please explain contingent liabilities more than 800 crores? were are they exposed to? Source of information?

1 Like

I am just looking at their balance sheet in screenr

As far as I know I don’t know if they have any serious contingent liability

Except any lawsuits by sdp

Or if any legal agreement with the existing customer for compensation incase of non completion of project

1 Like

Good time to add the stock right? Have added some in today’s 10% fall.

Operating margins are not lower than this for them historically. Also PE is super reasonable. I can only upside from here on both earnings and PE going ahead.

Heard that the stock is down due to some big exit today. Views from others on this?

2 Likes

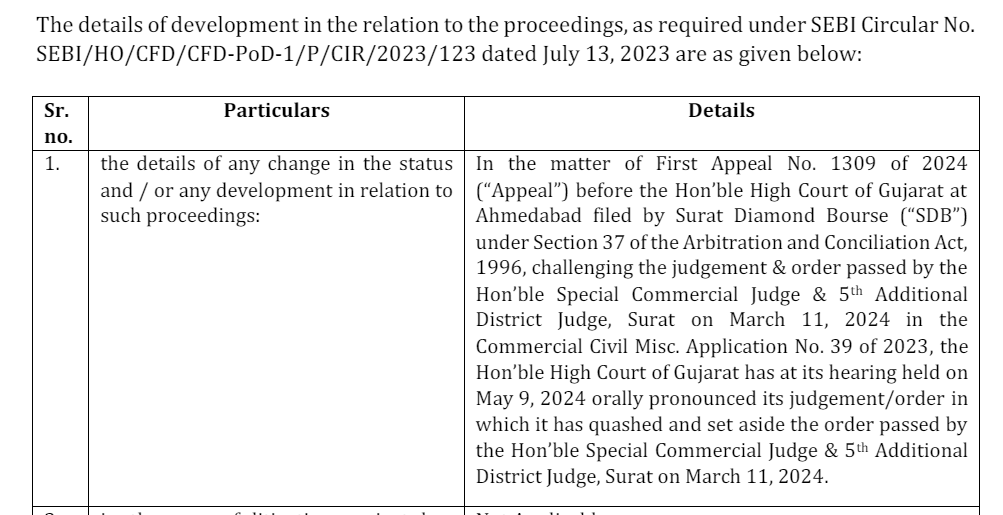

I think there is also overhang of ongoing disupute with Surat Diamond Bourse.There claim is approx Rs 530 Cr. and litigation is going on. so, the working capital of company is stretched and in case SDB dispute settelement is delayed , they may go for QIP. But, these disputes are part of business and in my opinion long term prospects of company is good.

Disclosure: Invested and no transaction in last 30 days

3 Likes

Value research article on PSP projects

https://www.valueresearchonline.com/stories/201137/psp-projects-hidden-gem-or-value-trap

Disc: Invested

2 Likes

Can someone throw light on these statistics I got from comparing annual report of March 2018 with March 2023.

PS Patel’s compensation was 4.09 Cr as March 2018 and went up to 15.6 Cr as of March 2023. (Yet to get the latest figures). During the same time, the companies net profit went up from 42Cr to 133Cr. PS Patel’s compensation has improved 4x whereas the PAT has grown 3x. Ratio wise, the comp is > 10% of the PAT (even though < 10 % of EBIDTA) Is this desirable?

Few thoughts:

-

Even after factoring in delayed revenue from projects such as SDB, why is the board giving so generous compensation to one individual?

-

When the PAT fell ~20% YOY (FY '22 to FY '23), PS Patel’s compensation was seen rising from 14.8 Cr to 15.6 Cr for the same timeframe. Isn’t compensation linked to performance? What is in it for shareholders?

-

From what I know, PS patel does not offer shares to employees. How can this organisation sustain from this one man army. This does not sound well.

Please help me understand if this is par for the course? These certainly don’t seem like a good situation.

1 Like

No stock becomes multi-bagger by adding 5-10 Cr to the annual bottom line by cutting CEO’s salary.

What matters to me is that the company has done 3X net profit in 5 years. If PS Patel can deliver 4X in next 5 years, shareholders might be happy to further compensate him.

However, if you are bringing in inequality angle between him and his employees, then it begs a different discussion and different forum. Also, I believe ESOPs should be offered to select employees, who are key for company’s success and to retain them.

Thanks,

You are right that we need to reward merit. That being said I became a bit skeptical looking the growth of PAT and growth in comp. Shouldn’t performance be linked to PAT ?

On my other point though I am not worried about inequality but rather the incentives for others to perform.

to me it looks positive, as I wrote earlier, I was expecting 100Cr only

In the November call, they only cited ~100Cr of receivables for booked, unbooked, and retention money. Even in a recent call, I heard a similar figure; what is the 400Cr amount? According to my understanding, it is using a price increase provision following a force majeure to negotiate 100+ crore. I see the focus is largely on recovering ~100 crore.

disclosure: invested

3 Likes

Settlement of SDB was a big overhang on the stock price. Now that its closed, it seems the price is ready to take off. I believe It should touch 750 i.e. 200 DMA.

