division (food grade phosphoric acid) (<10% of sales)

Agrichemical Technical division

- Enters into long term contracts (5-year) with MNCs (main customers are UPL, Nippon Kayaku, Adama, Corteva, Kuvera) to manufacture AI for finished formulations. This gives revenue visibility + attractive gross margins (38-42% vs generic AI gross margin of 25-30%). Company claims that shipping costs are included in these contracts

- They have 5-6 molecules making 100 cr.+ sales (major ones: Metamitron, Metconazole, Diflufenican)

- 30% revenues come from patented molecules (currently 4 molecules, I don’t know the names)

- Capex is partly funded through customer advances (50-50 split)

Intermediate division

- Have established new relationships with pharma companies (Mylan, Laurus, Divis) to manufacture advanced intermediates to supply to European markets. These do not require EU audit, however their customers do regular (i.e. pharma cos) audits

- FY22 revenues should be 130-140 cr. These products are import substitution in nature

Industrial division

- Has a capacity in Pune that makes food grade phosphoric acid that is supplied to beverage manufacturers (Coca, Pepsi). They have been suppliers to their India operations for 20+ years

- Earlier, supplies were limited to their domestic factories (45 cr. annual revenues in FY21). Recently company has managed to get supply contracts to their other Asian factories (Korea, Singapore and Thailand) and this segment is currently doing 80 cr. annual revenues.

