Yes that is healthy as long as growth comes, and was essence of post

Last I checked, Mayur have no returns for 7+ years horizon till date - compounder as per my limited understanding don’t have such character , Mayur vs Balkrishna from the point it got listed in chart , and point of Post was to relate Pix and Balkrishna, and possibilities of Pix following path of BKT - rest my case here - (BTW am invested in all three of these - allocation differs)

Yes, that’s the thesis for most of us as well. Growth will make investment heavy biz look leaner and aligned to growth, doubt if working capital can/will change drastically, but as top line grows, it would look healthier in proportion.

There are some fantastic insights in the latest concall held by Gates in February last month that builds a longer term conviction in this business. Gates’ Q4FY21 concall.

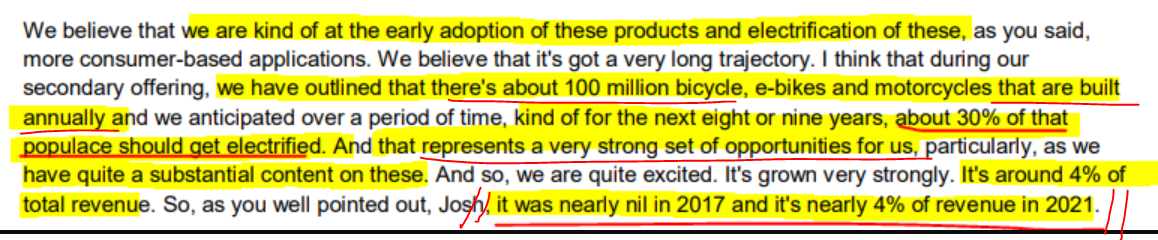

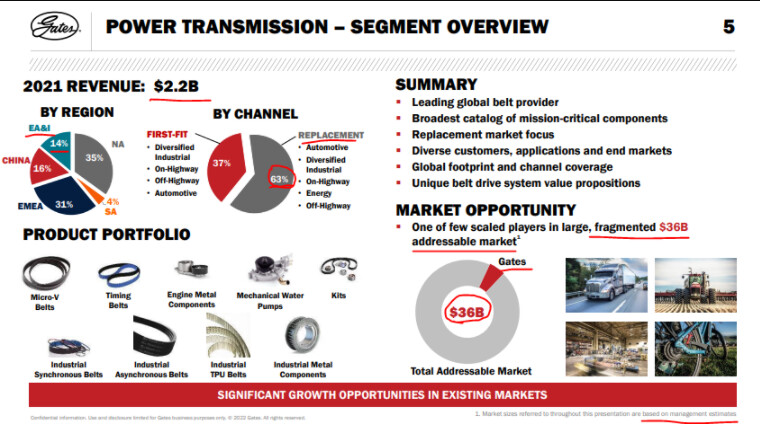

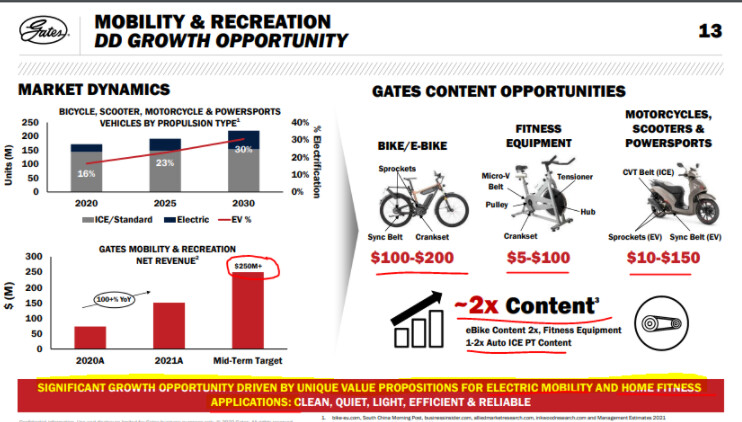

The most interesting bit of the call was their discussion on the opportunity in the EV space. It was Nil for them in 2017 and is 4% of their $2.2 Billion Power Transmission business currently, that is close to ~$88M or >650cr in INR terms.The largest organised player globally has 1.4x of PIX’s TTM revenues from EV segment.

