Subject: Disclosure under Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015 – Details of Litigation

Pursuant to Regulation 30 of the SEBI (Listing Obligations and Disclosure Requirements) Regulations, 2015, we would like to inform that the company has filed Writ Petition (Civil) bearing diary No. E-4580239/2024, in the Hon’ble High Court of Delhi against Superintendent Engineer, Bareily and Others. The details as required under SEBI Circular No. SEBI/HO/CFD/CFD-PoD-1/P/CIR/2023/123 dated July 13, 2023 are as given below:

- brief details of litigation viz. name(s) of the opposing party, court/ tribunal/agency where litigation is filed, brief details of dispute/litigation;

The Company has filed Writ Petition (Civil) bearing diary No. E-4580239/2024, in the Hon’ble High Court of Delhi against the Respondent namely Superintendent Engineer, Bareily and Others concerning Project “Construction of Residential Building of PAC Mahila Batallion, Badaun, Uttar Pradesh”. The petition is filed under Article 226 of the Constitution of India, seeking the issuance of a Writ of Mandamus or Certiorari to quash and set aside the termination order dated March 27, 2024 and impugned communication dated 10.10.2024 issued by the Respondent arbitrarily. The Company contends that the termination was executed arbitrarily, without due consideration of the reply and explanation provided by the Company, and without affording an opportunity for a personal hearing, thereby contravening the principles of natural justice and the mandate of Article 14 of the Constitution of India. - expected financial implications, if any, due to compensation, penalty etc.

At this juncture, the financial impact remains unquantifiable; therefore, it is deemed inapplicable. - quantum of claims, if any;

Not Applicable

Adani group in advance stage for acqire psp projects company… will se if deal possible then promoter mr ps patel stand after sold it…

Nothing from the respective companies yet. Please mention rumors as rumors instead of declaring as facts.