Growth plans

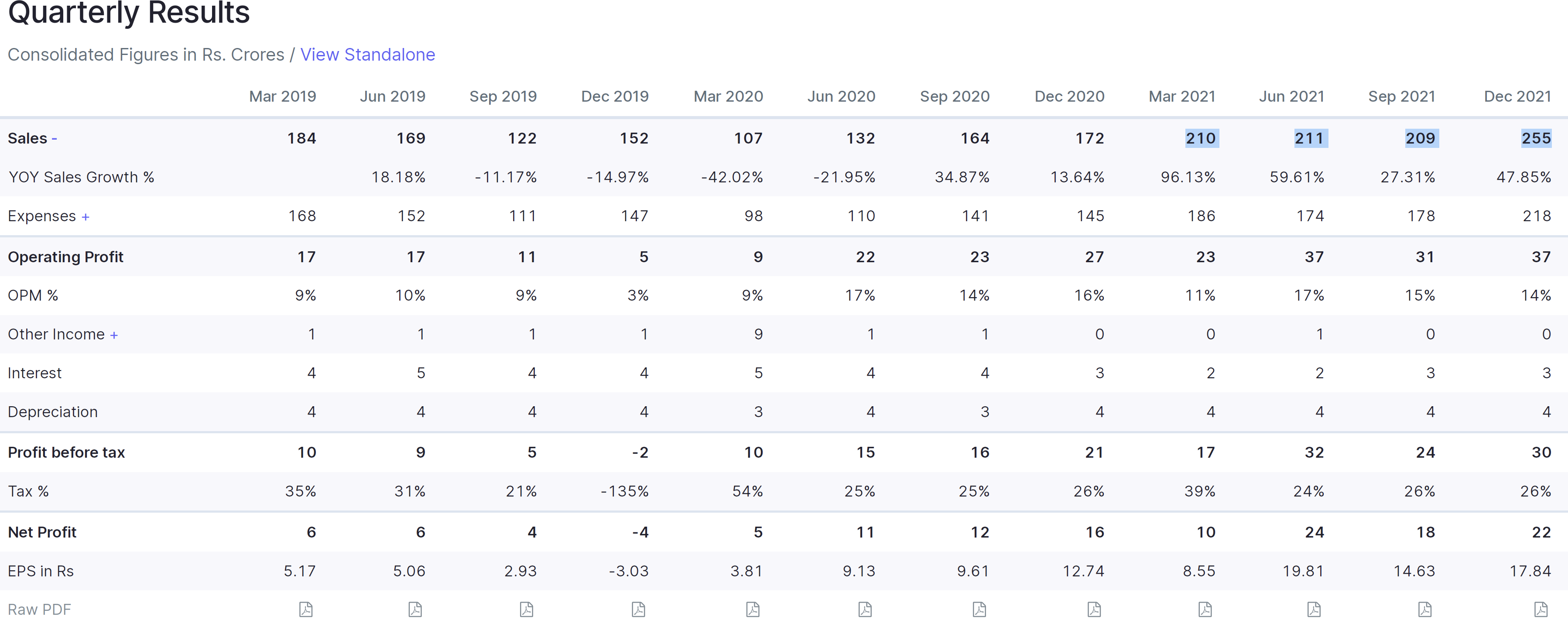

FY21 and 9MFY22 sales growth has been strong at 23 and 30% respectively. FY22 growth has largely been due to 3 new products (one with Nippon Kayaku, one with a Singapore based company which mostly likely is Syngenta, and the last one is an Indian customer). Contribution from these 3 new products has been ~20% of FY22Q3 sales (i.e. around 50 cr.). So on annualized basis contribution would be around 200 cr.

Management is targeting 1500 cr. revenue by FY24/25, 60-65% of this should come from agchem (900-1050 cr.) with remaining coming from intermediate and industrial division. I feel they can do 1400-1500 cr. sales by FY25 and I am sharing the maths around it below.

Projections for FY25

FY22 intermediate sales ~130 cr., this can increase to 250-300 cr. once their validation batches with Divis/Laurus/Mylan go through. These are new products and import substitutes (and don’t require FDA/EU audit). They have not disclosed product names.

FY22 Industrial sales ~ 80 cr. (vs 45 cr. in FY21), this should increase to 150-200 cr. given that they have started supplies to other Asian factories of Coca and Pepsi. Currently, they are struggling for capacity and are looking to lease out another factory in Pune. Management has mentioned that Coca/Pepsi want to increase supplies from Punjab from the current 1-2% to 15%, I will take the 15% number with a pinch of salt. However, even an increase to 4-5% can mean sales of 200 cr+

Now, this leaves 1000 - 1100 cr. from the agchem division [1500 – (250-300 from intermediate) - (150-200 from industrial)].

To reach this level of sales (from FY21 level of 513 cr.), they need to have a portfolio of 10-15 molecules (assuming 70-100 cr./molecule). In FY21, they had ~5 molecules contributing 100+ cr. In FY22, they commercialized 3 new molecules. This implies they need to maintain sales for these molecules + add a couple more molecules in the next 3 years which is very plausible. So the main bet in this story is strong sales growth in their agri division + margin increase.

