AR23 notes

Quick summary:

- Top two customers account for 55% of sales (vs 62% in FY22)

- They have lost a major contract due to registration issues (more in description below)

- Management is investing in team + capabilities to grow business

AR23 notes

Miscellaneous

- Portfolio of 12 products (vs 10+ in FY22) in contract manufacturing for MNCs and Indian companies

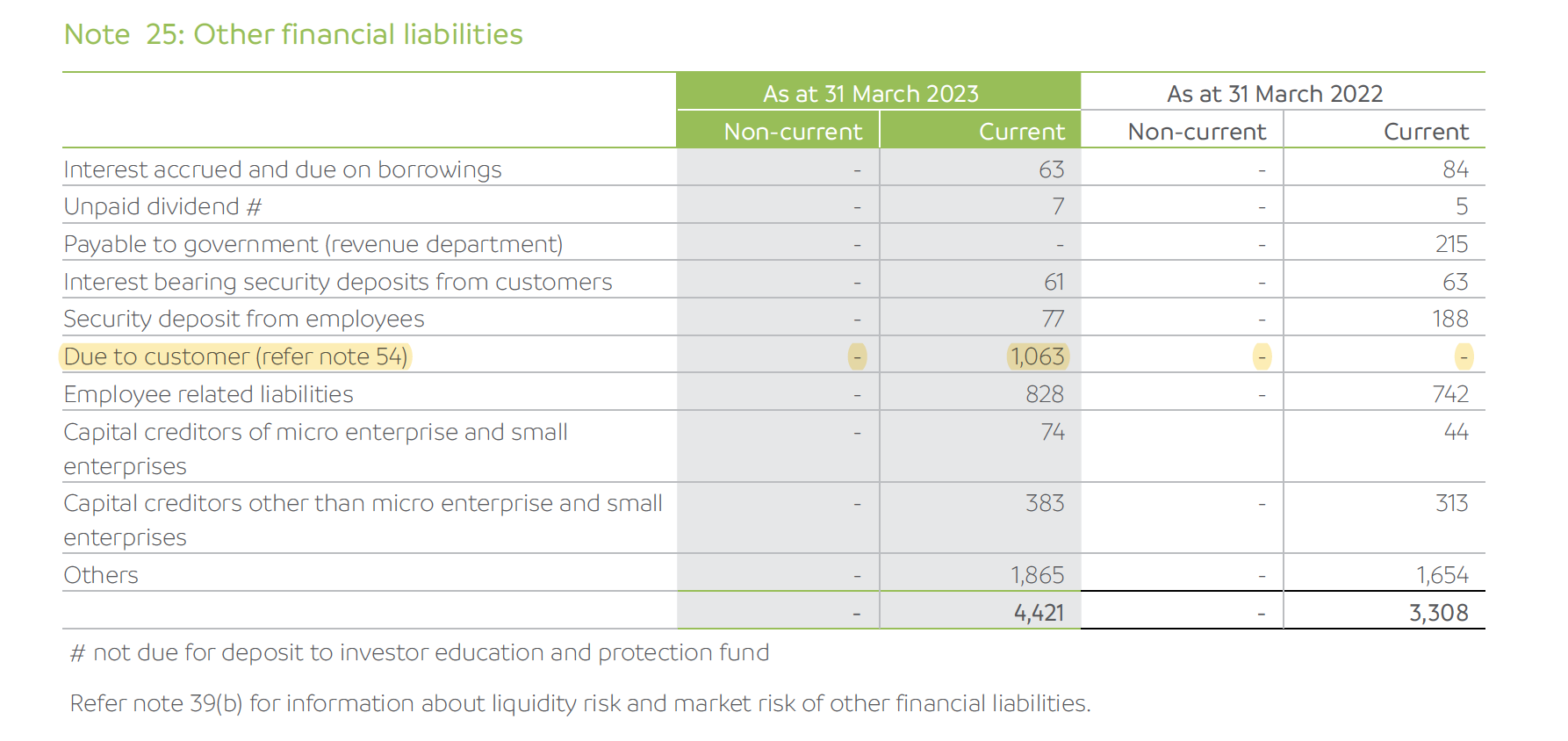

- Had an item called “due to customer” of 10.63 cr. This is relation with an overseas customer and loss of contract due to registration issues . During FY23, as a result of product registration regulatory issues faced by the customer , the Company and the customer have preferred to enter into a settlement arrangement pursuant to which the original contract for supply of goods now stands terminated. Company has recognized 2.84 cr. as settlement income (net of certain expenses aggregating to 2.25 already incurred pursuant to the original contract of supply)

