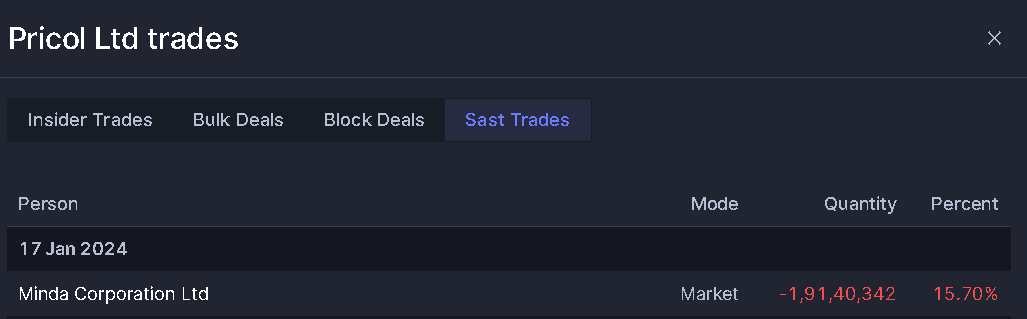

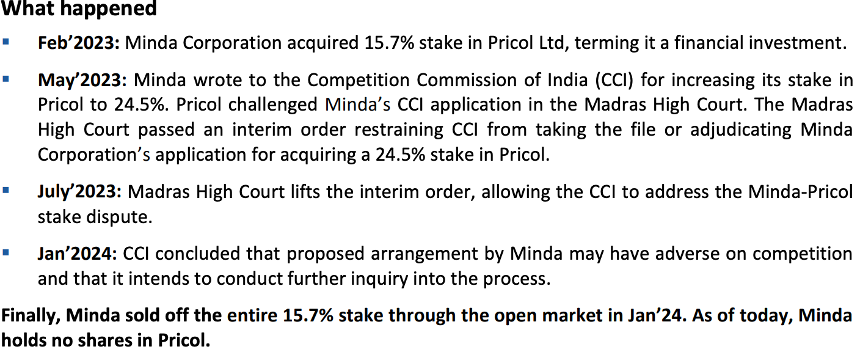

Minda recently got clearance/approval from CCI for buying stake again. How do you think event will impact Pricol?

Disc: holding from 2 digit levels.

Minda recently got clearance/approval from CCI for buying stake again. How do you think event will impact Pricol?

Disc: holding from 2 digit levels.

Minda sold their stake completely or the lion share in January itself. This fall is not because of that i believe.

Definitely not because of that. Just saying that if the management succeeds in executing their 3.6k crore Revenue guidance at 14% EBITDA margins by 2026, the share is then currently trading at FY 26 Forward PE of 15 after this fall.

But any idea when will be get a clarity on the GST issue? So far the management has said that a similar issue went in their favour earlier so they expect this to be on same lines.

Pricol near 200DMA @326 & Fib Retrace level 0.5 @327 .It breach 30 WEMA @358. May be consolidate & trend change.

overall market is correcting check vstop on monthly timeframe

GST Issue is the main concern before fresh move. Once there is clarity on the tax dispute, fresh moves may be possible.

Sector: Auto Ancillary

LCD->TFT

Driver Information System (DIS) is used to indicate the instantaneous changing parameters in the vehicle such as speed, engine RPM, engine temperature, fuel level, fuel economy, service reminder, phone connect, navigation assist and various warning indicators at vehicle level.

In Feb 2022, The Co. entered into a strategic technology partnership with Sibros Technologies Inc., a California-based co. providing Over-the-Air (OTA) connected vehicle software systems for OEMs worldwide, to deliver deep-connected vehicle solutions in the Indian and ASEAN markets.

In 2023 Pricol Ltd announced a partnership with China-based Heilongjiang Tianyouwei Electronics for Driver Information System (DIS), including e-cockpit, heads up display, for vehicle segments.

In 2021, Pricol Limited, came into a strategic partnership with Candera, a leading Human-Machine Interface (HMI) tool provider and development partner for worldwide automotive and industrial customers. This technology partnership with Candera will bring global HMI solutions into Pricol’s range of Next Generation Connected Driver Information System (DIS) products serving across all vehicle segments.

In 2022, Pricol in partnership with PSG Institutions has launched a Center of Excellence (CoE) to develop high efficiency micro motors and Robotics and artificial Intelligence based processes and equipment.

In 2022, Pricol has entered into a partnership with BMS PowerSafe, a part of Startec Group, to manufacture and sell Battery Management System (BMS) for Indian Market. BMS PowerSafe is recognized as the top 3 pure players of BMS suppliers in Europe.

