As per my understanding, there is no CRR requirement on NBFC’s as it is for banks.

Takeaways from the Extra-Ordinary General Meeting of Piramal Enterprises held today.

Defending the company’s decision to sell the DRG subsidiary, Ajay Piramal said PEL was getting a good value at 5 X sales and 19 X EBITDA. DRG was acquired for US $ 635 m in 2012 (equity plus debt) and is being sold for US $ 950 million. The depreciation of the rupee in the past eight years have ensured that the Rs 3400 cr investment appreciated to Rs 6750 crore.

Responding to shareholders’ queries, Piramal said the DRG subsidiary is housed in a Dutch holding company and the proceeds after payment of debt would be routed to India.

Ajay Piramal was non-committal about declaring any special or interim dividend. He told shareholders that the company distributed 40 per cent of its profits as dividends.

Responding to share-holders queries about the fresh rights issue, Piramal said there were fresh opportunities in this market and cash in the balance sheet would make the company strong. He clarified that the Pharma business was not being sold. It will have a turnover of

Rs 5000 cr. "Both our lending book and Piramal Healthcare will continue to grow.

disclosure: holding

7 Likes

2 Likes

I can’t read the article as it is premium, can any one pls report what is the latest cost of borrowing for Piramal from article or any other source.

Heard that Manappuram latest borrowing rate is 6.12 % for 90 days CP.

Puneet

CPs of short tenures have much lower interest rates. Companies lending to infra sectors for long periods were relying on short-term CPs which resulted in a major asset-liability mis-match. Manapuram is borrowing on short tenures and could also be lending for short tenures - three to six months since it is a gold loan company.

Cannot compare Manapuram with Piramal.

disclosure: holding Piramal. no holdings in Manapuram

Piramal cutting down Retail Real Estate finance Business(Construction Finance Division)

Adding Teams for Retail Business (Consumer Business)

Interesting time ahead.

Mr Ajay Piramal is shrewd, realistic and competent Promoter.

Such type of business transformation takes time. Take the case of IDFC first for example. But diversification is indeed a good step for long term sustainability.

It’s true that Transformations takes times, but Piramal already started the things, aiming Retail dominated Loan Book.

Better Late than never.

Q3 earnings call - management messages:

• Addressed systemic liquidity issues by adding over Rs. 14,000 crore to the balance sheet – 1) CDPQ Rs. 1,750 crore, 2) Rights Issue Rs. 3,650 crore, 3) DRG sale Rs. 6,750 crore and 4) Shriram Tran Fin Rs. 2,300 crore

• Raised long term funds of Rs. 43,000 crore to address previous asset-liability gaps – now bank borrowing is 67% of liabilities, CP’s are negligible – also looking at foreign debt/ECB’s as liability sources

• Over the last few quarters, re-financed loans of Rs. 10,000 crore at par and recently raised Rs. 1,900 crore at 9% p.a.

• Current book value is Rs. 34,000 crore on pro forma basis and debt to equity is only 1.2X – creating scope for balance sheet expansion through organic and inorganic opportunities

• Focus on diversifying from wholesale lending to a balanced assets portfolio – 1) in home loans, competitive intensity in targeted segments has reduced, 2) looking to launch consumer finance on a tech-based platform by aligning with a large telecom operator

• Large exposures being reduced – 1) top 20 exposures have reduced by Rs. 3,500 crore over the last six months, 2) currently, only one exposure exceeds 15% of net worth – and by the end of Q4, #1 and #2 exposures expected to be lower than 12% and 7% of net worth

• Pursuing co-lending opportunities with PSU banks, pension funds, foreign banks etc creating fee income and ROE upsides

• Within wholesale lending, yield has increased from 13.4% to 14.9% in the last five quarters

• In the pharma business, 90% of revenues are from global pharma through contract development/manufacturing (CDMO) and complex hospital generics and 75% of global pharma is in regulated markets; the balance is in India consumer healthcare – overall, a differentiated business model that has delivered solid, consistent performance, despite the industry facing numerous challenges such as generic pricing pressure, buyer consolidation and increased US FDA scrutiny

• The pharma business has cleared 36 US FDA inspections, 162 other regulatory inspections and almost 1,100 customer audits since FY12, without any OAI or production stoppages

• CDMO business provides integrated services to execute early/late stage development with increasing share of innovative products in the portfolio based on capabilities in niche complex areas such as antibody drug conjugates, high potency API’s and sterile injectables – and further brownfield expansion is planned

• Complex Hospital Generics business – increasing market share in inhalation anesthesia and adding new products

• Pharma business planned to be under 100% subsidiary, funds to be raised and eventual separate listing for financial services and pharma; also evaluating re-entry into domestic formations through an acquisition

6 Likes

https://ibgnews.com/sourav-ganguly-new-face-for-polycrol/

Piramal getting aggressive in marketing OTC products…

Hi All,

I found 3 efficiency parameters which are improving for piramal enterprises.And I am unable to find reason for such drastic improvement in Working capital days.

