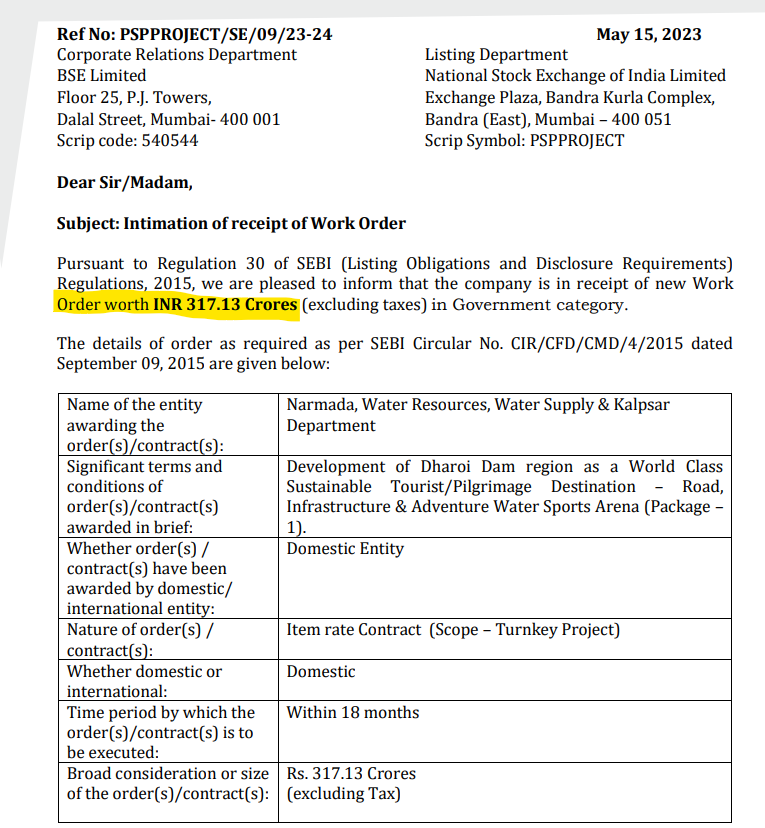

Another significant order win.

With this, the total order inflow during the financial year 2023-24 till date amounts to INR 758.38 Crores.

Another significant order win.

With this, the total order inflow during the financial year 2023-24 till date amounts to INR 758.38 Crores.

This is my take on the company

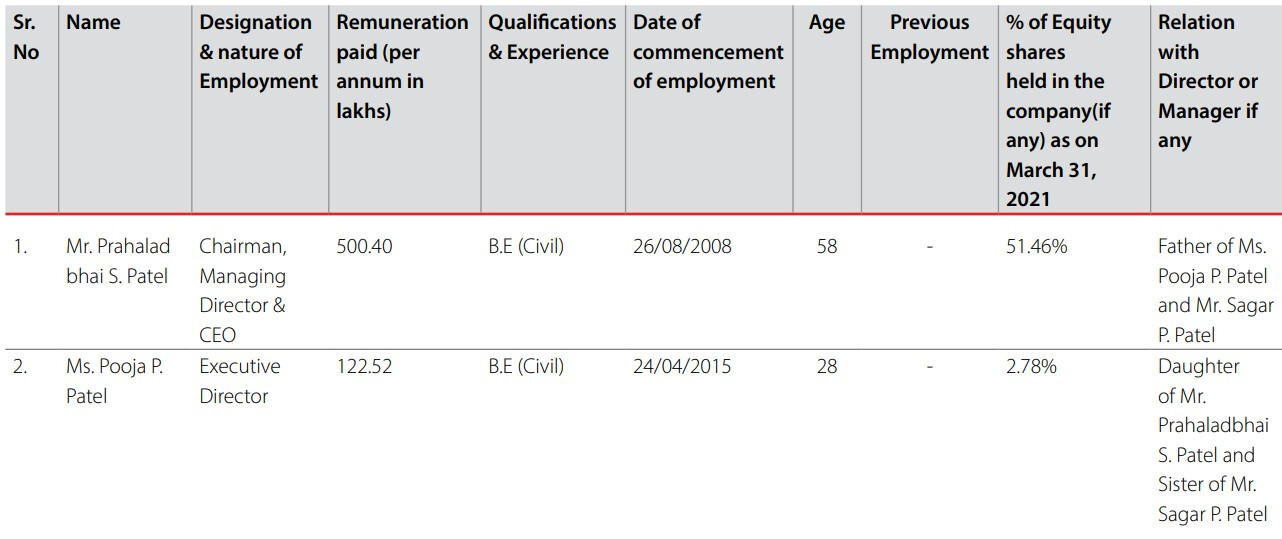

PSP Projects, incorporated in 2008 and led by Mr. Prahalad S. Patel, a first-generation civil engineer with 37 years of experience, has emerged as the second fastest-growing construction company in the small category in India. With its geographically diversified presence across six states, including Gujarat, Rajasthan, Karnataka, Uttar Pradesh, Maharashtra, and New Delhi.

