Hello everybody, I’m Puneeth a 15 year old investor from Bangalore. I began investing on October 20th 2021, after my mother telling me to begin investing while I was still young. I’m usually curious about new things, and I loved reading books on the same. I began with Intelligent Investor(as one does) and then read books by Peter Lynch(which are still by far my favorite). Soon I started working much more on investing, as it sparked my curiousity as a scientific art, not purely quant based nor is it purely narrative. I now genuinely learning more about investing and recently I have started to learn a bit more TA as well(keyword - started).

As I am in summer holidays, I have spent >8 hours on most days on investing/reading, whereas on most days with school I would work for 2 hours or so with genuine interest.

All book recommendations are welcome whether they are about investing or not(currently on The Biggest Bluff)

Aim

- To learn as much as possible on all methods and types of investing without discrimination(TA, FA, long term, short term, BAAP, Buy and Hold, High Churn, Momentum, Contra Deep Val, Concentrated, Diversified, Timing the markets etc.)

- To achieve 50% annualised returns over a decade out.

- Volatility is fine but aim to never blow up(Stoplosses etc.)

- Never stop doing brownfield capex on myself

Why I aim for a highly unlikely 50%?

My aim for 50% CAGR returns for the next 10 years sounds like a very very far reach and impossible to achieve without excessive leverage or risk. Even veteran investors like Warren Buffet, Munger, Graham, Templeton, Pabrai, Soros, Lynch, Li Lu or Sleep do lower annualised returns, how would I possibly beat them? For starters, they do manage a much much larger portfolio than mine, where I would have an edge. It also means that I can afford to look into micro/small caps businesses that are out of reach to many. Even though Warren Buffet has compounded his money at 20%+ for 60+ years, it would not be prudent for me to aim the same while starting out. Warren Buffets were much larger during his initial years(where I am) with smaller capital. His initial partnership did 31% over the DJIA’s 5% over the same period. But he has mentioned how in the decade preceding the existence of the Buffet Partnerships he averaged around 50% compound annual returns, killing the Dow. I’m no Warren Buffet, but I will try my best to shoot my shot. My favourite investor Joel Greenblatt also crushed the S&P while returning 45% over 20 years, a legendary track record. He focused on special situations(spinoffs, a lot of them). He also ran an incredibly concentrated portfolio, at one point having 40% of his fund into the spinoff of Marriott(although they are preferential shares with a few privileges). Michael Burry did 50% in his initial years too. Finally, I believe in the growth story of India. I do think the situation for me, being born in the country I was born in, gives me tailwinds.

I believe the target is achievable, but time will tell.

I’m also rapidly expanding my circle of competence, and I will never stop doing Brownfield expansion on myself. I will continue to optimise and improve myself constantly(Kaizen). “Those who keep learning, will keep rising in life” - Charlie Munger. I will live by that statement. I will definitely make mistakes along the way, I will try my best to prevent them, but as they inevitably happen, I will try and learn from them all.

Investment Framework

I’d describe my investment style to be a constant work in progress(as I’m still learning). I focus on companies that are -