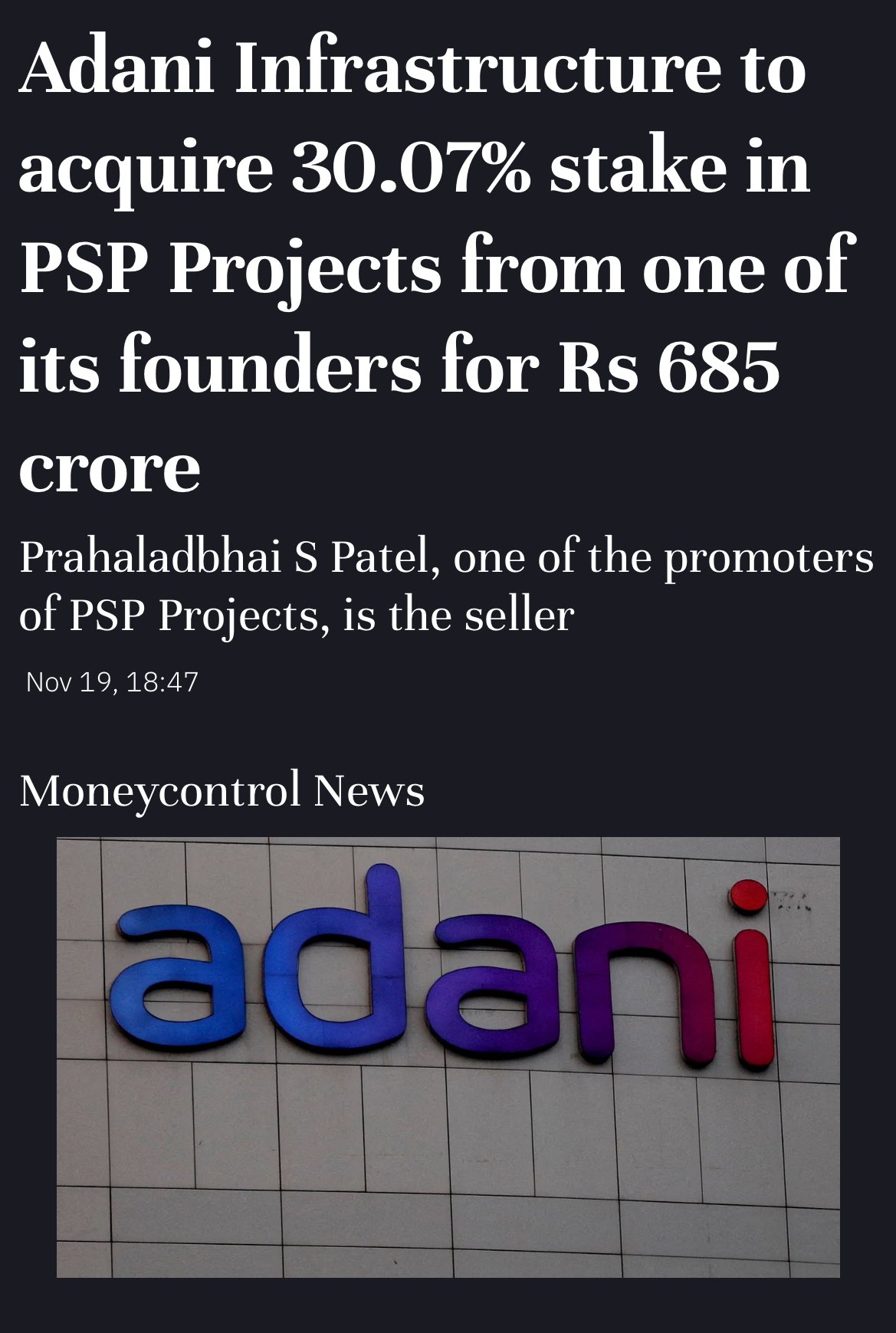

Edit: Its Official, Adani Infra set to acquire stake through Open Offer to Promoter. Office Price @642

The deal values PSP Projects at Rs 575 per share, 15% lower than its closing price on Tuesday.

Why they had to do it at discount? This is near to the lowest price of the last 52 weeks. Some side deal ![]() ?

?

Disclosure: Invested

My thoughts exactly. How is that the promoter has no confidence in his own company. It seems he has greater confidence in Adani. That is why he is still holding 30% and selling the remaining 30% to Adani. He might hope to cash in at a higher price two years from now, if Adani can turn this company around and get big contracts.

Disclosure: Invested from lower levels

Listened to the company’s conference call following the Adani acquisition. Key points discussed about the acquisition are as follows:

-

The promoters are selling their stake at ₹575 per share, whereas the QIP was conducted at over ₹650 per share.

-

The rationale behind the stake sale is leveraging the Adani Group’s expertise and unlocking opportunities in various projects such as airports, Dharavi redevelopment, data centers, etc. (Additionally, the Adani Group is aiming to build its EPC companies for its projects).

-

The company is projecting EBITDA margins of 10% or higher.

-

Out of the current order book of ₹6,000+ crore, only ₹500 crore pertains to the Adani Group.

-

There is an agreement between the Adani Group and the promoters ensuring 50:50 ownership, even after the open offer.

-

The promoters are obligated to remain with the company for at least five years and cannot exit during this period.

-

The promoters expect better utilization of the precast facility, which is likely to be margin-accretive and significantly reduce the construction cycle.

Disclaimer: I invested during today’s dip caused by the Adani-US issue. I’ve been following this company for over three years.

Doesn’t it show that the promoters are not able to grow the company independently.

If they are selling stake to adani just to get some deals from them it seems like a bad move IMO.

We are talking about 30% stake sale.

Yes, @CHAC3MEN, it’s an open secret, and this has been evident in its performance over the last 2-3 years. One thing I am confident about is the quality of its construction. As a civil engineer (from Adani Institute ![]() ), I have seen and heard about the way the company operates. The construction quality is comparable to L&T. In fact, the promoter has publicly mentioned in many of his interviews that the company aspires to deliver L&T-level quality.

