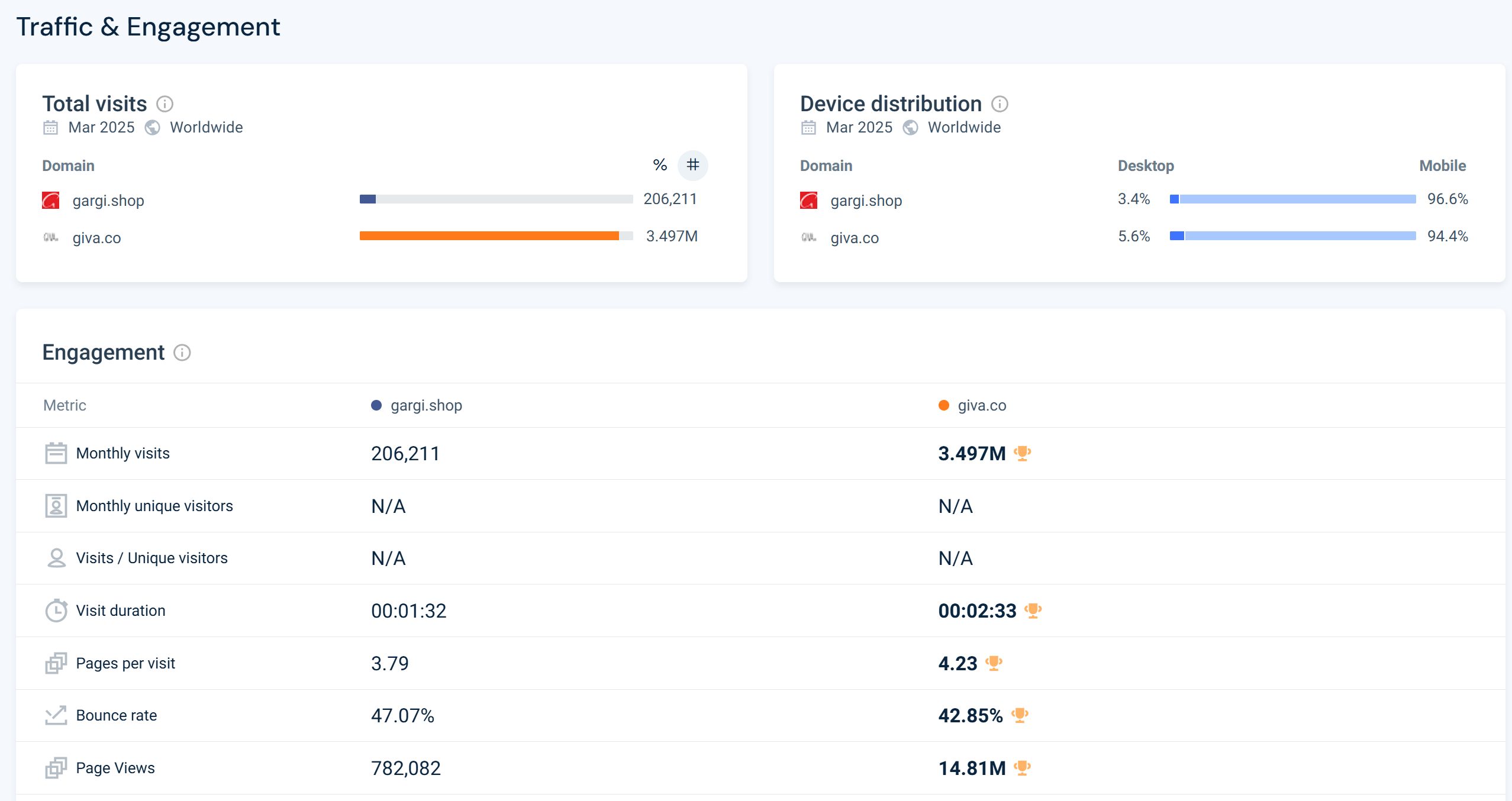

See the traffic on Giva’s website vs Gargi’s

Giva is kiiling Gargi.

Genz generation is going to shop this online for gift or personal use.

Gargi needs to evolve in marketing front. This is not a manufacturing or luxury business. This is fast fashion business and marketing is the pillar of it.

Management needs to focus on marketing.

Need to watch their distribution and marketing strategy.

a reduced OPM margin vis-a-vis last couple of quarters (20% vs 30% range) - may mean that a lower margin product is gaining traction in the market (silver vs diamond - not sure about the margins and this is conjecture)

expected revenue de growth in the next quarter (as it will be compared to the q1 of the last FY wherein the inventory was sold off)

One more things market may not have liked is fund raising , I think they already have 50 cr of cash in balance sheet , what’s the need of raising more funds ?

