Excellent perspective on real long term investment. It takes decades of experience to have this clarity of thought. Though I am investing only since last 8 years, long term perspective seems to be working for me. It has helped me avoid low quality companies when I think of 10 years holding perod.

3 Likes

Hi there! I wanted to message you, but mail option seems missing in your profile, can you please mail me? I’d like to discuss something that is relevant to your post, but outside the scope of this forum.

Thanks

Arun

1 Like

Do not share your email/mobile no on public forum. You can simply send it through private message.

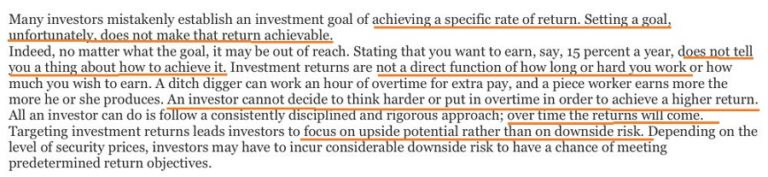

This extract posted by Alpha Ideas (from Seth Klarman’s book on Margin of Safety) talks of the problem with setting goals for investment returns (like a CAGR of 25%)…the leitmotif of this thread (a very high bar at 25%), and of course of many commentators.

If you set goals for investment returns, you will focus only on the upside, not on the downside; end up making mistakes or take for granted hidden extraneous factors that gave you good returns which may not continue (one of which is luck). What an investor can do is to follow a consistently disciplined and rigorous approach. Returns will follow

Ofcourse @phreakv6 cheekily pointed out some time ago that the popularity of threads in VP forum is an indication of the current mood. On that count this thread has dropped off the charts substantially and the one on Midcap stock carnage rose up rapidly ![]()

10 Likes

Last 3-4 months have seen significant corrections in some perceived ‘Quality’ stocks. I myself had and know of a few senior investors who have a major allocation or Core portfolio comprising of these stocks.

For eg: Gruh, Page, Eicher - once perceived to be untouchable leaders in their respective fields have each had a ~ 30% fall within 3-4 months

| Quality Basket 1 | ||||||

|---|---|---|---|---|---|---|

| 15% + Steady Earnings Growth perception with significant fall | ||||||

| 17-Sep-18 | 31-12-18 | Current Price | Var % from 17-Sep-18 | Var % from 31-Dec-18 | ||

| Gruh | 337 | 318 | 243 | -28% | -24% | |

| Page | 32982 | 25239 | 23010 | -30% | -9% | |

| Eicher | 29664 | 23158 | 20300 | -32% | -12% | |

| Maruti | 9418* | 7465 | 7492 | -20% | 0% | * price on 28-8-18 |

In contrast, there have been some others having similar perception who have managed to hold on to price levels despite some headwinds

| Quality Basket 2 | |||||

|---|---|---|---|---|---|

| 15% + Steady Earnings Growth perception without fall in price / recovery from fall | |||||

| 17-Sep-18 | 31-12-18 | Current Price | Var % from 17 Sep 18 | Var % from 31 Dec 18 | |

| Bajaj Fin | 2605 | 2645 | 2525 | -3% | -5% |

| Avenue | 1525 | 1607 | 1583 | 4% | -1% |

| HDFC Bank | 1992 | 2122 | 2109 | 6% | -1% |

| Kotak | 1229 | 1255 | 1229 | 0% | -2% |

The game seems to keep becoming narrower with more names going out of the Quality list as compared to the new entrants.

The message seems to be that one has to be mindful of the chages in ‘perception of growth’

Looking back and trying to recount learnings, in case of Page and Eicher it seemed the signs of slowdown in sales volume growth were visible many months before the fall. Gruh-Bandhan merger was a bit of surprise to many, which I would classify as an uncontrollable risk associated with any investment.

Looking ahead, one must keep eyes open for similar trends for eg: Avenue - faster than expected reduction in SSG? Increased regulation in pricing - HDFC AMC, fee income of Banks?.

20 Likes

Hi Donald,

Hope you are doing good.

I was eagerly looking forward for a write up on 2019 from your end.