an impressive order book of Rs. 5,052 crores as of FY23, PSP Projects has secured orders worth twice the market capitalization of the company, standing at approximately Rs. 2,700 crores. Notably, the company witnessed a record-breaking order inflow of Rs. 3,421 crores (excluding GST) in the last fiscal year, representing a phenomenal growth rate of 90% compared to FY22.

What sets PSP Projects apart from its competitors is its exceptional financial management. Despite being a working capital-intensive business, PSP Projects boasts the industry’s best working capital cycle of 41 days, ensuring efficient cash flow management. Furthermore, the company has achieved a negative net debt position, demonstrating ample cash reserves to meet short and long-term obligations—an extraordinary feat in the construction and engineering sector, where high leverage is often the norm.

PSP Projects’ client base spans diverse sectors, offering stability and resilience to its revenue streams. While a significant portion of its revenues currently comes from Gujarat, the company has taken steps to diversify its order book, mitigating regional concentration risks. Moreover, the ongoing government initiatives and infrastructure push, combined with a revival in private capital expenditure and stabilized raw material prices, are poised to further fuel PSP Projects’ growth trajectory.

As the company sets its sights on the future, it aims to achieve a robust topline of Rs. 3,000 to 4,000 crores by FY25-26, with a revenue target of Rs. 12,700 crores by March 2024. PSP Projects’ ability to pass on raw material cost inflations to customers, coupled with its efficient asset utilization, has contributed to its high Return on Capital Employed (ROCE), further enhancing its profitability and competitive advantage.

Nonetheless, as PSP Projects expands and ventures into higher-value projects, it will face intense competition from industry titans such as L&T, Shapoorji Pallonji Group, and JMC, among others. It will be fascinating to observe whether PSP Projects can surpass these giants or risk fading away. The company’s strong expertise, timely project completion, and brand recall, as evidenced by its substantial number of repeat orders, provide a solid foundation for success.

Moreover, PSP Projects’ strategic focus on asset-light operations and select high-value segments with favorable margins positions it for sustainable growth and enhanced shareholder value. This is complemented by the managing director’s recent decision to reduce his salary, demonstrating dedication and loyalty towards both shareholders and the business itself.

finally i believe the corporate governance of the company is excellent. the most important risk is that of key man risk- Mr Prahladbhai Patel. he is the one who took the company from nothing to where it is today. although there is succession planning (his daughter is actively involved in the business), this risk is what scare me majorly besides the cyclicality in the industry.

VERDICT- proxy to play the infrastructure theme in India.

Any source on this? Couldn’t find anything about this reduction in investor PPT or concall or Annual Report

It’s there in the annual report

check this out from the 21 ar

in previous years the remuneration of prahalad sir was 540 lk, it was reduced this year.

while the salary of his daughter increased from 102lk last year to 122.52 this year

also another thing is, prahalad sir’s salary was 540lk in 2019 too and didnt increase in 2020 (while the profits of company increased from 90 to 129cr) as he was expecting some disruption. so when the disruption came he reduced it to 500lk

i hope it helps

Wonderful and honest interview

CFOs are really low when compared to op profits on income statement. The company is doing wonders but I do worry about the cash. I guess this is the risk in investing in small construction companies

In the first quarter of the fiscal year 2024 (Q1FY24), PSP Projects Limited, a construction and infrastructure development company, displayed strong financial performance and notable developments in various projects. Their revenue from operations experienced a significant year-on-year (YoY) growth of 48%, reaching Rs. 510 crore. Additionally, their outstanding order book as of June 30, 2023, exhibited a 15% YoY growth, totaling Rs. 5,321 crore. The company’s order inflow for the quarter also saw substantial growth, rising by 38% YoY to Rs. 758 crore.

Throughout the quarter, PSP Projects completed five projects, including the Surat Diamond Bourse. The company is actively participating in bids for major projects, such as the redevelopment of Ahmedabad and Delhi railway stations. Furthermore, they are exploring opportunities in the gems and jewellery park in Navi Mumbai.

