Hi guys,

I am new to this forum. I would like to take this opportunity to open this thread on this microcap company.

The company is located in Nagpur, Maharashtra and commenced its operation from 1981. The company manufactures wide range of rubber V-belts and related products.

The key raw materials are synthetic rubber and natural rubber.

Key financial data – 2014-15 (Rupees in crores)

Equity 13.62

Reserve 135.59

Revenue 221.86

Of which exports 94.94

Net profit 3.91

EPS 2.87

As against market cap of 68 crores, the company is having net debt of Rs. 134.43 crores which is a cause for concern.

The company borrowed term loan @ 13.75% to 14% towards capital expenditure, new product .

The company sold one of its business for Rs.85.62 crores in the year 2012 and partly retired the debt.

Incidentally, the company declared special dividend of 30% in addition to 15% out of the profit on the above sale.

The company has exported products to more than 50 countries particularly to Europe and Middle East.

To cater the exports, the company is having two subsidiaries, namely, Pix Transmission Europe and Pix Transmission Middle East.

Pix Transmission Europe is having Pix Transmission Germany as its subsidiary.

Further, the company is having joint venture at Ireland and Middle East.

Though, the key raw materials synthetic and natural rubber are at low level , the margin is low due to stiff competition and economic slowdown.

The company is number one in India in this field.

The company is commanding brand equity in local and abroad.

It is having state of the art technology in adopting for manufacture and excellent infrastructure for hi-tech applications.

Hence , its products fall in special category.

The future performance of this company hinges on the growth of automobile industry, machinery manufacturing and agriculture.

The net profit of the company for the year 2014-15 has been halved over 2013, due to exchange rate fluctuation, high depreciation and interest cost.

The financial cost of the company itself is around Rs.15 per share.

For the current year also, the Q1 performance was dismal.

However, the company came out with better performance in Q2.

WHY THIS COMPANY?

The promoter, over the period, increased their holdings from 52% to 60.54%.

Though the dividend has been reduced from 15% to 10%, the dividend yield is attractive at 2%.

This shows the promoter’s confidence over the company.

The company is servicing the debt very well.

On clearing of at least 75% of debt alone, the earnings will increase substantially.

There is no pledge of shares by the promoters.

The company will show reasonable CAGR by cashing development of new products, capital expenditure made and rupee depreciation.

Due to economic slowdown, the company is not in a position to take opportunity of low key raw materials cost.

The company is continuously spending amount for new product development.

Once the economic revive, the company can increase the business as well as improve its net profit margin.

CONCERN

As on 31.03.2015, the company was having investment in liquid funds to the extent of Rs.12.9 crores and cash and cash equivalent at the extent of Rs.15 crores. It is not clear why this amount has not been utilized for prepayment of high cost debt. (In the year 2013-14 also, the company kept cash and cash equivalent at high level)

The company share is listed only in BSE.

Dis. Since I invested, my views are highly biased. The views are only to share information and it should not be construed as my recommendations for purchase/sale .

I request the members to critically analyse the company and to understand the future prospects of the company.

Hi

@ Agarwal

Here PE ratio is not the only criteria to ascertain the margin of safety…

The company made huge capex for development of niche products by availing term loan.The annual financial cost Rs18/-crores. forms major part of exps. Product wise .it is the best company in India command excellent brand value in India and abroad.

As against the market price of Rs.50/- the BV is 111.

The bottom line and top line will improve on revival of economy.

I recall PIX transmission while we were buying Belts from them…product quality is good… but Competitor were producing superior quality belts-(Competitor Fenner) since Pix fall under cyclical & Parasitic industry demand is driven basically from Auto sector and Agri business and lastly Capital goods industry as of now i don’t see superior performance as of now.from any of the above sector. will put in my watch list and monitor the performance.As rightly said by Gaurav there is no margin of safety and DEBT is too high for the income generated by the company.what kind of moat will protect them in coming days as these products are more commoditized…

Disclo : I don’t hold stocks but it’s under my radar

@Girish

Fenner India is the pioneer in India for manufacturing rubber V belt and it is more than 100 years old company. The company was the part of erstwhile Madura Coats.The working of the company was severely affected after taken over by Manuchabria,then infamous take over king.Now Fenner is under the fold of JK Singhania group.and they are taking all measures to bring back the glory. Pix initiated action from 2010 for improvising and development of new products.

