A significant portion of 2W sold are fitted with analog and LCD instrument clusters. OEM’s have started making shifts from analog->LCD->LED->TFT.

With EV’s, OEM’s most preferably choose LED or TFT.

Observe the last quarter revenue growth. Most 2w OEM’s sales were grown at a low single digit, but pricol’s revenue growth was in double digits. As the value per vehicle contribution from pricol increases, then Pricol is poised to grow at a much higher rate compared to the sales of 2W. All of this puts Pricol is in a sweet spot.

Monitorables:

Pricol is also planning to use their expertise in IC’s and foray into instrumentation in industrial sector.

Can company crack the PV market? I know they’re supplying to Tata motors.

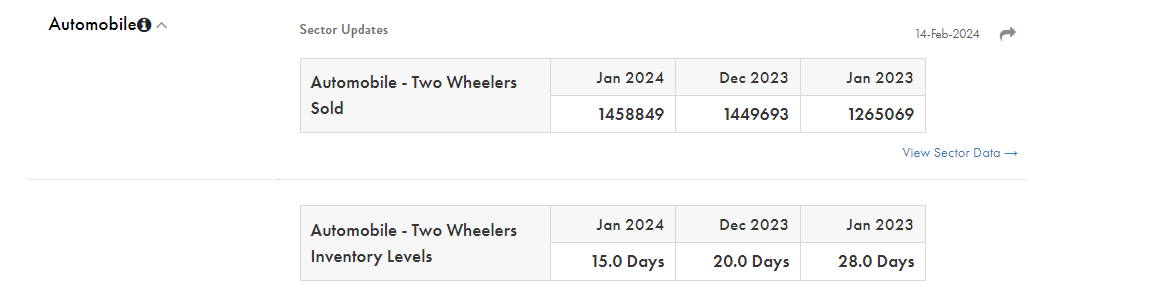

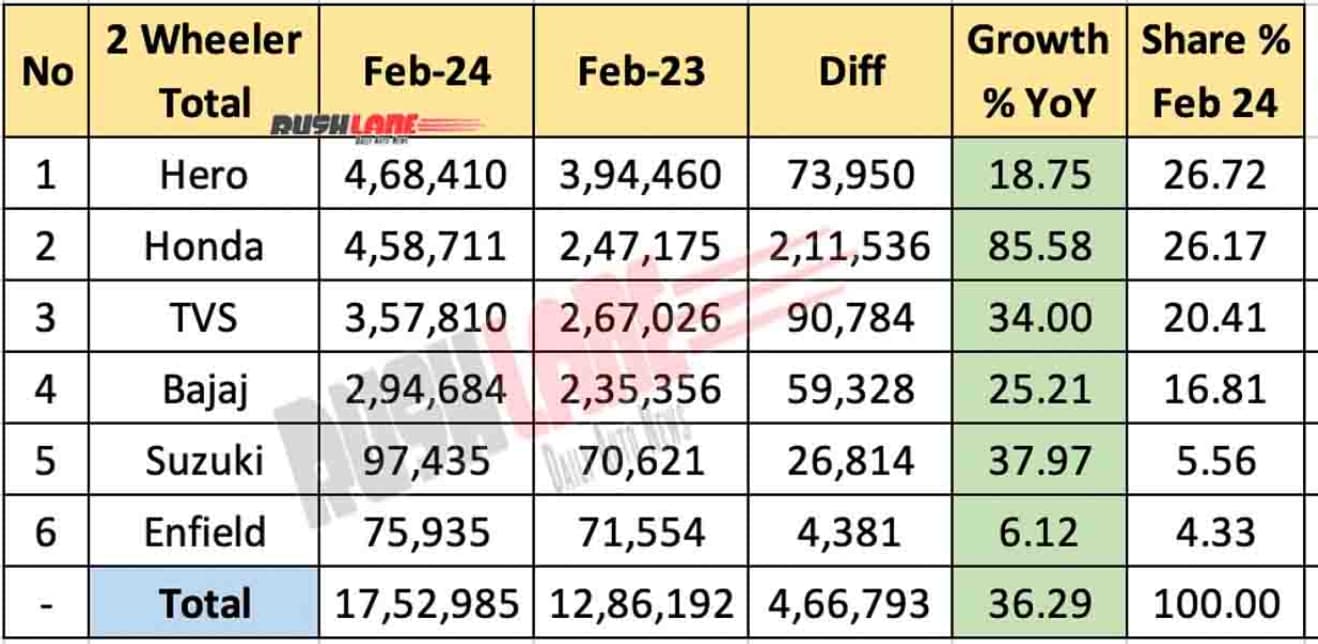

Since almost all 2W companies posted good sales report in the range of 20%, we could see a very good result from Pricol for Q3FY24.