Hope to see you soon here.

6 Likes

Hi @Donald

This wonderful thread provided a lot of good learnings/insights on the portfolio strategy, categorizing bets (table from an earlier post in this thread), restructuring process, capital allocation, building cash positions, and following exit-triggers.

This thread gained huge momentum in the BULL phase of the market (2016 - 2017) and It would be great if you can restart this thread in the BEAR Phase of the market (currently experiencing) with renewed thoughts, strategy, process, and learnings; it will benefit most of us (or atleast beginner like me). Thanks.

Regards,

Vinoth

2 Likes

Thanks @vinoths - for reminding me of my duty to share more and add value to this thread in my own way and others can add to it, please

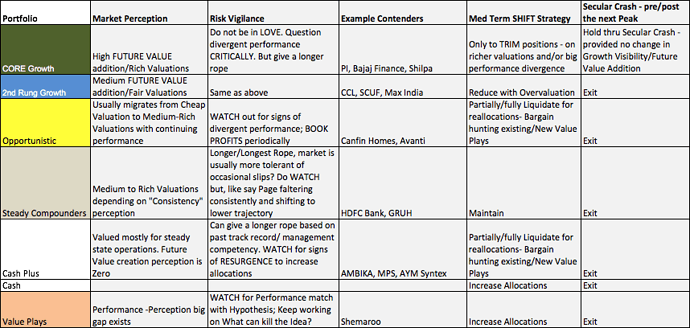

The picture above is a good place to start - as it is illustrative. Thanks Vinoth for drawing attention to it again. (I will locate the excel and do structural update when I find the time - will need some time as I have moved systems in between). For now a quick and dirty update is certainly possible.

Portfolio Structure - An additional component has come in since 2017/18 in my process - that one could consciously maintain/carry a couple of contrarian bets in the Portfolio. This has come in as I realised form 2016 onwards - that Reversal to the Mean - is a LAW. Sooner or later most portfolio contenders need to go out of Portfolio after 4-5-6-7 years of heady growth. My personal examples of prominent top-of-mind exits Astral - 4 years (was proven wrong, its still going strong), Mayur (5), Ajanta Pharma (5) Alembic (5) - were proven right. PI Industries is the only one that has consistently found a place and survived a decade plus; A Bajaj Finance may get there - we have to see.

Similarly this is true the other way round trip. An essentially good business (we need to be careful to check on Industry tailwinds, competitive position stable or growing) will also follow the reversal to the mean law and come back into reckoning. So we need to keep tracking our past winners. So Ajanta Pharma and Alembic are back in reckoning as possible consistent growers/performers going forwards. As a vehicle one could be more comfortable with Alembic over Ajanta - and the reasons could be evident from the results first of past many quarters, Concalls that provided glimpses into the promising differentiated future, latest Alembic Pharma Management Q&A Feb 2020 providing further insights. One should be clearer about the Alembic picture, how well differentiated a business it is today, and how the ODDS might be stacked in its favour of doing well in the medium term; Ajanta Pharma could too - but perhaps one doesn’t have that strong insights onto Ajanta business as of today and medium term; time for another Ajanta Pharma Management Q&A?. We should actually explore possibilities of doing it online - if Ajanta Management agrees to it. Will explore that option!

So where do contrarian bets fit in?

I realised that for any portfolio to be structured well for an all-weather performance, it should be designed in such a way that at least 2-3 out of 4 parts must always be ON and performing. Think I had started a thread on all-weather portfolio, somewhere - may be these two could be merged - if it makes sense - will have a look, again.

It’s like nothing was happening on the PI counter for close to 2 years? Hovering between 800-1000 when growth was flat. But one could be sanguine and holding through with high allocations all through that period - knowing a few important things about the business - most importantly - starting 2 new factories dedicated to independent single molecules at an investment of 300 Cr. With asset turns of 2.5 and above this easily meant 600-750 Cr additional revenue stream coming on a year to max 1.5 years down the line. Besides structural changes in the industry indicated that PI CRAMs business would get more and more traction in the next 2-3-5 years.

