Good news for shareholders of PSP Projects, company emerge as L1 bidder for project of 357 crore in gujarat.

b5f0363b-550a-4164-855c-4e1681519c58.pdf (422.9 KB)

Good news for shareholders of PSP Projects, company emerge as L1 bidder for project of 357 crore in gujarat.

b5f0363b-550a-4164-855c-4e1681519c58.pdf (422.9 KB)

con call-November

Order Book and Order Inflow:

Projects and Awards:

Financial Performance:

Closing Order Book:

And revenue guidance is 2600 cr for FY23-24.

Order book:

Company currently has an order book of ~ Rs. 1000 cr (secured in FY24 so far). To achieve their target of Rs. 3000 cr, they need additional Rs. 2000 cr order book.

From the existing pipeline, with success rate of 15%-20%, they can expect orders of ~ Rs. 1200 cr.

For the balance order of Rs. 800 cr, they need to bid for Rs. 4000 cr worth of projects.

If they win Delhi station development (a very BIG “IF”), they would surpass their own targets. Otherwise, the asking rate is huge given that we are entering election mode where the focus of government will be more on completion of existing projects and less on awarding new projects. But they can get projects from private sector too.

Revenue:

Rs. 2600 cr for FY24 seems realistic. Lets assume they are able to deliver it. So, for FY25, they would be targeting ~ Rs. 3100 cr.

Existing order book: Rs. 4900 cr

Expected orders H2 FY24: Rs. 2000 cr (Rs. 3000 cr target – Rs. 1000 cr already booked)

Revenue for H2 FY24: Rs. 1500 cr (Rs. 2600 cr full year – Rs. 1100 cr H1 FY24 actuals)

Carry forward of orders to FY25: Rs. 5400 cr.

(assuming unbilled amount is maintained at current level)

For FY25 revenue target of Rs. 3100 cr, they would need orders worth Rs. 15500 cr, i.e. additional orders worth Rs. 10000 cr. That is a big ask. So either the market has to open up big time, or the company will need to get aggressive in bidding (may impact margin).

Valuation:

Assuming they are able to deliver revenue of Rs. 3100 cr for FY25 and assuming average EBIDTA of 12% (they are guiding 11-13% range), FY25 EBIDTA would be Rs. 372 Cr.

Last 10 yr avg. EV / EBIDTA valuation is 9. If I apply the same here, their EV for FY25 is Rs. 3348 Cr.

Reducing debt of Rs. 300 cr (likely debt level as highlighted by management), Mcap comes to Rs. 3048 cr. This gives us 6% upside from existing level of Rs. 2880 cr Mcap. So the business seems fairly valued at existing level with limited upside.

Any opposing viewpoint is desirable.

Disc: Holding for more than a year. No transaction in last 30 days.

Very nice observation and evaluation Santosh Ji. One thing, have you worked out the industry level EV / EBIDTA ratio?

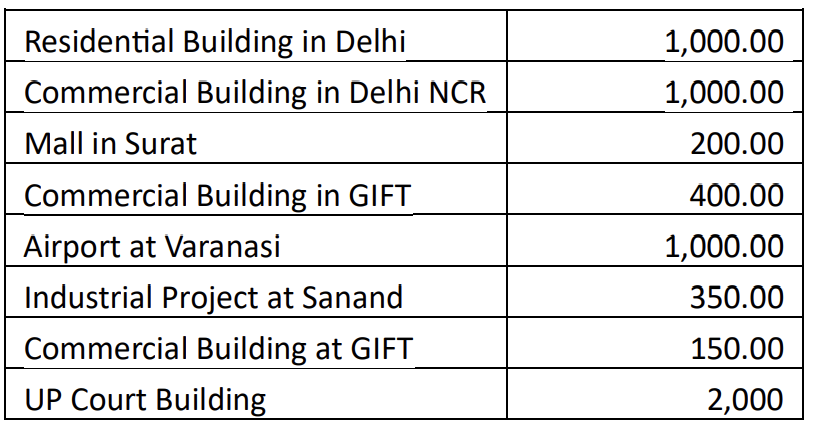

Project Awards:

Project Completion:

Order Book & Projects:

Order Inflow:

Recognitions:

Financials (Q2FY24):

Revenue Guidance and Projected Closure:

Project Level Updates:

Future Prospects:

Bid Pipeline Overview:

Project Timelines and Completion:

Capital Expenditure (CAPEX):

Debt Reduction and Finance Costs:

End of March 2024 Debt: Expected reduction, but not specified.

Combined Long-term and Short-term Debt: Currently Rs.377 crores.

Finance Cost: Anticipated to remain Rs.10-11 crores on a quarterly basis.

Fixed Price Contracts Percentage:

Other Expenses and Run Rate:

Promoter Stake:

Precast Revenue:

UP Project Receivables:

SMC Project Execution for FY24:

Investment in Precast Facility:

Recent Expenses:

Future Investment:

Total Investment: Rs. 160 crores – Rs. 165 crores

Phases Commissioned:

Production Capacity Expansion:

Debt and Working Capital Analysis:

Order Inflow and Diversification:

Bidding Strategy and Election Year:

Precast Mould Utilization:

Bidding Discipline and Market Competition:

Litigation and Arbitration:

Thank You. No, I haven’t done industry level analysis. Also, its a very fragmented industry. Only other listed company in similar business I know of is J Kumar (from Maharashtra). Their avg. EV / EBIDTA is 4.5.

