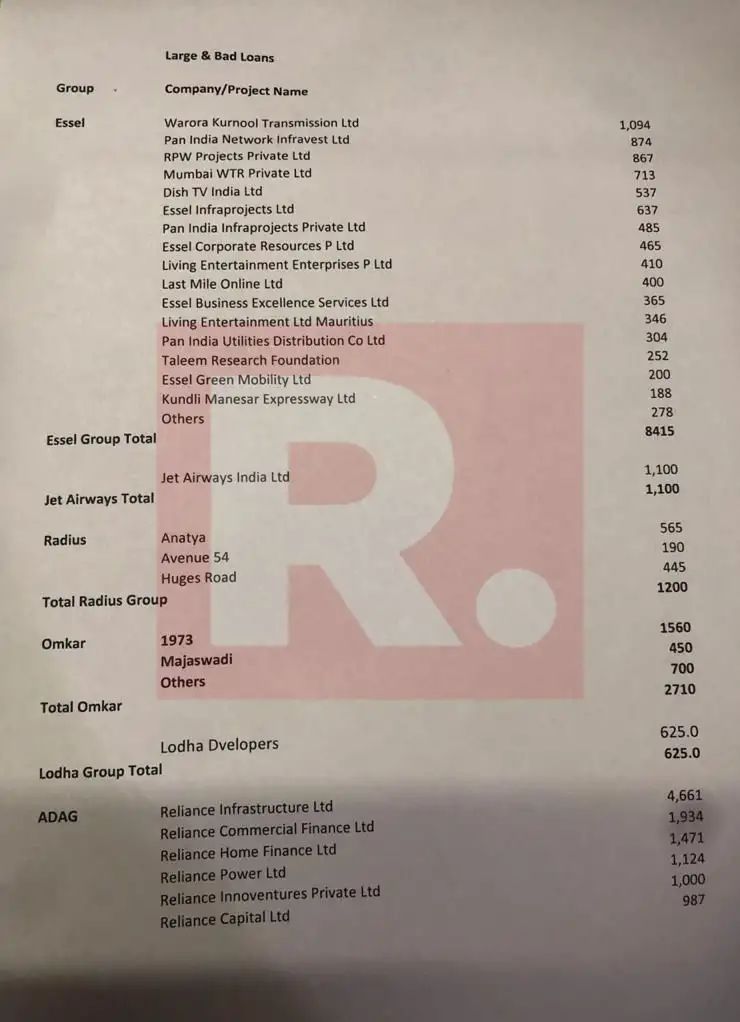

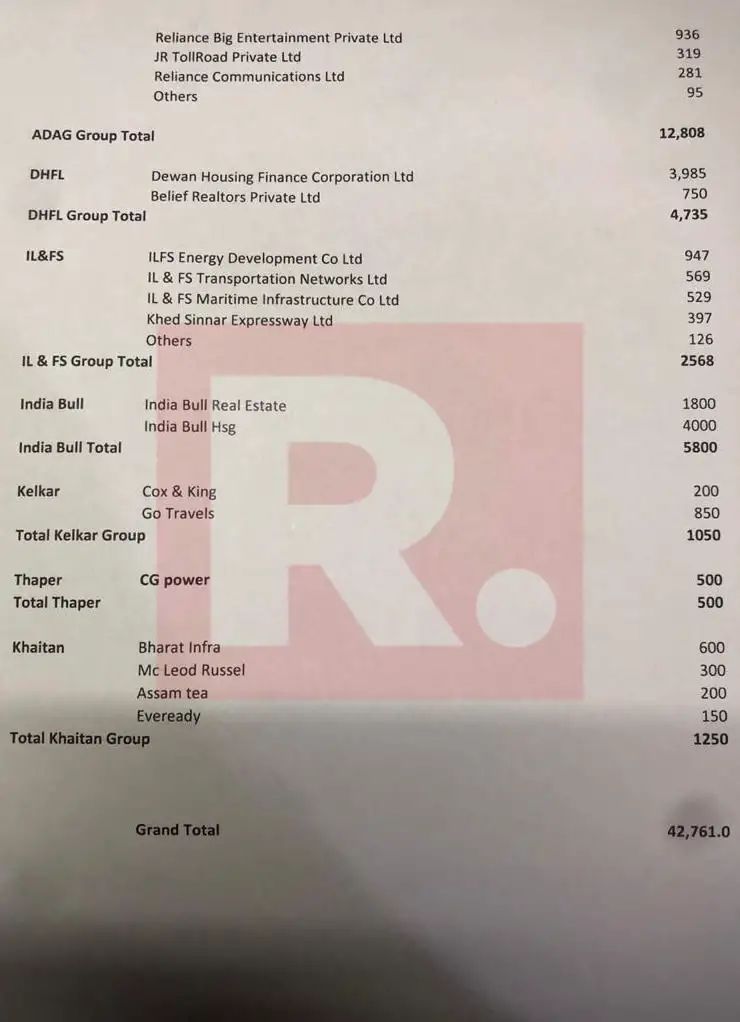

Data from the above link suggests that both Lodha Developers and Omkar Developers have defaulted on their Yes Bank loans

Piramal Enterprises has also lent to these organizations.

Can someone confirm, throw some more light?

Data from the above link suggests that both Lodha Developers and Omkar Developers have defaulted on their Yes Bank loans

Piramal Enterprises has also lent to these organizations.

Can someone confirm, throw some more light?

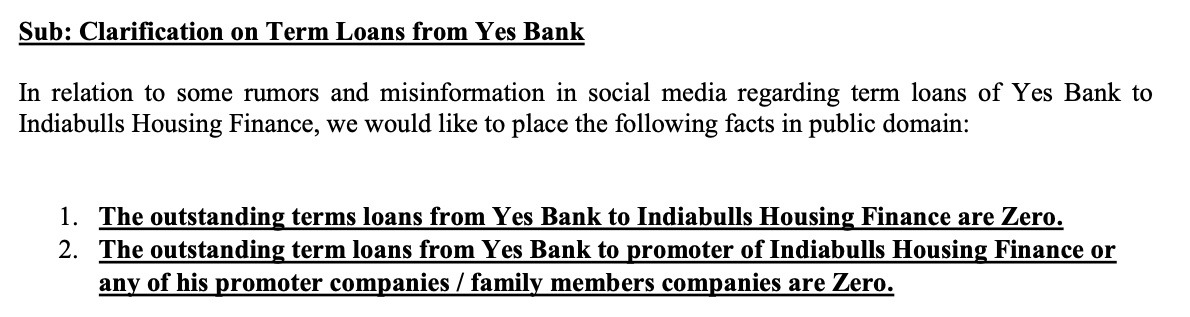

Indiabulls which is on this list has clarified as follows today:

https://www.bseindia.com/xml-data/corpfiling/AttachLive/69ff92fd-97c4-4260-a735-e533b1f26524.pdf

Have not seen any other news on Lodha defaulting. Hence would take this list with a pinch of salt right now (maybe 2 pinches since its from Republic TV)

I guess the list is EITHER large OR bad loans, and not BOTH large AND bad.

In any event, Republic TV is very avoidable.

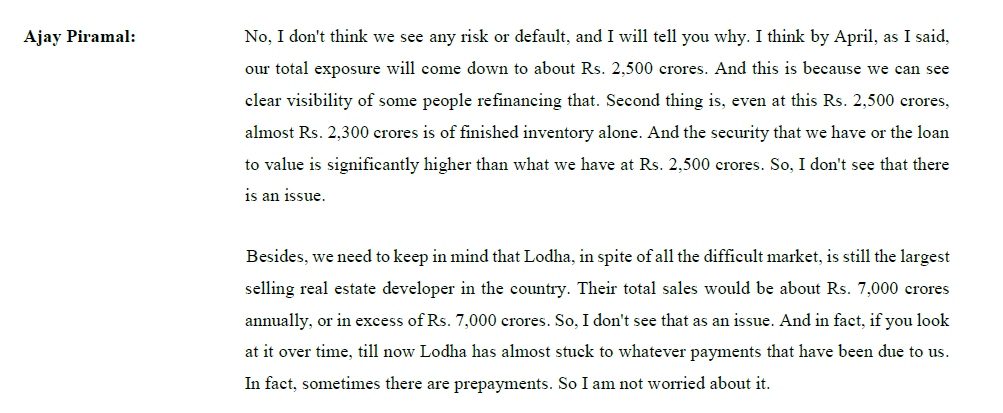

Piramal Enterprises Limited –Conference Call with Group of Investors-March 12,2020

Very timely con call (above link). Here are some of the important snippets which keeps coming up related to Lodha.