Disc: Invested from 150 levels, added at every dip and may be biased.

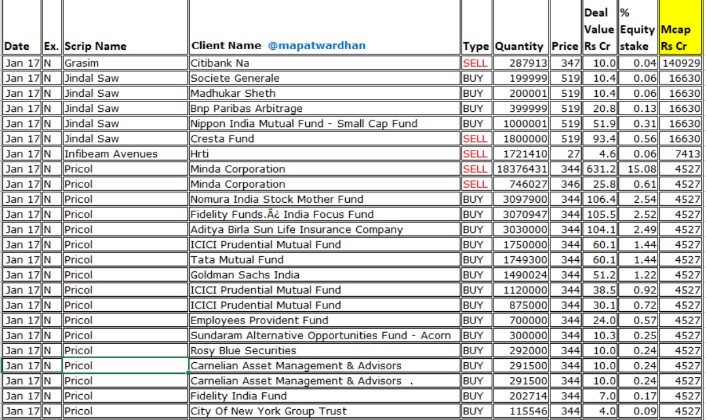

Minda made ~250 cr in this investment. This is significant for a co with ~10k market cap.

Now Minda, Pricol and investors in both the stocks would be happy

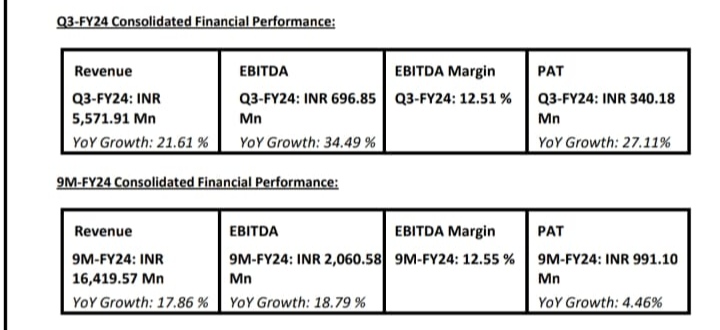

On the revenue from operations, we have grown by 21.61% on a Q3-to-Q3 comparison and our EBITDA has grown by 34.49% during the same period.

Our EBITDA margin stood at 12.51% from revenue from operations at 5,571.91 million. For the nine months of FY’24, our EBITDA margin was at 12.55% and the total revenue was at 16,419.57 million

We are working on E-Cockpit with one of our major customers. The SOP is likely to start by FY’26.

The cluster business contributes to about 70% of the total revenue and the 30% comes from the non-instrument business.

Segment-wise breakup- Two-thirds of our revenue coming from two-wheelers and 15% coming from the commercial vehicles and 5% to 7% comes from the personal passenger vehicles and the remaining coming from tractor and off-highway segment

Exports- We stand at 10% of the total revenue coming from export, primarily because there has been some slowdown both at the US and Europe markets and we hope recovery to happen from next year onwards

Red Sea crisis impact- Because of the Red Sea issue, the logistics time has gone up by a couple of weeks because it has to be rerouted. So, what we’re doing is, we have started that rerouting and now it has come into normalcy. So, we are not taking any issues currently because of the Red Sea.

The margins will not be impacted due to the increasing use of electronics in our instrument cluster, rather the margins will go up. If you see that more and more electronic clusters that we have been having since 2020, our margins have been going up. This is due to our comprehensive end-to-end solution, which includes design, development, manufacturing engineering, and tool production. This comprehensive approach not only improves our margins but also ensures that our products meet the customer’s expectations, thereby enhancing our overall business performance.

We are moving from a product-based company to a solution-based company. This is what we have explained in the few earnings call also. If you are only doing a product with electronics, then your margins will not be very high. But if you are moving into like a technology product giving solutions to the customers, your margins are not under threat.

Disc brake and battery management system are something which is under development. In the next 12 to 18 months, we would be launching those products for a number of EV customers across the various two-wheelers, which will not only include new age EV which is going to be the primary focus and also to our traditional OEM. Revenues should start from FY 26 onwards.