At any point of time - its good to include one or two Contra bets that have high visibility of kicking in higher trajectory of earnings a year or two down the line. One should be careful to define Contra bets in a way that these are NOT Value traps. Industry tailwinds are stable or getting better, Competitive Position is stable or getting better; just that earnings are going through a consolidation. There are always candidates for these in most market conditions (if you have a decent investible universe pre-identified) (except extreme uncertain conditions like now, better to wait for more clarity to emerge here to define ones Contra bets in these conditions). The good thing about Contra bets (in normal times) is that Market attention completely shifts away form them, Valuations become extremely reasonable (or extremely attractive like now in bear markets) with high-margin of safety, and the best part - one can allocate as much as one wants (read Capital Allocation Framework high conviction x high undervaluation) - without impacting prices.

Rest of the Portfolio structure remains same as before:

Core bets examples - Bajaj Finance and PI industries still belong in that category. Shilpa probably no more qualifies to be there there; Corporate Actions and Performance Record on Quality/US FDA front main reasons - despite recent performance uptick.

I define Core bets - as ONLY those - where we have significant insights and confidence - that the business is a) most likely to survive - has the financial strength and the leadership to steer it past industry/business challenges b) through/past the cyclical phase will only get stronger as it gains more market share from space vacated by others c) we will have the CONVICTION and the guts to average down - even if the price halves from current levels. (also as shared in the Market Meltdown Actionables thread)

2nd Rung growth - Absolutely we should be out of these - as conviction might not be strong, and we might NOT be able to average down if prices become 30-40% cheaper

Opportunistic Bets - This is NOT the time to be adventurous; This is the time to ensure Survival first, as shared more in Market Meltdown thread by multiple senior investors; time to pay heed to that; Acknowledge we dont know - as exemplified and re-enforced by Charlie Mungers latest interview advising just that.

Steady Compounders - These are structurally important to ALWAYS have in the Portfolio. HDFC Bank continues to remain a possible strong contender there; GRUH post the Bandhan Merger is OUT for obvious reasons; Bandhan bank I would categorise as a high-growth high-risk model; RIsks might be managed well so-far, but doesn’t mean it isn’t inherently more risky and is not more vulnerable during these very tough times, and tougher times ahead?; Scaling up will not be that easy either on Corporate Banking side (more risks a la RBL, compounded more by geographic presence limitations) or Retail Banking (too many similar sized players). Hoping to see more value-additive posts on Bandhan Bank soon from ex-bankers and others in the Financials industry in Team VP (please).

Cash Plus - These times indicate CASH is king; so CASH plus all moved to Cash

Value Plays - NOT the time for these now; As clarity emerges post gradual lift of lock-ups, and we are more aware of the labour disruption mitigations possible, and supply chain mitigations, and all other business-specific micro issues and Management responses to the Opportunities and Challenges before them - This will certainly come into contention. Probably within 6-9 months timeframes - as we have more CLARITY on lockdown impact.

Cash is now around 40% levels in Portfolio; so there is enough ammunition to take advantage of better and better bargains if they become available. Still Invested around 60% in Core Bets (incl. Compounders) only. Alembic Pharma is probably a good addition to Core bets.

Edit1: As mentioned in market meltdown thread, once we had more clarity on the seriousness of what was before us, had no hesitation in booking losses (slightly north of 25% from Dec/Jan peaks) to survive this phase with complete peace of mind, and energy to devote to working hard - at improving processes, get deep domain experts to contribute on VP to solve unsolved puzzles and throw more light on survivability of prospects, engage everyone again in business/industry scuttlebutts, in a bid to identify and position ourselves better for the next set of winners - 2-3 years out from now)

Disc: This Portfolio structure is for educative purposes only. This is NOT a buy/sell recommendation. I may or may not be invested in the stocks mentioned/discussed. My views on the Portfolio structure/components can change suddenly with more insights on a business/industry. I may not be prompt in updating the Portfolio Structure and/or Components