- During last two years, have invested in building new managerial positions, inducting professional talent and investing in research. Widened capabilities across more chemistries

- Enhanced process yield, decline in energy consumption per unit of output. Looking to use new hybrid technology to moderate power and fuel costs.

- Used idle manufacturing capacity for new product development in existing and adjacent product spaces . These products are awaiting customer approval while some others are at a pilot production stage

- Looking to double proportion of revenues from new products

- Continued to transform its approach from product sales to being solution providers

- Macro issues: floods, droughts, increased power, fuel and freight costs, geopolitical challenges

- Has approved Effluent Treatment Plants with incinerators to treat the waste materials in Derabassi and Lalru. For disposal of solid waste, it has a tie-up with Common Effluent Treatment Plants close to manufacturing sites. Both are zero liquid discharge facilities

- Installed MVRE (Mechanical Vapor Recompression Evaporation technology) to ensure zero liquid discharge. Installed scrubbers in its boilers to control emissions. Undertook asset upgradations, such as installation of multi-effect evaporator for water treatment

- CSR : Spent 1.33 cr. (vs 75.94 lakhs in FY22)

- Employees : 1228 (vs 1213 in FY22) + 530 (vs 867 in FY22) on contractual basis

- Share price (low): 821.7, (high): 1597.95

- Shareholders : 21’029 (vs 19’419 in FY22)

- Average increase in employee salaries (ex-managerial) was 12.46% (vs 10.34% in FY22) and managerial remuneration decreased by (-18.96%) (vs 43.65% increase in FY22). Managerial remuneration decreased due to superannuation of some KMPs

- Management remuneration : 6.94 cr. (vs 6.04 cr. in FY22) (1.18 cr. was commission vs 2.26 cr. in FY22)

- R&D : 3.01 cr. (vs 3.3 cr. in FY22). Out of this, 0.77 cr. was capitalized (vs 1.45 cr. in FY22)

