Pix is market leader in the non-OEM segment and Agricultural segment based on this thread at least . Do you have any data to prove that it is not?

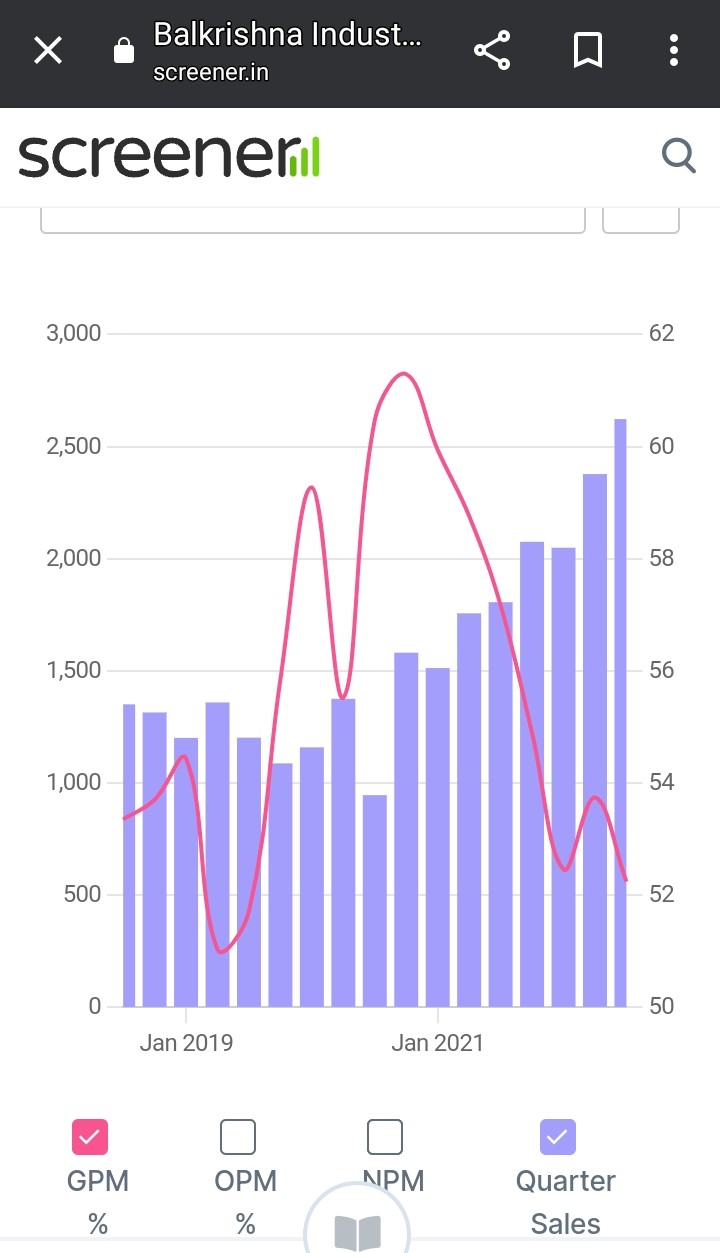

Did you check what the gross margins of Balkrishna were when it had a marketcap as Pix has now? Please provide those details as well so that the community can benefit from your observations .

This Pix v/s Balkrishna debate is meaningless. I am interested in Pix as a potential investment and I feel there is a tendency to overhype certain stocks.

Anyway what is more important to analyse is what are sustainable long term EBITDA margins of Pix.