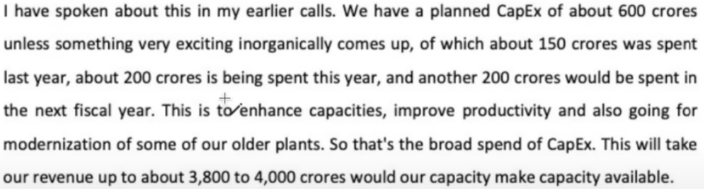

Pricol has a planned capex activity for Rs. 600 crore from fiscal 2023 to fiscal 2025 to enhance capacity( from Internal accurals), mainly of new products, which are part of the productivity linked incentive (PLI) scheme and also for routine modernization and refurbishment of lines.

Concall Highlight

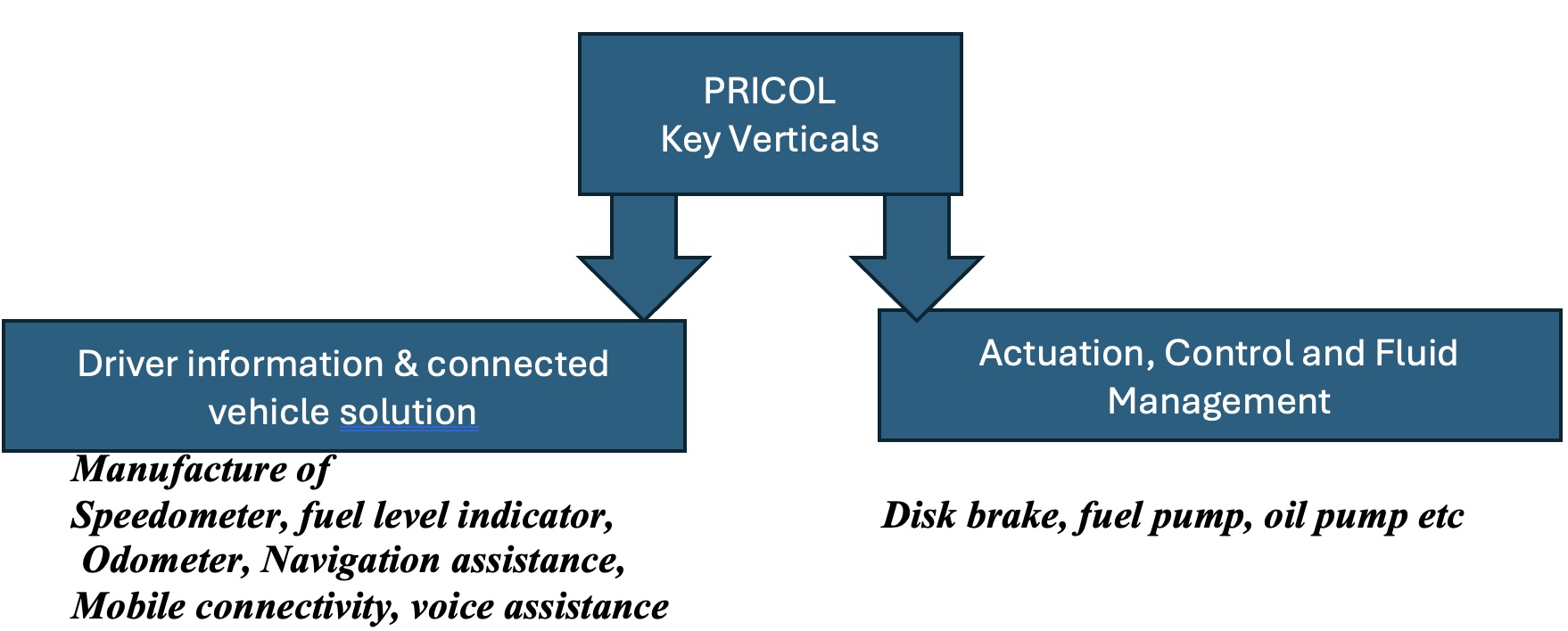

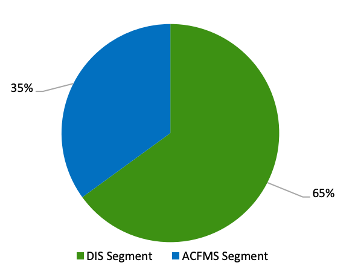

• 65-70% from driver information systems and connected vehicle solutions(DISCVS). 30-35% from actuation, control and fluid management systems(ACFMS).

DISCVS

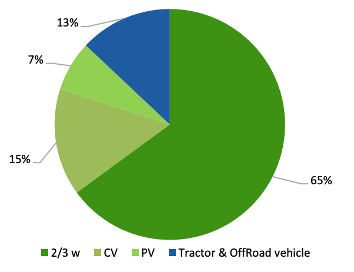

• ~60% from 2 wheelers, ~35% from commercial and offroad vehicle, balance from passenger vehicle

Market cap = 4,746cr (>1000 cr)

PE = 36.8 < 33.26 industry PE)

PEG = 1.07 (should be < 1)

ROCE = 20.1

ROE = 18.3

D/E = 0.12 ( should be < 1)

CMP/BV = 5.99 ( should be < 1)

CAGR sales growth 3 yrs = 16%

CAGR profit growth 3 yrs = 47%

EV/EBITDA = 18.17 (which is > 10)

Operating margins = 12%

Pricol’s net debt/equity level has always stayed low - below 1x - due to its efficient cash flow generation and timely repayment of debt.