-

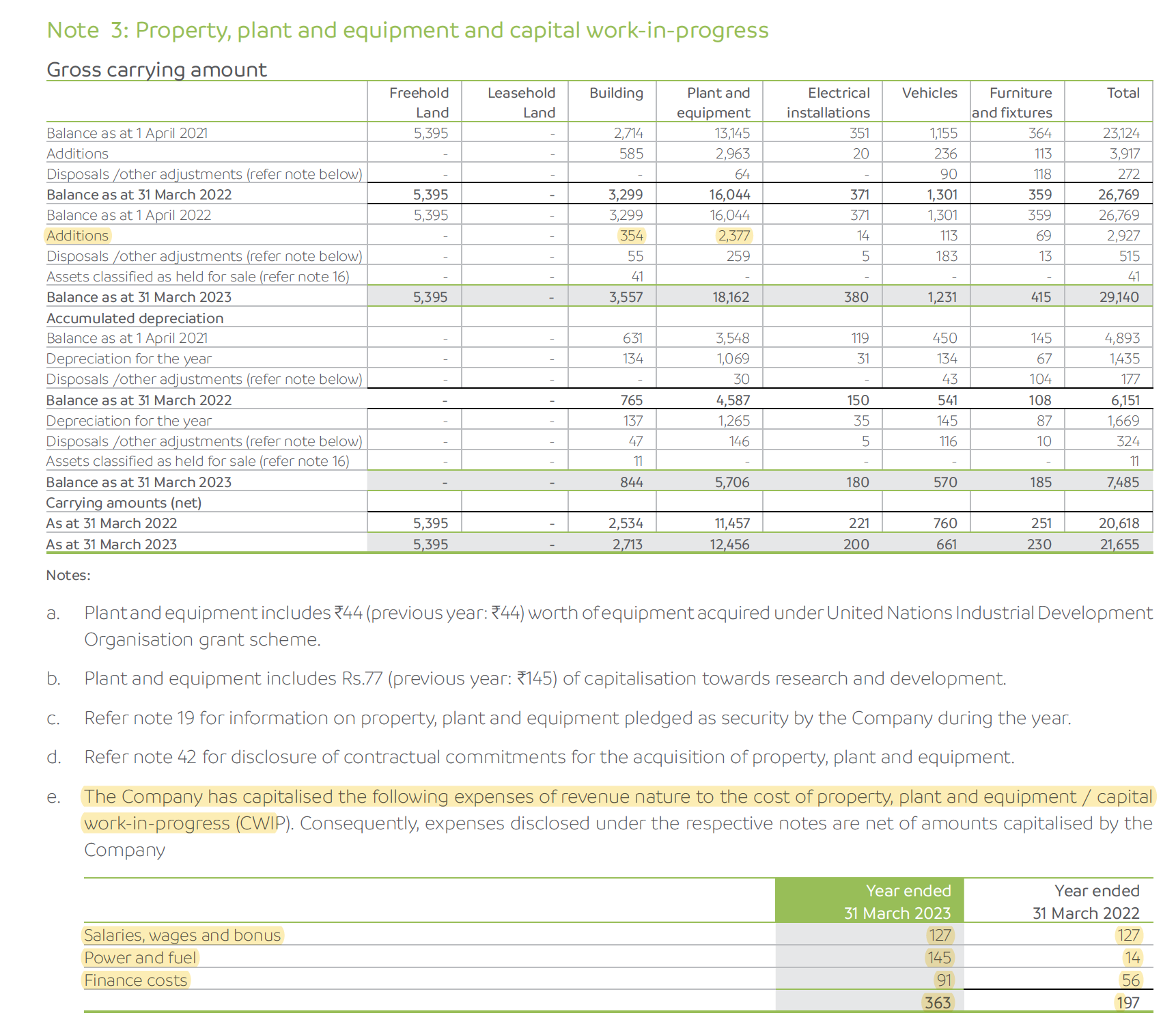

Capex: capitalized certain part of operating expenses in CWIP

- Did not hedge commodity or foreign exchange in FY23

-

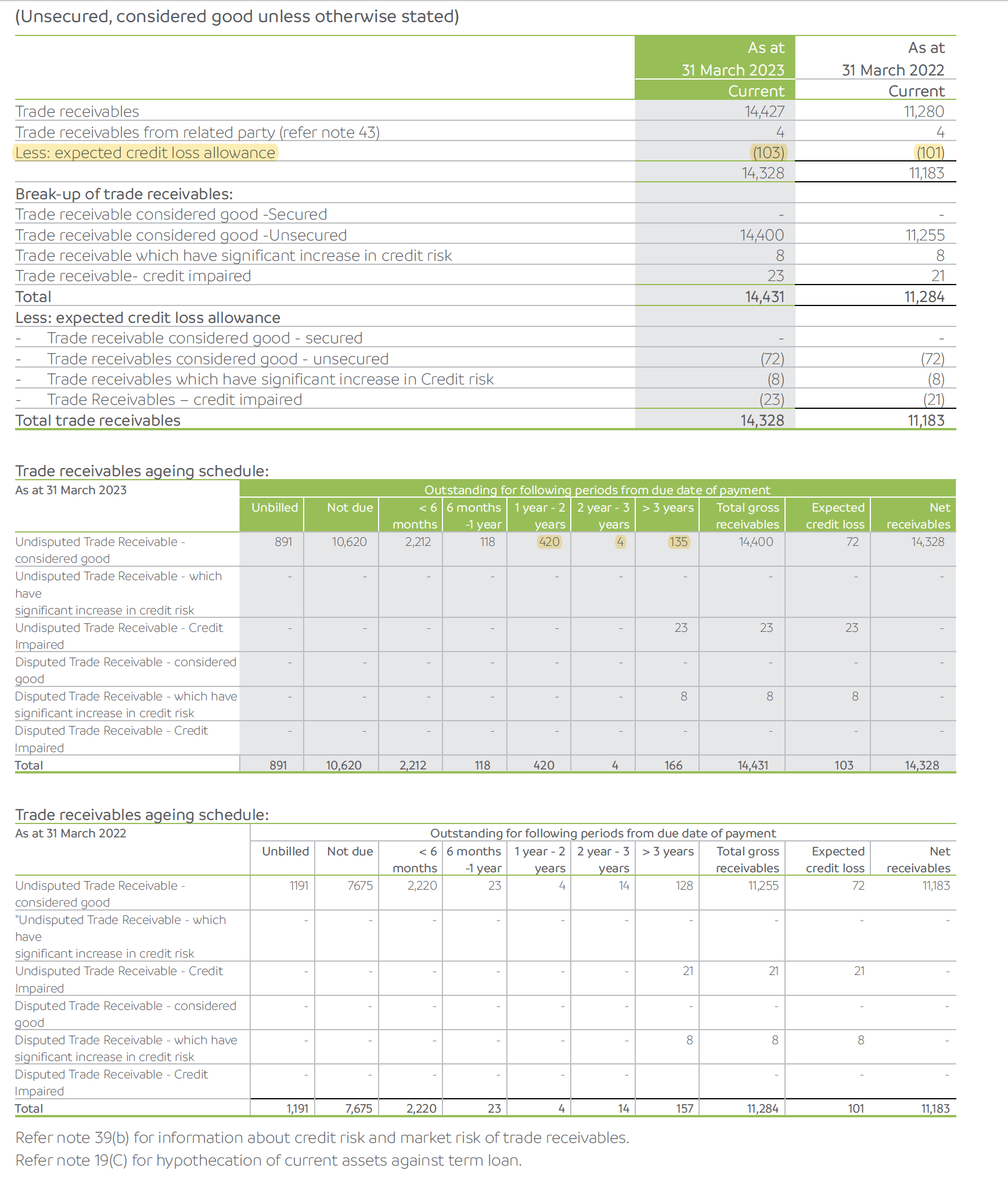

Receivables : Provisioned 1.03 cr. (vs 1.01 cr. in FY22). >1 year receivables increased to 4.6 cr. (vs 1.46 cr. in FY22)

- Customer advances : 6.96 cr. (vs 18.6 cr. in FY22)

- Revenue from top 2 customers was 414.44 cr. (vs 503.71 cr. in FY22) and 138.68 cr. (vs 75.83 cr. in FY22)

- Contingent liabilities : 22.86 cr. (vs 13.41 cr. in FY22). All are tax related

- Auditor remuneration : 38 lakh (vs 34 lakh in FY22)

- Foreign outgo : 139.58 cr. (vs 114.58 cr. in FY22); translates to 13.87% of sales vs 12.27% in FY22

Revenue breakup:

- Agrochemical division Derabassi: 739 cr. (vs 664 cr. in FY22)

- Specialty chemical division Lalru: 153 cr. (vs 156 in FY22)

- Industrial chemical division Pune: 116 cr. (vs 111 cr. in FY22)

Geographical revenue breakup:

- India: 395.42 cr. (vs 426.96 cr. in FY22). In domestic revenues, sale of services was 97.36 cr. (vs 126.11 cr. in FY22)

- EU (including UK): 414.47 cr. (vs 360.71 cr. in FY22)

- Japan: 54.33 cr. (vs 89.8 cr in FY22)

- Israel: 40.03 cr. (vs 10.48 cr. in FY22)

- USA: 29.36 cr. (vs 1.81 cr. in FY22)

- LATAM: 27.22 cr. (vs 4.9 cr. in FY22)

- Others: 17.85 cr. (vs 22.4 cr. in FY22)

