Its a good question that you have asked.

There could be several reasons for 2 stocks in the same industry having different valuations. How are valuations determined? They are obtained essentially by discounting future cash flows using a discount rate. Therefore, any factors that impact either the cash flows, or the degree of their certainty or the discounting rate itself can impact valuations.

Along those lines, the reasons for valuation differences in the same sector/industry could be split into fundamental and perceptional reasons. Elaborating on them below

Fundamental reasons

-

One business has superior ability to generate cash i.e. high CFO/PAT - Both Minda and FIEM score very highly on this. Both companies have low Cash conversion cycle and working capital needs

-

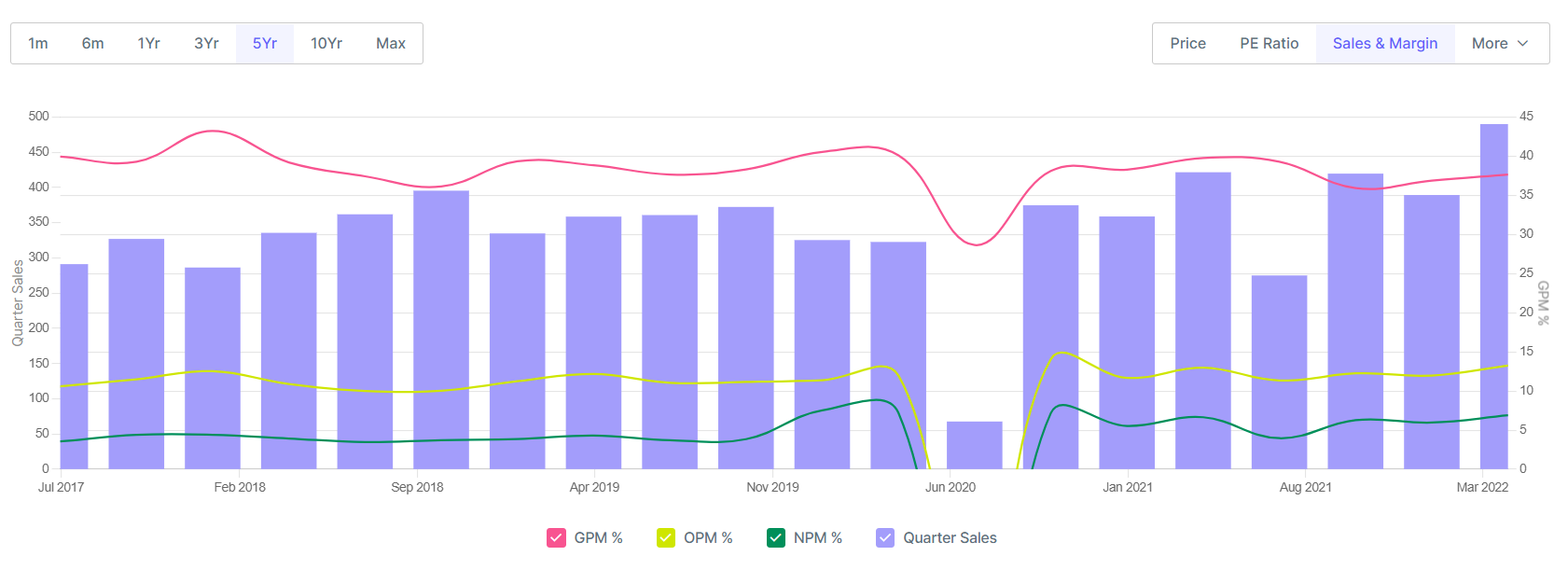

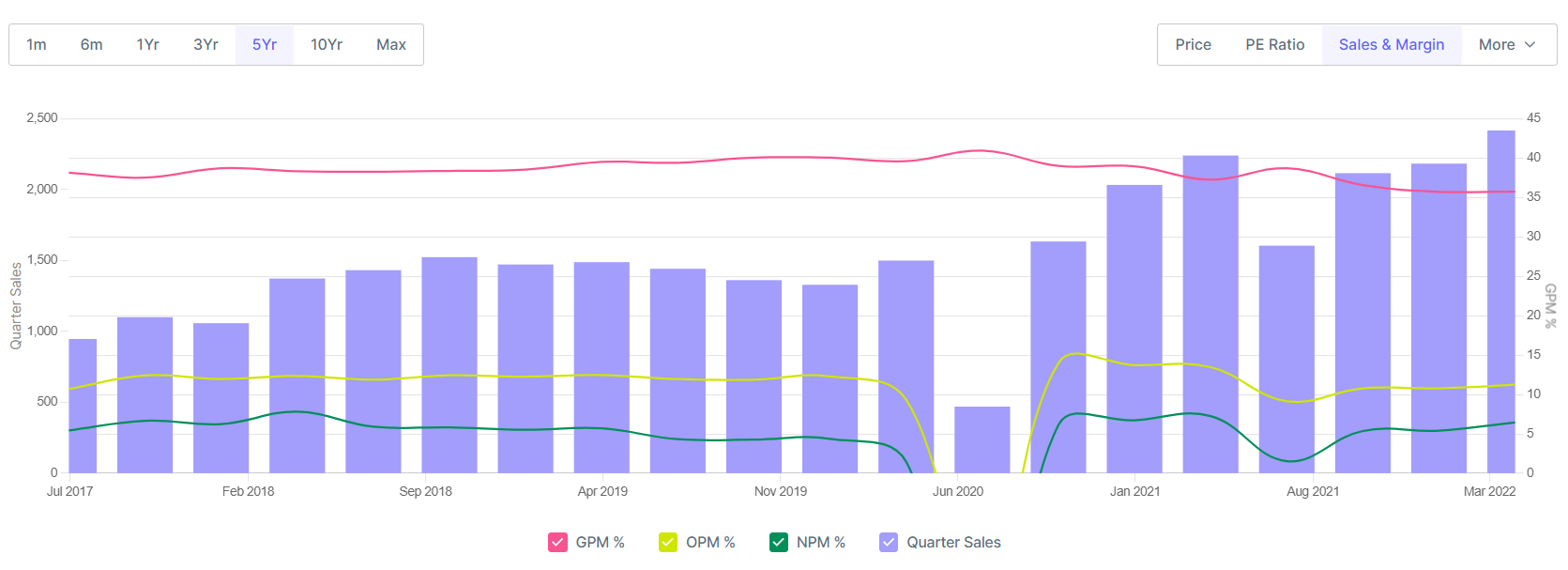

One business has superior gross and operating margins - Once again, FIEM and Minda are pretty much similar here with 35-40% GMs and 10-13% OPMs over the last 5 years

FIEM

Minda

-

One business has a superior capital structure - FIEM scores over Minda here with almost a zero debt balance sheet. Although Minda also has a very, very strong balance sheet with 15x Interest coverage ratio. So while FIEM scores better, investors don’t really penalize Minda here.

-

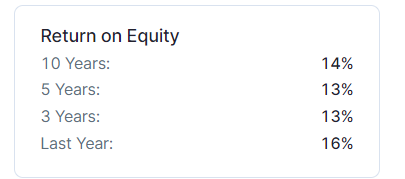

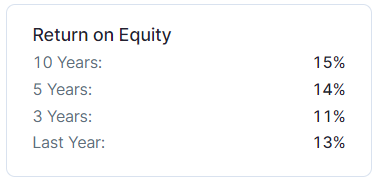

One business has superior return ratios i.e. ROE or ROCE - Again, FIEM and Minda are pretty similar but FIEM’s ROEs are on a clearly increasing trajectory due to higher asset turns resulting from migration to LED lights in vehicles.

5. One business may have higher quality of revenues - By quality of revenues, one means sustainability and diversification of revenue sources. FIEM is essentially a 2W lighting player with diversifications in mirrors and other moulded parts. Minda has far greater diversification with 20+ product categories in the OEM segment. Market perhaps views Minda’s revenue quality to be higher and more de-risked than FIEM’s

FIEM ROE trend is increasing

Minda ROE trend

Perceptional Reasons

-