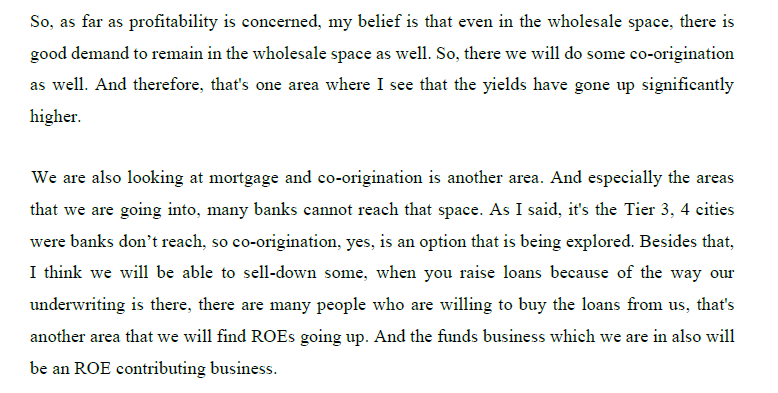

How PEL wants to improve profitability going forward.

Above quotes are Mr Piramal’s own word and one has to take it with a pinch of salf if one goes by an old adage - “Do not trust a man who is in trouble”. Not hinting that PEL is trouble, but being a wholesale funding NBFC, caution will be helpful.

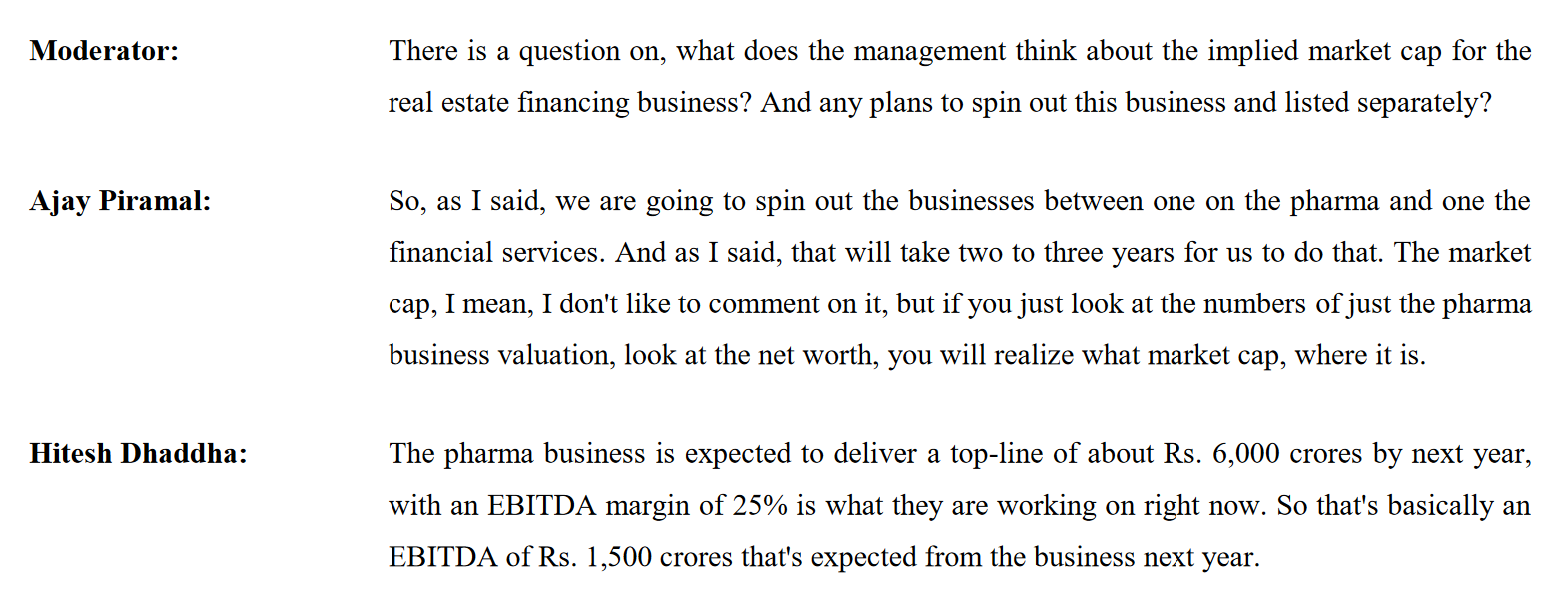

The steep correction has given an interesting opportunity. PEL market cap is approx 20,000cr. In that they have 12-13,000 cr of cash(Rights issue + CDPQ) So the remaining business of financial services + Pharma + Shriram investment is valued at 7,000-8,000 cr, which is not demanding, even if one takes into account few big accounts defaults.