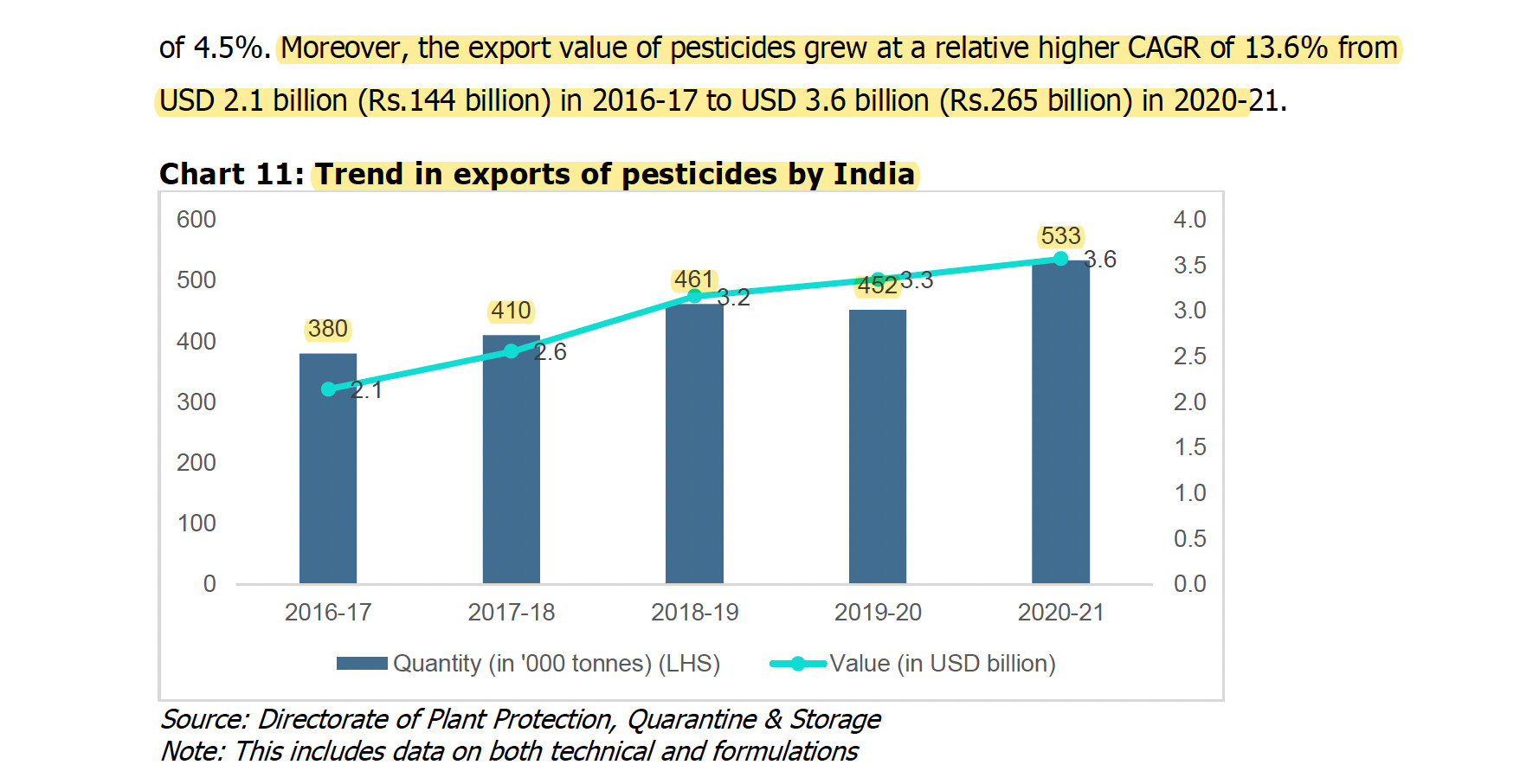

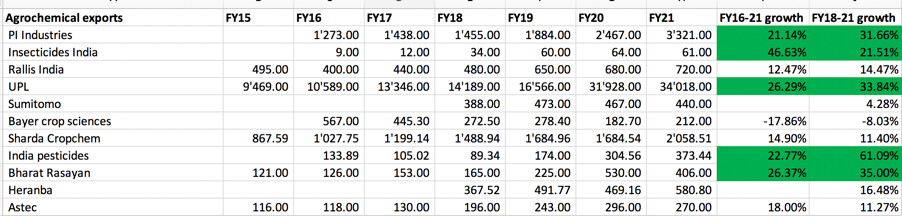

To put a bit of context, exports has been growing at very high rates (20-50% CAGR) for a large number of domestic technical manufacturers since FY18 (details below). Most of this growth is due to supply chain diversification strategy followed by the innovators (who control 75% of global agchem market).

The current Mcap of Punjab is ~1740 cr., if they achieve 1500 cr. sales, then there is quite a bit of money to make. Most of the large agchem technical exporters are currently valued at 4-6x EV/sales (except those with past governance lapses like Meghmani or Heranba). For Punjab to get those multiples, margins should increase to the industry standard of 18-20%. I feel Punjab can do much higher margins because their gross margin (of 40%) is higher than its peers. Most companies make 30-32% gross margin except PI which makes 45% kind of gross margin.

I will summarize my work on their molecules and major customers in the next post.