In my understanding, InvIT is just a monetization route where Powergrid can get back their invested equity along with their returns and then decide whether to give it back to shareholders, pay down debt or bid for more projects. Its important to note that Powergrid only monetizes TBCB assets which are acquired via competitive bidding (where ROEs are lower) compared to regulated assets where they make 15.5% ROE + incentive income.

About the bidding details, please refer to the Motilal report on this thread. I dont have enough expertise to give an informed answer.

The main reason for me buying Powergrid was that they had large CWIP which was supposed to come onstream and lead to improved freecashflow which should be returned as dividends. This thesis actually played out and I exited last year. You can see my thoughts below.

The reason for my exit was mainly around growth concerns as most of their large assets already got commissioned. Hope this is of some help

Disclosure: Not invested (no transactions in last-1 year)

To add to what Harsh mentioned, pl see below news on pginvit for additional tranches from power grid. Power grid has found InvIT route to be expensive and they are looking at securitisation of cash flow route. I think they also mentioned it in latest concall. Pginvit will be impacted significantly by this move

Can someone highlight the impact of transfer of these 6 assets SPVs from REC to power grid ? Will the cashflow if PGINVIT has anything to do with this ?

These are new project won by Power Grid through competitive bidding - they will have to build these assets first.

Bids are floated by either PFC or REC’s consulting arm with SPV incorporated and Transmission Services Agreement signed with counterparties by the SPV. After Reverse auction, the SPV is transferred to the Successful bidder

I do not think there is absence of operational assets to handover for Power Grid. That is why they had asset monetisation targets for FY23. They have mentioned in their concall about evaluating InvIT route due to costs involved.

The level of governance in PSUs is really pathetic. The board and management of of such an important PSU are completely helpless and can only ask the ministry to make an appointment of an independent director

Similar question had come during Con Call of IndiGrid, looks like the receivables are not evenly distributed thru the year, some quarters get higher cash flows, hence may have to dip in reserves.

Nothing alarming

I find it puzzling that PG InvIT trades at a 25% premium to NAV. The reasoning usually provided is that it has an extremely low leverage at less than 1% LTV and it can undertake fully debt funded NAV-accretive acquisitions at highly competitive cost of debt due to its sponsor pedigree.

But the sponsor, Power Grid has itself indicated that they are looking at securitizing cash flows of their existing assets for monetization rather than an outright transfer to the InvIT. Also, PG InvIT’s management has indicated that there aren’t enough third party transmission assets available for them to expand their portfolio. Even IndiGrid has had to diversify by acquiring generation assets to expand their portfolio. PG InvIT isn’t keen on acquiring non-transmission assets. In this scenario, what use is its balance sheet if there are not enough opportunities to deploy it?

Are there any other factors that I’m missing which would justify the significant premium to NAV that it enjoys?

Apologies for posting here as there’s no separate thread for PG InvIT

This is the reason why PGinvit is stinking and has fallen from 140 plus to 106…if there is no addition of new project, eventually maintenance costs will eat cash flow and you can keep dipping into reserves so much, so as to keep paying the DPU. Market is expecting DPU to fall in this invit…and even the venerable Indigrid is not in its usual form these days but in much better shape than PGinvit…all my 2 cents…take it with a pinch of salt

I fully agree on the current scenario and keeping an eye on its movement. 11.3 per cent yield on a Triple AAA government rated instrument is too tempting to ignore. My view is that Market is not liking the idea of Power Grid Invit dipping into reserves last quarter for maintaining DPU guidance and their future commentary is also currently not encouraging.

I stil may get tempted to enter below 100 mark as 12 percent yield and long runaway will give enough margiin of safety and a postive management commentary can trigger rally to 140 levels.

Pointing it out here, that the current 11.3 percent yield might not sustain beyond FY 24.

In their Aug 7 concal, the PGINVIT management did say that maintaining INR 12 per share distribution for the year will not be possible for next year (32:30 PGInvIT).

Disclosure: invested, tracking closely as I invested mainly for the passive income

Amit…PGInvit is nose diving every day and at almost 12% yield (pre-tax) now. Market is of course factoring in a reduction in DPU in the future but if the slide takes it ugly levels of 80s/90s, what one can gain by yield is lost in capital loss…what is your take?

