The Company is engaged in the retail business of costume and fashion jewellery under the brand name “Gargi” by P. N. Gadgil & Sons" which was launched in 2021 under the artificial jewellery segment. The Company deals in 92.5% certified sterling silver jewellery, brass and copper jewellery, idols and other gift articles.The Company operates through shop-in shop model and has point of sales (POS) counters at 30 showrooms across the states of Maharashtra, Gujarat and Karnataka of P. N. Gadgil & Sons Limited and P. N. Gadgil Art & Culture Foundation pursuant to its agreement with respective companies.

Promoters:

P.N Gadgil & Sons[promoter] is a regional jeweller with almost 200 years of history and an annual turnover of 5500 CR.Gargi is mainly paying rent to the promoters of 3L per store and a 10% commission on sales for using their brand name.

Expansion:

Company has opened 2 new Shop in Shop retail point of Sales at Shoppers Stop (Viviana Mall), Thane and Shoppers Stop (Inorbit Mall), Malad, Mumbai. The Company also has plans to open its standalone retail stores in the FY 2023-24 and expand through franchisees[FOCO MODEL].

Strategic Thinking:

There is a difference between mass and class. Bank deposits are growing by 35%, equity investment is growing by 15%. If Bank deposits are mass, equity investment is a class. So we are in class. Certain people who only know the importance of the brand, importance of the quality, importance of the finishing, they only get attracted to the branded jewellery. And we are thinking about them.

