Hello all,

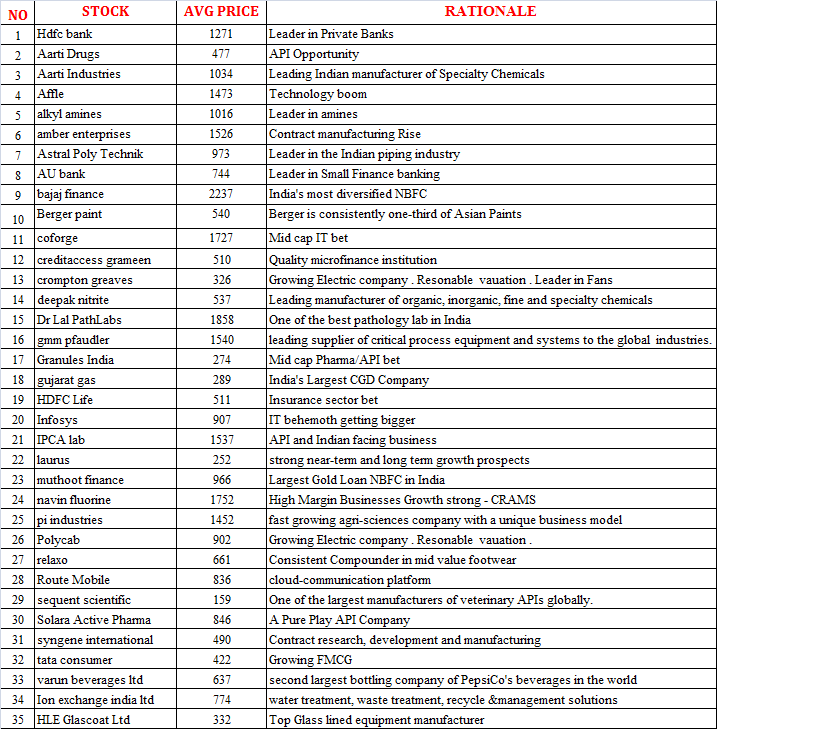

I am sharing my portfolio along with my rationale . 2 years back I got into Stock market. I identified all these shares by reading articles, expert opinions and little bit of research from my part. I would love to get your opinion and suggestions. Please point out my mistakes as well.

The goal is to generate 20% compounded returns over the long term. (20-25 years). At present my portfolio returns stands 65 % in 2 yrs.

Thanks Sir for your suggestion

I bought coforge in March market fall as it’s a consistent performer in las few years … n averaged it in recent fall…

Although I’m not still 100% convinced abt the bet …

Midcap IT Shares ran up very much in last 8-9 months.

N I shouldn’t over diversify my portfolio… N I’m confused among Mindtree, Mphasis, LTTS Or persistent system . Which will be good bet for long

Please guide u and other senior members Opinion . Will be helpful.

The first thing that comes to mind is the number of companies in your portfolio. It’s a herculean task to keep tabs on 35 businesses. Few questions:

What is the weightage (in %age) of each company in the portfolio? Are there good number of companies with <1% allocation?

How are you planning to follow up on business prospects and key structural changes in the long run?

Why Berger paints, and not Asian paints? Do you believe it will take away market share from Asian Paints? Your rationale on the same

I usually find very difficult to follow up on more than 15 companies. It takes a toll on me.

Trimming the number of companies would help in focusing on few high conviction bets IMHO.

I am just telling you to research a bit more about LTTS, Persistent and Mindtree. Every company has their own pros and cons. For example single client exposure for Mindtree is very high, otherwise everything is okay. LTTS is a niche Enterprise R&D company. Persistent is transitioning from product only to include services as well. Declining revenue from DXC portifolio for Mphasis has been worrying, but they are able to win some big orders to compensate for that. Its simple, if you dont understand the business, just don’t buy that. It is not a recommendation, but my bet is on LTTS for long term to compound at 15-20%.

Dear Sir,

IMHO stock selection process is critical in building a Portfolio.

Some of the crieteria I use are

• Do we understand their business?.

• How is the quality of the business?

• How is the Management? Are there any Governance issues?

• Does it have a long run way for Growth?

• What is the debt level in the Company?

• Are there any share pdege by Promoters?

• Is the valuation fair? Etc.

If verything is fine, then the stock may be short-listed. If everything is fine except that the valuation is high, the stock may be included it in your watch List.

You have not mentioned about your stock selection crieteria. I presume you also follow a similar good process for selecting your stocks. May be it is a good idea to evaluate each stock based on your selection process.

Wish you good luck in your investment journey

Thank you. Yes all these criteria i see .

Most of the stocks in my portfolio is from pharmaceutical, speciality chemicals, IT , consumer , Financials .

These is where I believe in next 20 years wealth will be created

I avoid Infra , Alcohol/ Cigarettes, metal , Auto, Real estate due to its cyclical nature…

I understand I might be missing some great companies here .