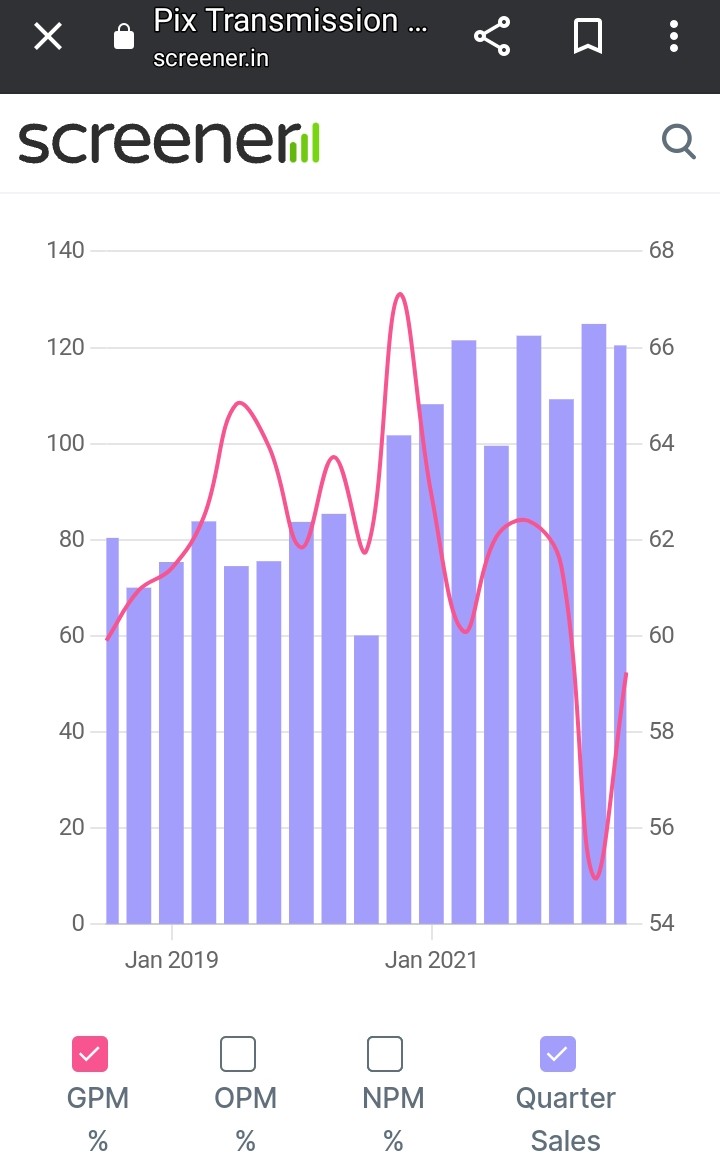

Pre Covid EBITDA margins in FY19 and FY20 was 20%. It shot up to 30% in FY21 and was 26% in FY22. You will see this trend in a number of commodity processors- for example plastic pipe companies or rubber or faux rubber processors like Balkrishna and Pix.

This is because as raw material prices go up companies make inventory gains. Further, let say you mark up prices by 10% over cost. If commodity prices go up your cost goes up and so the same 10% will end up giving your higher EBITDA/kg of product sold.

Since August/ September most commodity prices are falling. So first you have inventory losses which compress margins and then 10% of cost will yield lower absolute EBITDA.

If you notice Pix quarterly numbers there is no EBITDA growth YoY since September 2021 quarter even though sales is growing YoY.

Sales growth is coming due to Price hikes. Co is going through a capacity constraint. New capacity goes live from September onwards. Thus, the topline growth is a function of realizations and not volumes.

To me it looks like both are similary affected GM wise and sales have increased for both but on different scale.While BKT deserves its esteem,PIX has also done well.

Also,in this thread,the discussion is about whether PIX can become better and become like BKT ,not that it already is.There are capexes which will in near future help them in increasing volumes and hence all the discussions.To me it looks like that those discussions are based on data points and adds more value to the thread than generic ill substantiated observations on commodity price.

I was also looking at PIX and have not been convinced enough about its potentialities because probably current price bakes in a lot of tangible future developments.But atleast I now know which contributors can be trusted and which not .