One stock has lower free float of shares than the other - If you see, Minda barely has 7-8% of its market cap as free float due to high promoter, DII/FII and large retail investor holdings. Whereas, FIEM has about 22% of free float market cap, about 3X as much as Minda. This gives Minda stock an advantage. Lower float for a good company generally means higher than average stock prices as liquidity is low.

-

One stock has higher DII/FII holdings - Clearly Minda has higher FII/DII holdings at 23% vs only 11% for FIEM. DII/FIIs have lower expected rates of return than retail investors because of their well diversified portfolios and long term nature of holdings. Therefore, a higher concentration of DII/FII holdings usually means a higher stock price as DCF calculations will factor in a lower cost of equity. So Minda has an advantage here.

-

One business is tied to a sector which has headwinds at the moment - FIEM’s entire revenues come from 2Ws (96%) whereas Minda’s revenues are split equally between 2W and 4W. The 2W industry is in one of its worst phases right now, with demand well below 2019 levels, where as the 4W PV and CV segments have started picking up already.

Therefore, if you look at the fundamental and perceptional factors that go into deciding a valuation multiple, FIEM is as good if not better than Minda on fundamental parameters but lags well behind in perceptional parameters. Perception is a servant of fundamentals and perception does catch up with fundamentals at some points (Although sometimes this may take an unreasonably long time). Therefore, if FIEM management keeps up this level of execution, I see the stock getting rerated over the next few years. Having said that I don’t expect FIEM to match Minda’s 2.7x P/S ratios. I believe Minda is heavily overvalued at 2.7x P/S. I would peg FIEM’s fair value at around 1.5-1.7x P/S at current levels given recent execution (Take this with a spoon of salt, a large part of assigning a multiple is “art” rather than science). Its a good time to add the stock in my view as the market hasn’t completely discounted FIEM’s increased ability to generate ROE due to LED migration.

PS: Invested and biased

PPS: Would love for other boarders to add to this model of analysing valuation differences. Are there any other key factors that contribute?