• The rise in debt in FY20 was mainly due to high capex in the previous 2 years followed by low cash flow generation (semiconductor shortage issues). However, this was repaid quickly starting next year.

• CAPEX funded by internal accurals

Total reserves increased = YES

Total borrowings decreased = YES

Total fixed assets increased = YES

Cash flow from Operations in Last 3 years (Positive + sequential growth ) = YES

Net Cash flow for last 3 years (Positive + sequential growth) = YES

Debtor days - reduced from 56 to 50

Inventory days - reduced from 81 to 72

Days payable - reduced from 92 to 75

Cash conversion cycle - reduced from 45 to 47

Working capital days - slight decrease from 24 to 23

Financial risk profile is healthy with low debt levels and nil debt funded capex plans over medium term

FII holding - 6.50%

DII holding - 6.92%

FII shareholding increased in Dec month by 2.54%

DII shareholding increased in June month by 1.33%

Public Holding- 17.78 % is private entity out of 48%

Q2 concall

Minda’s investment in its competitor Pricolserves as a testament to Pricol’sleadership and technological prowess in the industry.

PLI scheme:

With an earmarked budget of $3.5 billion (or Rs 25,938 crore) for the automotive sector, is designed to offer financial incentives of up to 18%, fostering the growth of domestic manufacturing in Advanced Automotive Technology (AAT) products and encouraging investments throughout the automotive manufacturing value chain.

Pricol has been approved by the Ministry of Heavy Industries (MHI) for participation in the Component Champion Incentive scheme. Within the ambit of this PLI initiative, a total of 95 applicants have received approval, with 20 recognized as Champion OEM and 75 as Component Champion.

Await further clarification regarding qualifying products, capex and timeline for the same. Will be using CAPEX for same

Addition of customers and products – diversification to non-automotive business. As part of a strategic move to reduce reliance on the cyclical automotive sector, Pricol is actively exploring entry into the industrial instrumentation segment

The management has indicated an estimated capital allocation of Rs 2bn for a potential acquisition, signalling the company’s readiness to invest in strategic targets if identified.

While the management has not announced any acquisition yet, this would reduce the dependence on the cyclical automotive sector and bring uptick to the margins along with robust revenues, considering the strong technological expertise and R&D capabilities that Pricol possesses.

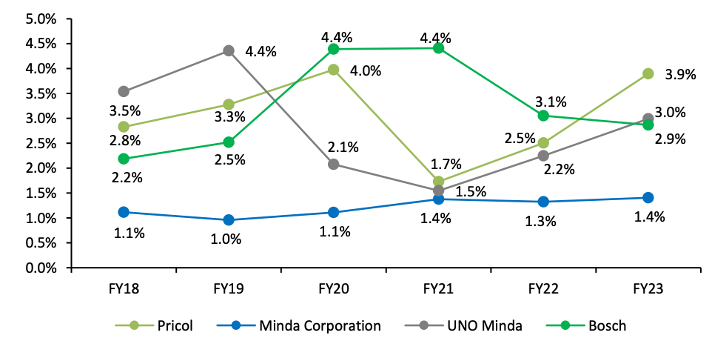

Pricol’s R&D expense as a % of standalone revenues stands tall versus competitors like Minda Corporation & UNO Minda, and is comparable with Bosch. Going forward, we expect R&D as a % of sales to remain in the range of 4-4.5%, showcasing Pricol’s commitment to fostering innovation for growth across all product development functions.

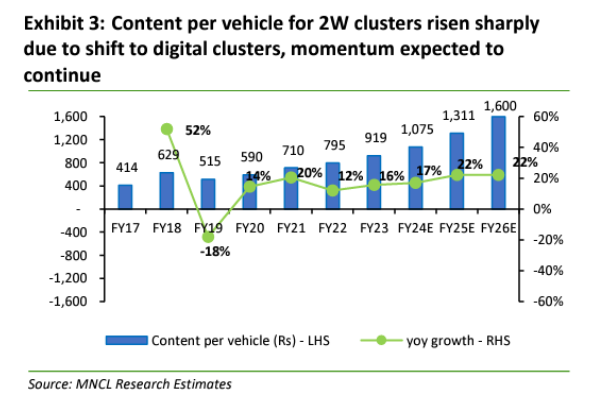

The introduction of BS-VI emission standards starting April 2020 spurred the trend from mechanical to digital instrument clusters, which are technologically advanced and command a higher content per vehicle. Pricol was quick to embrace BS-VI standards and secured numerous new business across various segments, leading to ~40% of the overall revenue for FY2020-21 contributed by these new business acquisitions.