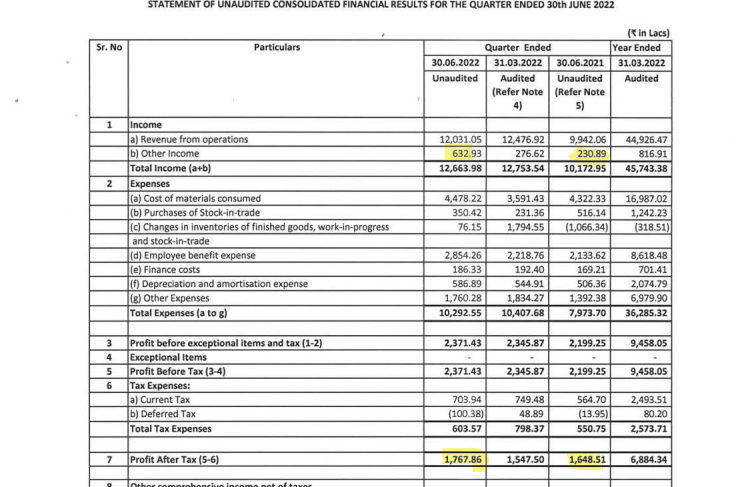

Pix came out with a decent set of Q1 numbers. What is most heartening, are the growing Sales of 120.31 Crs., a growth of 21% over Q1 of last year. This despite plant not working at optimum capacity due to the simultaneous expansion being carried out in the same premises. The Co. is well on its way to doing 600 crs of Sales in the current year.

Let us ignore the high other income of 6.32 Crs. for the current qtr. as it inflates profits & complicates matters!

The Gross margins are well on their way to normalcy. The Cost of Sales is down to 40.76% in Q1 as opposed to 45% in the previous Q4, which was 39.86% for the whole of PY 21-22. This should fall further in the coming qtrs. This means that the high raw material costs of Q4 are to a large extent being passed on. With falling commodity prices, they should get back to normal sooner than earlier anticipated.

What has perhaps upset a few investors is the further fall in operating margins in Q1 to 21%. This is due to the steep hike in employee cost, up from 22.18 crs in previous qtr to 28.54 crs. Employee cost unfortunately is loaded at the front end, as it is increased at the beginning of the year. Its impact will not be felt as much for the year as a whole as Sales grow to about 600 crs. I suspect, for the full year. as a percentage of sales & profits, the employee cost will be at about the same level as last year. If only mgts. take their annual salary hikes in Q3 or Q4, this would not be felt as much!

So all in all, things are moving in the right direction. Pix has created enormous shareholder value over the last 2-3 years, and I feel the party is a long way from getting over. With booming exports, growth looks more predictable now than it did three years ago. So keep the faith guys!!

hi VP members

new to investing and to VP

thanks all the people in the thread for wonderful research

just one thing i noticed from recent quarter results is that if you look closely at q1 22 and q1 23 results although bottom line appears to have increased but if we deduct other income from bottomline in both we get a degrowth in income of 20% YOY

please feel free to correct me if i missed something here

Isnt this by itself a big red flag. Do any long term trackers have am opinion here. I wouldn’t touch this company with a flag pole if Dr. Malik is correct.

But out of the last 4 quarters, 3 have seen YoY PAT decline and 1 quarter of tepid YoY growth.

People said the same about the likes of Everest Kanto and Tanla. But then when numbers disappoint the stock gets hammered. So please don’t say red flags don’t matter.