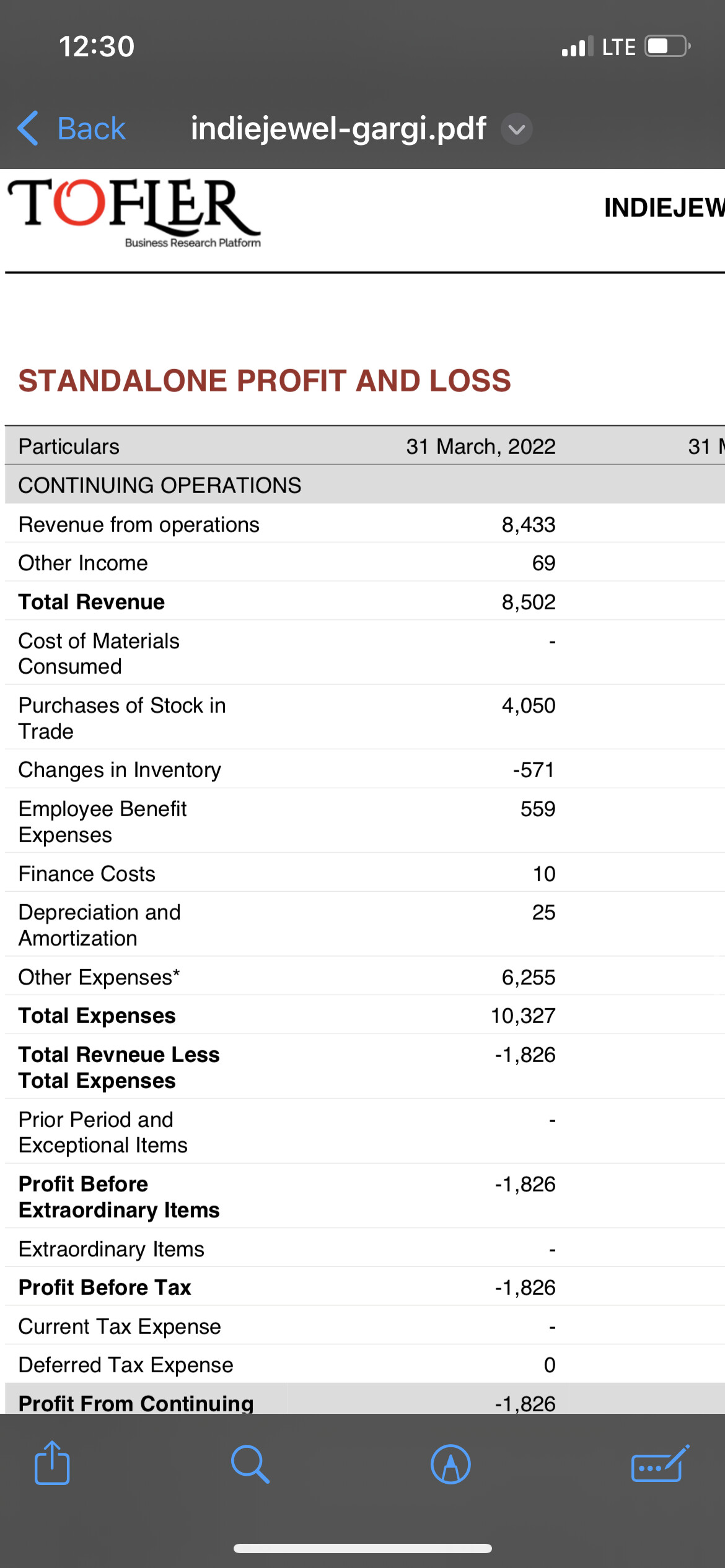

Profitability:

Inventory gets sold within 5 to 7 weeks.

Targeting PAT margins of 6-9%.[Imo these margins will come after they start deploying franchises{FOCO model} till then they can enjoy 15% PAT margins,till date{march 2} they have not given any franchises.

TAM:

TAM of fashion jewellery is 18000 CR.The main thing in this company is its parent is doing a turnover of 5500 CR with its 30 stores and GARGI is also present in these 30 stores. The amount of operating leverage playing is enormous.Even if the parent is not able to grow, GARGI in my opinion will at least get 5% business from its parent, which is 275 CR.Because of the brand already created by the promoter there is a very little need of marketing. Even if the products of GARGI are priced high compared to the market it will not affect much because an anchor is created by the price of original Gold[only if the customer visits the store to purchase gold ornaments].

Competitive Advantage:

Established brand name.

Trustworthy brand.

Brand known for its services.

Risks:

1.The only risk I can see is, if they are not able to grow by the FOCO model,it will eat up the margins.

2. The stock is fairly valued.

3. Management is conservative with its growth.

4. Competition from unorganised player.

5. Giva a private player is currently doing 80cr with 60cr loss.

6. The opportunity is huge, it totally depends on management execution. Management is has turned a 500cr business to 10000cr business(it includes bullions business).