R&D expense as a % of standalone revenue stands at 3.9% as on FY23

• Pricol’s business was facing multiple headwinds in the form of increase in freight cost due to the Red Sea issue and integrated circuit (IC) shortages

This drop in sales could go on for a few months, till the brands find a way to package their EVs to make it more attractive

Stock has rallied in past 6 months by 16%, Has very attractive fundamentals , can be bought at 370’s range , should cross 450-470 in next 1 year , approximate upside of 30%.

Short term impact of FAME policy on EV sector may slightly impact the stock**

Disclaimer: Not Holding the stock

How can you be so sure about the 30% ?

Pricol Limited is engaged in the business of manufacturing and selling of instrument clusters and other allied automobile components to OEMs and replacement markets.

The business was started in 1974 and is headquartered in Coimbatore, Tamil Nadu.

The company provide solutions in two verticals:-

Driver Information System (DIS).

Actuation Control & Fluid Management Systems (ACFMS).

DIS -

DIS monitor’s the vehicle systems and provides us with the parameters such as speed, engine RPM,

fuel level, phone connect and various warning indicators at vehicle level.

The DIS are currently being offered via LCD, TFT and Hybrid mechanism.

LCD -

LCD Clusters offers a digital monitoring of critical vehicle information in different type of LCDs like Segmented LCD / Dot Matrix Display, Positive Type, Negative Type, Color LCD with different background color White / Blue / Red / Amber.

Credit - [https://pricol.com]

TFT -

TFT Clusters offers a digital monitoring of vehicle information with different sizes of TFT like 2.8”, 5”, 7”,10.25 &12.2”. Different Themes & Modes are Possible according to the Rider’s Selection and Vehicle Ride mode, respectively.

Credit - Pricol

Hybrid -

Hybrid Display Clusters offers digital monitoring of critical Vehicle Information in LCD and Information about Safety, Security & Convenience in TFT display.

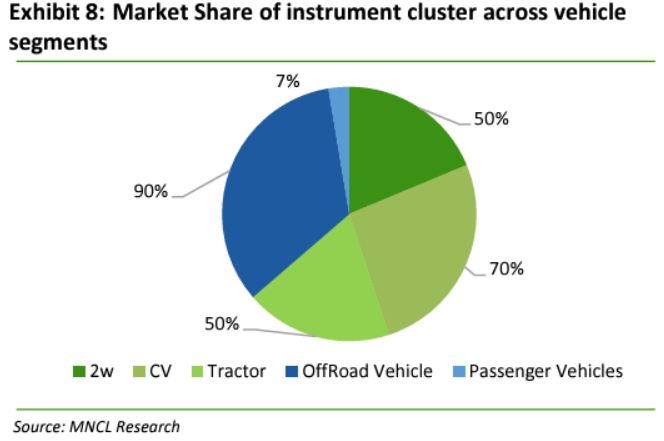

Pricol ranks as 2nd largest manufacturer globally for instrument clusters.

It holds a substantial market shares-

Credit: MNCL Research

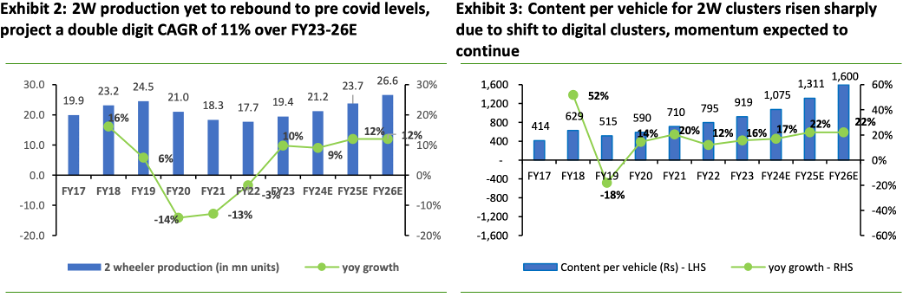

With the implementation of BS-VI standards, There has been a gradual change noticed in the instrument cluster industry with the transition from the manufacturing of mechanical clusters to digital which have 3x/10-15x higher content per vehicle compared to mechanical clusters.