), I have seen and heard about the way the company operates. The construction quality is comparable to L&T. In fact, the promoter has publicly mentioned in many of his interviews that the company aspires to deliver L&T-level quality.

I exited my holdings for PSP yesterday.

Thesis for entering the stock (some 6 months ago) :

PSP came across as a company hungry for growth, with a solid track record of timely execution and a negative cash conversion cycle. With the growth happening in Gujrat and UP, the company appeared to be a beneficiary of urbanization theme.

Reasons for exiting just days ago:

- Primarily I saw a number of issues related to failures in either execution or challenges from the clients who delayed payments / cancelled projects etc.

- The order book growth seems have slowed down. While company gave a guidance of 3500 incremental order book at the beginning of the FY 25, the realized order book is only 1400 crores by the end of first half.

- Uncertainity with respect to case with Adani (the major factor) and the deal itself. It seems that the company is probably in trouble and is constantly seek funding.

- Finally, there are other good buys in the EPC space which are somewhat better with respect to order book growth and the business uncertainties.

Disc : My own view. Not a recommendation to sell or buy.

Hello members is this some big order come soon… psp projects hiring some 400 seniour engineer approx salery 1 lack month means 4 cr additional salary Simmilar to last qtr 3 months profit…obious some big bigger comming soon… from adani infra side…

the company is in receipt of new Work Order for “Civil

Structure and Finishes work for BIFC - 2 Building” for Brigade (Gujarat) Projects Private

Limited at GIFT City, Gandhinagar, Gujarat worth INR 107.10 Crores (excluding GST) in

Institutional Category. The project is to be completed within a period of 24 months.

@jayraj_khachar , as per their annual report last year PSP had 2000 employees. So, 400 new hires would make it 20 percent more employees in best case scenario (i.e. if we assume employee turnover is zero which is not usually the case. Construction sector has quite high turnover imho).

2000 employees had a revenue of 2500 crores last year. Average revenue is 1.2 crores per employee. 2400 could get revenue to 3000 crores (again ignoring turnover).

Disclosure: not invested. But yet to do a proper due diligence

Anyone tracking recent senior management resignations from PSP? Senior Vice President Project Execution, Vice President - Procurement, General Manager- Contracts, and Company Secretary have resigned in last couple of weeks. Some of them have been with the company since its inceptions it seems looking at their employee code (4 & 5).

On the margin front, they are reducing guidelines on 23.05.2025

It is not about reduction. It is more about the performance and the availability of labour and the crisis through which the construction industry is going on since last 1.5 to 2 years or maybe next 1 year or so. So just I’m making myself a little bit safe in terms of percentage by 1%. Otherwise, we’ve already given you 9% to 10%. Now I’m saying 8% to 9%.

Page 2 of 15 During Q1FY26, the construction industry was suffered by labor shortage and PSP Projects were no different. During the quarter, we faced labor shortage in the month of April-May 2025. And during Q1FY26, there was a 37% shortfall in labor. Now, the good part, at present we are at 19% labor shortfall. The minor impact of this and monsoon will come in Q2FY26 also, but I am confident of the shortfall further reduce starting August '25.

Page 5 of 15: Guidance

So better we give revenue guidelines on the verge of second quarter completion. And EBITDA margins, yes, still we are in the range of the same thing what we have been telling, we’ll be in the range of 8% to 9%.