COMPETITION:-

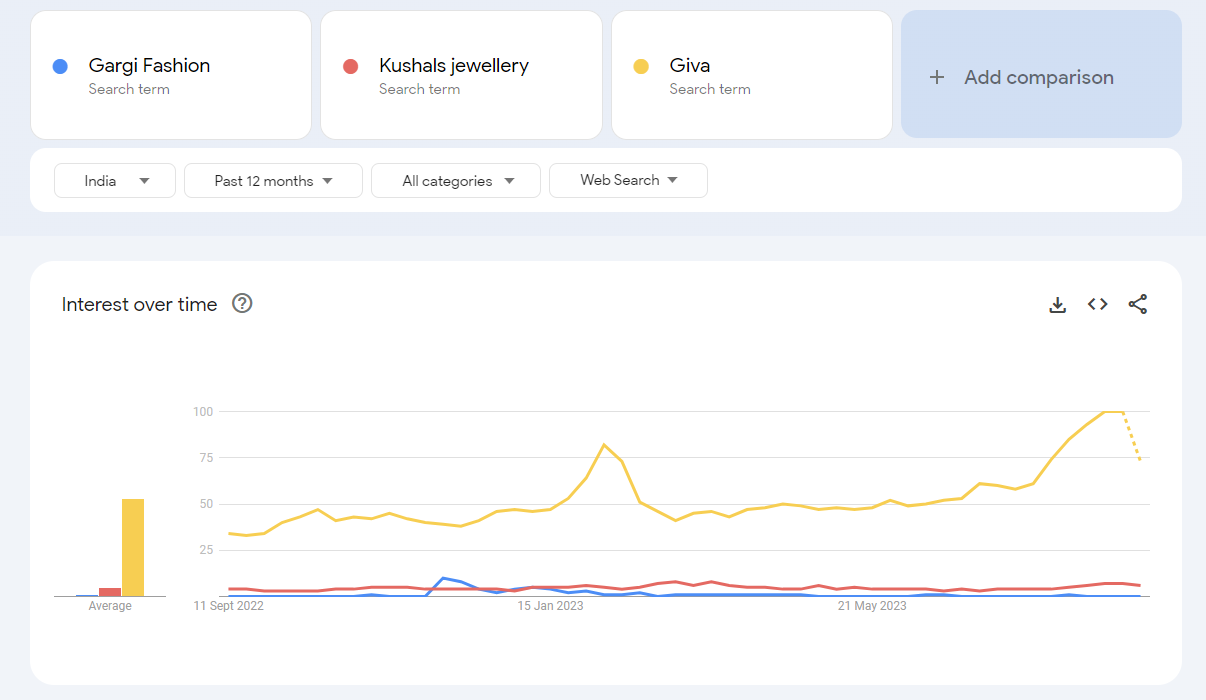

The closest competitor of Gargi is a brand called Giva. Giva is a startup from Bangalore, with a revenue of 80cr and a loss of 18 cr, key thing is they have a great gross margins compared to Gargi.

Thanks for this thread. Some further insights/notes:-

They’re doing pretty great in terms of website design. I noticed features like “Shop The Look” which are high end and you see them on websites like Svarovski or Monica Vinader

Instagram page of Gargi is a nice mix of catalogue + local influencer videos and it has decent traction given the size of the Company. Maybe they could improve upon responding to customer comment section or introducing CTAs like Insta Shop

Their cataloging strategy is excellent with some high def photos (and not CGIs) of model adorning the particular SKU.

Their products unfortunately have no reviews / ratings either on Amazon or their own website. On Amazon, I also noticed that if you search for PNGS Gargi, it shows you some other competitor results on sponsored tag. They might need to fix this.

They have lower SKUs as compared to Giva or even lesser known brands such as Voylla.

Competitive intensity is significant in this category. Premji invest backed Giva, Nykaa backed Pipa + Bella.

I find Aditya Modak to be a very humble - undithered by what competition is doing - sort of a guy. In an interview he talked of how startups are focussed on cust. acquisition but not on retention. Talked of omnichannel advertisement when they open SIS in MBOs such as Shoppers Stop etc. I got the sense that he knows what he’s doing.

I don’t expect fireworks here since they’re not spending huge on advertising, yet at the same time, they’re doing a lot of the things right that even top consulting firms have advised to much bigger Nifty 50 brands So I see some foresight, pursuit of excellence here.