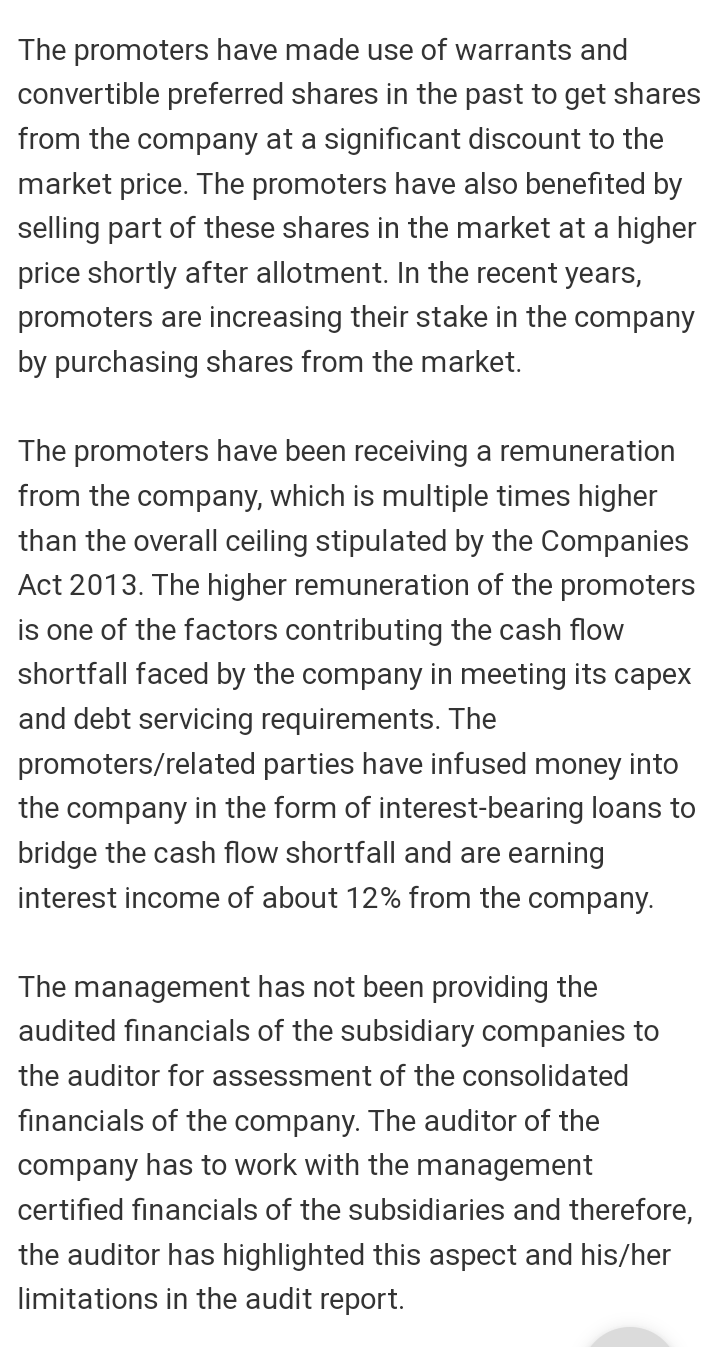

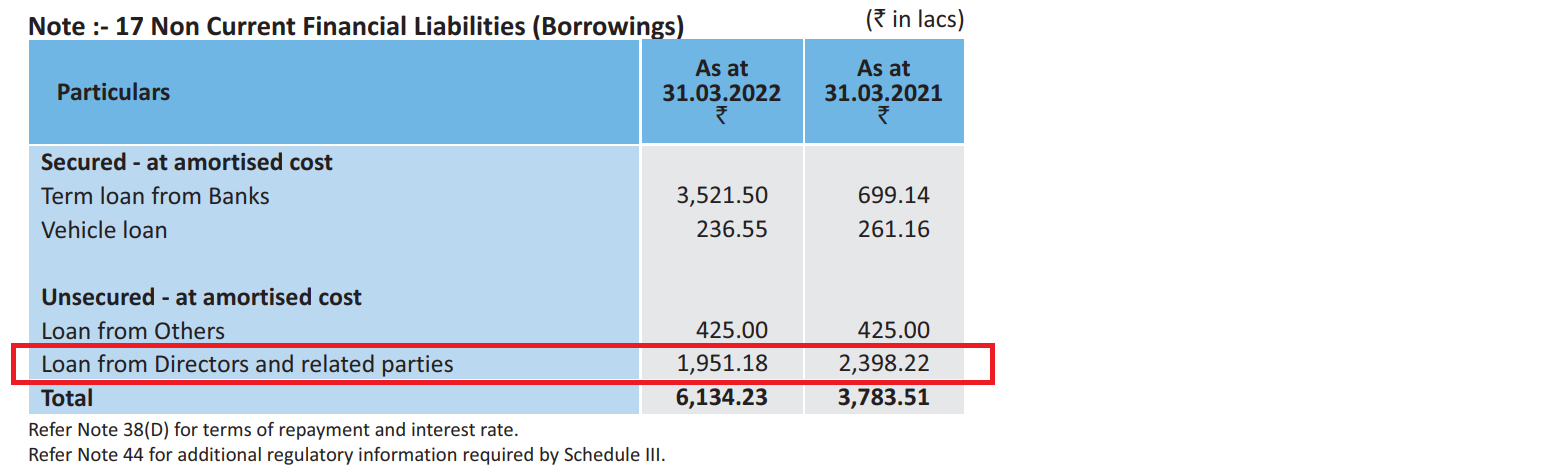

The Director compensation as a % of Net profit stands at 13.3% for FY21-22. This was 11.7% in FY21-22. This is indeed a concern and investors should write to the Management asking them about this. The Law permits Directors to be paid in excess of 11% of PAT via special resolutions requiring majority shareholder approval, but that approval is just a token as Promoters hold 61%

