Hi @Donald

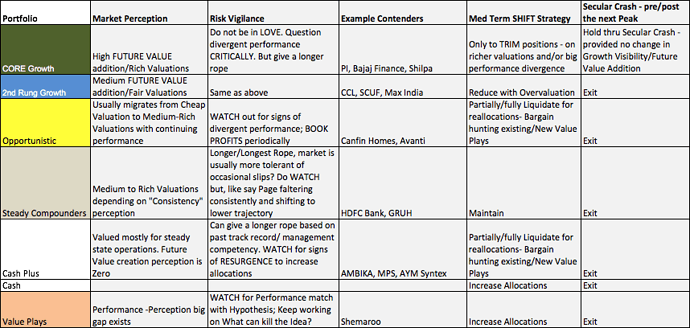

This wonderful thread provided a lot of good learnings/insights on the portfolio strategy, categorizing bets (table from an earlier post in this thread), restructuring process, capital allocation, building cash positions, and following exit-triggers.

This thread gained huge momentum in the BULL phase of the market (2016 - 2017) and It would be great if you can restart this thread in the BEAR Phase of the market (currently experiencing) with renewed thoughts, strategy, process, and learnings; it will benefit most of us (or atleast beginner like me). Thanks.

Regards,

Vinoth