50 Likes

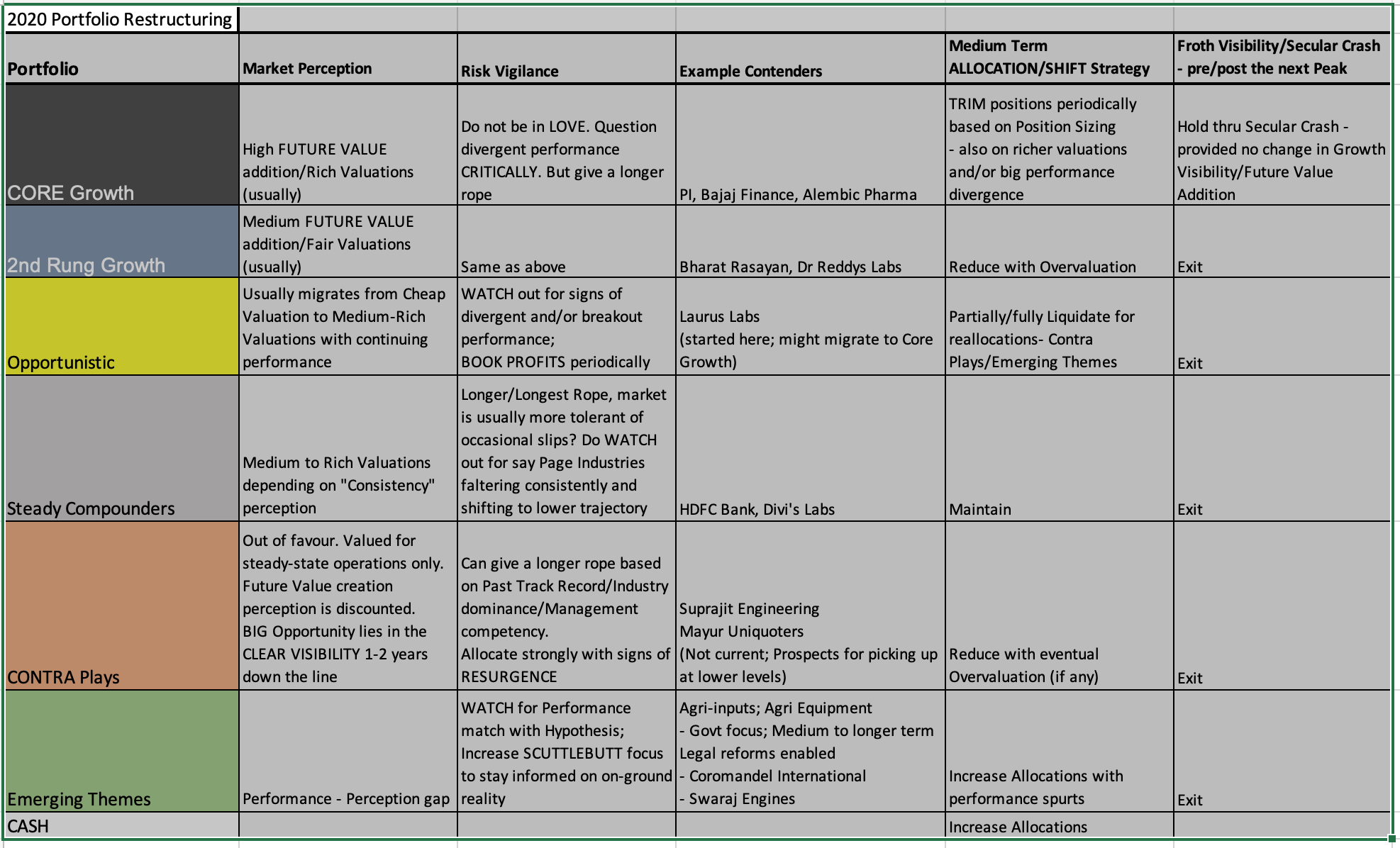

Have been receiving some requests again for a proper update on this portfolio re-structuring thread.

So the above, is an updated summarised table on the same.

Next comes the oft-asked rejoinder, how should we be thinking - given the way markets are behaving currently. There are some signs of clear froth emerging, which many of my senior friends indicate may well get extremely heightened over the next 30 days, and more.