PSP Projects has maintained its revenue guidance of Rs. 2,600 crore for the entirety of FY24. In terms of financial performance, the company achieved an EBIDTA (Earnings Before Interest, Taxes, Depreciation, and Amortization) margin of 12.7% during Q1FY24. The net profit for the same period stood at Rs. 37 crore.

In line with a commitment to sustainable development, PSP Projects has taken steps to integrate environmental, social, and governance (ESG) considerations into its operations. This includes the establishment of an ESG Steering Committee to guide and oversee the company’s efforts in this direction.

PS Patel salary for FY23 is almost 15 Crores now (increased 3 times). Son and Daughter taking 2.4 Cr each, basically 20 Cr salary for the promoter family on profits of 140 Cr. That is a big red flag for me. I can digest PS Patel salary at 10 Crore given his importance but his son of 27 yrs of age (less than 5 yrs of experience at PSP) is now taking 2.4 Cr home.

Disc - Invested

my statement was in regard to the covid years, thats when the remuneration was voluntarily reduced, so that company’s financial are not pressurised.

second of all we cannot just compare numbers and say his progeny doesnt deserve that much remuneration, we dont know the level or kind of work they are currently doing.

these numbers are not so high that it becomes a big red flag, atleast for me.

my point is everyone wants to make money, even the promoters, as long they continue growing, we need to give them some leeway

our investing frameworks cannot be imposed on the overall operations of the company and management

Everyone has their own opinion and I respect yours completely. My point is not to compare numbers here but mention few things that I feel are not in the best interests of minority shareholders. Giving 2.4 Cr to someone with just 5 yrs of experience is something that I don’t like as a shareholder unless the person proves me wrong (I really wish he does). Also, the promote salary numbers are high if we look at SEBI’s limit and general market norms as well.

I personally have no problem giving even 20% of PAT to promoter if he is doing something extraordinary but for the past few quarters, management has missed it’s revenue guidance multiple times

They always guide for big growth numbers and then when they fail, we get some excuses, some of which are valid though but you can’t always blame external factors. Either improve your actual numbers or do better predictions. Again, my personal opinion after following the company for around two years now. Still invested

My notes of 2nd Aug, 2023 concall

Completed the Surat Diamond Bourse, the world’s largest office building.

Outstanding order book as of June 30, 2023, at Rs. 5,321 crore, with 15% YoY growth. Private projects make up 46%, government projects 55%.

Completed 5 key projects during the quarter, including Money Plant high street and Reliance Corporate House.

Order inflow in the quarter grew by 38% YoY to Rs. 758 crore, with significant projects such as tourist destinations and commercial complexes.

Uttar Pradesh projects contributed significantly to revenue, reaching Rs. 915 crore.

SMC administrative building project is progressing rapidly, with excavation completed and Rs. 90 crore revenue booked.

Q1FY24 financials: 48% revenue growth to Rs. 510 crore, 37% EBIDTA growth to Rs. 65 crore, with a 12.7% EBIDTA margin.

Poised for opportunities in infrastructure development, given government initiatives and historical order inflow in Gujarat.

Well-positioned to bid for large projects, with a strong track record and eligibility criteria.

Revenue Guidance: The company is maintaining its revenue guidance, with no upgrade. The earlier guidance was Rs. 2,600 crore.

UP Projects: Out of the outstanding order book of Rs. 576 crore for UP projects, approximately Rs. 450 crore is expected to be completed by March 2024.

Surat Municipal Project: Expected revenue for the year is around Rs. 300 crore, with potential growth to Rs. 450 crore to Rs. 500 crore from FY25 onwards as finishing activities start.

Geographical Concentration and Addressable Market:

Construction Industry Landscape:

Precast Facility and Repeat Orders:

Debt Increase Explanation:

Competition in High-Ticket Projects:

EBITDA Margin and Margin Guidance:

CAPEX as a Percentage of Revenue:

Interest Costs:

Order Inflow Target for FY24:

Project Updates:

Is this a yearly recurring income? What sort of project is this?

“In Jan.2023, PSP was awarded an order of ₹1,344 crore from Surat Municipal Corporation for construction of tallest administrative building.”

Yearly recurring as long as the project isn’t over.