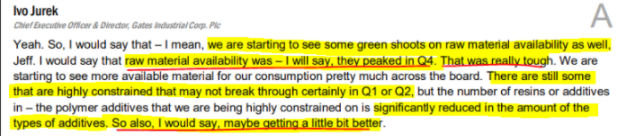

Raw Material situation is bad but it has stabilised now and is starting to get better. They have taken multiple price rise to combat RM issues and may take further price hikes.

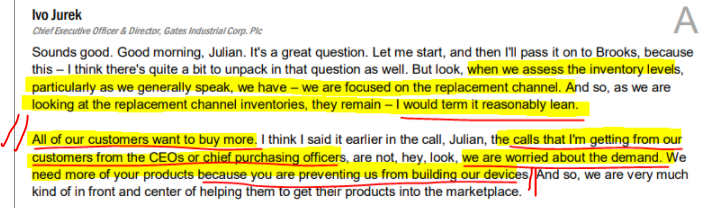

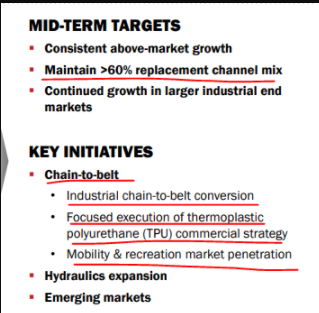

According to their estimates, this is a $36B fragmented market. This is a big number. Interesting to note that >60% of their revenues is from the replacement market and their mid-term target is to maintain that.

The Indian Rubber industry is poised to grow rapidly. The industry comprises of both natural as well as synthetic rubber which compliment each other, in that most rubber products contain a combination of both. The share of synthetic rubber in India is about 35% as compared to 65% globally. Not only are we consuming all the natural rubber that we produce, we are a net importer of natural rubber. As technology improves, the use of synthetic rubber in the mix will only go up. The Govt., aware of this, is vigorously trying to promote synthetic rubber due to the enormous export potential of rubber products. India’s per capital consumption of rubber is only about 1.2 kg as compared to about 8 kgs in China & over 10 kgs in the industrialized world. As the Indian GDP grows, the rubber consumption is set to grow disproportionately.

Attaching a link to a recent article on the rubber industry & various companies in the sector, that is quite informative. Of all the companies discussed, Pix perhaps enjoys the highest operating margins, indicating that it is the least commoditized in its products.