As far as I could see, the o/s loan to directors was 19.5Cr at FY21-22 end as opposed to 24Cr in FY20-21 end and a total interest of 1.7Crs was paid on that. Taking an average o/s balance of 22Cr, 1.7Cr amounts to 7.7% interest. So I don’t think there’s any leakage happening here. Unless I have missed some data and my calculations are wrong.

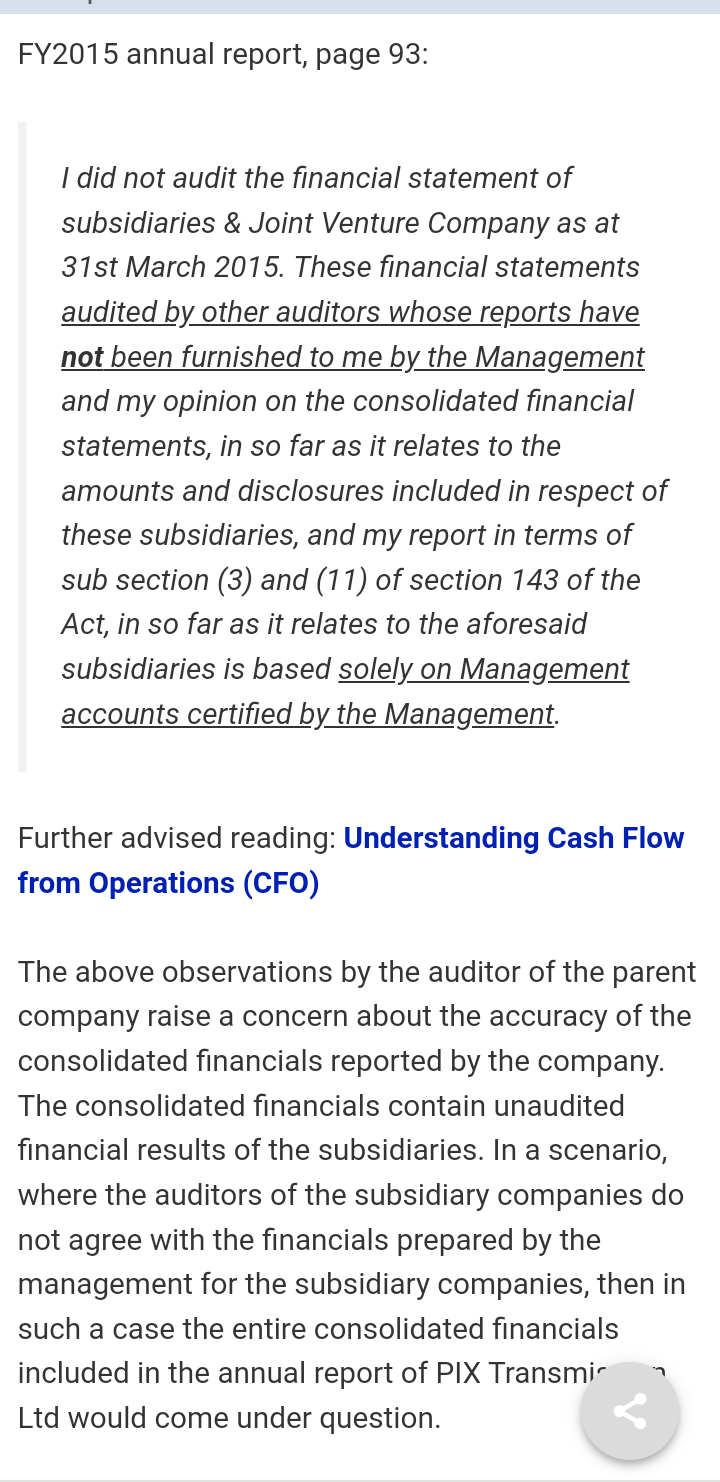

The concern about non-audited foreign subsidiaries is also valid. It seems that Pix’s European subsidiary (England) is not audited at all while the Dubai subsidiary is audited by a local firm. The auditor’s report mentions that foreign subsidiaries which contribute ~20% of PIX topline and ~10% of PIX total assets (This is the European subsidiary) are un-audited and they rely on Management data to certify their financials. People more experienced in accountancy can comment whether this is a red flag or common practice in Indian small/mid caps.