Note- Invested.

I have recently started tracking Piramal post the fall. This thread has been extremely helpful!

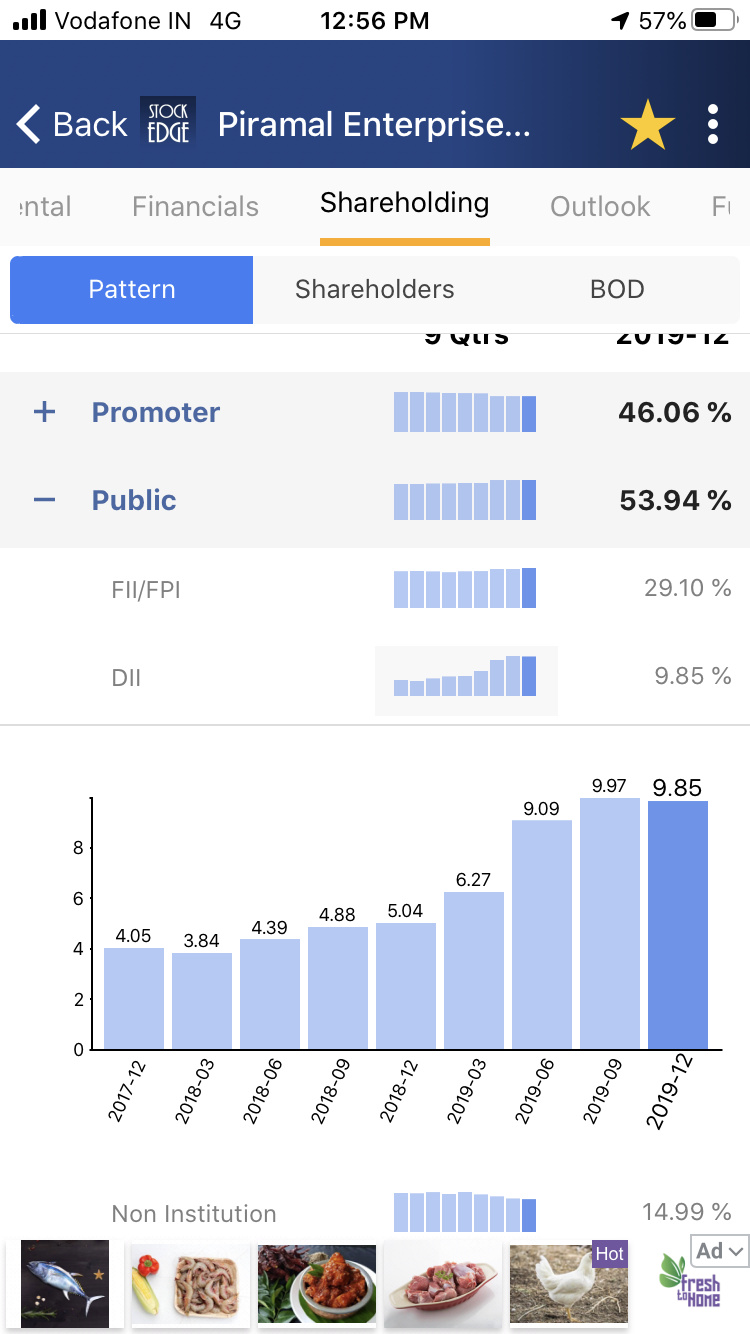

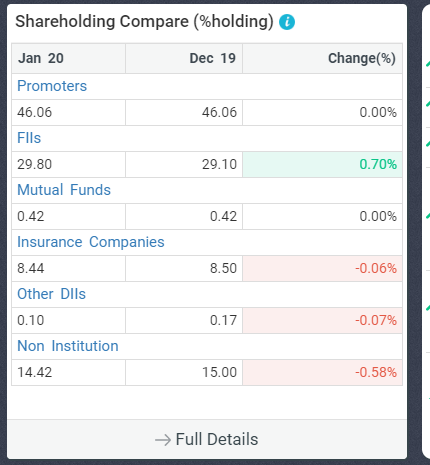

One thing that struck me was the shareholding pattern. Even though the FII holdings are high, the domestic mutual funds holding is negligible. Do we know the cause for this?

