AGM notes

R&D is key to success. R&D spend is 0. It merged with other expenses. From coming year, We will share separately.

This year, will introduce new generation product, will spend can couple of crores. They have an RD facility specifically dedicated and it has some 15 Employees, their salary gets clubbed in Employee benefit.

Ball park number for R&D 2-2.5 crores.

They have a Dedicated GM.

Comments on switch from chains to belts ?

Servo motors, call for timing belts, which Pix produces.

Couplings or chain drives can’t replace v belt. Chain drive is noisy. Cannot work on high RPMs. Chain is costly too vs Belts, chains can be applied in specific applications where low load is needed.

EV scooters has belts, we will drive that. We are working with some players like Ather

Atleast next 20 years, no issue with belts.

Global market size : 20 billion dollars. We are not even fraction in this market

Agriculture belts : We are largest in agriculture segment.

Whole world needs Roti, kapda, makaan.

Roti : Area of land not grow, more mechanization needed, hence our belts will be needed.

Kapda : Textile big consumer of belts.

Makaan : infrastructure. We need lot of port, highways, canal, irrigation system, airports. It needs belts. Infra will include Real estate, we got cement, steel, mining need belts.

At Pix Agri belt at 10% (~50 crores)

Agriculture is driven by climatic conditions/changes.

We are focussing on Vietnam, developing that in agriculture can be a 10 crore market.

Russia, Ukraine We are still supplying receiving payments. Western Europe seeing challenges.

Iran we used to do with INR trade. Last 2.5 years, RBI put sanctions. Now stopped. It is 10 crore market for us.

If RBI is now trying for INR trade, need to bypass Iraq sanctions.

Capacities are fungible, for all belts. We are most well spread companies in this space, say some end customer slows, we will divert to others. Our competition is focussed on a specific end market and hence can call for troubles.

Pix traditionally has been after market company.

In OEM, no brand creation. We tell we are suppliers toMM, Tata motors, IFB, whirlpool, Ingersol Rand. But brand creation not possible, ultimately they print their name.

90% of products in Replacement market. That is where value company wants to focus.

India : 300 distributors

US : 500 distributors (need to confirm, is it this wide?)

You walk down hardware company, u will see pix.

After market Replacement, high margin vs OEM.

For me to setup an office globally need 25-30 crores. US looks uncertain under Joe Biden. Hence use US distributors.

45000 SKUs. (This for me is really impressive)

When we go to open trade, Germany 30 days, US 60 days from end of month, Walmart(90 days after it leaves shelf).

I buy from reliance : upfront payment (they buy carbon black). Also birla supplies.

90 days is industry trend.

Total receivables made some changes to reduce them.: overseas business, due to uncertainty except for old distributors old (25-30 years sure money is secured), everyone now is upfront payment. India also we now take upfront payment.

With time, days will come down.

Global market is 20 billion dollars.

Indian is < 2 billion dollars.

We can grow fast in exports.

Globally, it may not be visible, underlying organizations away from China. US dependent on China, gradually moving away. Whirpoll US sole suppliers were china. Today we got orders for 3 million belts p.a. Elastic belts.

Market is large.

We are among Top 7/8 globally.

Motion industry in US. One single customer has 140 million dollars order they will not come to us.

They will never come to us. For that I need atleast 140 million dollars sales.

All their systems, linked to Gates system.

Globally very small player.

Gates belt revenue : 3 billion dollars.

Bando : 1 billion dollars

We do distributor analysis where it goes in end user, will do for strategy.

We try to pass on prices.

Normally cant increase prices once/twice a year.

India we did this time, 1st July, 8-9%. We need 50% more (total 15%), EBITDA margin 25%.

Globally anytime we increase.

All our suppliers are monopolistic suppliers. Take it or leave it. Price of comodity reduces, we dont get full pass on. Thing that has increased 10 won’t come down 10, now will come down 1rs.

Earlier we used to annually, half yearly, quarterly now price applicable on dispatch.

Carbon black. (Largest player) : price on dispatch

Natural rubber : when I started 4 rs a kg now it is 175 a kg

Carbon black : 2.9Rs now 140 rs

We will focus on own efficiencies to maintain margins.

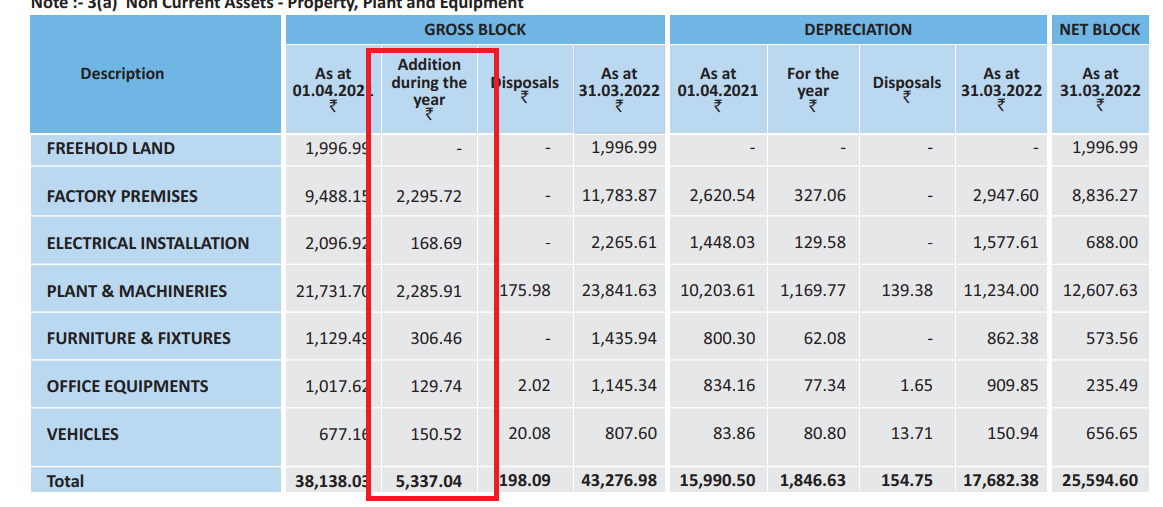

New expansion will prepare for 800-900 crores (75k belts a day gone unto 150k belts per day). Current capacity is 65000-70,000 belts per day.

From drawing board to reality in capacity is 18 months.

We have enough land bank with us. Now get land land is tough.

When we work with Global customers who are from industry. Come here for audits, they say best we have ever seen.

Customers coming to us and asking, do you guarantee enough FG to supply to us. They need reliability. They are sticky.

We increased inventory since

Belts for EV vehicles. EV works on motors. EV scooters has belts. Honda/TVS/Yamaha/Piaggoe scooters (competition with Japanese bondo belts), has belts. New generation mototrcyles has belts. Usually motorcycles dont have belts.

Ather 2W approached us.

We try to generate a higher generation of product, works under strenuous life, higher life, more value addition.

Now it is getting traction.

Last year also 8-9% hike

Distributors are exclusive

Every automotive has own spare part dealer network take product from u and push through them.