Also audit fees have jumped by 150% from 6 Lakhs to 15 Lakhs this FY. What changes in the company must have necessitated such high jump in auditor remuneration when revenues have only increased 20% YOY? As per the latest AGM resolution passed, now they have appointed MSKA for 22 Lakhs per annum. Again, a steep rise.

Some of the questions raised by Dr. Malik are valid in my view. Even though they may not point to any Corporate mis-governance, they are red flags. Experienced investors in PIX who have attended the AGMs @RajeevJ@sahil_vi@ayushmit can probably throw more light on these concerns. The biggest concern for me is the huge jump in Auditor fees and what justifies the jump?

Concerns expressed imho are not relevant to how investing works in smallcap in india. As long as co can deliver profitable growth, paying directors more is something market is willing to digest.

Good points and definitely something to think about. High compensation might not necessarily be a red flag. But other points mentioned related to audits and audit fees is definitely something that needs to be thought about.

I have limited understanding of how other smallcap companies do it but taking high salary and then lending to the company at high interest rate might not reflect well on the managements image.

Maybe someone needs to ask these questions in AGM etc.

Funny thing about red flags is that they only get importance in hindsight, when something goes wrong.

Salary - yes, it’s a bit high and I hope the management takes note of it and takes steps to stop increasing the same and reward themselves by way of dividends etc.

But this is not a deal breaker for me. Usually I have seen that in small/mid caps it happens as there are several family members involved (and some CAs advice to charge the max amount allowed) and it’s better that they take remuneration upfront rather than through wrong/hidden ways. Infact the other way I think is - if the margins are so good despite such salaries then it means that the core profitability is even higher and its good for longer term.

As you mentioned, interest looks reasonable.

In almost all audit reports, one will see the same language for foreign subsidiaries. No Indian auditor will take responsibility as they don’t audit themselves. Regarding the steep increase - i think it might be due to the reason that they have appointed MSKA. MSKA is a very big and reputed firm…i think it is amongst top 10 or so. If so then charges will be higher and it’s good that the co is getting better auditors.

Salary - yes, it’s a bit high and I hope the management takes note of it and takes steps to stop increasing the same and reward themselves by way of dividends etc.

But this is not a deal breaker for me. Usually I have seen that in small/mid caps it happens as there are several family members involved (and some CAs advice to charge the max amount allowed) and it’s better that they take remuneration upfront rather than through wrong/hidden ways. In fact the other way I think is - if the margins are so good despite such salaries then it means that the core profitability is even higher and its good for longer term.

Agree with you, its not a major Corp Gov risk IMO but may paint a picture as a minority shareholder unfriendly company. I have written to the company asking them about this, let’s hope they respond.

In almost all audit reports, one will see the same language for foreign subsidiaries. No Indian auditor will take responsibility as they don’t audit themselves. Regarding the steep increase - i think it might be due to the reason that they have appointed MSKA. MSKA is a very big and reputed firm…i think it is amongst top 10 or so. If so then charges will be higher and it’s good that the co is getting better auditors.

That makes sense and should be the explanation. Ajmera and MSKA were joint auditors this FY. Seems like they have split the compensation of 15 Lakhs half and half. Next year as MSKA takes over completely, they have hiked the rates to 22 Lakhs, most likely paying a premium for MSKA’s reputation.

Always good to hear the views of folks who have been invested in a stock for a long time and have interacted with the Management. Its re-assuring for newer shareholders.

Replies received from the company to my queries. They are more or less in line with what @ayushmit has already said. But good to see that the company is responding to retail investor queries. I have found many small-caps not bothering to reply.