If details ofJK Fenner is available comparison with pix can be made.

Now what happened in the stock markets is not our business, but its still doing well, its paying dividends, its creating wealth and most of all Somi Belts is not a real competition as its the only listed Indian company as Pix has foreign promoter and great experience in doing the job, as soon as india picks up, we need machinery and they needs Material Handling that can only happen using belts provided by these guys, they supply many belts for various industries and have a great reputation. I think there will come a day when every Indian company making some thing needs MH and convener belts are going to be used, then you wont get Pix at Market Capt to Cash Flow: 2.18. I am positive the days inventory outstanding will reduce.

The company to consider final dividend and fourth quarter result on 28.05.2016.

The co. already declared 10% interim dividend.I expect better growth both

top and bottom line.

However one positive(?) aspect is the management proposed 5% final dividend in addition

to 10% interim which repose faith on future prospect by the board.

Hi

The company came out with much better performance.

Y O Y finance cost reduced considerably.

In its note the management exudes confidence over future prospects due to

better economic condition.

The company has declared excellent Q2 results.

What is more, it has stated in its report the order position has been improved

and expect better perfomance in next two quarters

I have not come across any guidance given by the management

for reducing DE ratio.However it is observed that the finance cost is

lowered every quarter despite improvement in revenue.

Disclaimer:Recently I completely exited to book profit and

no other reason

Pix transmissions is looking interesting at current levels. Q1 was possibly affected by GST issues like many other companies, & the stock seems to have been hammered down to attractive levels. What I particularly like about Pix is its high operating margins of around 20%. Can’t think of too many companies of this size that are commanding such margins. Which also means that any meaningful growth in Sales would lead to a disproportionate growth in profits. If only the mgt. would liquidate its investments / cash in books for debt reduction, this story could be re-rated instantly.

Even if Pix, currently available below its book value of Rs. 121, can repeat last years performance, at the current market price of Rs. 113, it is available at a multiple of around 10 times its current year earnings. It is relevant to note that the mgt. has been sending positive signals by a continuous increase in the rate of dividends for the last 3 years. The high dividend payout ratio also adds to the flavour!

A decent Sept qtr., with improving operating margins seems to excite the markets. Despite the near 50% run up, the stock still appears to be quite cheap. Even a 10% growth in Sales over last year could potentially re-rate the stock, given its improved margins. With the economy set to pick up, Pix appears to be in a sweet spot.

@RajeevJ sir and fellow PIX investors ,

I am a novice to value investing and to VP, so please excuse if my analysis is not rock-solid. I took a small position in PIX in Oct and trying to build conviction to load up more despite the run-up in prices. However, I see some potential red flags and would invite your counter arguments on them.

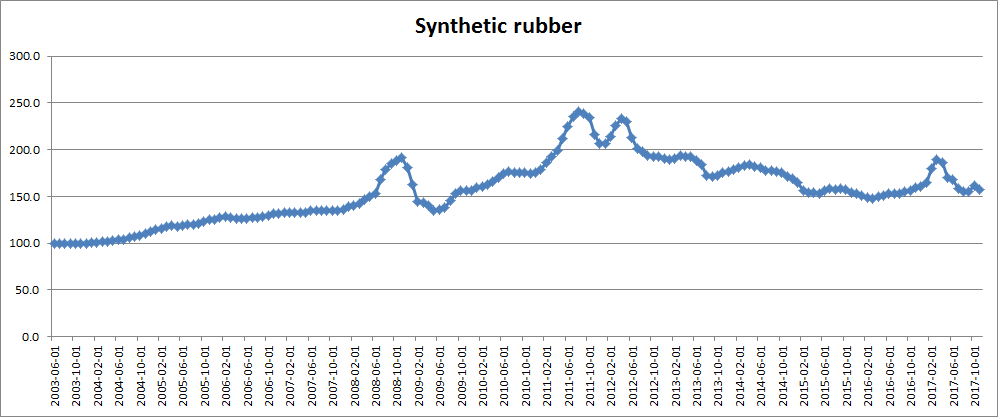

1).I understand that Synthetic Rubber [SR] (and not natural rubber) is the key raw material for PIX. There seems to be a strong correlation between SR price and PIX’s COGS. COGS was 58% in FY13, then fell steadily to 42% in FY17 just as SR prices declined from their peak in end of 2011.