Please provide any counter point. Why shouldn’t one invest at this price / valuation for 10-15 day short term gain?

But what about the cash flow, did they receive complete cash i.e. 1960 crs. (excl. GST)?

yes they received most of it

1 Like

In May 2024, an out-of-court settlement had been reached between the

Company and SDB on the basis constructive dialogue, discussion and

negotiations, effectively resolving all the disputes between the parties. Under

the Settlement, SDB has agreed to pay a total amount of INR 170 crore over

and above INR 1,790 crores already certified by them. With this settlement,

the total approved project value amounts to INR 1,960 crore excluding GST.

Till now, the Company had recorded revenue of INR 1,896 crore in the

accounts and now the remaining revenue of Rs.64 crore will be recorded

upon the receipt of the certificate from SDB. We expect to receive the

payments in tranches before the end of H1FY26.

3 Likes

Hello members… last order recieved company value around 650 cr…

Almost projects complete in 12-15 months

And near ahmedabad all projects so company capable to delivered in time… great value added…

I am from ahmedabad and investor in these company… project continue devloping by psp around here feel proud and faith in core strenth…

So pls share any members any negative clue for future outlook … pls share

1 Like

Psp projects has sit on around 6000 cr market cap almost 2 year completed this order book so 3000 cr per year… margin 10-12% ebidta means 300 cr means PE ratio below 10 in future fy 26. i think in these market scenario these kind of deal best for investor and also past project and future continue projects feel proud as an investor… add some more share in past week…

2 Likes

-

Q1FY25 revenue at Rs. 612 crore, up 20% YoY

-

EBITDA at Rs. 73 crore, up 14% YoY

-

EBITDA margin at 12%, down slightly from 12.69% in Q1FY24

-

Net profit at Rs. 34 crore, down 7% YoY

-

Rs. 64 crore revenue booked from Surat Diamond Bourse (SDB) project

-

Rs. 54 crore EBITDA contribution from SDB project

-

Core business revenue (excluding SDB) grew 7.5% YoY

-

Focus on smooth execution of ongoing projects

-

Aim to ramp up order book with new projects in building space

-

Increased focus on precast technology by large corporates

-

Company becoming eligible for broader range of projects (sports complexes, tourism, airports, etc.)

-

Labor scarcity issues post-elections affecting some projects

-

Increased material costs and site overheads impacting margins

-

Lower core EBITDA margins addressed; management expects improvement from Q2

-

Clarifications provided on debt repayment and SDB receivables timeline

-

The company’s core EBITDA margin (excluding Surat Diamond Bourse project) was lower than usual in Q1 FY25, at around 3.5-4%.

-

Management attributed this to several factors:

- Additional expenses of Rs. 25 crores incurred on UP Medical projects due to cost escalations and site overheads.

- New high-value projects awarded in Q4 FY24 are still in initial stages and not yet contributing significantly to EBITDA.

- Some projects faced labor scarcity issues post-elections.

-

The company expects these issues to be largely resolved from Q2 onwards.

-

Guided for EBITDA margins to improve to 10-11% range from Q2 FY25.

-

Some residual impact from UP projects might continue (estimated at Rs. 5-10 crores in Q2), other projects are not facing similar cost pressures.

Debt repayment and SDB receivables timeline: -

As of June 30, 2024, the company had debt of Rs. 260 crores.

-

They received Rs. 104 crores from Surat Diamond Bourse (SDB) in early July.

-

Rs. 60 crores of director’s loan was repaid using this amount.

-

Current debt stands at around Rs. 200 crores (as of the call date).

-

Regarding SDB receivables:

- Total outstanding was Rs. 225 crores.

- Rs. 104 crores received in July 2024.

- Remaining Rs. 121 crores to be received in 4 tranches by October 2025.

- October 2025 is the final deadline, regardless of SDB’s office sales progress.

- March 2025 was never the agreed timeline for full receipt.

-

Precast facility running at full capacity; revenue expected to reach Rs. 200-250 crore this year

Targeting revenue of Rs. 2,800 crore for FY25

Expect EBITDA margins to improve to 10-11% from Q2 onwards -

Outstanding order book at Rs. 5,890 crore, up 11% YoY

-

Order inflow guidance maintained at Rs. 3,500 crore for FY25

-

Bid pipeline of Rs. 6,000 crore

-

Expecting 10-15% annual growth in coming years

-

Capex of Rs. 17 crore in Q1; projecting Rs. 60 crore for full year

-

Opportunities in new sectors like semiconductors

-

Risks from project delays and cost overruns (e.g., UP Medical projects)

5 Likes