- Growing their topline at 30%+

- Have some scope for improving margins

- Have scope to grow their ROCE

- At a reasonable price

- Improving WC situation

- High conversion of EBIT to CFO

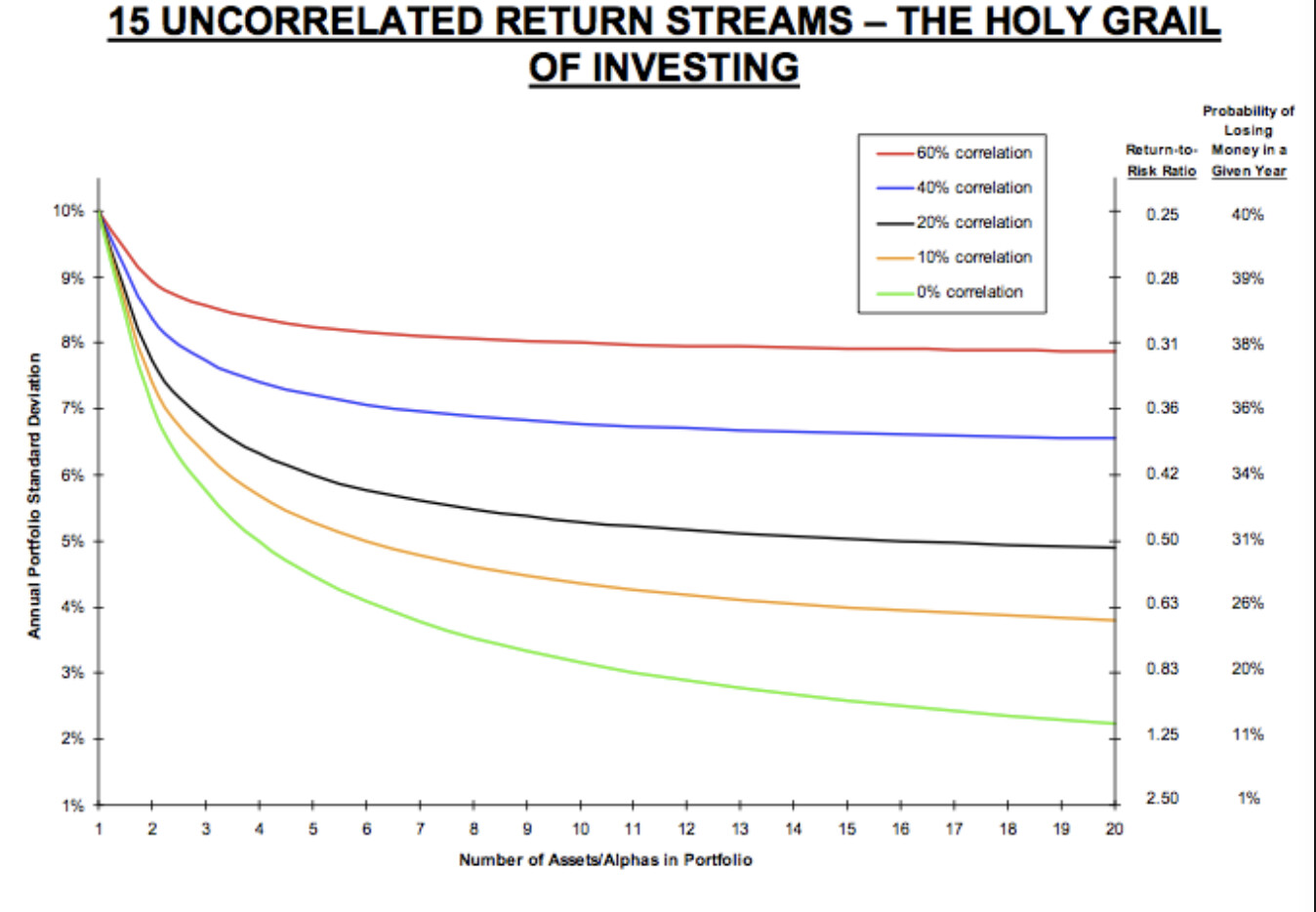

I also maintain a fairly concentrated portfolio of <5-6 stocks. While I agree that the concentration is definitely very high, I will reason out the concentration. The number is loosely based on the stand deviation model for asset classes.

If we take each stock as a separate source of alpha with a 60% correlation, most of the power/safety of diversification is taken by just a few sources of alpha. Of course high concentration has its risks, which I’m willing to take. As of right now(subject to change as I learn) the risk to reward is satisfactory with few stocks.

