U cant compare the two….

hdfc life is into life insurance and icici lombard is in general insurance…

both have different dynamics…difference TAM…different size of opportunity…

U cant compare the two….

hdfc life is into life insurance and icici lombard is in general insurance…

both have different dynamics…difference TAM…different size of opportunity…

Sure will keep in mind. Thanks!!

Missed the merger news.

Agreed on watchlist point.

Can you share the link to the article about LIC loosing to private players.

Personally , I also believe private players be it banks , life insurance , AMCs are better.

Thanks!!

Hello,

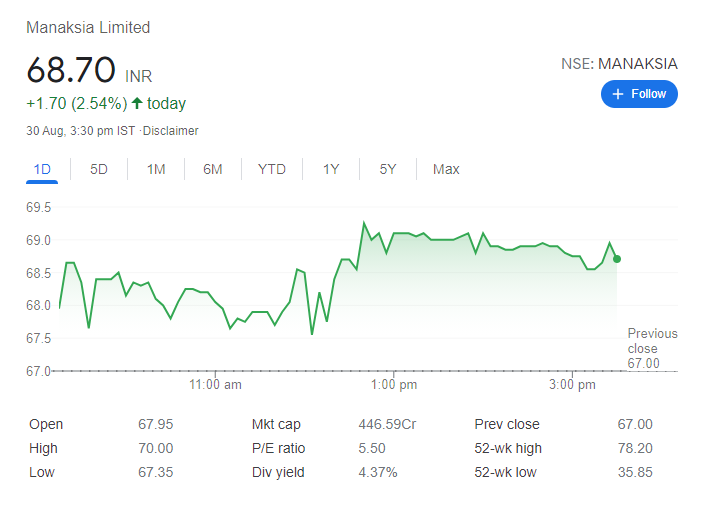

May I know your opinion on Manaksia Industries.

FINANCIALS:

Market Capitalization:440 crores. TTM profit:78 crores. P/E:5.57

Main reason why i am interested in this stock is that the latest annual report released 4 days back discloses mutual fund investments of around 400 crores.On top of that the working capital of 263 crores.As a result it is now trading at a deep discount to MF investments +WC.Also all comparable stocks like NILE,Ram Ratna Wires,Precision wires are also at higher P/E multiples.

Furthermore,the company has paid 117 percent of its profits last year and 33 percent of its profit this year as dividend.

The shareholding has also gone up in the past year by 2 percent to close to 75 percent.

The main point that may be affecting it’s share price could be it’s nigerian subdiary,but they have generated cash and invested in mutual funds in india.Not only that they are paying very good dividends and also buying shares from the open market.Promoter holding is 75 percent.

The credit rating of the 3 group companies are A,A,BB .I just wanted to point this company out because not many are discussing this company,but are interested in it’s group companies like Manaksia steel.

These guys have never diluted their equity either.

BUSINESS DETAILS:

Sponge iron and value added steel products comprising Cold Rolled Sheets used in interior and exterior panels of automobiles, buses and commercial vehicles, Galvanised Corrugated Sheets used in the rural housing sector and factory buildings and Galvanised Plain Sheets, used in the manufacture of containers and water tanks and Colour Coated (Pre-painted) Coils and Sheets for sale to construction, housing, consumer durable and other industries.

Aluminium rolled products in coil and sheet form used in closures, bus bodies, flooring and general engineering

purposes and Colour Coated (Pre-painted) Coils and Sheets for manufacture of heat exchanger fins for air conditioners

in the HVAC sector and Aluminium alloy ingots used in the steel and automotive industry.

Roll on Pilfer Proof (ROPP) Closures for liquor and pharmaceutical sectors, Crown Closures for beer and carbonated

soft drink sectors.

Kraft, Brown and Fluting paper

Kindly share your thoughts.

Disclosure:Invested.

Aniesh,

One of the best portfolio and amazing entry prices…

Iam invested in most of these companies from your portfolio and bought Laxmi organic on listing day… Excellent results and growth potential

Aniesh, you have a wonderful portfolio right here. Great job in selecting such quality stocks. I suggest you look into Orient Electric from the consumer durables segment. The reason being, due to Covid the pent up demand on consumer durables have increased and it will reflect in the upcoming quarters of the company/sector resulting in better topline and bottomline performance. Also it would be great to have your views on it too.