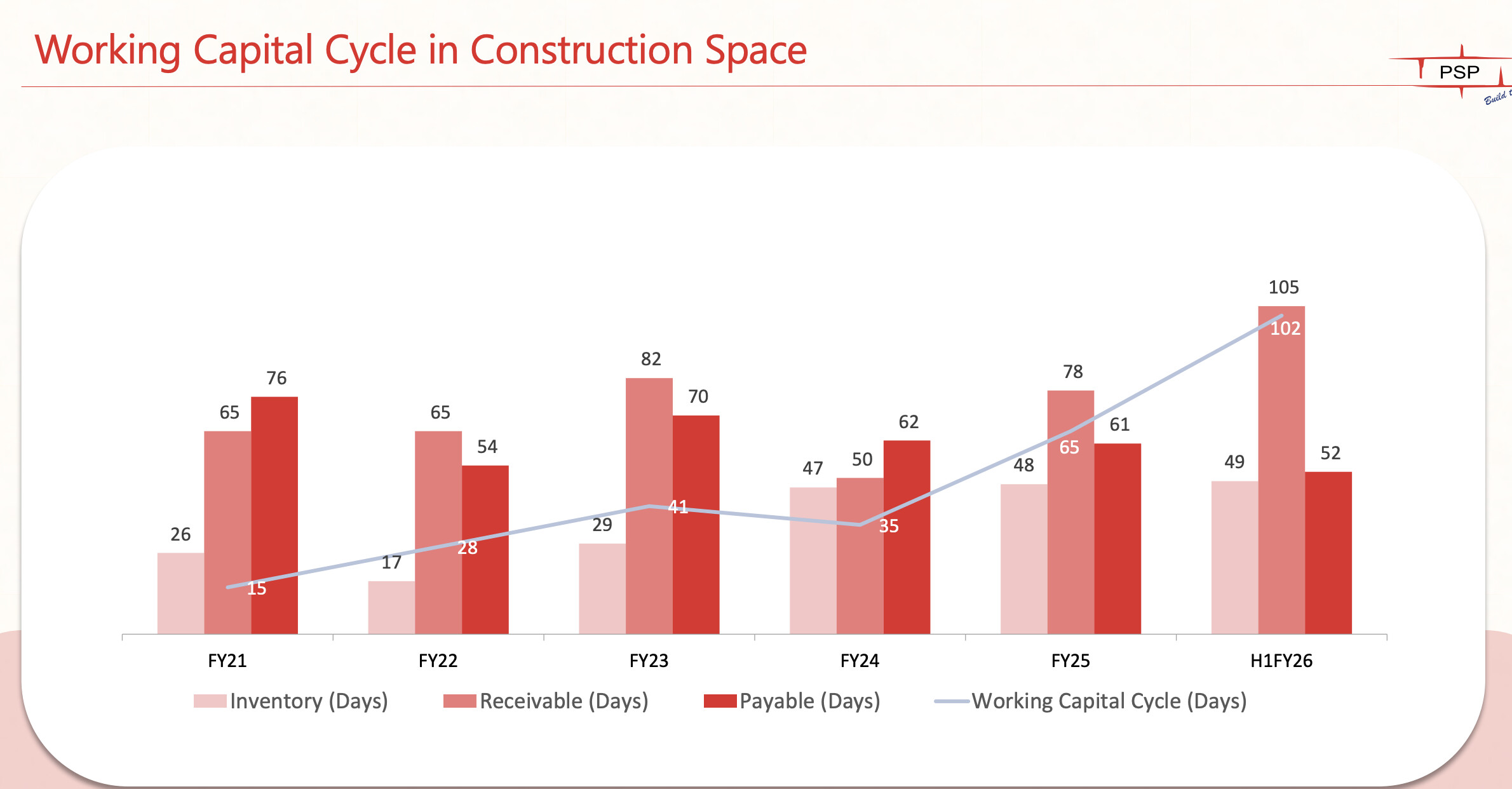

Page 7 of 15: Working capital reduction

And whatever working capital which we are using today from the banks as fund base can get reduced to a drastic level by end of third quarter.