Very timely & informative call indeed. Few observations:

1 - We are not privy to their lending books so have to take their word for it and discount as appropriate.

2 - The fact that AP has put in 1700 crore personally in Jan 2020 is reassuring. I don’t see many other promoters rushing to buy their shares in the current fire sale. PEL insider trading window has been closed from 5 - 20 March due to interim dividend meeting.

3 - Correction in large HFCs in last one month: HDFC (-21%), LIC HF (-30%), PEL (-40%), PNB HF (-44%), Indiabulls HF (-47%).

My takeaway is that correction in Piramal is not totally out of context. Further Piramal is the least leveraged amongst all these players, has completed its capital raise ahead of market dislocation, and has a cushion in the form of its Pharma business which is not available to other players. Very hard to call a bottom given what’s happening globally to much better businesses, but I’m focusing on survivability currently…

Disc. Tracking

The DII is primarily driven by LIC i.e. 8.4% of total shares, while, mutual funds contribute to 0.4% of total shares.

With 20K Cr. market cap, it should sit within the mid cap universe for MFs, however, there has been limited uptake by mutual funds.

dont know what is aligning with PEL…maybe it is pure of short selling giving the economic downturn happening in the world and shutdown of mumbai…its very sad to see what is touted as next bluechip fall from the grace of 3300 to 670

PS learned the lesson hard way never have too much allocation if u have still high conviction

dont know what to do with 2K@2400

The market cap of piramal is is almost same as the amount of money raised by selling shriram investment + data analytics + rights issue . This is just the liquidity raised recently .

if we assume that NPA of piramal is not going to be so huge, Piramal enterprise is trading at cheap valuations.

Hold on sir. Bad time to sell now.

Don’t even think of selling it, when things are good future 10 yrs profits are priced in, during crisis future 10 yr loses are priced in today only. Reduce the exposure when they separate the Pharma & Financial business, but again that will be a completely different situation and needs thinking …for now hold the urge of selling don’t convert notional losses into permanent loss.