The revenue contribution by vehicle segment in DIS for FY23 is as follow -

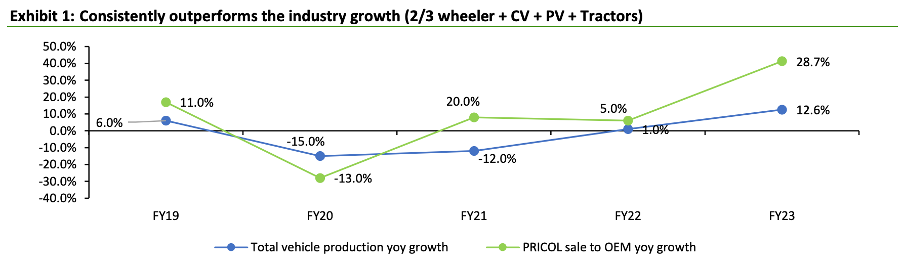

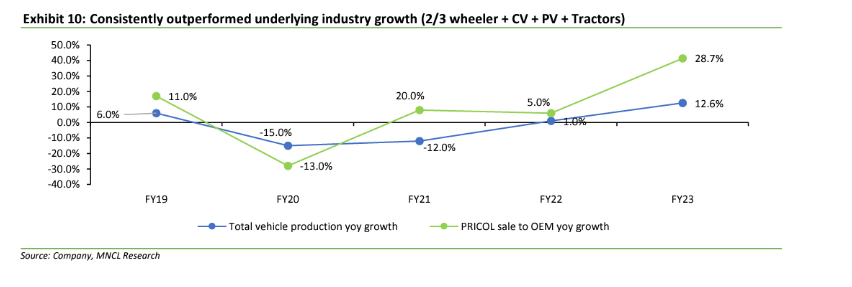

Since, it’s a proxy to vehicle manufacturing companies, Its sales are directly proportional to the production of vehicle units.

With the headwinds during the pandemic era, the challenges posed by BS-VI standards, shortage of semiconductor and higher interest rates, the sales growth was sluggish during FY19-22.

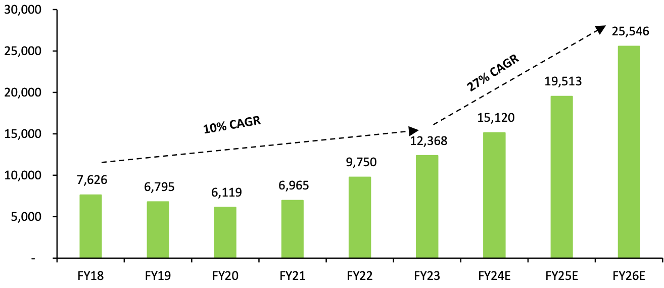

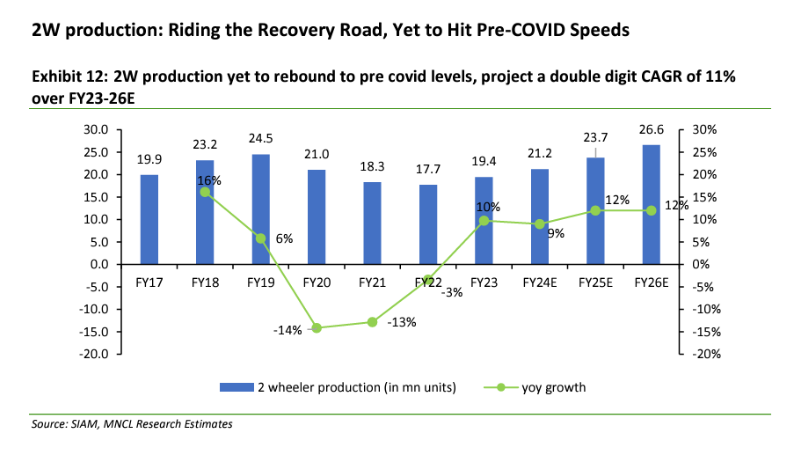

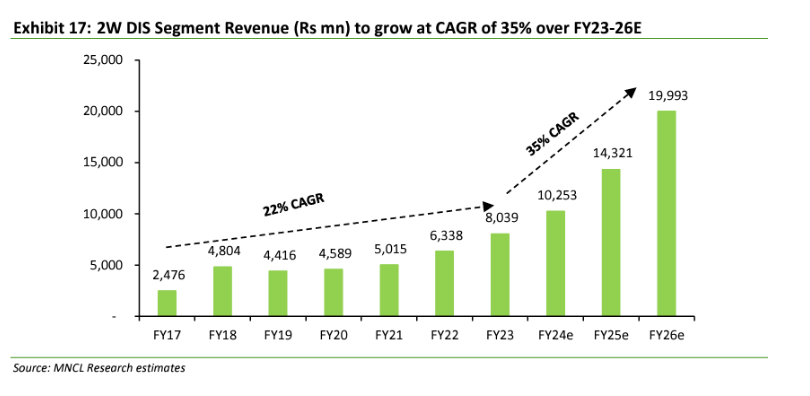

Now since the automobile industry is started to cooling off and various factors are in placed to be aligned and with the likely reversal of interest rate cycle leading to substantial moderation in rates, surge in replacement demand and increase in rural demand, The 2W industry is expected to grow at a CAGR of 11% from FY23-26E and with a market share of 50% in 2W instrument clusters, Pricol is positioned to be a major beneficiary of the robust growth in 2W production.