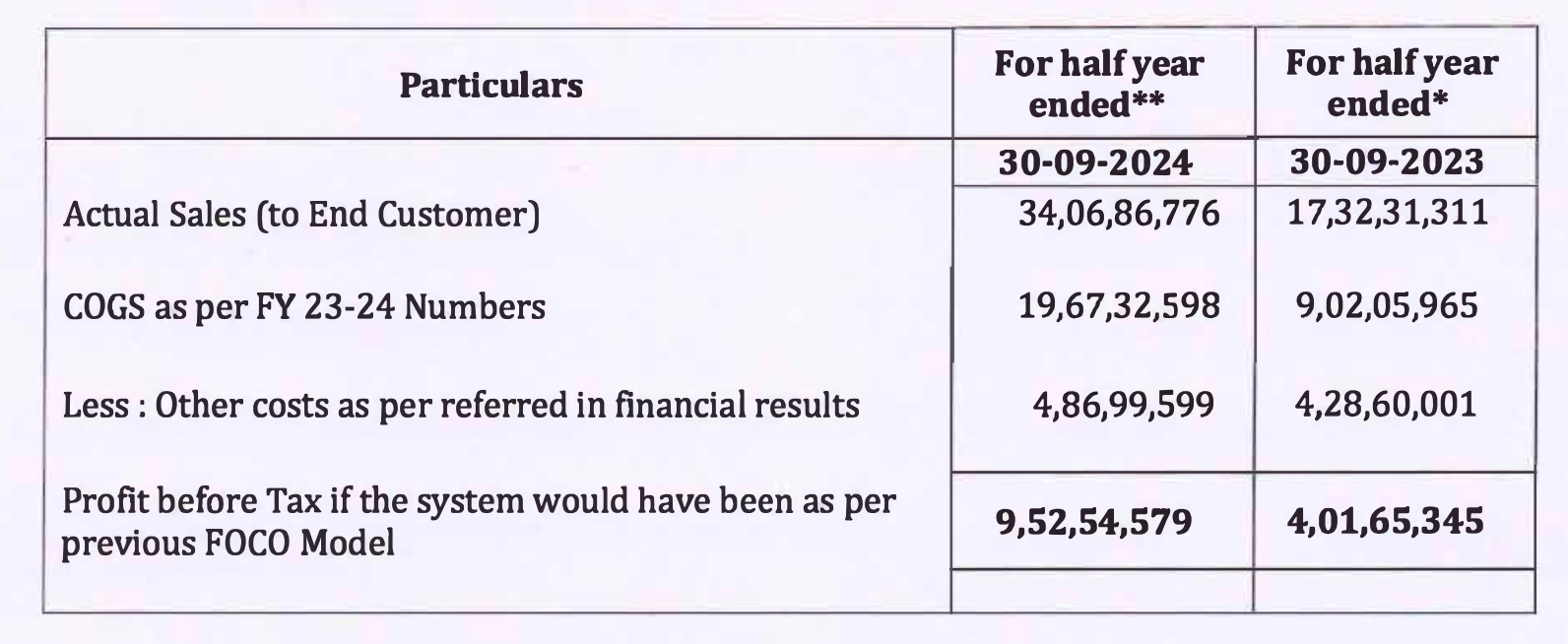

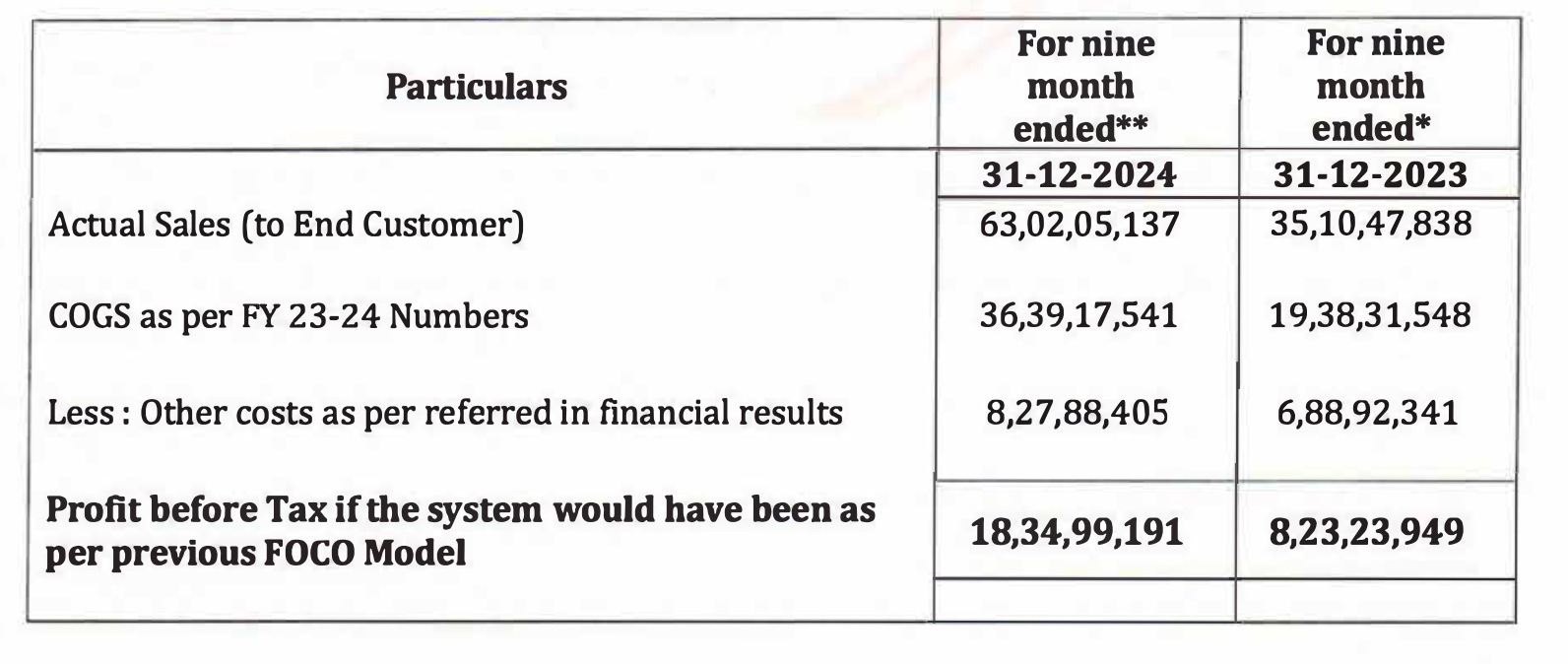

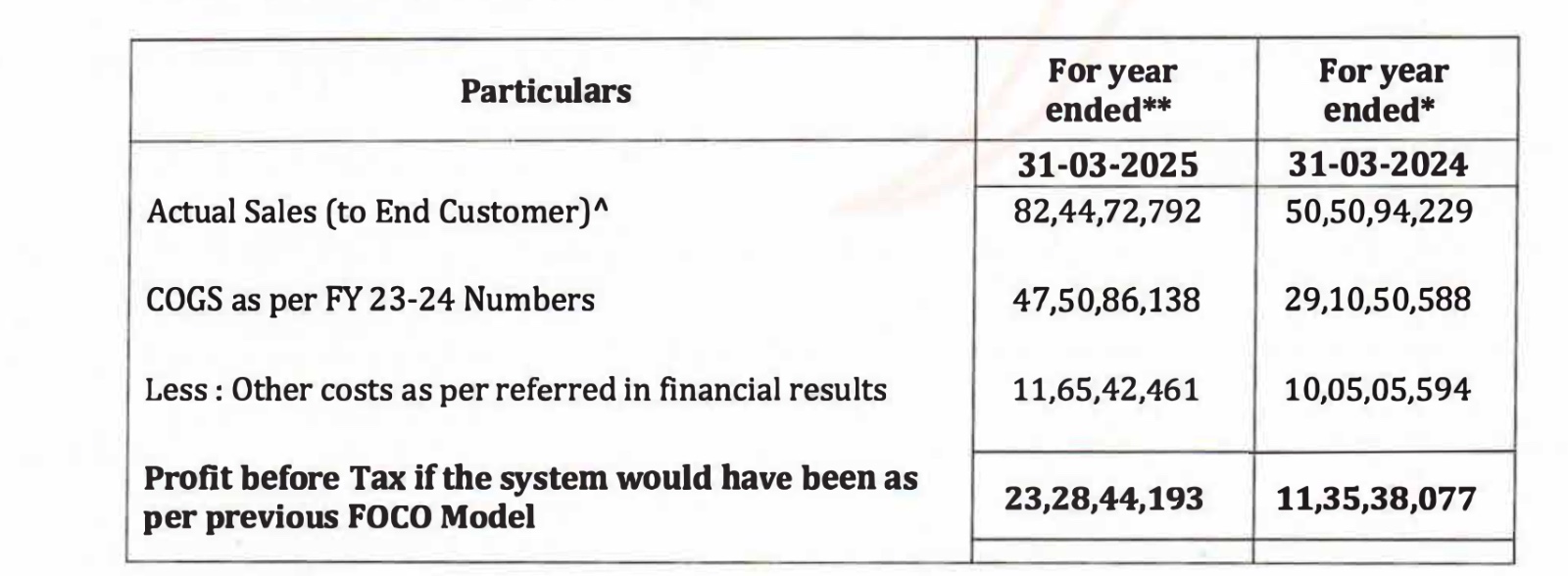

Margin has not dipped much, they have given revenue and profit, in foot notes, for last 4 quarters if they had followed FOCO model. (A tables in every reault document of last 4 quarter)

That shows their revenue (sold to end customer) for fy25 is 82cr. Also if you compare the marging from q3, its just about 1% down

Sales surely is down but thats the seasonality of business

I recently shared a few jewellery brands with a friend to gather consumer-level feedback. Here’s a summary of her insights:

GIVA stood out for both product quality and design appeal, especially when compared to Gargii, which she found less compelling in both aspects.

