Thanks for sharing, good write up with good insights

1 Like

Hi,

Thank you for sharing these articles.

It seems piramal is quite cheap now.

Quoting Beowulf Capital’s article.

“The market is today valuing the INR 34K crores worth of assets at less than INR 10K Crores. It can also be reasonably shown that the INR 2.5K Crores to Lodha is reasonably safe. So, the market is valuing close to INR 31K crores of others at INR 7.5K crores.”

Thanks,

Deb

One thing to take a note is, out of a 60K Cr loan book, selling 1.5K Cr loan to Brookfield says either the price wasn’t right or they did not want the other loans. They hold $1B in distressed real estate assets – so having gone through your book, buying just a tiny portion of your assets mean, the majority wasn’t the right fit. Either too risky or too expensive.

1 Like

they regularly sell their loan books and earn fee income. this is their strategy.

disclosure: holding

CARE affirms rating of Piramal Enterprises Limited https://www.equitybulls.com/admin/news2006/news_det.asp?id=264746

1 Like

Hi All,

Price movements of a stock in a short span/near term is mostly related to liquidity and sentiments.And the price movement of a stock in long run is a reflection of the fundamentals and growth of the company.

Having said that the recent stock movement seems unwarranted. PEL came from 2500 levels to 700 odd levels.Around 2/3rd of the market company gone.And on Thursday It went 50% higher breaching the upper ckt multiple times and finally setting 20% higher.Even on friday it went 20% higher(again breaching the ckt levels couple of times) and finally settled 5% higher.

We all know how sound the management is.Its Pharma Business is doing good.the only problem is with lending sector,but Mr. Piramal has managed the things pretty good,In fact better than many players in the same field.So why the stock price is behaving so irrationally?

Thanks,

Deb

[quote=“babu44b, post:1713, topic:324”]The answer to your question lies in your first paragraph copied below. Overthinking is not good let the dust settle down…few players will survive this rest will thrive ![]()

Price movements of a stock in a short span/near term is mostly related to liquidity and sentiments.And the price movement of a stock in long run is a reflection of the fundamentals and growth of the company.

3 Likes

I am very cautious when rating agency gives rating to NBFC/Banks. CARE is the worst.

Just one example of CARE Rating on Yes bank (before YES Bank fiasco) - https://www.yesbank.in/media/press-releases/yes-bank-upgraded-to-aaa-with-stable-outlook-by-care-ratings

When NBFC/Bank speak more on credit rating during concall, be careful! Because fees to credit rating agency is paid by the company who want to get rated!!

1 Like

While rating agency ratings need to be taken with more than a pinch of salt,i think comparison of PEL with Yes Bank is not apt.

Globally the reputation of rating agencies had taken a huge hit during the 2008 Financial crisis,a similar thing happened here in August 2018 when ILFS(rated AAA) defaulted and the subsequent DHFL saga.

Ever since then rating agencies in India have been under a lot of pressure and while things may go back to the “shop a rating” days that were common prior to this,it may take a few years for things to become business as usual.