Disc: Invested

Could you please mention/share the scrip name of the stock

Yes.That is the one.

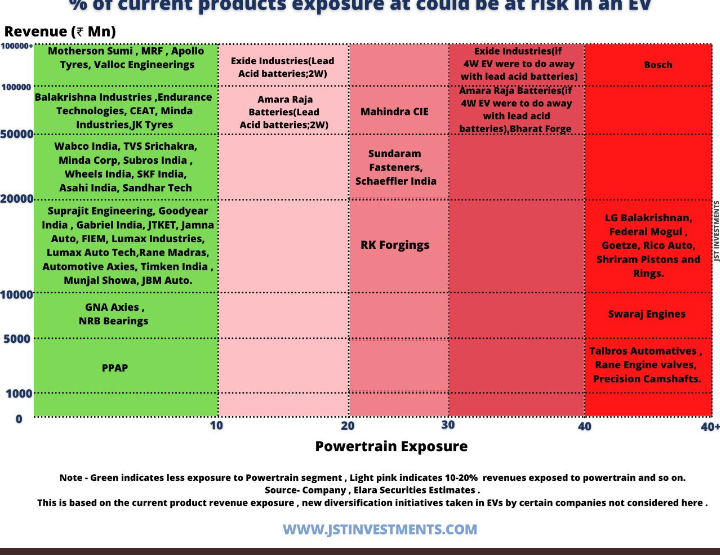

Stocks marked red are more prone to E - Vehicle disruption.keep a track…

Holding : Endurance technology and Sona Comstar in that space

Clean Science and Technology Limited (CSTL) foray into Hindered Amine Light Stabilizers (HALS) series. HALS series comprises a range of products which find application in diverse end industries including polymerization inhibitor, water treatment, paint industry, coatings industry etc. The estimated market size for HALS series globally is approximately USD 1 billion. CSTL would be the first company to develop HALS series in India.

Invested .

Recent addition :

Core PF : Whirlpool, Safari, Aavas Finance , Dalmia Cement , Endurance technology

IPO/Demerger : Glenmark Life , Tatva , Clean science , Tips Industries , MTAR ,CAMS , Easytrip

Positive on Consumption, Tech, Real estate , Environment related stocks for next few years …

Quality financials Will keep performing…

Environment related stocks as in ?

Gas , Water purification , E-vehicles, Clean energy, Green Chemistry, Ethanol etc

Gujarat Gas, Ion Exchange, IEX (Energy Exchange Platform), Dwarikesh are some of the companies I am invested from the above stock type

Hope you are keeping an eye on AU bank, some top level management attrition issues

Bought Strides Pharma for its upcoming Demerger of Stelis bio …

Usually I buy after listing but seeing the Demerger performance of recently listed Meghmani finechem , thought it’s better to buy before listing as market is well aware of stelis potential… i won’t be surprised if continuous upper circuit happens here as well…

Board approved listing on feb2021 hopefully in next 5-6 months it will happen…

Not bullish on Generic Pharma space but strides corrected well , so got a better entry point and margin of safety… If generic does well that will be added bonus…

Demerger watchlist :

Is there confirmation from Strides Management on Stelis demerger or its IPO? They had told they will demerge in Feb 2021 as you rightly pointed out but as per their recent concall they are unsure of demerger or ipo of stelis.

I agree with your point on current valuations of strides they give you really good margin of safety provided your thesis on demerger on stelis is intact as per management.

Regarding Meghmani Finchem since i have tracked it closely i will like to point out to some differentiation between them

Meghmani shareholding before demerger

Disc: tracking & Invested in Strides

“There is significant holding of institution in it they will most likely not keep stelis as it will be smaller then their minimum portfolio size these might give you some opportunity to enter in stelis because of selling pressure”

Will institutions really sell Stelis if it lists?From the looks of it Stelis could be valued at a few thousand crore.