2W DIS revenue is expected to grow at a CAGR of 35% over FY23-26E.

Company Key Customers in the 2W segment:-

The company is the market leader with 70% of the domestic market share in the commercial vehicle instrument cluster.

The company has increased its market share from 45% to 70% over the FY19-23.

Company key customers in CV Segment:-

At present, Pricol commands a 7% market share in the PV segment, primarily due to its partnership with Tata Motors and is poised for continued growth in collaboration with them in their ICE and EV offerings.

Company key customers in PV Segment.

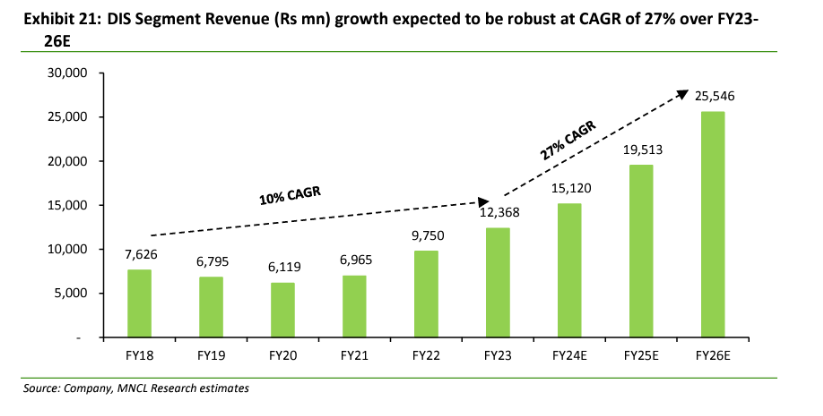

With the increasing premiumization of transitioning from mechanical to digital cluster with an increase in TFT shares to 20% by FY26E and higher CPV, 2W production reaching pre-covid level and expected to grew at CAGR of 11% over FY23-26E, More EV penetration and growing presence in PV segment.

DIS segment is poised for a robust 27% CAGR over FY23-26E period.

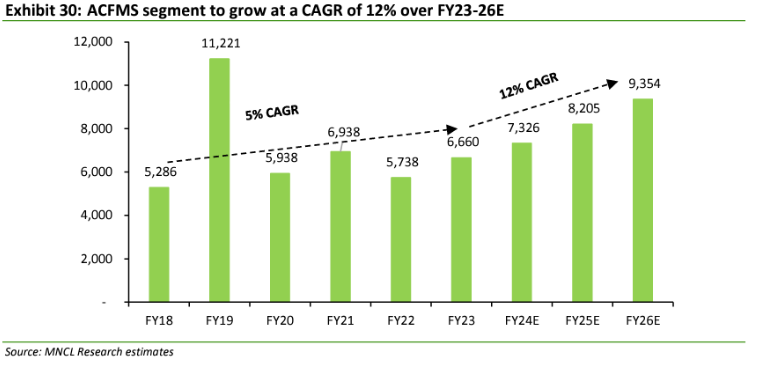

Actuation Control & Fluid Management Systems (ACFMS) segment:-

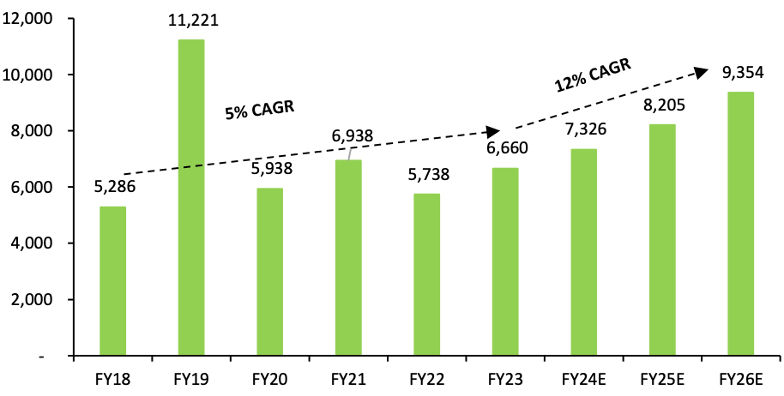

The ACFMS segment contributed 35% to total consolidated revenue in FY23. Currently, water pumps, oil pumps, and fuel pumps collectively contribute ~60-70% to revenue of the ACFMS segment.

Pricol Market Shares -

Pricol introduced new products under ACFMS i.e electrical coolant pumps, electrical oil pumps and BMS foray into EV-specific product as 2W ICE engines are at the risk to being obsolete due to increasing EV penetration over the next 5-7 years.

