• FY26 Guidance of 3600 crores organic sales maintained unless any

catastrophic geopolitical event

• Slow down in ev 2 wheelers due to fame subsidaries ( Loss of sale)

• DIS sales 65% comes from 2 wheelers

• If and when there is need promters will incrase stake in the company

• Steadily increasing margins continuing to aiming for 13.5% ebidta margins

• New products ususally contribute by around 20%

• Revenues from MOU ventures to start contributing from FY26 ( most of them being exclusive in nature)

• EV two wheeler contributing 7-8% of volumes ~ Value contribution is a bit higher

• 8/10 ev two wheeler’s TFT display is from pricol

• Two wheelers Average mechanical DIS cluster costs 300 rs vs 1250 electronic ( Can go up till 2500 rs avg)

Key Variables to track here would be is the loss of revenue due to fame subsidaries is on off or a structural loss

Also the execution towards FY26 3600 Crores story

Driver Information and Connected Vehicle Solutions (DICVS)- 65%

Actuation Control and Fluid Management Systems (35%)

ACFMS is mostly towards export so slightly higher Margin.

But DICVS Margins are also improving as electronics prices have Stabilized. From average Value of Rs 300 per DIS now we are in the range of Rs 1200 but going forward it will be around 2500 in next 3 years.

In DICVS Segment 65% revenues comes from Two wheelers, 20% from Commercial vehicles and rest from Passenger Vehicles.

Revenue growth during this Quarter is slightly less mainly due to less EV sales due to FAME subsidy issue. Now EV again started to pickup from October. EV Vehicles form 8% of the sales by Volume and slightly more by Value.

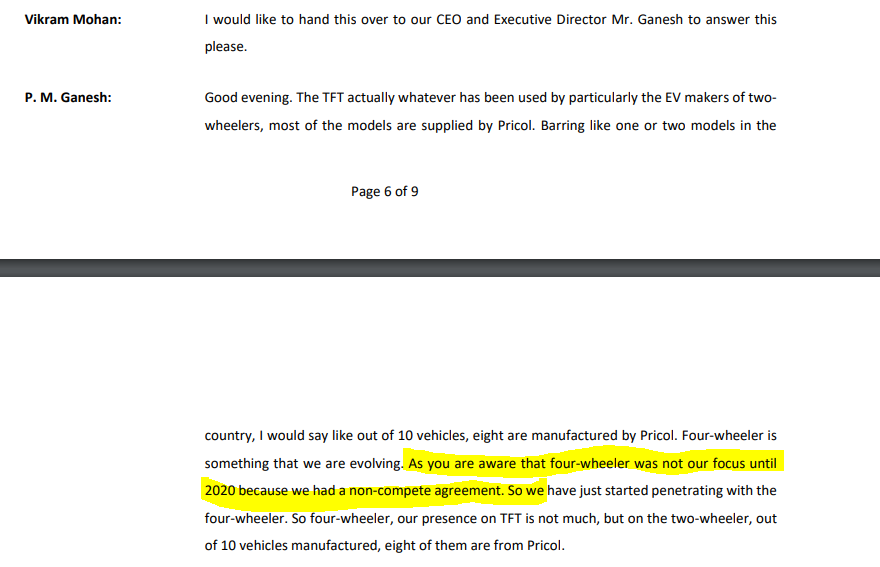

In the Two-wheeler segment 8 out of 10 TFTs were manufactured by Pricol. In Four-wheelers we didn’t start early due to non-compete clause which ended only in 2020. So, now only we are starting in Four-wheeler segment.

In The ACFMS we have moved from low value products like oil pumps and chain tensioners to BLDC fuel pump and electric coolant pump. This has increased the average selling price from Rs150-200 to more than Rs 1000.

Revenue Guidance of 3800 crore to 4000 crore by FY26 maintained.

Revenues from Joint Ventures like Sibros and BMS power Safe will start from FY26.

EBITDA Margins of 13.5% will be achieved much before FY26 with sequential improvement of 0.3 to 0.4 in every Quarter.

Capex Plan:

Out of the total 600 crores Capex plan, 150 crores spent on last year, 200 crores is being spent this year and remaining 200 crores to be spent next year for modernization which will help in making revenue in the range of Rs 3800 to 4000 crores.