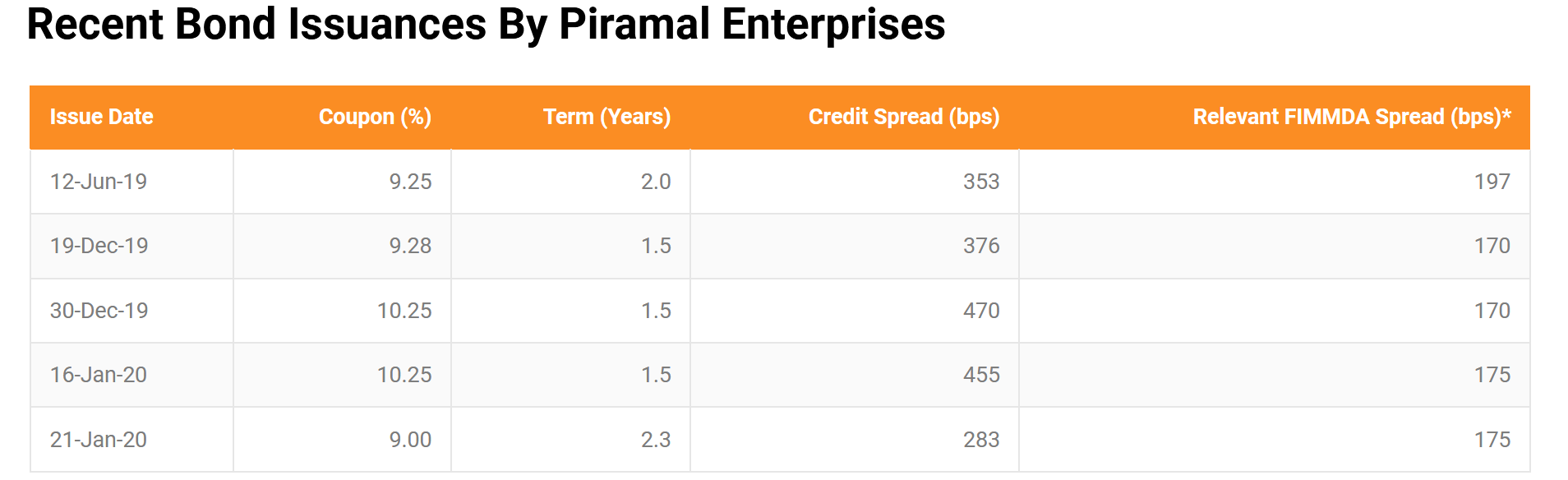

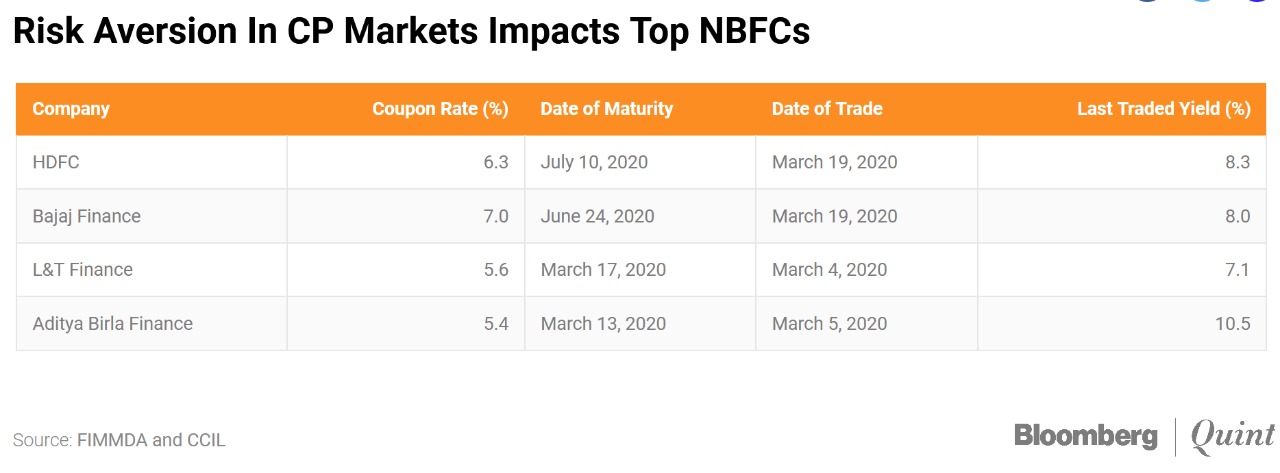

A better marker than ratings is the how the borrowing costs of the company are trending,that tends to signal building of stress or the easing of the same.

1 Like

Citi Research says HDFC and Bajaj Finance are relatively better positioned to come out stronger from this crisis. The global research house has upgraded Bajaj Finance (target Rs 3,900), Aavas Financiers (Rs 1240) and Piramal Enterprises (Rs 1,130) to ‘buy’ ratings from ‘neutral,’ but have cut price targets for all three.

how this selling of 20% is value addition for existing shareholders?

the proceeding will go to retire debt mostly or will they buy some formulations or any pharma business?

It will help in price discovery of pharma business and eventually would get fetch decent valuation during spin-off

1 Like

According to past concalls by management, they want to infuse the amount for growth funding for pharma business (maybe for inorganic acquisitions). Also they want to demerge the pharma business and make them debt-free (probably through internal accruals).

Their pharma business valued at 18000 cr of which they will divest 20 percent. Add Shriram stake 4000 crores . Total 22000 crores . Market cap is 22000 crores . Which means their financial services business is worth 0

Am I missing something here ? Here is a mix of pharma and a distressed nbfc well capitalized . Fallen from 3200 to 900 . So Piramal valuation is low. They raised good equity funds in last 6 months . Q1 onwards their interest costs will come down as they pay off higher rate loans. Another good news expected is launch of consumer lending business via Reliance Jio/Retail/Ecommerce . They will try and replicate Bajaj with Reliance customers .

Dhiren,

You are missing NPAs this business can have which can wipe out their equity. You are also missing debt on their books. Probably you might want to see few research reports on calculation of enterprise value and market cap of these businesses.

7 Likes

Agreed. Their loan book is 61k cr and their debt is 41kcr. So 20kcr of equity. Do you expect 30% NPA?? Also you are missing LTV ratio i. e. 2x. So you are giving zero value to the collateral.

Again, it doesn’t work like that.

Firstly LTV is based on historical valuations. Now, the asset prices will take hit so we have to lower this. Secondly, many collateral is linked with underlying cashflows which can dry due to various reasons we all know.

Third, assume that they default on loans and Piramal procures the collateral, do whatever, like finishing construction, JV or outright sale etc. >> all this takes time and your money is stuck. So, loan growth takes a hit.

Fourth, new loan disbursements will dry significantly (a) due to lack of demand (b) conservative approach from Piramal…

Fifth, there will be asset-liability mismatch in terms of cashflows, as they might not get all the money from disbursed loans but they have to keep repaying deposits/bank loans they have taken.

Now, consumer loans which was silver lining for incremental growth has also taken beating in short to medium term due to external environment.

Now question to investors…why should this not trade at discount to book value if there is NPA problems coupled with lack of growth visibility??

Disclosure: No position; Not a buy/sell recommendation;

9 Likes

- Asset price may take a hit of 10-20% according to me.

- i agree your point on cashflows and liquidity.

Think they have enough liquidity.

My point is how can be we so sure about the NPAs. One should get 360° view about the risk management policy as well as the solvency of the borrowers. If this happens i think the overall banking sector will get affected when you are lending to tier 1 developers.

Also coming to consumer finance business, when the growth of India is affected then how can we expect a company to outperform.

Disc. Not invested. Not a buy call.

Personal view: I think the consumer finance sector is much under penetrated. I am of the view that the sector will see some new market coming after the pandemic as there will be issues relating to liquidity rather than solvency in short run.

1 Like