Exclusivity on SIBROS? - It is a complete bucket of solutions that we offer to the customer as an end-to-end connected vehicle solution and SIBROS would be a part of it. So, we have the Driver Information Systems connected with the Telematics solution and have SIBROS for the cloud. So, it will be a combination of everything. So, if you ask me exclusivity, it is not there, but if you see this kind of connected vehicle solution whatever we’re offering to the market, I think we’ll be rather very exclusive in whatever solution we’re giving to the customers

FY26 guidance depends on customer launches, order book is quite strong , just that end user industry needs to be tracked

New models launched by Hero MotoCorp uses pricol’s e Driver Information Systems, also used in Tata Motors EV Punch and also for ICE engines

Business: end-to-end solution for the customers starting from the design, development, manufacturing engineering

Financial highlights

revenue grown by 21.61% on a Q3-to-Q3

EBITDA margin stood at 12.51%

Working on E-Cockpit solutions with an undisclosed major OEM and launch likely by FY26

TFT clusters, market moving from LCD to TFT, refer ACMA India website for industry data

2W is their bigger market segment in India (refer auto industry sales data as is Proxy to auto play), 66% rev from 2W, Commercial vehicle contributes to about 15% of topline, 7-8% from personal passenger vehicles & 10% revenue from Exports.

cluster business contributes to about 70% of the total revenue and the 30% comes from the non-instrument business.

Risks as imports raw materials, Red sea issue impacting logistics.

with increasing electronic cluster compared to instrumental cluster expects margins to improve, into the high margin leg of value chain.

Strategy: moving from product to more of solutions/ services business as soultions-based business has better margins compared to product based.

Revenue guidance for FY26 —> not sure about 3.4 to 3.6K guidance fulfilling dependent on these 2 product launch and EBITDA margin of 14%

Disc brake and battery Mgmt system under development, in 1-1.5yr launching these 2, their rev will start from Q4 of FY25.

SIBROS partnership under testing, an Telematics which is the part of the connected vehicle solution but currently in POC stage.

The product manufactured by them a critical component in EV, Telematics track many vehicle parameters

Top customers TVS, Hero Motocorp, Bajaj, Royal Enfield, Honda, Suzuki, TAMO, Ashok Leyland, Volvo, Eicher

70% from driver information systems and connected vehicle solutions(DISCVS). 30% from actuation, control and fluid management systems(ACFMS).

With in DISCVS:

Around 67% from two wheelers

15% from commercial vehicles

7-8% from passenger vehicles

Remaining (~10%) tractors & off road vehicles

90% revenue comes from the domestic market & 10% from exports.

Product launches in Q3 fy24:

Launched a number of products in the last quarter.

Hero Xtreme 125 cc

Hero Maverick 440cc

Tata motors punch (EV & IC)

Switch mobility (EV wing of Ashok Leyland, IeV3/V4 series)

Daimler (Prime model)

New products/solutions being worked upon:

Majority of these products are being worked upon(in development), some of them are in the proof of concept stage. Most of these products contribute to revenue from Q4 FY25. So significant upside can be seen in FY26 revenues and could be a contributor to the FY26 guidance of 3600 crores.

E-cockpit with one of the major customer

Battery management system

Disc brakes

SIBROS partnership.

This is not exclusive to Pricol but the solution that Pricol is working upon is kind of exclusive and Sibros telematics in the cloud is one part of it. Pricol is working on an end to end solution and Sibros will be part of it.

Oil & air pumps

Launched with Tata motors and Ashok Leyland last quarter

Telematics solution

Top customers:

2 wheeler:

TVS, Hero, Bajaj, Royal Enfield, Honda & Suzuki

Passenger vehicles:

Tata motors, Ashok Leyland, Volvo & Eicher

Off-road: JCB

Guidance

Order book is looking healthy & very strong. Guidance of 3600 crores by FY26 is intact and depends on the customer launches & how market is going to be. As I mentioned above there are a number of products being worked up on which should cater to this guidance starting Q4 FY25.

Company is also looking for inorganic growth in the non auto segment, nothing at the moment to speak of.

Red sea impact: There is a couple of weeks of delay in shipping and the company has rerouted and now came to normalcy. Export is 10% of revenues, so not much of an impact.

Margins:

EBITDA margins 9M FY24: 12.31% vs 11.83% same period last year

Company guiding a 13.5% EBITDA margins and is expected to reach before FY26.

There was a question on margins being affected when they enter into ore electronics, to which management answered that they are transitioning into a solutions company from a product company (providing end to end support). Company is working on the off the shelf component which customers can easily plugin.