Q2 fy24 582 (yoy growth of 12.8% & qoq growth of 7.8%)

Q2 fy23 516

Q1 fy24 540

H1 fy24 1122 (yoy h1 growth of 16.5%)

H1 fy23 963

Net profit:

Q2 fy24 33 (yoy numbers not comparable due to very less tax rate last year, qoq growth of 3.8%)

Q2 fy23 48

Q1 fy24 32

H1 fy24 65

H1 fy23 68

Impact of FAME subsidy issues on EV sales in the first half of fy24. Though the volume is less (about 7-8%), the value is higher due to higher kit value in EV sales. This should stabilize going forward, seeing positive traction in October sales.

Revenue distribution

65% from driver information systems and connected vehicle solutions(DISCVS). 35% from actuation, control and fluid management systems(ACFMS). This will be more or less going forward (+/-2%).

With in DISCVS:

Around 65% from two wheelers

20-25%% from commercial vehicles

Remaining from four wheeler passenger vehicles

Share of new products in overall sales is about 20%.

This should go up slightly higher in fy25/26 as they are launching new disc brakes and other products.

Capex

600 crores of capex planned in the next couple of years starting last year. About 150 crores was spent last year, about 200 crores is being spent this year, and another 200 crores would be spent in the next fiscal year. This is to enhance capacities, improve productivity and also going for modernization of some of the older plants. This will take our revenue up to about 3,800 to 4,000 crores.

Pricol has made key investments in Surface-mount technology (SMT) for printed circuit board (PCB) Assembly Line and Disc Brake assembly lines.

Guidance

Company guiding for 4000 crores of revenue by fy26. 3600 crores by organic growth and 400 crores of revenue by inorganic growth.

H1 growth was around 16%, expecting a similar range in fy24.

In a capex related question management does mention that they are looking for inorganic growth as well if something exciting comes up.

Margins

EBITDA margin guidance of around 13.5% in next couple of years with an increase of 0.3-0.4% every quarter. This should happen before Q4 fy26. Current margins: Q2 fy24 12.42% vs Q2 fy23 12.97% and H1 fy24 12.57% vs H1 fy23 13.01%.

Margins generally higher in ACFMS export products.

Kit value

Two wheelers kit value has evolved from 300 to the current value of 1200. Expecting it to reach about 2500 in the next 3 years.

Four wheeler passenger vehicles, still a nascent stage. Commercial vehicles this number is much bigger.

ACFMS vertical, they were moving from small value oil pumps and chain tensioners to more complex BLDC fuel pump, electrical coolant pump, and other products which are more towards the Rs. 1,000 mark as against what we were supplying at Rs. 150 and Rs. 200.

8/10 EV two wheelers use TFTs from Pricol. Four wheeler is still at a nascent stage.

MoUs

Signed MoU with BMS powersafe to produce battery management systems for the Indian market.

Signed MoU with Sibros for Connected Vehicle suite of solution, for which trials have already started for the proof of concept ideas with at least 10 vehicle makers.

Management expects revenues for these products will start flowing down from fy26. 4000 crores guidance is based on the current order book and does not include revenues from these MoUs.

They also signed an agreement with TYW based in China for the advanced display information systems for the Indian market. More details of this are expected in coming quarters.

Ownership

Minda corp has acquired a stake of 15.7% in the company through open market purchase. In response to this, management has increased stake by 2% in Q1 fy24. Overall management is owning 41% (including extended family members) and if need rises they would like to increase this further.

MIscellaneous

Other expenses to be in range of around 42 crores going forward (in line with inflation)

Things to look for in the coming quarters:

Improvement in EBITDA margins (they are a bit lower compared to last year numbers as against management commentary of this going up)

EV sales pick up in coming quarters

Minda corp stake increase related issues

An eye on the growth as this year it seems to be doing less than what is required to reach fy26 target.

Disclosure: Got interested and started buying after Minda corp bought the shares from the open market. Currently forms about 3.7% of the overall portfolio. Will continue to add it in the coming days. Not an expert of valuation, the goal is to buy good companies to hold for the long term as long as the underlying business is performing.

There is no disclosure of any development in the 4 wheelers and commercial vehicles segment.

This will help Pricol grow faster, but their focus is only on the 2-wheeler segment.

Please share the insight. Is there any entry barrier in the other segments?