I have found that a well-hedged strategy always works best for me.

a) In March I had moved to 40% CASH levels - that allowed me to stay put in Core bets along with Compounders like HDFC Bank

b) Once there were clear signs of first-order positively affected sectors providing the ONLY visibility, added more of Pharma and Agrichem to move to 25% cash progressively to 15% Cash currently

c) I will be getting back to 25% Cash, and progressively to 40% CASH levels (probably soon)

Having a hedged position - where I do NOT try to maximise the juice - helps me sleep well, all through. Whether the markets produce V-shaped recovery - which it did in select sectors - and was getting more broad-based, to now becoming a Trader’s Mecca - someone like me is CONTENT having participated meaningfully. And if say it goes on to a prolonged bear-market of 1 or 2 years plus after a big build-up and melt-down, I think I will sleep well. I will be more energised to work harder on the next-set of opportunities. I will have ammunition to back me up.

This is the first time in 10+ years of active investing - that I have purposely added trading positions where I found there is high visibility (among my current portfolio bets; none additional). I believe this is a “Traders Market” till the inevitable fall, and felt confident enough to try out a few things - of course under my Mentor Hitesh Patel’s able guidance ![]() . Which means for certain portions of the Portfolio, I am on the look-out to Cash Out progressively as froth builds in them/overall market. Already considering trimming positions in the best-performers (read already frothy, or big position sizes) to allocate more to those moving slower, more consistently (another Comfort Zone breaking/New style training for me)

. Which means for certain portions of the Portfolio, I am on the look-out to Cash Out progressively as froth builds in them/overall market. Already considering trimming positions in the best-performers (read already frothy, or big position sizes) to allocate more to those moving slower, more consistently (another Comfort Zone breaking/New style training for me) ![]() .

.

While I will remain well-hedged for practicality reasons, I do belong to the Camp that thinks this merry-state of affairs has to end sooner than later. The disconnect with real-economy, rising inflation (which is inevitable), hugely widening disparity between haves and have-nots - will prevail over the liquidity-driven (?)/otherwise rally. When that will happen there is no point second guessing. I am happy to leave some juice on the table, again - in tune - with my progressive discomfort, wherever I see frothy valuations. And perhaps in a month or two months - that may well be across the board, given the current momentum.

Another very important aspect I think I should be highlighting - else I will not be doing justice to my role, perhaps.

Market Awareness - Different Phases/Different Strokes (?)

It’s been surprising for me to notice how many years of active investing/reflection it takes, before something very crucial registers strongly in us. Most of my colleagues have proven to be super successful investors over the last 5-10 years - and very interestingly, most with very different styles. But with super-success, there seems to be a price to pay ![]() .

.

We seem to start discounting the fact that our performance record is first a function of the Opportunities that Mr Market offers us, and only then a function of all other things - hard work, investing acumen, temperament and self-knowledge, process discipline, ability to be patient and strike hard when Mr Market offers the opportunity, and so on.

The Deep-Dive-Works-Best Phase

The price inevitably is that we start to think that our style (that worked so beautifully for us) is the ONLY style!! I can certainly confess that by early 2016 (2010 -2015 I had seen only one way up, up and up - from 10x to 20x on many bets to 50x even - witness VP Pubic Portfolio). It was a function of the Opportunity that Mr Market offered primarily between 2010-2013 - you could buy 30% growers with 30% RoE at 5-6x to max 12x earnings. By some strange luck everyone of our so-called strongly differentiated business models we picked was growing at 30-40-50% plus levels. And we could be very very choosy while picking - not many were interested in the markets then (unlike now).

Low-Hanging-Fruits - Anything Works - Phase

And then came 2016-2017 timeframes - where everything was flying. Everybody made money in Markets. You could throw darts and come up with big winners. Lots of lots folks decided to turn full-time Money Managers. Luckily for me Avanti Feeds and Bajaj Finance best performances came to the rescue and shored up the Portfolio beautifully (thanks to high allocations) and I didn’t feel that useless a guy. But I did recognise hey my style, isn’t working that well, there were no cheap bets around anymore - certainly not the strongly differentiated business models I preferred; let alone that - anything that offered a hint of being special or little extra growth was bid up to over 25x earnings or more. High Allocations were NOT possible (Undervaluation simply didn’t exist).