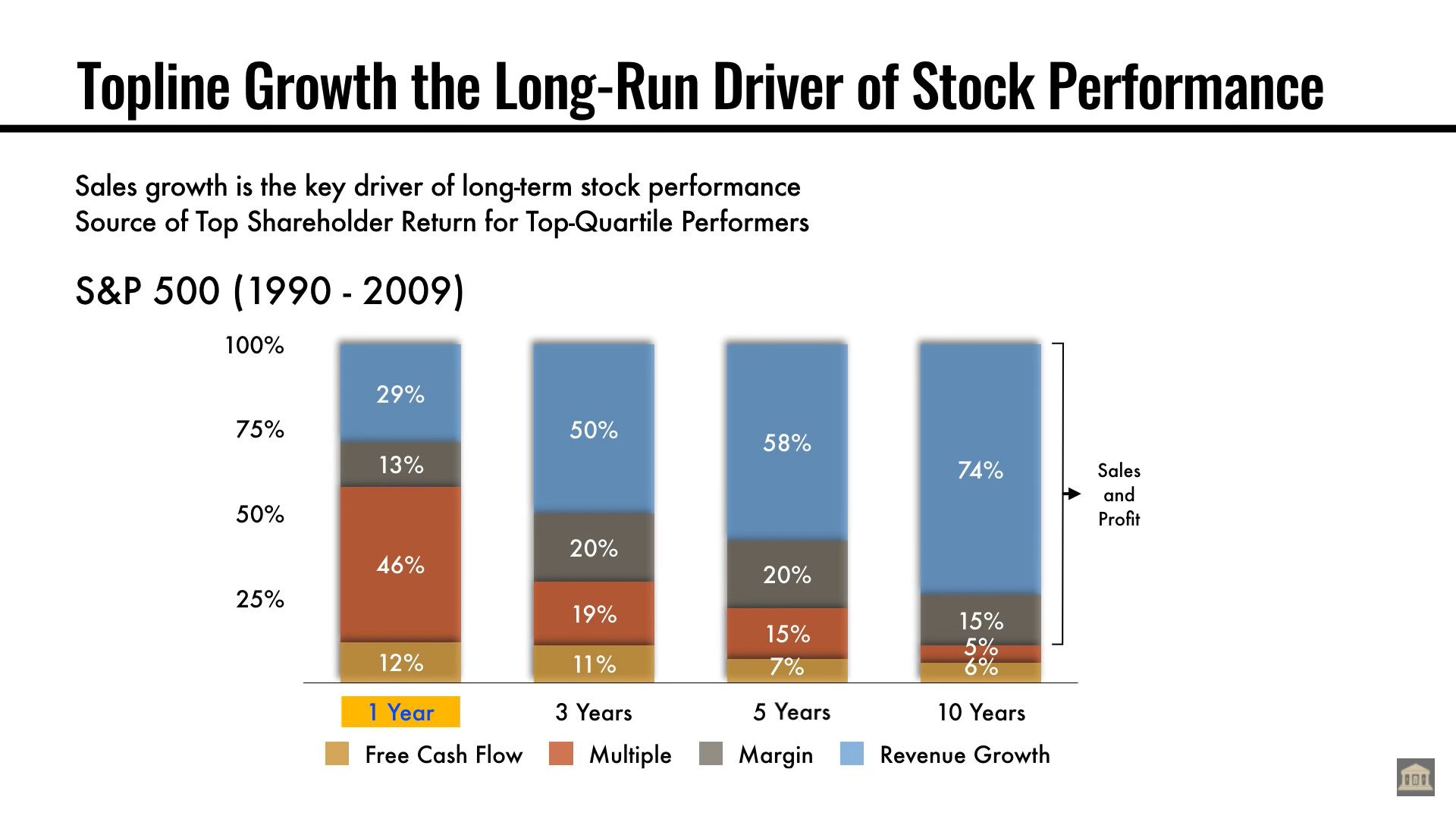

Another point I’d like to mention is re-rating/multiple expansion.

This is a screenshot from SOIC’s video(couldn’t find the report itself). In periods of 1 years and even 2 years, much of the growth other than topline and margin expansion is multiple expansion(a change of narrative). Sometimes I ride a trend thats already taken place but in certain cases I like to find companies that can re-rate and show some multiple expansion. Many times a case can be made for multiple expansion on the back of ROCE growth in the future.

Usually if the re-rating has taken place it leads to muted stock movement unless held for very long term.

I also have a higher rate of churn. I don’t buy stocks for long term, or rather I don’t see the point for my small capital to not take advantage of the fact that I can move in and out of stocks in a flash. So I don’t like to tag myself as a long term investor. I’d like to further elaborate this point by giving the example of Warren Buffett.