I think precast plant of PSP will benifits from West DFC project of railway, because it reduce logistics cost for company and can complete project (Outside Gujarat )early because of own precast plant. What’s your thoughts about this?

https://www.bseindia.com/xml-data/corpfiling/AttachLive/e220d528-9bd5-490c-82df-00d5e4a36648.pdf

ppt quarterly

PSP Projects Q2FY24 Concall Summary

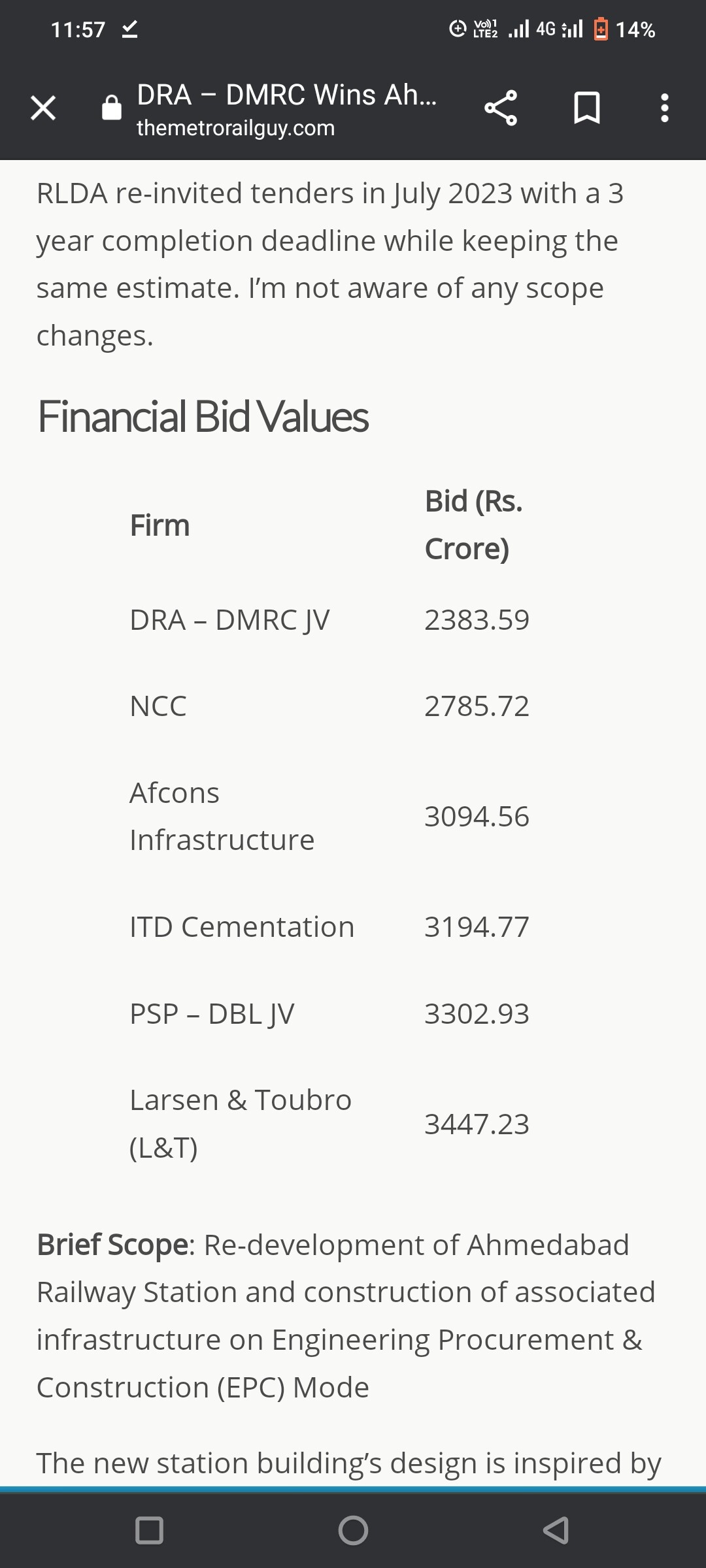

In last concall of Q1 of PSP Projects, Management told about Ahmedabad Kalupur Railway station redevelopment project in which PSP Projects were going to bid in around September, but I came across the news that “another competitor with joint venture” emerge as lowest bidder in that project and value of this project is above 2000 crore.

Link is given below about news :

It’s not the lowest, it’s L5 .

Competitor with joint venture emerge as lowest bidder, please read carefully.L1 bidder is Dineshchandra R Agrawal Infracon - Delhi Metro Rail Corporation (DRA - DMRC JV).