In such environments - when it is too easy to make money - due process gets thrown out of the window - except for the extremely extremely disciplined (and I don’t think I know of one good example among my investor friends ![]() ). In the information over-supply environment, things run up in a week or less, folks advise you to first buy, and then complete your homework. And then another inevitable happens - quality of portfolio bets drop significantly if we keep adding to the tail. This happens even to concentrated portfolios like mine too. Widely diversified portfolios probably suffered more deterioration (because by its nature, one doesn’t have to be too picky).

). In the information over-supply environment, things run up in a week or less, folks advise you to first buy, and then complete your homework. And then another inevitable happens - quality of portfolio bets drop significantly if we keep adding to the tail. This happens even to concentrated portfolios like mine too. Widely diversified portfolios probably suffered more deterioration (because by its nature, one doesn’t have to be too picky).

In such environments, Fear of Missing out (FOMO) takes over - and something like a Shivalik Bi-metal I felt compelled to jump on to the bandwagon - knowing fully well that there indeed was a lot of promise, but my/our homework was incomplete (being based primarily on Mgmt. version of things sans any meaningful market/industry scuttlebutt).

Only Operating-Leverage Works Phase

We all know what happened subsequently in 2018 and most of 2019. Small and Midcaps were hammered out of shape. What helped the Portfolio was having a few well-performing large Caps like Bajaj Finance, HDFC Bank or a large mid-cap like PI industries, all with large allocations.

But even in the 2018-2019 environment there were friends who made tons of money ![]() . These were the guys focused solely on Operating Leverage plays. Nothing was cheaply available, right? So the only thing that works consistently in such an environment is business out-performance. They were smart enough to figure this out and would only bet where growth visibility was very good, Operating leverage at play evidence was almost a no-brainer (Rs 1 of incremental sales would clearly land Rs 2 or Rs 3 of incremental EBITDA), and this fore-knowledge/anticipation of enhanced earnings curve was no-doubt bolstered with hard scuttlebutt work, and that worked fabulously! They merrily hopped around from one to the next - once the curve seemed to flatten.

. These were the guys focused solely on Operating Leverage plays. Nothing was cheaply available, right? So the only thing that works consistently in such an environment is business out-performance. They were smart enough to figure this out and would only bet where growth visibility was very good, Operating leverage at play evidence was almost a no-brainer (Rs 1 of incremental sales would clearly land Rs 2 or Rs 3 of incremental EBITDA), and this fore-knowledge/anticipation of enhanced earnings curve was no-doubt bolstered with hard scuttlebutt work, and that worked fabulously! They merrily hopped around from one to the next - once the curve seemed to flatten.

Moral of the story?

-

Even these guys started thinking/saying - Yes - Operating Leverage is the ONLY game in town

While there is some grain of truth in the statement that Operating Leverage focus is great and a MUST-ADD in everyones investing toolkit (irrespective of style), there also comes a time when Operating Leverage doesn’t work anymore - witness March 2020 and thereafter, or the early stages of any bear market, which may again come on us sooner than later, inevitably. That is the time our Deep-Dive VP style works best (we have all the time to keep dissecting, be very very choosy, keep allocating more as higher conviction builds up on those that execute well to stand out from the rest - allowing us to separate the wheat from the chaff). I know some of us are waiting eagerly for that eventuality

While there is some grain of truth in the statement that Operating Leverage focus is great and a MUST-ADD in everyones investing toolkit (irrespective of style), there also comes a time when Operating Leverage doesn’t work anymore - witness March 2020 and thereafter, or the early stages of any bear market, which may again come on us sooner than later, inevitably. That is the time our Deep-Dive VP style works best (we have all the time to keep dissecting, be very very choosy, keep allocating more as higher conviction builds up on those that execute well to stand out from the rest - allowing us to separate the wheat from the chaff). I know some of us are waiting eagerly for that eventuality  .