Q1. Directors’ remuneration - Directors’ remuneration as a % of PAT stands at 13.3% for FY21-22 which is significantly higher than the 11% cap as per Section 197 of Companies Act. While Company is free to pay its Directors more than the cap via a special resolution, higher than 11% remuneration is usually interpreted as being unfriendly to minority shareholders. Does the Management have any plans of bringing the Directors’ remuneration below 11% going forward?

A. Directors’ remuneration is commensurate with the size and nature of our business and the additional burden that Directors shoulder to ensure the Company performs at optimal levels so as to consistently deliver value to all concerned stakeholders.

Q2. Auditor fees - Auditor fees in FY20-21 was 6 Lakhs, in FY21-22 was 15 Lakhs and I can see in the AGM resolution, Auditor fees will be 22 Lakhs in FY22-23. What is the reason for 3.5x increase in Auditor fees in 2 years when Pix revenues are increasing only 20% YOY? As far as I am aware no. of subsidiaries and business complexity have remained the same, so why the steep increase?

A. With a view to further strengthen the Company’s adherence to accounting standards and to safeguard its interests, the Company enlisted the services of MSKA & Co which is considered to be one of the pioneers in their industry. As such, their professional fee is at the higher end of the spectrum.

Q3. European Subsidiary not audited - Why is Pix’s London based subsidiary not audited at all? This was mentioned in the Auditor’s comments for consolidated financials. This subsidiary contributes 20% of PIX revenues and 10% of PIX assets, so it is definitely a material subsidiary for the company. Why is this subsidiary’s financials not audited and will the Management start the practice of auditing for this subsidiar from FY22-23?

A. Your Company complies with all the laws prevailing in its countries of operation. Currently, the threshold has not been reached to perform a full audit of our European subsidiary. If and when the threshold is reached, your Company will take the requisite action.

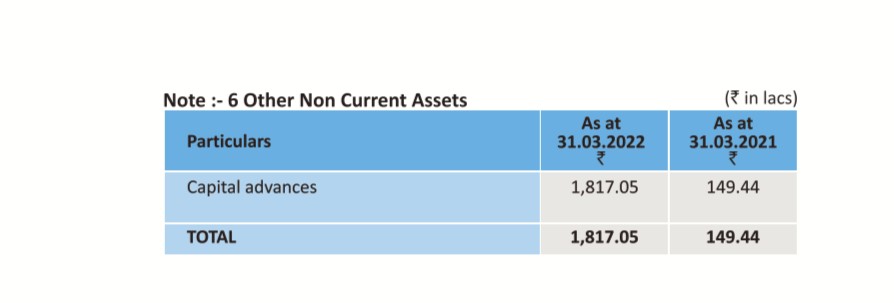

Hi Rajeev, I am been following all your posts on pix since the beginning of this thread, and thank you for sharing your thoughts and info. Can you please help me understand this increase in Capital Advance in 2022 Balancesheet? this amount is up from 1.5 cr to 18.17 cr. Thank you

@Raj_Praj

This amount is probably advances given towards purchase of plant/ machinery for the proposed expansion. There are many contributors to this thread who are tracking the balance sheet closely, who are welcome to shed more light on this.

Generally speaking, once I am comfortable with the mgt, I try to focus more on my basic investment thesis playing out well & on track. If I am not comfortable with the mgt, I will exit the Co. altogether. I believe that other investors too could benefit by following this policy. It has helped me too in keeping my focus. For me, the Pix mgt has walked the talk & I have confidence in their ability to deliver.

Meanwhile, the Co.'s expansion is hopefully playing out to plans. The phase wise expansion should be completed sometime later this year. I expect the enhanced capacity to support Sales of about 750-800 crs. This could be more or less consumed in the coming year 23-24 & I will certainly not be surprised if the Co. were to announce the next phase of expansion in the next six months!

We are already in the beginning of September & shortly one will start extrapolating the numbers for 23-24. If only the Pix mgt would initiate investor con calls a couple of times a year, many of these growth issues could be addressed. As the market cap grows, Co.'s are known to get more responsive to investor concerns. That said, we are talking of a 1200 cr. market cap Co. so we can assume that the mgt knows a thing or two!