Indeed, as I could understand idea is to keep growing direct business and gradually taper off DXC business. New wins in direct business are encouraging. Also, recent news that DXC would be taken over by Atos. With Atos having significant offshore India presence, what do you think is future of Mphasis’s DXC business. Do you see it as a short term threat? Also Blackstone getting out and new PE investor coming in - how do you see the valuation play. With a PE of around 22, it is significantly cheaper than other comparable midcap IT but there are reasons around it. Your thought?

I believe the minimum revenue visibility for Mphasis from DXC is there until Sep 2021. Going by management commentary I don’t think they are going after DXC after that, and that was the reason that they worked so hard to win large deals. Also, I kind of got the sense from concalls that the revenue from banking and capital markets (BCM) will be more when the interest rates are low. And most probably they will remain low for the next 6-12 months. This is helping them in their BCM vertical growth. What after that? Finally, no one knows when Blackstone will exit. But their initial investment is already more than 3x. The exit of Blackstone is a looming risk. If Blackstone exits, then they can’t mine other Blackstone companies like they would have when they were an investor. The valuation at which they exit will be keenly monitored, if and when they exit. We all saw what happened with GMM Pfaudler. I think the market is keeping that in mind and valuing low compared to peers. But if the large deal win momentum continues, then rerating may happen. There may be things which I don’t know.

Agree, however as per some reports I read, other big PE are after Mphasis so I would think that their companies would open up once blackstone exit? maybe there could be some exit clause on new business as any new buyer would know these risks if we as small retail investors so clearly can see them. Also, once a blackstone company would remain a blackstone reputation and hence can keep mining some existing companies on merit, reference and goodwill. Agree all this is a fundamental speculation so many things we would not know and hence the comparative lower valuation. Thanks.

Also, I agree on your comments on LTTS and it is one of my largest holding in tech companies bucket. What are your thoughts on Oracle Financial services? It is valued at 17 PE with a Oracle pedigree, focus on digital banking/cloud/insurance and a Product company. I understand market values growth but is that all it values? What about owning a Product and IP, that too not just any product but one of the best in BFSI? Thanks

Disc: Hold LTTS, Oracle Finance and Mphasis as mentioned above so views will be biased. Not a buy/sell recommendation

It’s a good portfolio. I won’t say much since the fact that you stick to quality says a lot in itself. The number of companies is always up to you but over time you’d want to get a more concentrated portfolio of say a dozen or more companies. But that’s entirely up to you. All the best!

Stocks you can consider upon correction: HUL, Asian Paints, L&T, and Pidilite.

Yes Sir initially I had around 50-55 companies. I bought it down to 35 .

This the reason y I started a topic on valuepickr . Where I can get lot of suggestions n learn things…

Noted . Al company u suggested are of high quality TY

Hi Aniesh

80% stocks are great stock but couple of stocks have management integrity issue. Example Varun beverage got Tax fraud dispute and paid huge bill as penalty. Generally you can spin off company which have lagging management integrity and increase allocation.

If I am in your position I will increase AU small finance and spin off credit access.

Spin off HLE glasscoat with addition allocation GMM.

Spin off varun beverage and add more allocation tata consumer.

PI industries proven consistent compounder but alkyl amines,Deepak nitrate are now running with maximum OPM and peak utilization. Small disappointed will make market jitter on those company valuation.

Allocation and amount of money invested matter a lot in generating good return long run . If we have conviction then we should back maximum amount of that stock with high allocation. We cant have many socks with 1 or 2% allocation instead spin off similar sector stock and ride with winners.

Just my thoughts.

agree we should always remain with winners. I got ur point of Spin off . Ty

Being a person from law field my knowledge in area of Finance is very limited. Suggestions and opinions of experienced n knowledgeable is very helpful… TY for support

I have few small caps stocks as well… Invested small quantity in total less than 5% of my portfolio

KEI - Amongst India’s top three wire and cable manufacturers

Sumitomo- Growing agrochemical MNC

Nippon AMC - Amongst Top 5 AMC

JB Chemical- Indian market facing pharmaceutical

IOL Chemical- leading bulk drugs company

Apollo Tricoat - India’s leading steel pipe and tube manufacturer.

I found these small cap stocks have good fundamentals and credible management . So during the March 2020 fall I bought few f .

Most i booked profit. Few above mentioned i still hold

Hi Aniesh…I’m also building my own portfolio and the problem I’m facing is how do we continuously invest in so many stocks…I was thinking of doing a monthly SIP but due to limited funds availability it looks difficult…can you share what strategy are you using.

I would also request other senior members for their guidance in this.

I make sure 25% of my salary is kept as saving every month n hold the cash

I buy stocks wen market fall, I understand timing the market is is not easy. But I’ve seen atleast in every 2 months there comes 3-4 days where market remains weak . That’s where I find opportunities…has to keep patience n wait

N secondarily few stocks falls due to some negative news stock is down 10-12% that time i buy .

I invest mostly in in IT , Pharma , speciality chemicals, consumer business and Financials. Avoid cyclic I am inspired by coffee can investing strategy . Buy quality n keep holding for long