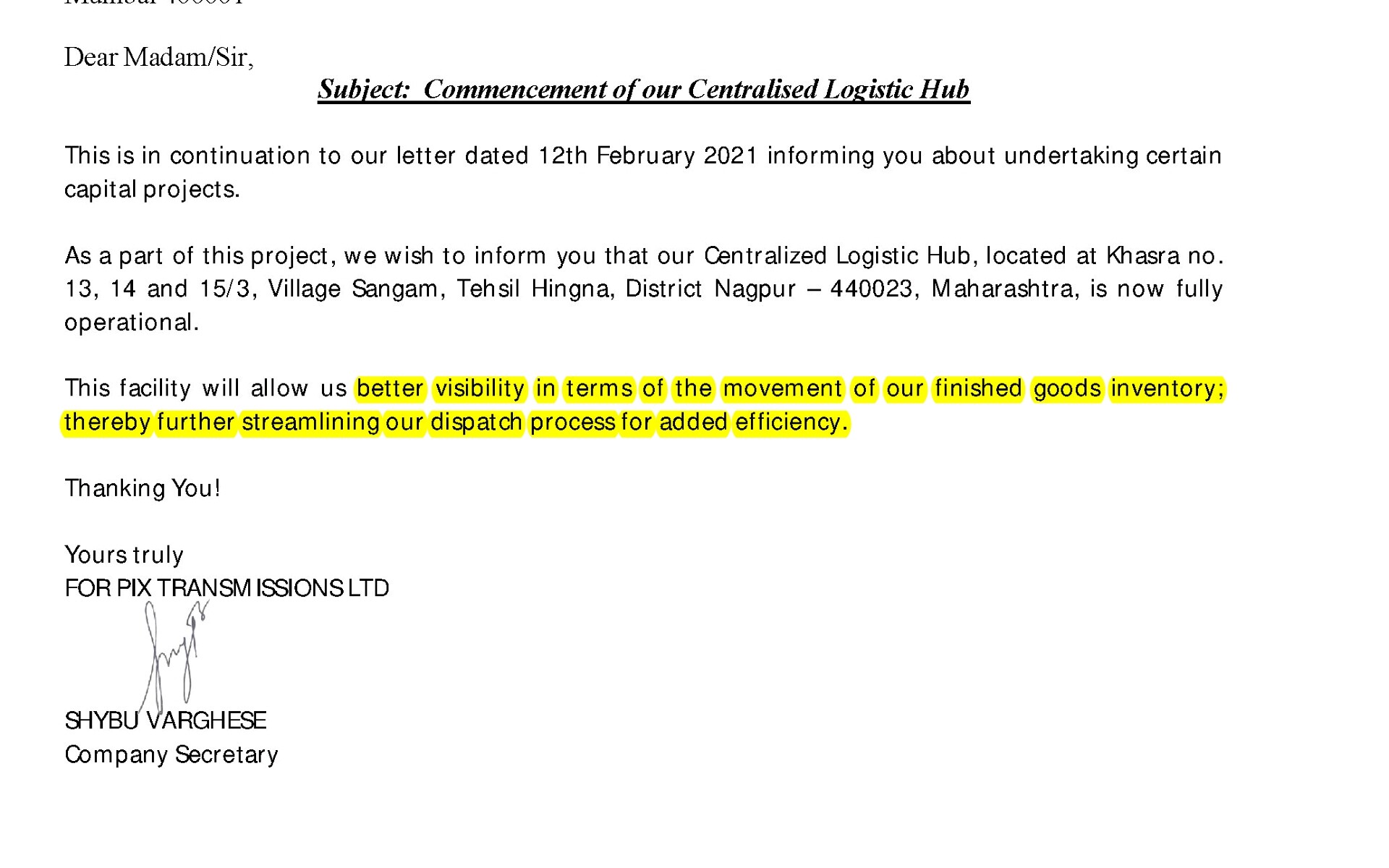

Lot has been told about inventory and working capital challenges in Pix biz model,with centralized WH commenced, it should help improve on both parameters

Some advantages being

Space optimization

Inventory count visibility real-time vis a vis backlog

high moving / high value vs low moving/low value based decision for stocking

faster turn around time for delivery ( Receivables clock starts early )

Reducing wastage

Logical would be to have warehousing systems integrate with ERP to have end to end visibility, per AR ERP implementation was done under Amrapal sethi credentials.

Q1-Q2 23 onwards it should reflect in numbers. If working capital optimization is visible ( thus cash flow), more so reasons towards re-rating.

Margin impact. margins down similar to Gates Q1 (due to Covid related supply disruption and increase in logistics cost). Gates has guided for margins inching up in coming quarter on normalization.

Overall seeing how the Q4 was volatile even for large companies, a stable execution on topline and record revenue.

