Many of these store might start yielding results in FY26

2 Likes

margin lower due to reduction in gross margin from 43 pc to 39 pc and ebitda margin down from

31 pc to 21 pc. need to understand what led to 4 pc reduction in gross margin , is it due change in product mix towards more of silver jewellery vs diamond studded 14C gold jewellery ?

Further drop of 7 pc from gross margin to ebitda margin is explained by investment in opening new exclusive stores .

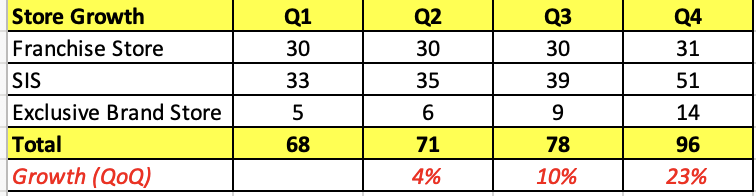

They have exceeded their new store opening guidance ; they had guided to reach 12 new excl stores by mar but they are at 14 , similarly SIS also they had guided to reach 35 by March but they are at 50

3 Likes

Does anyone understands the complete Gadgil Family tree and relation between PNG & Sons and PNG Jewellers?

My current understanding is that PN Gadgil & Company started in 19th century (1858) from Sangli and time after time business was divided between different family members. In 2012, When PN Gadgil & Company was divided between PNG Jewellers (Blue colour logo & Stores, Currently run by Saurabh Gadgil) and PNG & Sons (Red colour logo & Stores, Currently run by Govind Gadgil & Amit/Aditya Modak)

PNG & Sons is actually the promotor of promotor of Gargi by PNGS.

Please correct, if i am wrong.

Also PNG Jwellers are opening a new brand called “Lifestyle by PNG” , will this be a competitor to Gargi?

3 Likes

Both are completely different propositions.

Gargi (wardrobe jewellery) is targeted towards younger working women / early jobbers; with the typical ticket size being around ₹500 to 2500

Lifestyle is a gold jewellery collection; ticket size varying from ₹7000 to 3 lakh

1 Like

I see many SKUs on Gargi website which are upwards of 10k. Do we have any indicated sales contribution by price point? (From any historical con-call)

If PNG Jewelers compete with Tanishq, does this mean Lifestyle by PNG will compete with Caratlane?

Given the market opportunity and synergies, the possibility of PNG Jewelers to launch their fashion Jewelry range remains open?

1 Like

Gargi concall notes for q4 fy 25 :

Fy 25:

- 3.75 crores spent in Marketing , q4 it was 2. Cr.

- B2c sales 82 crores , 62% growth yoy.

- Added 9 stores in H2 fy25.

Fy 26 :

Key initiatives ,

- 12-15 stores will be opened . 50% stores outside Maharastra.

- Blinkit will give visibility for less than 1000/- price range from Utsav.

- Gargi will be launching app on both playstore and iOS together, mostly to avoid giving out huge cut to online platforms .

- 2 Franchise stores in North East will be opened in h1.

- This year marketing cost will be higher at around 7 cr. Will impact bottomline this year due to this in terms of margin but absolute numbers will show growth..

Goal of 10% from online sales in 2-3 years right now its 4% .

Backend( factory) ready to handle 75 stores, right now stores count is 45.

B2c Top-line same growth can be expected.

Potential for another 20 standalone stores in Maharastra where Pn Gadgil son’s stores are not there.

H1 fy 26 6-7 stores to be opened , 5 will be outside Maharastra.

Industry growth is at 25%, Company can beat market.

Last year new stores and current year h1 new stores growth can be seen in Fy26.

On B2c topline of 84 crores of fy25 , we can see growth on topline excluding B2b revenues. Q1 will be better than q1 of fy25 for b2c revenue, need to exclude b2b of last year.

Q4 margin dropped due to marketing cost and Human Resources. Sliver cost had gone up which impacted gross margins, this can happen for 1 quarter once every 2-3 yrs.

Earlier 85% sales used to happen in pngs parent stores now its at 77%

Shopper stop is at 6% , online is 4% will hit 10% in 2-3 years .

Working capital cycle and gross margin : Parent still absorbs the most of the cost where stores are inside the parent stores. Margins are similar at all sales channels.

Stock turn at 4x.

New store setup :

Fitment cost around 25 Lakh, inventory 400 sq feet inventory 30 Lakh for silver jewellery and 50 Lakh for diamonds at label price not cost basis. Not looking at investors/vc types for expansion, need franchise partners who can setup and execute day to day business.

Fund Raise :

Cash lying will be used for inventory build up. Before august 31s 15 cr will be raised as preferential by promoter for marketing costs.

Currently we have 80 stores including shopper stop.

Diamond studded jewellery was 45% for fy25.

Q3 and q4 are strong sales quarters due to seasonality.

Main board :

Once 3 years are completed in December 2025 will apply for moving to main board.

10 Likes

Promoters buying shares worth Rs 15 Cr in the company around current price (considering SEBI ICDR regulations pricing formula) is a huge vote of confidence.

As per my calculations, 10 days VWAP is 905.64 and 90 days VWAP is 979.15. So if relevant date is today, then promoters has to pay min Rs 979.15 per share for preference shares. So company is delaying the relevant date declaration so that high stock price days of Mar 2025 would get removed from past 90 days calculations

3 Likes