Synthetic rubber is a crude oil derivative and crude levels are expected to increase (moderately?) over next 1-2 years.This could erode PIX’s margins. 10% increase in COGS can result in OPM going down from ~20% to ~16% or a ~20% fall!

Low interest coverage (FY 16 @1.4 and FY17 @2.5) exposing PAT to interest rate rise (RBI can very possibly increase rates in 2018).

I could not find any references in recent ARs on debt reduction plans and/or liquidation of current assets/ investments. Was there any mention in conf. calls or elsewhere?

Historically wafer thin net profit margin (~2%) questioning PIX’s “brand” value and moat. A reference was made to this also by @param77 earlier in the thread. Why should we expect that Sales growth will lead to accelerated profit growth?

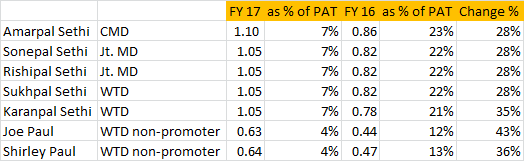

High promoter remuneration as % of PAT. The promoter group together got paid 5.3cr in FY17 and 4.1cr in FY16 against PAT of 14.7 and 3.7cr respectively. Isn’t that excessive? In addition, AR17 lists rather generous benefits for the execs.

What evidence there is to guard against Promoter capturing an outsized part of profit growth going forward. FY 17 as % of PAT FY 16 as % of PAT Change %

Amarpal Sethi CMD 1.10 7% 0.86 23% 28%

Sonepal Sethi Jt. MD 1.05 7% 0.82 22% 28%

Rishipal Sethi Jt. MD 1.05 7% 0.82 22% 28%

Sukhpal Sethi WTD 1.05 7% 0.82 22% 28%

Karanpal Sethi WTD 1.05 7% 0.78 21% 35%

Joe Paul WTD non-promoter 0.63 4% 0.44 12% 43%

Shirley Paul WTD non-promoter 0.64 4% 0.47 13% 36%

I would really appreciate to hear your counter-view on the above points!

Thanks!

Capex that has been done over the past 4 years in the V-Belt business seems to be coming on-stream now which explains the top line growth. No more ‘Capital Work in Progress’ on the books since all Capex has been absorbed into Plant & Machinery now.

They seem to be unaffected by the sharp rise in Carbon Black prices (EBITD margins have gone up YoY). This could be due to pricing power for their products (the cost of a v-belt is a small proportion of the total cost of the engine). Another reason for this could be consumption of old inventory of Carbon Black due to which the higher cost hasn’t been accounted for?

We will need to talk to management to get a better understanding.

Concern now seems to be that they have put 19 Crores in Inventory and Debtors against a Cash Profit of 35 Crores.

Hi @seth_parth,

“Concern now seems to be that they have put 19 Crores in Inventory and Debtors against a Cash Profit of 35 Crores.”

I am not that well versed with balance sheet basics.

Where in this year’s result disclosure can I view the 19 crores Inventory& Debtors entry?

Also, where to locate/compute the cash profit figure of 35 crores?

Disc : Looking to enter at 135-140 levels if market permits.

Pix Transmissions came out with a great set of Q4 numbers. As I am not sure about the sustainability of Q4 margins, I am taking the profitability margins for the entire year 17-18 to average it out. The Company seems to have completed its current phase of expansion & is possibly reaping its benefits. The high operating margins have sustained / improved & this has led to a disproportionate growth in profitability with even marginal growth in Sales, as mentioned in my post September 24, 2017.

The expansion has been completed at an opportune time. The effects of GST implementation / demonetization have clearly been absorbed by the system & the economy seems to be returning to its earlier growth trajectory as the recent GDP numbers seem to indicate. This pick up should logically result in decent sales growth in the current year & with its high operating margins, we could see another disproportionate year of growth in profitability. A 15% top line growth in 18-19, could result in an EPS of about Rs. 20 for the year.

Despite its high margins, the stock is still available at about 10% higher than its book value of about Rs. 138 as on March 31, 2018

There could additionally be another pleasant surprise in store. These numbers pertain to the stand alone Co. It also has a couple of subsidiaries abroad. These subsidiaries are marketing Co.’s & their profitability has not yet been factored in.

FY 17 as % of PAT FY 16 as % of PAT Change %

FY 17 as % of PAT FY 16 as % of PAT Change %