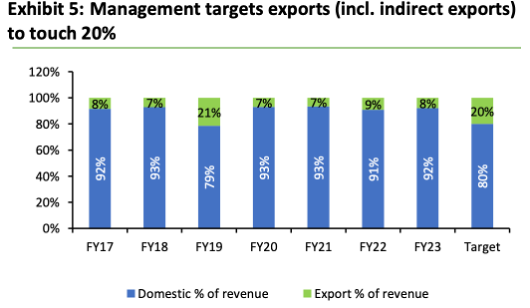

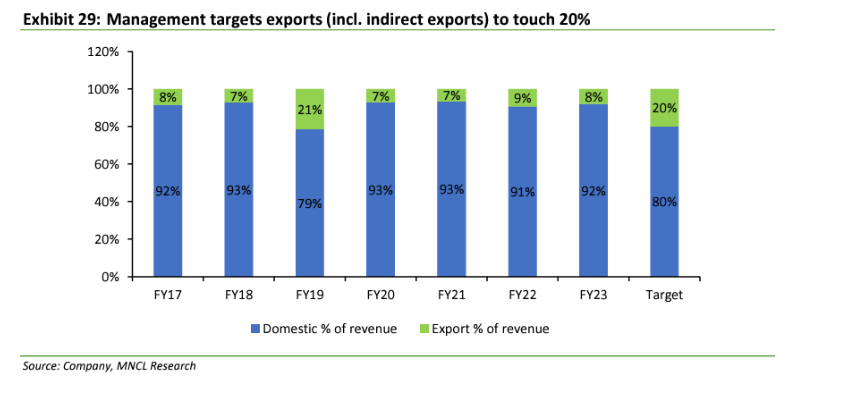

The ACFMS segment constitutes a significant portion of exports, accounting for ~90% of the total exports in FY23. Exports constituted 8% of the total consolidated revenues in FY23 and the company aims to scale up this to 20%.

The ACFMS segment grew at a CAGR of 5% over FY18-23.

With the selected customer win in FY23 for the product electric coolant pumps, fuel pump module assembly for Tata Motors and Bajaj.

The ACFMS segment is expected to grow at a CAGR of 12% over the FY23-26E with expansion in the export geographies, increase in domestic market share for the electric coolant and oil pump.

Risk associated to the thesis :-

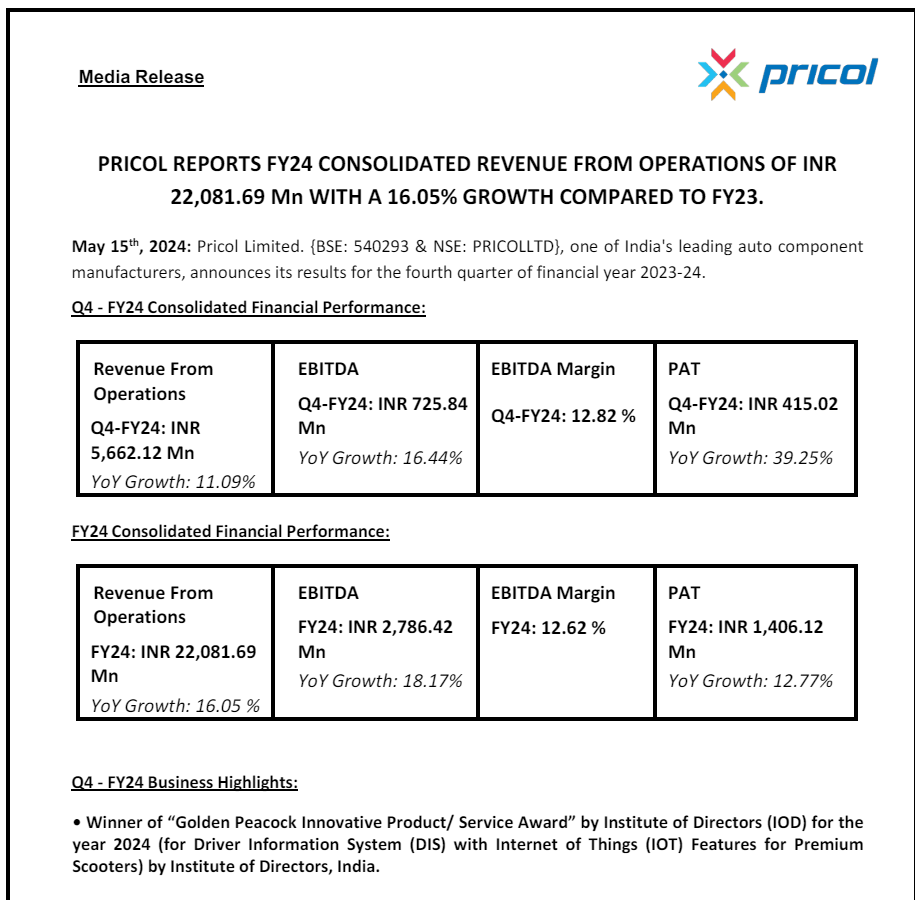

Excellent results by the company. 12% topline growth and 39% profit growth YoY.