Kalyan- I added some more of IRB invit in my HUF account at 70.30 on Friday. Regarding PGInvit, I have same apprehension on capital loss in short term and may add once price stabalizes

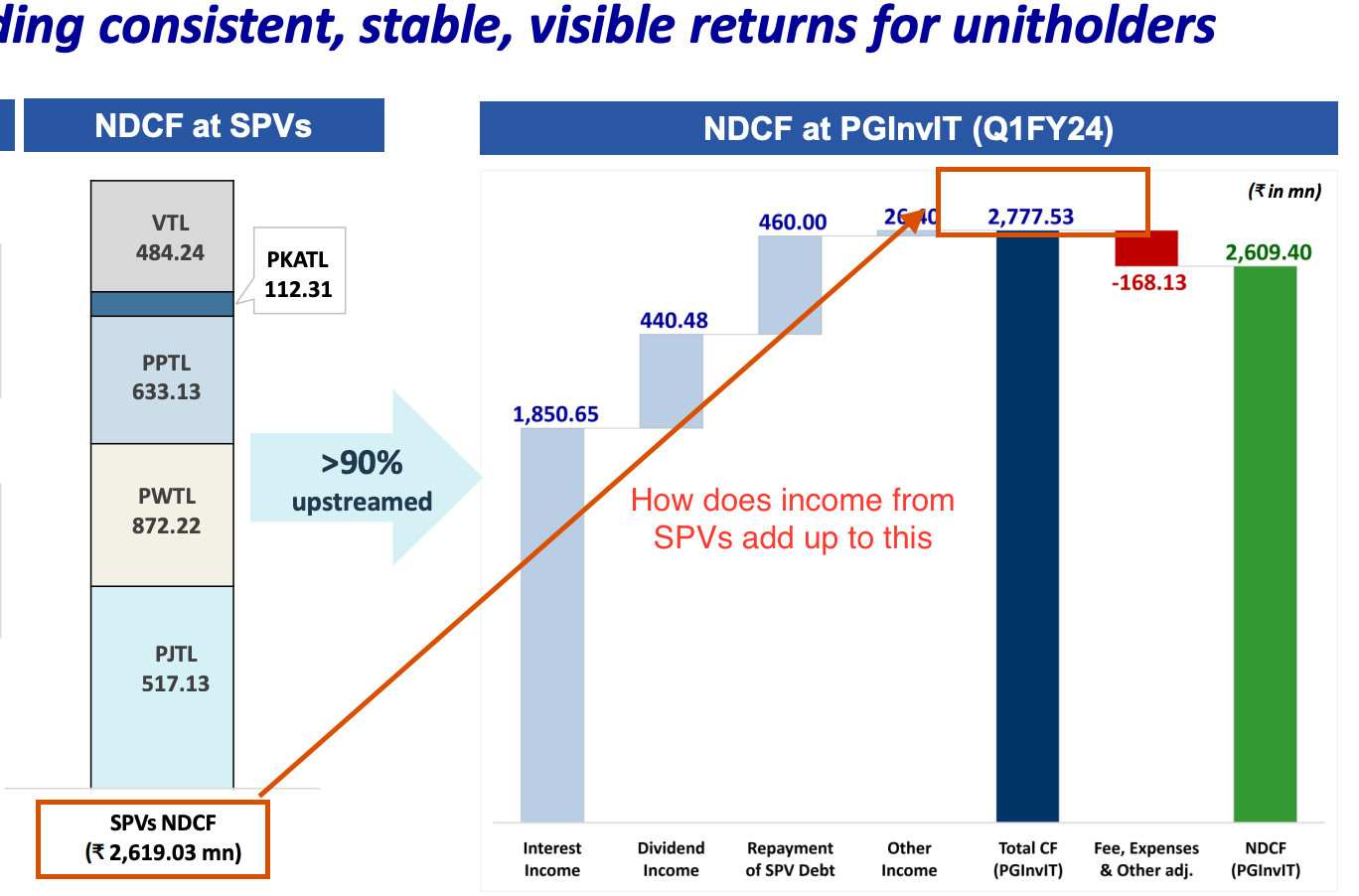

I tried calculating dividend per share from cash flow of SPVs published in their report. Next 10 year yield without dipping into reserves is on average 5.62% (SPV giving 90% CF) - 7.02% (SPV giving 100% CF).

Where as 10 year bond yield is around 7.2%, but we can expect some acquisition to happen in next 10 years.

Let me know if I am making any mistake.