I also shared Palmonas, a relatively new brand co-founded by actress Shraddha Kapoor. Despite its celebrity backing and a competitive price range (₹2,000 – ₹12,000), it failed to impress. The primary concern was its material – stainless steel with 18K gold toning – which, according to her, lacks authenticity and is unlikely to appeal strongly to Gen Z and millennials, who now increasingly seek either real metal jewellery or trend-forward, high-quality alternatives.

Interestingly, while GIVA operates in the same price bracket, it manages to deliver a superior value proposition. Its offerings have gained notable traction among the 22–35 age group, suggesting strong brand resonance and design alignment with this cohort.

However, the pricing strategy at GIVA also raises strategic questions. Given the aggressive pricing in the fashion jewellery segment, one wonders about their margin sustainability and the timeline to profitability. That said, GIVA’s rapid consumer adoption and repeat usage patterns may eventually lead to economies of scale and brand-led pricing power.

Giva is a VC/PE (Premji Invest & Epiq capital) venture, whose strategy is to acquire market share by burning money, hence they are loss making despite rasing 250+ crore

Pngs gargi is growing sustainability from internal accrual and small fund raises through QIP.

Moreover the fashion jwellery is 10,000+ cr market where pngs has a top line of 100cr and giva about 400-500cr. There is enough space for both of the co-exist and grow

New fund raise is only for 15 Cr so my guess is - this fund raise is to accommodate some specific high value investor like family office or big HNI or reputed PE fund etc. Lets wait and watch

Exactly my point, I think stock is down because people read screener numbers thinking margins are sharply down while company’s number are on expected lines (in not better)

I think the stock is falling because the growth is slowing down in the actual business i.e. sale to end customer.

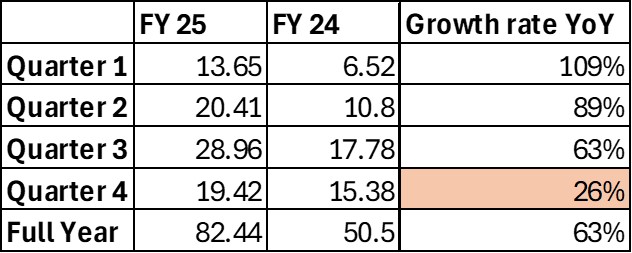

FY25Q4 actual sales - 82.44 Cr - 63.02 Cr. = 19.42 Cr

FY24Q4 actual sales - 50.5 Cr - 35.10 = 15.4 Cr

Rev Growth rate in Q4Fy25 => 26.1%

While if you compare the actual sales growth in Q3FY25 over Q3Fy24, it was 65%

It is a massive degrowth in my opinion and hence the stock is falling.

If you compare the QoQ performance, the growth has slowed down massively to -32%. While I understand that comparing the performance on a QoQ basis of a seasonal company is not something to look after. Degrowth last year for same period was -13.50%

Guys, try to understand the business first, they had an edge of their parent business. They didn’t spend a dime to get what the revenue they have. Because most of the sales came from their parent’s shops. It is obvious if they want to grow, they need to spend much in marketing and stuff this may hamper the margins and you get to know the ability of management to grow the business. I had mentioned in my first post under TAM regarding this that it is easy to get short term revenue because of the parent’s business even had mentioned a psychological effect that may play to get the business from their parents shop.

Disclaimer:- I haven’t tracked this business after my first post. Not invested.

Stock has been de-rated from 95-100 PE to 30-35 PE. Even at 25%+ Revenue Growth (60% for full Year) & 100% Profit Growth (Quarter as well as Full Year), I believe stock is trading at a very reasonable valuation.

Management has given a conservative & High Confidence guidance of 30% sales growth & with Operating leverage profit should grow faster.

Even if there is no re-rating of stock upwards, there should be 30%+ CAGR in EPS which might reflect in price, giving a 30% CAGR return on the stock

Additionally, if the management decided to move to main board this year (They should be elligible), it will be a big boost to sentiments and it will be open for investment by Mutual fund industry (Who are currently mandated to not invest in SME board).