- Exports go to 29 countries

Banking relationships

- Term loan from RBL bank at 11.25% interest rate is repaid fully (vs 4.96 cr. in FY22)

- Term loan from SVC Cooperative bank is at 10.85% (vs 9.7% in FY22) (36.94 cr. vs 44.58 cr. in FY22)

- On 20 April 2023, availed working capital term loan under ECLGS scheme from SVC Co-operative Bank Ltd. for 15 cr. (0 in FY22) at 9.25% interest rate. Loan has a moratorium of 2 years from the date of first disbursement and is thereafter repayable in 48 equal monthly installments

- ICDs were 15.85 cr. (same in FY22) at 12.75-16.50% interest rate

Total income of SD Agchem (Europe) NV was 17.52 cr. (vs 12.58 cr. in FY22) with profit after tax of 0 cr. (vs 2.89 cr. in FY22)

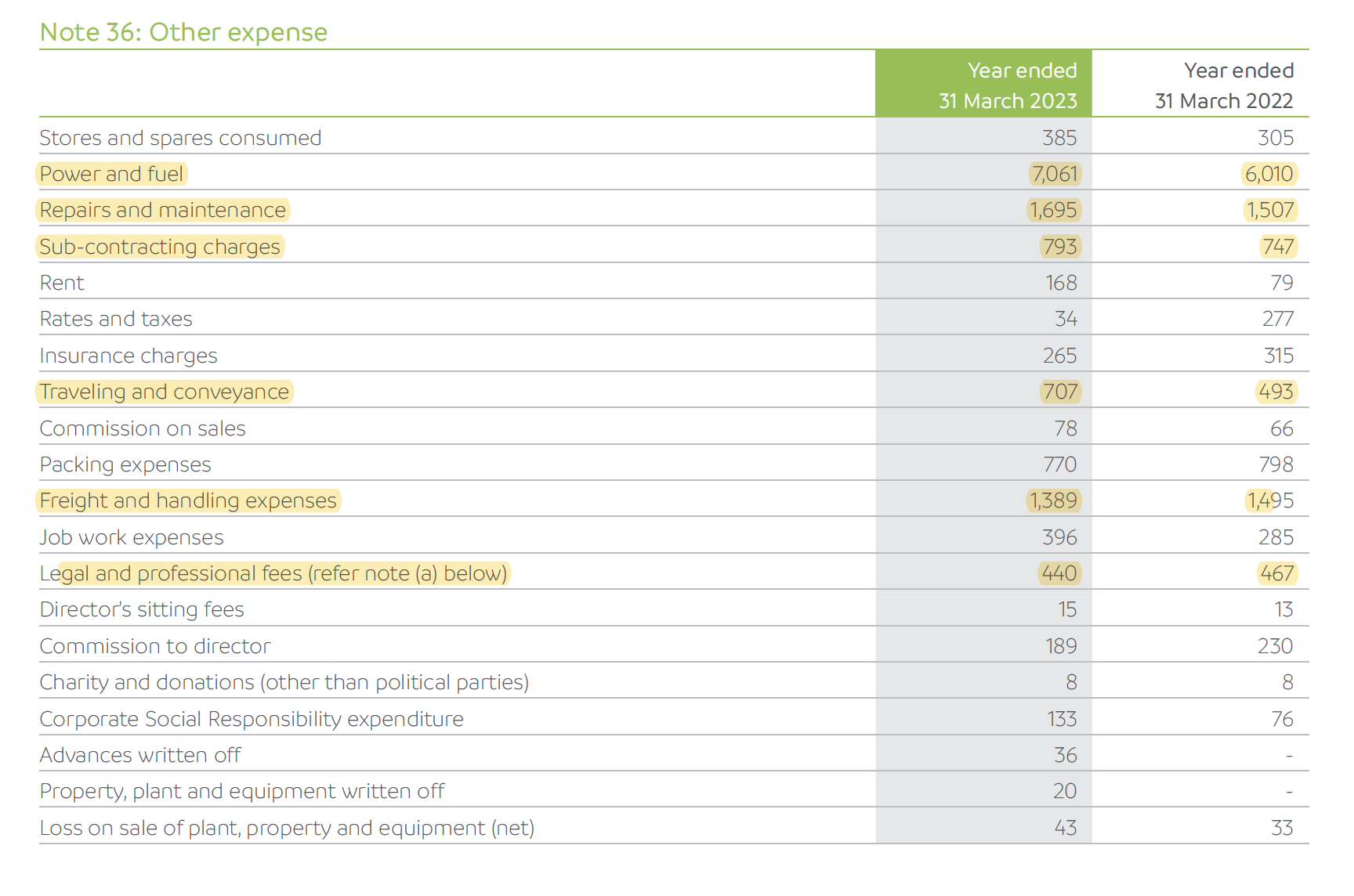

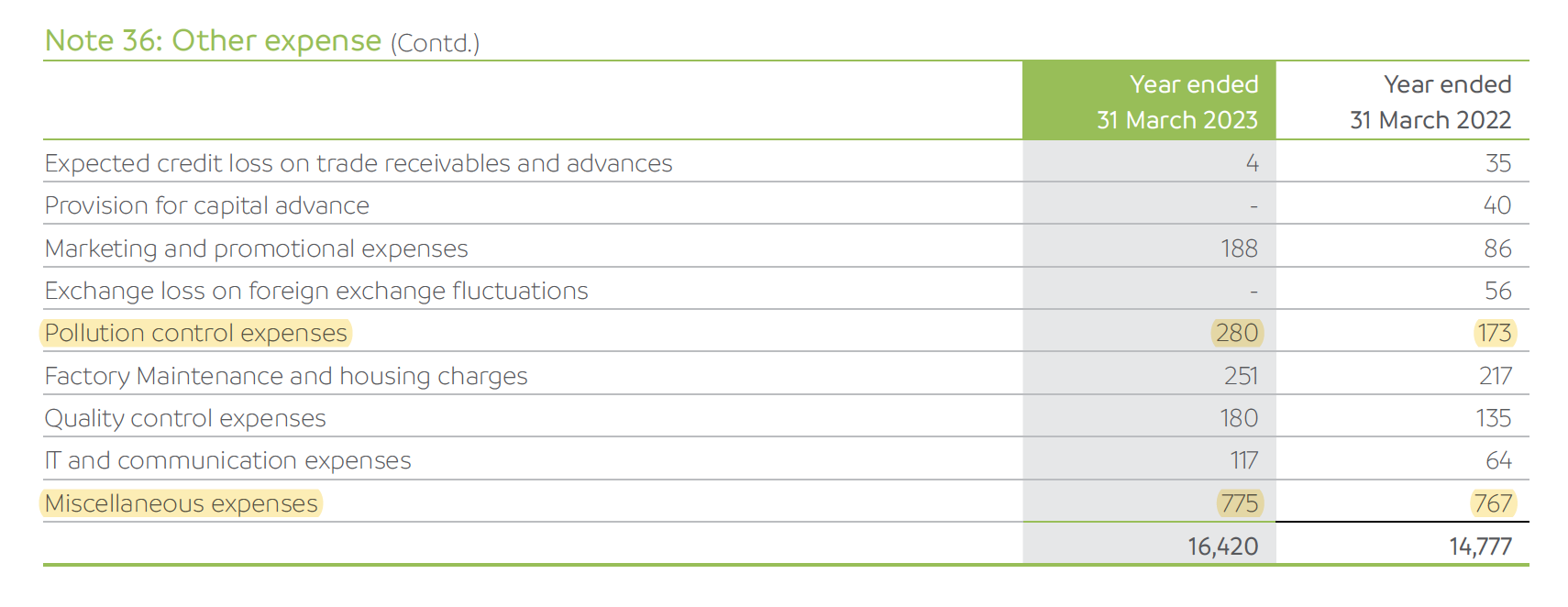

Other expenses breakup

Disclosure: Invested (position size here, no transactions in last-30 days)