EPC business works on order books. So long as business has orders, they will make money (subject to margins) irrespective of the competition (they compete to secure order, after that there is no competition). Its basically discounting future cash flows based on orders they have in hand + likely orders they can win.

lowest bidder for a 296 core project

Whats latest update on PSP Projects? Stock has been underperforming since 1.5 years and giving negative returns?

Recieved 3 Government project worth of 935.41 Crore (excluding tax)

Order inflow guidline by management is about 3000 Cr during FY23-24

Anyone know why the profitability got hit in the latest quarter? Sales growth is continuing though.

Net profit of PSP Projects declined 12.10% to Rs 31.08 crore in the quarter ended December 2023 as against Rs 35.36 crore during the previous quarter ended December 2022.

Sales rose 40.90% to Rs 704.75 crore in the quarter ended December 2023 as against Rs 500.16 crore during the previous quarter ended December 2022

Per concall, they said this was because of 1 time expense on UP project of c.5 Cr. UP project is expected to end next quarter and they do not foresee incurring this again. Overall margin guidance is at 11-12% in FY24 and going forward.

Another reason for dip is interest which is attributable to Surat diamond dispute receivable + UP receivable. If Surat diamond does not reconcile by March 24, then arbitration is reqd which might take an year. To curtail high interest cost, Co has passed QIP resolution recently. If its gets resolved, they expect to get debt to normal levels. Capex guidance stays at 4% of revenue. Precast facility is currently operating at 50% utilization though at a lower margins [EBITDA positive] which they expect would ramp if opportunity strikes (i.e; if someone is willing to pay a premium for early completion).

No provisions are made in books for Surat diamond dispute. Monitorable on bad debts.

Rev guidance for FY25 is 3000 Cr with margins of 11-12%. Mgmt did say in EPC project 1-1.5% fluctuations are normal.

However, to our surprise, major issues related to our several claims were not initiated by

the PMC as instructed by Surat Diamond Bourse Committee which totals to Rs. 538.59

crores (Rs. 430.30 Crores as additional claim, Rs. 65.72 Crores against approved but not

certified work done and Rs. 42.57 crores against retention). After that, we had several round

of meetings with the committee members, but they discussed and negotiated to a negligible

amount against our additional claim of Rs. 430.30 Crores, which is purely as per the contract

terms and related to rate validity & force majeure

20231207_CourtCase_64.pdf (pspprojects.com)

In the November call, they only cited ~100Cr of receivables for booked, unbooked, and retention money. Even in a recent call, I heard a similar figure; what is the 400Cr amount? According to my understanding, it is using a price increase provision following a force majeure to negotiate 100+ crore. I see the focus is largely on recovering ~100 crore.

Disclosure - invested.

PSP PROJECTS got project worth of 630.29 Crores (excluding taxes) for Construction of Gati Shakti Vishwavidhyalaya at Vadodara for Rail Vikas Nigam Limited in Govt. Category. The project is to be completed within 30 months.

Q3 FY24 Concall notes

Project Highlights:

Order Inflow and Bookings:

Project Development Updates:

Recognition and Awards:

Financial Outlook:

Strategic Vision:

Financial Performance (Q3FY24 vs Q3FY23):

Expense Analysis:

Capital Expenditure and Balance Sheet:

Working Capital and Credit Facilities:

Fixed Deposits:

Business Growth:

Promoter Shareholding:

Revenue Growth and Projections:

Margin Outlook:

Equity Raising and Financial Strategy:

Project Updates and L1 Orders:

Bid Pipeline and Project Status:

Financial Strategy and Debt Management:

Precast Revenue and Margins:

Nine-Month Precast Revenue:

Margins Expectation:

Current EBITDA Status:

Current Utilization and Capacity:

Potential Margins with Increased Utilization:

PSP PROJECTS got New Project and emerged as L1 bidder.

Management guidance for 3000 Cr order inflow achieved.

Construction and Maintenance of Human and Biological Gallery at Science City,

Ahmedabad for Gujarat Council of Science City worth INR 268.11 Crores (excluding

taxes) in Government Category. The project is to be completed within a period of 18

months.

2. Construction of Commercial Building ORYX at GIFT City, Gandhinagar worth INR

118.13 Crores (excluding taxes) Institutional Category. The project is to be

completed within a period of 24 months.

Emerged as Lowest Bidder (L1 Bidder) for the

project “Construction of Fintech Building at GIFT City” for Gujrat International Finance at

Gift City, Gandhinagar worth INR 333.05 Crores (Excl. GST). The project is to be completed

within a period of 30 months

must read court order

Receivables will be a problem for this company since most projects are government projects. Company is taking debts to execute projects until receivables arrive. I believe this is pushing the stock down. What do others think of this?

Majority of their problem has come from a non government project- SDB. Given that the project hasn’t managed to take off with diamond merchants, their retention money and last chunk of receivables have been kept pending beyond the stipulated time here.

Contingent liabilities today is at 800 + crores and is raising. History shows government projects usually pay late and gets stuck in receivables. Margins have come down too. They have been lowest bidders for multiple projects. My question is are they sacrificing margins and being too aggressive to grow revenues?