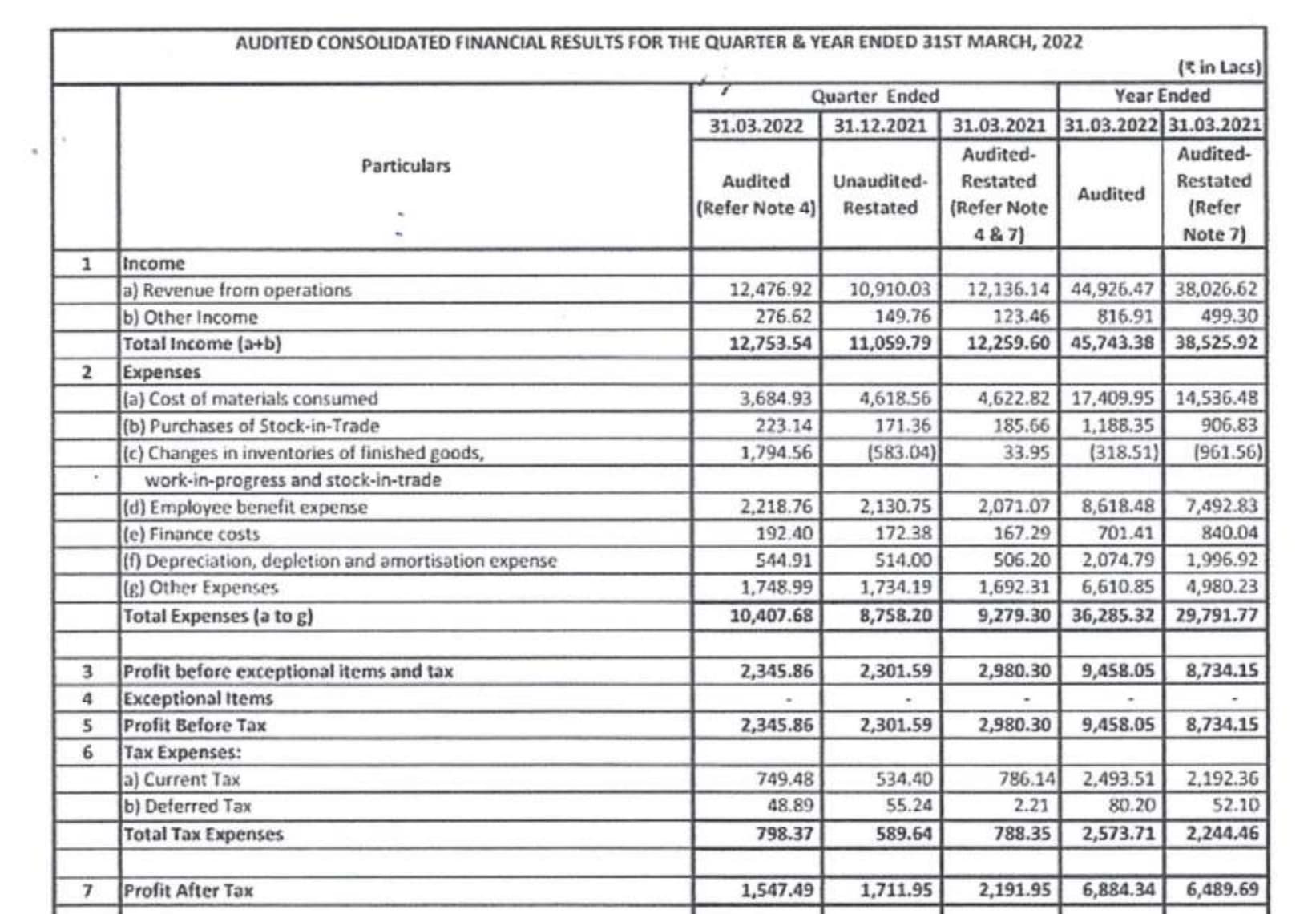

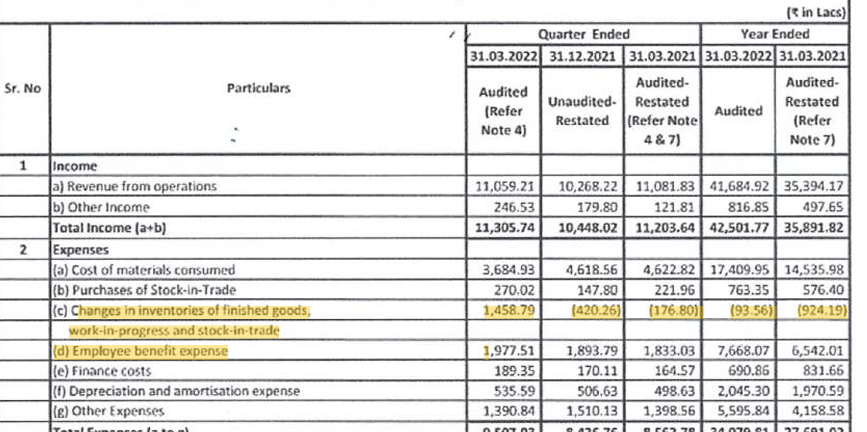

Numbers dont look encouraging to me. There is no growth in revenue on YOY basis, and there is significant hit in the margins.

This is a play on capex revival but it is not getting reflected in the numbers. And at this level, it doesn’t look undervalued.

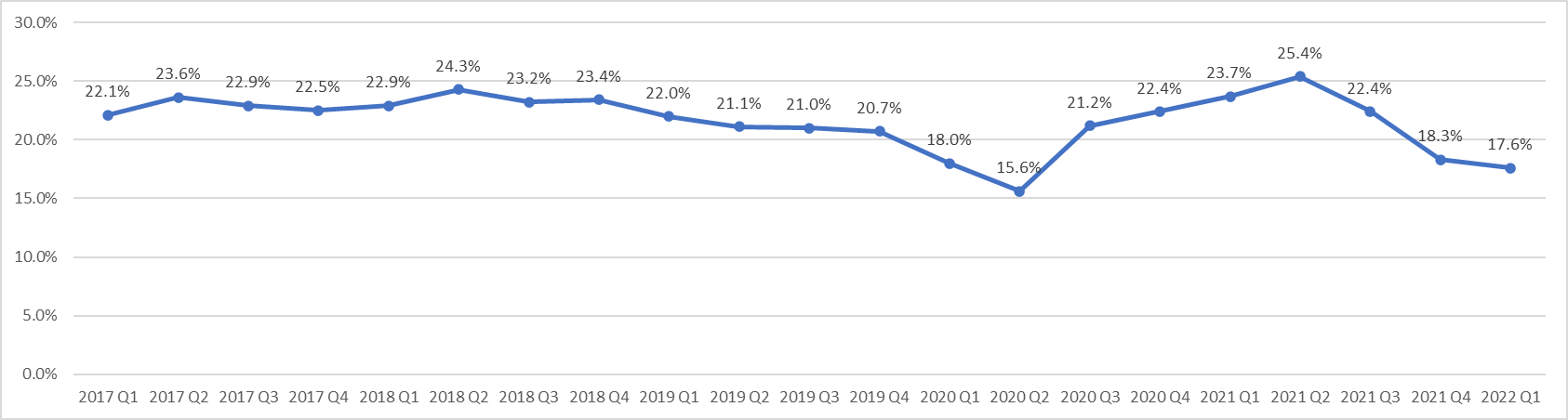

Normalised margin is around 21-22% mark, and they are currently 3-4 percentage points below the normalised margin. So Pix can also expect to see a normalised margin of 25% (without including the upside from their logistics investment).

What I find concerning is the flattish revenue growth (y-o-y) for two consecutive quarters. According to Gates, growth should revive to high single digits, and maybe Pix can grab a bit more share to grow at low double digits for the rest of the year - perhaps we won’t be seeing rapid growth of 20-25%+ this year - would be great to hear views from @sahil_vi and @RajeevJ ji.