In his early career(pre partnership days, right after meeting Ben Graham), he would buy and sell stocks rapidly, even more than the quoted 400 stocks in a decade(number is from partnership where he averaged 31% in alpha), before which he did 50% in alpha over the Dow. As an investor, I do believe an edge can be made by having different holding periods as compared to institutions, which is why I don’t prefer to constrain myself to short term/long term, wherever XIRR is visible/predictable to a reasonable degree I will hold.

Buffett only shifted to long term quality investing when Charlie Munger convinced him that Berkshire could not be scaled with small cap, high churn investment methods, at which point Buffett made the move to the next best option to hold stocks with a wide moat for the long term.

Coming to a sometimes misunderstood and disregarded form of analysis, Technical Analysis. It seems like an overwhelming amount of fundamental investors use Technical Analysis and Supple/Demand analysis for investing like the legendary Stephen Druckenmiller, Paul Tudor Jones, George Soros, Michael Burry, Jack Dreyfus.

I have read both Mark Minervini books, and the classic, “How to make money in stocks” by William O’Neal. I sometimes look into technicals and VCP’s(any form on contraction and tightening towards the right like cup and handles, cups, etc,), confirmed uptrends, channels where one could expect supply or demand etc. It is not a major part of my ideas(eg. bought Krsnaa in a downtrend with high amounts of overhead supply) but I do want to learn it better.

Portfolio

Since I started in October 20th, my portfolio(to date) has returned ~16.8% whereas Nifty started its downfall immediately since then and has returned -9%(I have booked profits in the past in Fineotex Chemicals, Affle, and breakeven on Tanla)

My current portfolio stands as such -

| Companies | Weightage | Ccst |

|---|---|---|

| Coffeeday | 5.6% | 30.1 |

| Gujarat Fluorochem | 19.5% | 2234 |

| Krsnaa | 34% | 605.3 |

| Cash | 40% | N/A |

-

Coffeeday - I bought this at the time I read Intelligent Investor, as it was a net-net. I read through their turnaround plan by management, where they elaborated on some of their assets, and I decided that it could be an asset play and was definitely not a worthless company. When I bought the company they had put Sical Logistics to sale(sold a couple of months back I believe), I believed there was some value to their coffee estates, they had 3300 crores in receivables from MACEL of which I believed atleast some could be recovered, they had a lease from The Jesuits on their corporate building in Bangalore which I believed could be with 100 crores or so. Promoters also never sold their shares(only invocation of pledged shares) and even though the company wasn’t of great quality or health I bought it. I do plan on selling(results today).

-

Gujarat Fluoro - The thread in valuepickr will do much mroe justice than I can.

-

Krsnaa - I have a full thesis on Krsnaa here and on website [KRSNAA.pdf (72.7 KB)]. But mainly, the diagnostic sector has had a bad time for a while now, and Krsnaa is the company least susceptible to undercutting in the B2C segment while also the fastest growing diagnostics company. The also have pretty low utilisation rates, when the utilisation rates rise operating leverage comes into play. It was also comparatively cheaper than other business(I believe on account of B2G receivables concerns even though govt has always paid out in the past decade)

There are a few companies that I’m tracking right now.

- Sandhar Technologies Limited - full thesis here(and on website)Sandhar (1).pdf (152.9 KB) But mostly buying the trough ROCE, OPM when RM costs are likely to fall(interest cycle at bottom, commodity cycle at peak).

- SJS - Play on premiumisation and 25% or so topline growth, some operating leverage too.

- Rolex Rings - Low Float(6.94% literally) + High DII, Promoter + 22% type growth has proven to be a good recipe in the past.

Out of these companies, Sandhar is the only one that I definitely plan on buying.

Credits

I have learnt a lot from investors like Peter Lynch and Joel Greenblatt(My idol), Mohnish Pabrai, Ashish Kacholia etc.

A few other investors I have learn a lot from include @hitesh2710 sir, @Tar sir, @sahil_vi sir, @ayushmit sir, and of course Ishmohit sir and SOIC team of which I am a member @Worldlywiseinvestors and I have probably learn the most from.