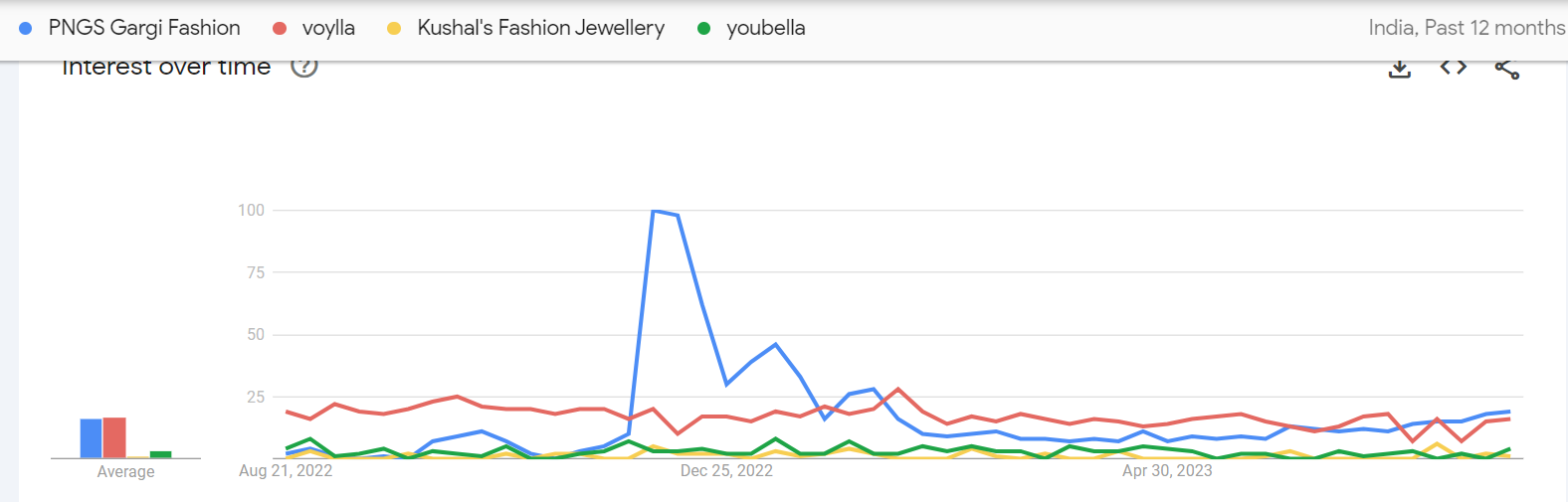

Google trend analysis shows that Gargi clearly saw a lot of interest from the investor community (spike around IPO time) which fizzled out… but if you see the past few months, the trendline is rising again

Company has commenced its commercial sale of 14 Carat Gold studded with diamond

jewellery from today i.e. 17th October, 2023 at some of its sales locations.

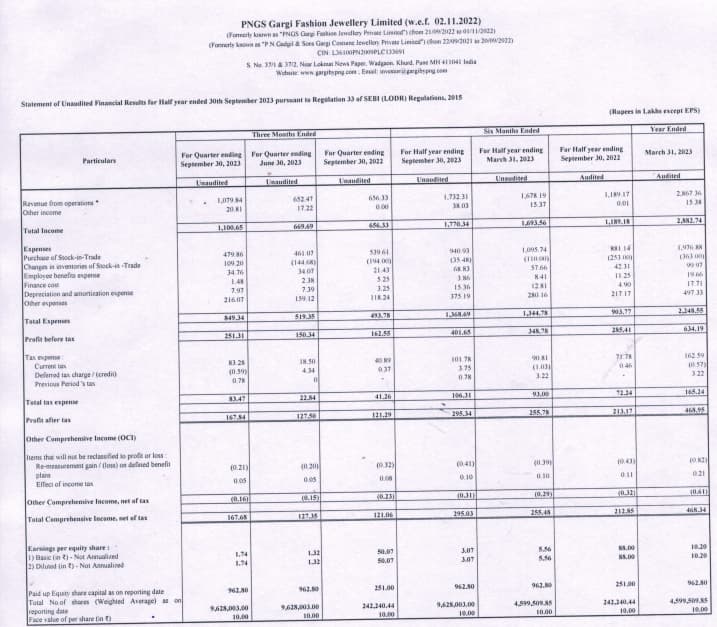

Its jewelry business…seasonality needs to be taken into consideration. Dec quarter is always the best quarter for all jewelry and gifting companies. So I don’t think we should compare QoQ for such companies

Delighted to attend the concall. Very humble and down to earth leadership team. Huge growth potential as company has hardly scratched the surface in terms of all India presence. Company publishing results (and hosting concalls ) on quarterly basis, even though they are mandated to publish only once in 6 months, being SME. Very conservative ( debt free company) and minority investor friendly promoters. On call, Mr. Modak mentioned how they came out IPO in 2022 at price of Rs 30 as promoters believe in leaving money on the table for the investors (they could have waited for 2-3 years and would have got much better price)

I believe this company fits very well in Mr. Kedia’s SMILE criteria - Small in size, Medium in experience, Large in aspiration and Extra Large in market potential.

If this is fashion jewellery then why is it seasonal? Fashion is not seasonal. According to them , the idea of fashion jewellery is more for day to day use . They would even prefer to call it life style jewellery as per the latest concall.

Company is trying to make it life style or daily use item but still its not. As of now, its jewellary first, fashion later. So seasonality would remain till the item become truly “fashion” item which I guess is few years down the line…

The management is relying on change of consumer attitudes for scaling up in future. Any investment here is purely based on assumption that people will adapt and it is not on concrete grounds. Sure management is improving performance on y-o-y basis but that could be because of initial adapters and it may not be major trend. It could also be a fad. I believe there should be some empirical evidence like demand not being seasonal anymore. That is when we can say this is more of a trend than a passing by fad. I can relate this to Tata Nano. It started as a vision of Rs 1 lakh car which is affordable to almost all. Sales picked up initially due to early adapters but then it failed to take off. The management was again relying on change of consumer attitudes which did not happen as buying car was more seen by consumers as a matter of prestige and nano somehow gave an impression of being a cheap car and hence low prestige.