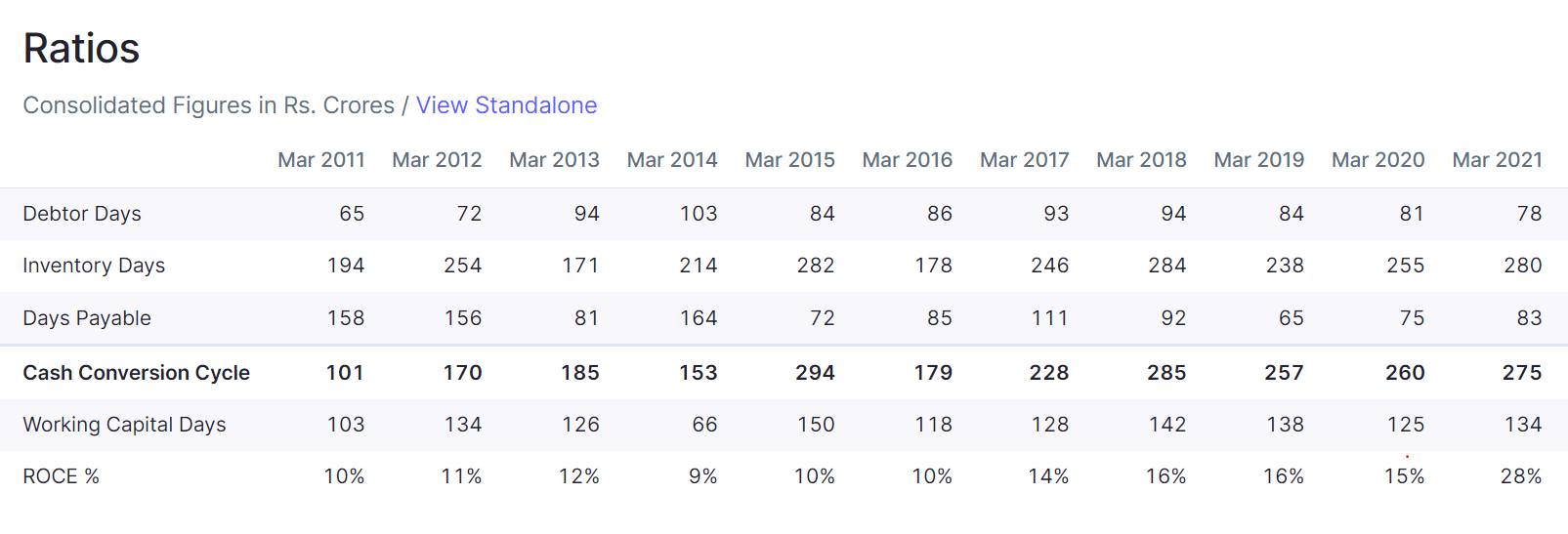

Cash Conversion cycle seems to be too high (275 day). While the Operating margins have improved over the period but the CCC have deteriorated due to high inventory days which means they are finding hard time to clear their inventory. Any thought on this would be appreciated.

Pix Q4 numbers optically seem to be a little below expectations, with margins coming under pressure. This was more or less along expected lines, with the increase in the RM prices. With RM prices usually being passed on only with a lag, the margins are expected to return to normal over the next quarter or two.

The important issue is that the story is very much intact. With the logistic hub ready & operational, the plant capacity increase is well under way. I gather that export demand is only getting better, & it is very likely that share of exports in the total sales keeps rising with each successive quarter & in a couple of years one may well see exports forming 65-70% of total sales. This increasing trend & focus on exports augers well for the Co. as the export market is many times the size of the domestic market, & once having made a break through, the stakes continue to get bigger & for an appreciable period of time.

I expect sales for the current year to be in the vicinity of 600 crs, but even if it ends the year closer to 550 crs, at current prices & with profitability returning to normal going forward, means that the stock is currently available at a multiple of around 10, which is the lowest that I can remember for quite some time.

Six months from now, the current price may appear to be quite a bargain!

FY’23

20% organic growth over FY’22(assumed) + 75% Utilisation of incremental capex.

We are taking only 75% utilisation as the capex will be done by Q1 FY’23, thus utilisation for remaining three quarters comes at 75%.