A similar question is being asked on E-cockpit solution where Visteon is a competitor, management agrees that there is competition and focuses on quality of the solution/innovation to win customers and penetrate. For e.g. they entered into passenger vehicles in 2020 and are doing quite well winning customers in the segment. They are doing good in the EV segment as well.

What’s Pricol moat?

One of the questions was about Pricol’s moat in winning new customers/penetration in the market. Below is what management said:

4.5% of revenue spent on R&D for the last 5-7 years.

In-house machine building (they do their own tools, own lines, own plastic injection molding & own PCB population)

Exclusive tie up with many of the chip manufacturers & have long term contracts with them.

A little bit of research is needed to see if these are really the moats and compare this with some of the best in the industry (say Sona comstar, UNO Minda etc.)

Industry is moving from mechanical to digital to tft to high end digital information systems. This helps increase kit value and Pricol is innovating in this segment and in the sweet spot to capture the market.

Awards received in Q3fy24:

Technology & Innovation award from Daimler trucks.

Best quality performance from JCB

Gold award from Tata motors.

Answers to “things to look for in the coming quarters from Q2 fy24” update:

Improvement in EBITDA margins (they are a bit lower compared to last year numbers as against management commentary of this going up)

9M FY24 EBITDA increased by 48bps and 119bps short of guidance of 13.5%

EV sales pick up in coming quarters

There are some hiccups in EV sales this year but this should do very well starting next year. Management mentioned a number of products they are working upon for EVs.

Minda corp stake increase related issues

Minda corp fully sold its stake and this issue is gone now. They made a good profit though (but may have gotten a bad name?).

An eye on the growth as this year it seems to be doing less than what is required to reach fy26 target.

My guess is FY26 will be a good revenue generating year compared to FY25 as several new product launches are going to happen from Q4FY25.

Things to look for in the coming quarters:

EBITDA margins : guidance of 13.5%

EV sales pickup/penetration.

Revenue target of 3600 crs by FY26.

Inorganic growth by acquiring something from non-auto space (management mentioned about 4000 crs by FY26 out of which they expect 400 crores through inorganically).

Disclosure:

Invested and have been buying after Q2 results. Currently forms about 5.66% of the overall portfolio with average purchase price of 305.

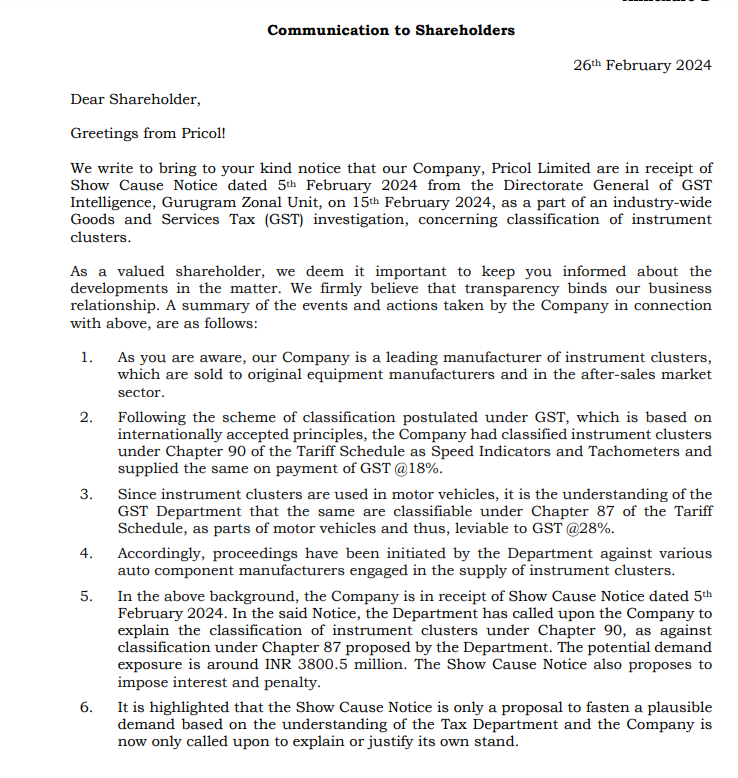

Thank you for the info. For ease of understanding, it is better that you add a foot note on what does this circular mean and its impact on PRICOL fortunes.

What is your opinion on whether economy is doing well or not?

GDP Seems to be doing well only based on investment, not on Consumption. GVA is just 3% up. This seems believable when all HUL /Nestle / Dabur, etc shows muted growth. But then, How Come 2- wheeler Sales keep increasing, that too in double digits?