On 4 wheels, it’s still a work in progress since their JV with the foreign partner ended in 2019. On 2 wheelers, I think they are just following the market forecasting where it is predicted that till 2030, EV 2 wheelers will have better growth than any other EV categories…

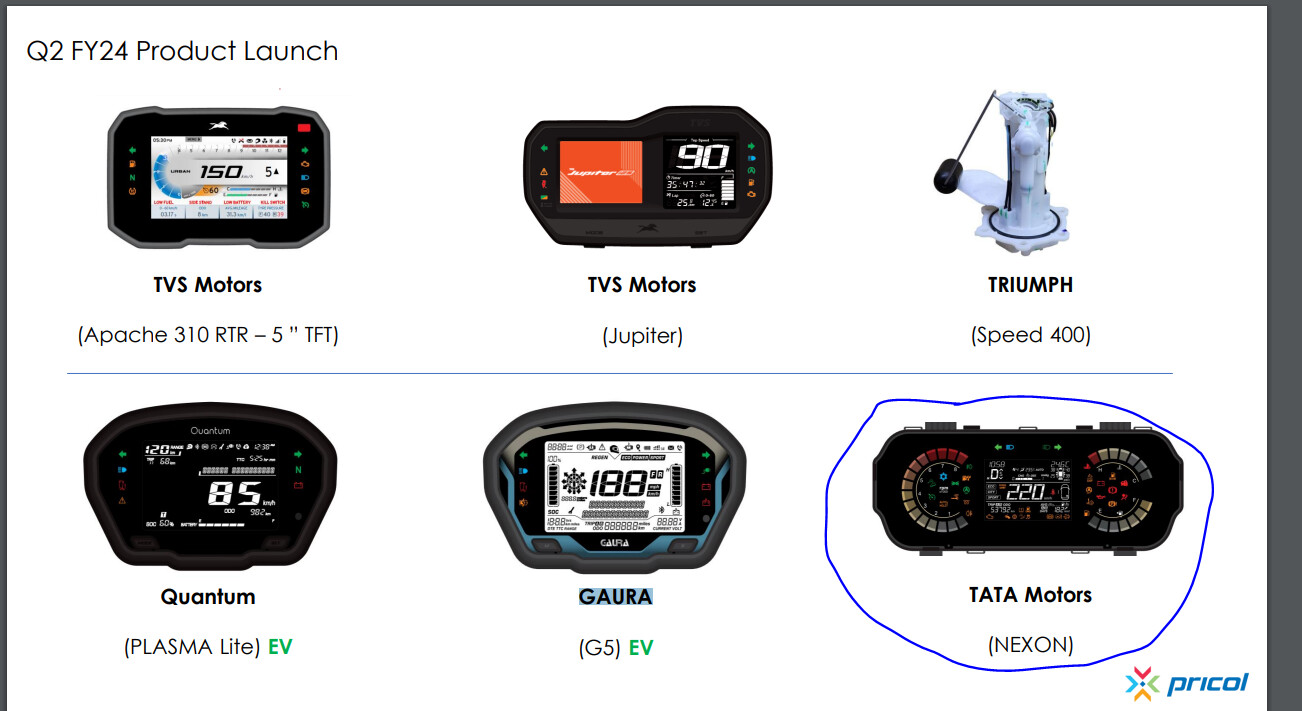

They have very less revenues from four wheeler passenger vehicles. I think they are trying to penetrate into four wheelers. In Q2 FY24 presentation there is mention of product launch for Tata Nexon.

Any particular reason for barring Ola? Since Ola has emerged as market leader in 2 wheeler EV space, not supplying to them can impact the growth numbers?

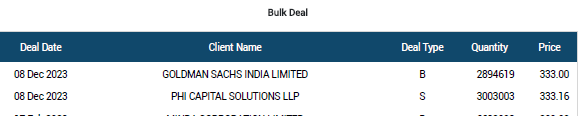

Looks like PHI is exiting this space. They sold their entire position (4.96%) in minda corp as well. Also since it got absorbed by a reputed institutional investor doesn’t look like something to worry as such.

Looks like Pricol shares are being picked up by marquee FII investors - first it was Goldman Sachs and now Franklin Templeton…its clearly a big thumps up for the company

Looks like Pricol has got into high valuation Zone. PE Is above 35 now ? What do you guys think of adding at this moment ? (Or) Is it good to do nothing, just hold what you have ? (Base case scenario is still yielding 10% cagr at his Market cap assuming revenue grows only 15%)

Better to wait for another quarter and see the results. Management had given guidance of doubling the revenue in 3 years but last quarter results was not in line with the guidance. So better wait and see what is this quarter’s results. One more point is that the entire auto industry is still not showing any slowdown per se. So keep some faith on the management…

I also feel that it is now in the high valuation zone and all the future growth prospects (3700 cr guidance in 3 years) is already factored in. The last quarter results were a little on the disappointing side. Tracking it closely. I feel if the results in the next quarter are also a little muted, then this could come in the buy zone. Overall I still trust the management to execute as auto is currently having a lot of tail winds.

PS: Invested from sub 200 levels and biased