Disclosure - invested & largest allocation in pf

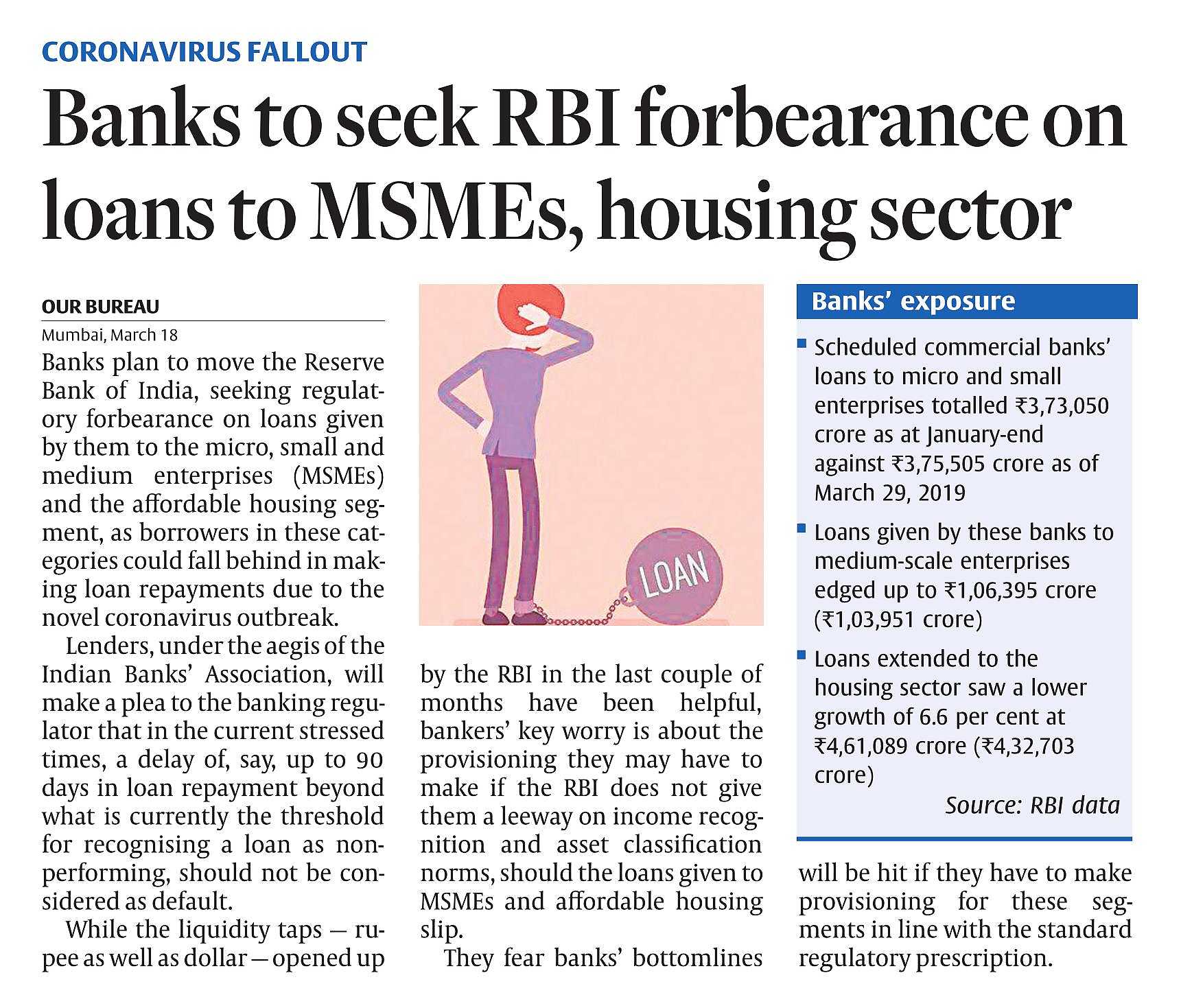

Next two quarters will be disastrous for financial institutions. In Australia, Big 4 banks are giving 6 month’s moratorium on housing loans. Government can also provide support if needed to financial institutions. However I think India’s financial position is not strong enough to provide any meaningful support. Hard to find a bottom here for financial institutions. It all depends on which ones survive at the end of this.

Banks have already approached the Reserve bank last week seeking regulatory forbearance,the Corona issue is likely to impact all lenders across the board.

This is definitely very interesting from a valuation perspective. I was looking to take a position but was driven away by the size of the stuck real-estate loan portfolio, which is 60K Cr as per the last annual report. The net worth claimed by Pirmal in the last conference call is, 33K Cr. So almost 2x the networth is stuck in real-estate loans to developers, with luxury apartments/properties as collateral. It’s been a few years and Piramal has not been able to exit these.

We are able to easily see the amount of cash generated and infused recently. And the cash the pharma business generates. We just aren’t able to see how old/rotten/non-performing the real-estate PF has gotten. Any pointers here on the scope of the issue would be helpful for new-comers to this scrip like me, to get more confidence.

I know its difficult for us to book 75% losses in such situations. Just sharing what I would have done if I am holding such positions.

3 approaches regarding same

2.Sell Completely book losses and move money into good banks HDFC/KOTAK/CIty union or all three diversified thus booking just 40% of my loses( PEL has fallen 70% and these banks around 40% from high.) as currently its difficult for NBFC too survive this triple finanacial+Healthcare+liquidity crisis

.

3.If can’t convince myself do above two options will just sell PEL for 1 day to give myself clear new perspective and then decide whether to buy again/hold cash/buy other fallen stocks.

I am holding Piramal from 550 levels and my cost average is ~Rs 1300 and it was 10% of my portfolio at purchase cost. Current price is attractive in my view and I have initiated purchase in very small quantities. Few reasons for purchase -

The company is assumed to be one of the most ethical company and expectation is there are no skeletons in cupboard.

Mr. Piramal is good capital allocator. He is currently sitting on vast amount of cash. He may decide to do some acquisitions at current distressed valuations and turn them around quickly.

Pharma business is performing and growing well. It has very good record of passing FDA inspections. So pharma provides the back-stop on valuation.

Company has stressed that they have enough cover for loan against real estate and current crisis may force real estate players to aggressively liquidate inventory to generate cash and in turn deleverage.

Disclosure - As I am holding the stock my views are biased.

A couple of interesting reads over the weekend:

https://news.asksmarty.in/brookfield-may-take-over-rs-1500-crore-piramal-loan-to-bengaluru-realtor/