Incremental revenue from incremental capex :

75% of 60 crores at 1x asset turn: 45 crores

Total revenues: 600 crores

EBITDA margin :25%

EBITDA : 150 crores

Other income: 10 crores

Interest : 15 crores

Depreciation :25 crores

PBT: 120 crores

Tax:25%

PAT: 90 crores

Currently trading at 13 times FY’ 23 earnings which is in line with historical valuations, hence do not see great upside or downside from here.

The upside trigger here may be disproportional increase in export revenues and/or increased domestic sales on the India capex story, both of which are unknown yet and hence havent been factored into my estimates.

Views from other participants are welcome to know more.

Disclosure: Initiated Small tracking position at current levels.

Intresting developments:

Pix transmission has launched its new website, I checked it it’s quite smooth and has good insights about the products and company as a whole.

In Vision and Mission , under Mission Company mentioned to grow revenue 2x every 3 years - This might seem a bold step to put this under Mission but that’s how it is.

This transformation happening is visible on all fronts and is quite impressive considering the size of the company.

This is progressive Corporate Governance practice. Good to see disclosures improving in quantity and quality. Looking forward to the start of conference calls now

With this capex, the gap between Pix and Fenner could be bridged. However, Fenner is also doing growth+modernization capex of 45-50 Cr per annum. “The company (Fenner) is expected to incur capex of around Rs. 45-50 crore per annum for moderate expansion and routine plant modernisation” (Rating Rationale)

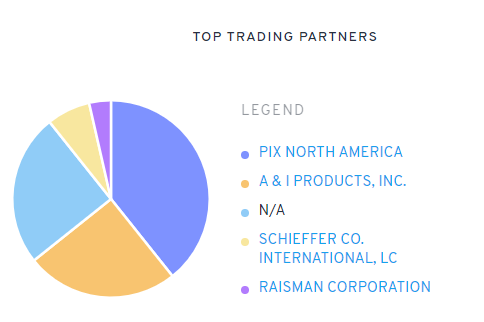

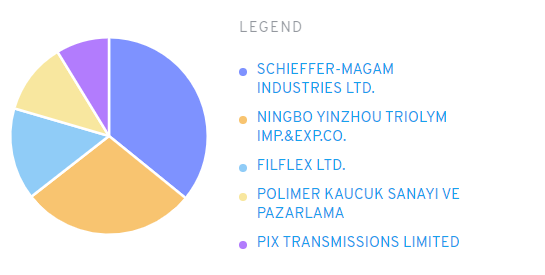

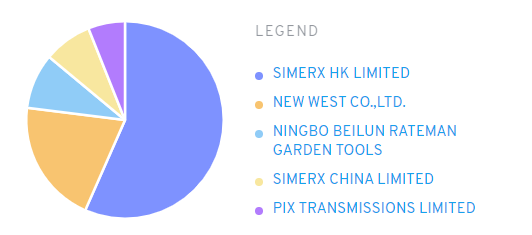

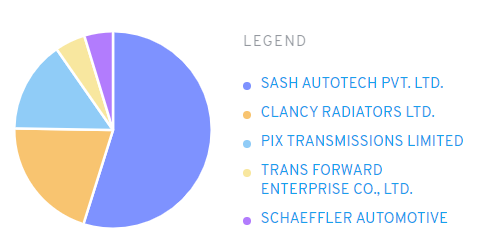

Some of their major US customers are A&I Products, Raisman, Schieffer

This was on share of XYZ customer in Pix exports. Conversely, let’s also check share of Pix in XYZ customer imports. One would expect this to be very low, since V belt is just one of the many items used in a factory. Despite this, Pix is among top 5 suppliers for each of them.

Schieffer:

Raisman:

A&I:

Of course this is a very small sample size, but to some extent we can infer that Pix would have a significant wallet share (Gates V belt doesn’t appear here since it is domestic, not imported).

Another one is Stens Corp, to whom Pix has supplied recently too