. -

While everyone MUST stay true to what works best for them (their own personal style that proves highly successful for them) everyone MUST learn to add complimentary styles. I picked up on the OPPORTUNISTIC bets style from Ayush and Hitesh (insisting all the while that my Opportunistic bets had to be a smaller subset of theirs - only those with the promise/ability to migrate to core/2nd rung bets passed muster). Now I am picking up the focus on OPERATING LEVERAGE at play (again with the insistence that they should belong to Core or second rung growth quality transition). I have also added CONTRA style (1 to 1.5 years strong visibility) since 2016 as mentioned earlier, since I find that allows me to allocate heavily to out-of-favour businesses with high margin of safety. A couple of bets there usually suffices for me.

-

All of us can learn from highly successful folks around us.

Be adamant enough to stick to our Core styles (and keep refining/strengthening that success plank) but also be flexible to experiment/add a little bit of other highly successful styles (we see around us) to the mix slowly, but surely. Actively seek out folks exhibiting success with styles complimentary to ours. Above all start becoming AWARE that there are DIFFERENT phases of the Market - where different mixes works. And what is working very well now, will inevitably change. I am convinced NO one style by itself, can do justice to the eternal quest for the all-weather/all-conditions, well-structured Portfolio.

Can we be better prepared?

I am sure we can. Think we need to PLUG this hole in VP for better Market-Phase-Awareness focus. That will help us all become more well-rounded investors - whatever be the level of our current Investing maturity.

PS: Usually I need to add only 2 bets a year to the Portfolio as a couple of bets inevitably mean-revert. This year I was lucky (due in part to March excesses, and due to excellent colleagues supporting to educate quickly) to add 4 seemingly excellent mid to long term prospects - Alembic Pharma, Bharat Rasayan, Laurus Labs, and Dr Reddy’s - subject to execution track/conviction build-up).

Most of the Credit goes to my super colleagues. Again goes to illustrate - make it a point to hear out our colleagues with strong conviction. Make it a point to work with folks smarter than us. Inevitably, we get smarter!!

Disc: This Portfolio structure is for educative purposes only. This is NOT a buy/sell recommendation. I may or may not be invested in all the stocks mentioned/discussed. My views on the Portfolio structure/components can change suddenly with more insights on the business/industry/Market Phase. I may not be prompt in updating the Portfolio Structure and/or Components.

149 Likes

Hi Donald,very thoughtful as usual. In my decades of investing experience, I have come to the view that mastering even one of the categories is generally enough for a non professional investor and the rest can be considered outside the circle of competence. Yes you’ll let a lot of opportunities pass by but there’s no one saying “swing you bum” as Buffett says. Personally if you get one of the categories right (and that itself is a tall order) you should be set although returns will be lumpy. So just pick one which suits your personality, where you have an edge and roll with it. Thoughts?

5 Likes

Interesting, and thanks for sharing your thoughts in details. I have question, if you can answer would be good to know - I see that you and infact many senior investors follow this core and satellite approach of investing. As you mentioned, it seems 60% is your core portfolio which you did not cash out in crash and 40% you used for momentum picks (the ones requiring deep dives etc.). Some questions which comes to mind which will help in understanding the concept and strategy more, would be great to have your thoughts -

- So, do you feel the 60% defines you more as an investor or the 40%?

- Have most of the stocks which are part of the esteemed 60% club followed the same lifecycle of first becoming a 40% momentum pick and then graduating to the 60% bracket. As I see at one place you mentioned that you took only those momentum bets which you felt have the ability of graduating to the core.

OR - The 60% club has more of coffee can picks - the WB buy and hold strategy, Peter Lynch way of identifying stocks of buying what you see and understand (rather than trying hard to understand new areas)

- Over Long term, has the compounding of 60% or the momentum plays of 40% switching from one to another been more rewarding for you?

Thanks again for sharing your experiences. its always good to learn from those who are so passionate about learning and sharing themselves! Best Wishes

8 Likes