Q2 FY26 Result analysis and Concall summary

Financial Highlights

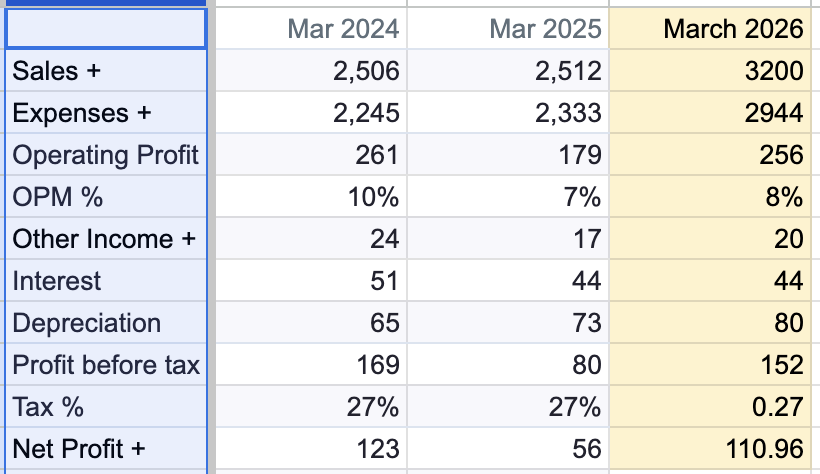

- Revenue: ₹703 Cr, up 20% YoY and 35% QoQ.

The management expects ₹2,000 Cr revenue in H2 FY26, taking the full-year estimate to ~₹3,200 Cr. - EBITDA Margin: 7%, compared to the guidance of 8–9% for H2.

- Working Capital Days: Increased from 78 to 105 days due to a higher concentration of order execution towards the end of September. Payments have started flowing in from October.

Operational Highlights

- Order Booking (Q2): ₹4,100 Cr (of which ₹4,000 Cr from Adani Group) vs ₹107 Cr in Q1.

- Total Order Book: Stands at ₹9,883 Cr as of Q2-end.

Guidance and Outlook

- Management reiterated H2 revenue guidance of ₹2,000 Cr with EBITDA margins of 8–9%.

- Order Bidding Pipeline:

- ₹7,000 Cr of Adani-related projects

- ₹1,100 Cr of external projects

- By March 2026, the company expects:

- Outstanding Order Book: ₹9,000 Cr (existing) + ₹8,000 Cr (new) – ₹2,000 Cr (execution)

→ Estimated total of ₹15,000 Cr

- Outstanding Order Book: ₹9,000 Cr (existing) + ₹8,000 Cr (new) – ₹2,000 Cr (execution)

- FY27 Outlook: Annual revenue run rate expected to exceed ₹4,000 Cr.

Key Concerns

- Limited visibility on ₹90 Cr receivables from the Surat Diamond Bourse project, pending recovery.

Opportunities

- The upcoming Commonwealth Games 2030, to be hosted in Ahmedabad, could drive major infrastructure investments.

As Adani is a key promoter, PSP Projects may benefit indirectly from related capex opportunities.

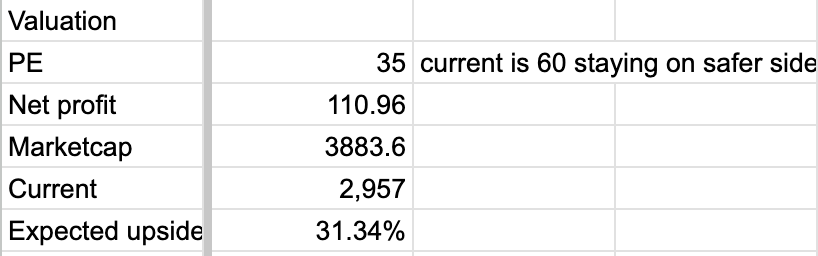

Valuation Perspective

- Based on management’s outlook and execution trajectory, an estimated upside of ~31% by next year is anticipated. (check screenshot)

Dis. Invested

Record order inflow of 4100 crore in Q2 is higher than last year’s total order inflow of 3500 crore.

7000 crore more order inflows expected in Fy26.

Good Operational performance turnaround in this quarter.