https://www.bseindia.com/xml-data/corpfiling/AttachLive/b22951d7-a2fa-4c3e-a143-b365292dc4ab.pdf

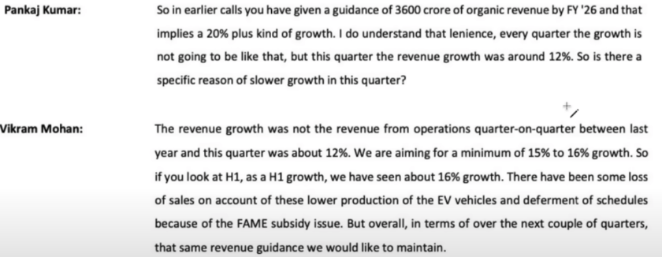

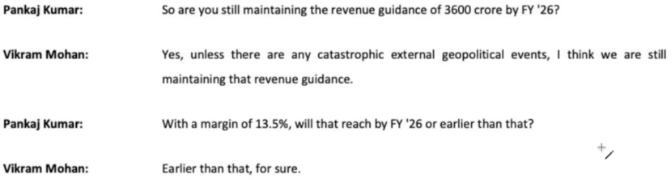

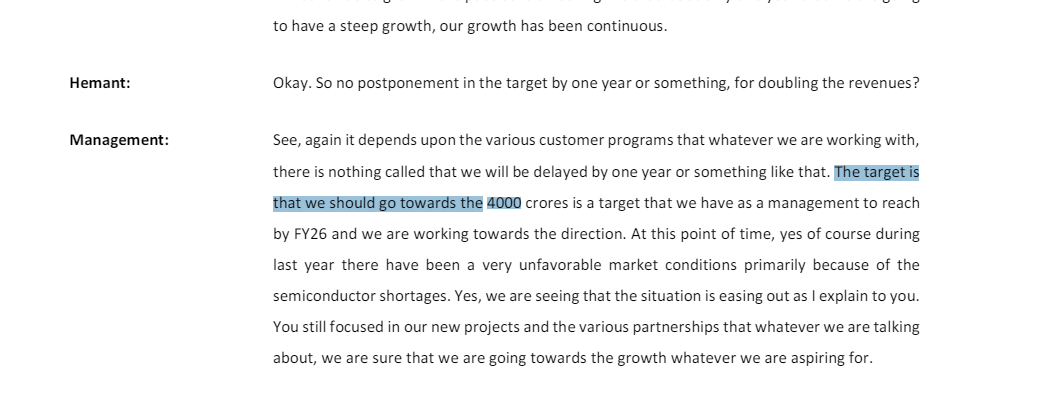

As per today concall Management has lowered the F.Y 2026 revenue guidance by 10% to 3600 cr ,earlier management guided for 4000 cr revenue and also export guidance lowered to 10% of sales instead of earlier 20% .

Wrt to Revenue guidance for FY 26 is Rs 3200 cr organic and Rs 400 cr inorganic. Company reiterated that they never gave guidance of Rs 4000 crin earlier calls and they gave only Rs 3600 cr (3200+400) projection. This was the reply given by the management to a pointed question on Rs 4000 cr guidance. FYI

The target or aspiration or guidance (or whatever one wants to call it) for 4000 cr was definitely mentioned. This is from Q3FY23 concall. Link below:

https://www.bseindia.com/xml-data/corpfiling/AttachHis/9d17bfbe-7a7c-459a-9360-d5059aba278c.pdf

Disc: Was invested till last year.

Mangment exports aniticipation was 20% earlier and now reduced to 10% . So reduced the guidence of topline from 3600cr to 3200cr from organic side. Inorganic side mainatining the same 400cr guidence. So total 3600cr topline guidence for FY26 by the managment.

Q4Fy24 result has been unexciting, while sales growth has been 16% but it was below expectation of 19-20%. Mgmt has been conservative in giving guidance, giving a sustainable guidance of 15-16% however, they remain optimistic of achieving 19-20% growth in next 2 years. Mgmt has been able to improve its EBITDA margin and is quite optimistic of achieving 13.5% in next 2 years.

Have launched disc brake and guiding for 120Cr rev in Fy25 ramping up to 300Cr by Fy27. E-Cockpit is ready and is being showcased to potential customer. Head-up display is also ready for customer inspection. BMS is seeing slowdown probably due to slowdown in EV sales in US.

Big setback is from export side, earlier targeting for 20% rev from exports, but looking at the current situation in US & EU revised it to 10%.

I am of the view that, mgmt is on track. There is temporary slowdown in EV adoption plus US & EU market is not looking good currently. Going forward I believe; the domestic auto sales will decide the momentum in this stock. At current valuation of 450rs, I believe it is fairly valued & there is no MoS.