1-> Working Capital days - In 2015 it was 53 days and in 2019 it is negative.gradually decreasing every year.As per my understanding the less Working capital days the more good the business is.and negative means business is getting paid before they delivered the products.ao what significant changes in the business model happened that lead to this significant change??

2- Days of inventory and Days of receivables are also decreasing which means finished goods are getting sold quicker than earlier and business is getting its payments from customers quicker than earlier also.

Anyone please guide by providing more details regarding these improvements.

Thanks,

Deb

1 Like

My last post was tagged for Moderation as I had placed a contrary view that price of Piramal may fall below Right Issue price, hence I did not participate in the right issue and the basis was

-

Retail holdings are never sticky, an increase in supply (free float) will bring the price down as many were stuck at a higher price level.

-

Such investors rush to get out once the price is averaged out.

The price of Piramal did fall but not upto the right issue price, my thesis was partially right.

Nonetheless, the point I am trying to make and highlight is we are rarely open to contrary views, our thinking is biased around what we already know, if it matches it is accepted otherwise ![]() I could see nearly 10 posts in a day on how to apply for Right Issues and now when the price is below the right issue price nobody wants to discuss anything. Contrary views helps everyone and personally i have benefited a lot.

I could see nearly 10 posts in a day on how to apply for Right Issues and now when the price is below the right issue price nobody wants to discuss anything. Contrary views helps everyone and personally i have benefited a lot.

However, the main reason for righting this post is,

-

I think that the market is not valuing the Financial business of Piramal appropriately and it is grossly undervalued. I am not a valuation guy and would need the help from fellow members if my understanding is correct.

-

At 1300 price it is valued for Pharma business ONLY i bet on the higher side.

-

Pharma business is doing well and will naturally act like a cushion and will not allow prices to fall further (Not below 1000)

-

Good Dividend will also act like cushion.

-

All the recent moves made by Ajay Piramal looks very rational/logical and most importantly he is executing whatever he is saying and not merely talking.

My only worry is their Business model is not set and are still prone to changing/modifying/correcting based on their mistakes and learnings. So the business model is not tried and tested and stood the test of time. This is the biggest risk IMHO.

Also, Yes Bank has given a very good opportunity to get into Banks and other financials, read somewhere in twitter today “In Bear Markets shares return to their Rightful Owners” ![]()

Disclosure - My views are biased, as Piramal now is my biggest holding in PF, Also i have broken all my allocation principals and my PF is skewed and concentrated towards financials Piramal being the largest chunk.

Thank you ![]()

11 Likes

As you have mentioned that contrary views are welcome, I would like to compare this stock with PNBHF which is falling as if there is no bottom. PNBHF management was compared to the likes of HDFC as the best in housing finance. The problem is in the sector rather than the management. PNBHF is perceived risky because of their higher allocation to developers (at 30%). How risky does that make Piramal with 100% allocation to developers? The argument that if the developer gets in to trouble, piramal can finish the project doesn’t hold water as even the projects of best developers are struck barring a couple like Godrej. Developer finance is very risky and if a project is stalled for 3 years, half of its value will erode in interest rates alone. In that, Piramal would fund high risk projects as evident from their high cost of funds. If a diversified bank with access to low cost of fund can fail (Yes Bank) because of its higher risk loan book, Piramal will not be an exception. Only positive is the high tier 1 capital which gives it the ability to write off non-performing loans. While pharma holds value and is much safer, will it be saved if finance falls. The signs from management so far is they will sacrifice pharma for finance.

6 Likes

Developer loans are inherently risky what you say is correct, but there is a big “IF” as it may or may not happen. Good news and price rarely come together, but i do not see any systematic risk in their financial business, which may break their backbone, NPA’s may rise given the bad situation prevailing around but every passing month it is coming out of the problem as it is continuously recovering from developers. We can go on and on discussing this but only time will reveal whats in store.

Mean while smart money is moving into the Piramal in these turbulent times ![]()

Regards ![]()

1 Like

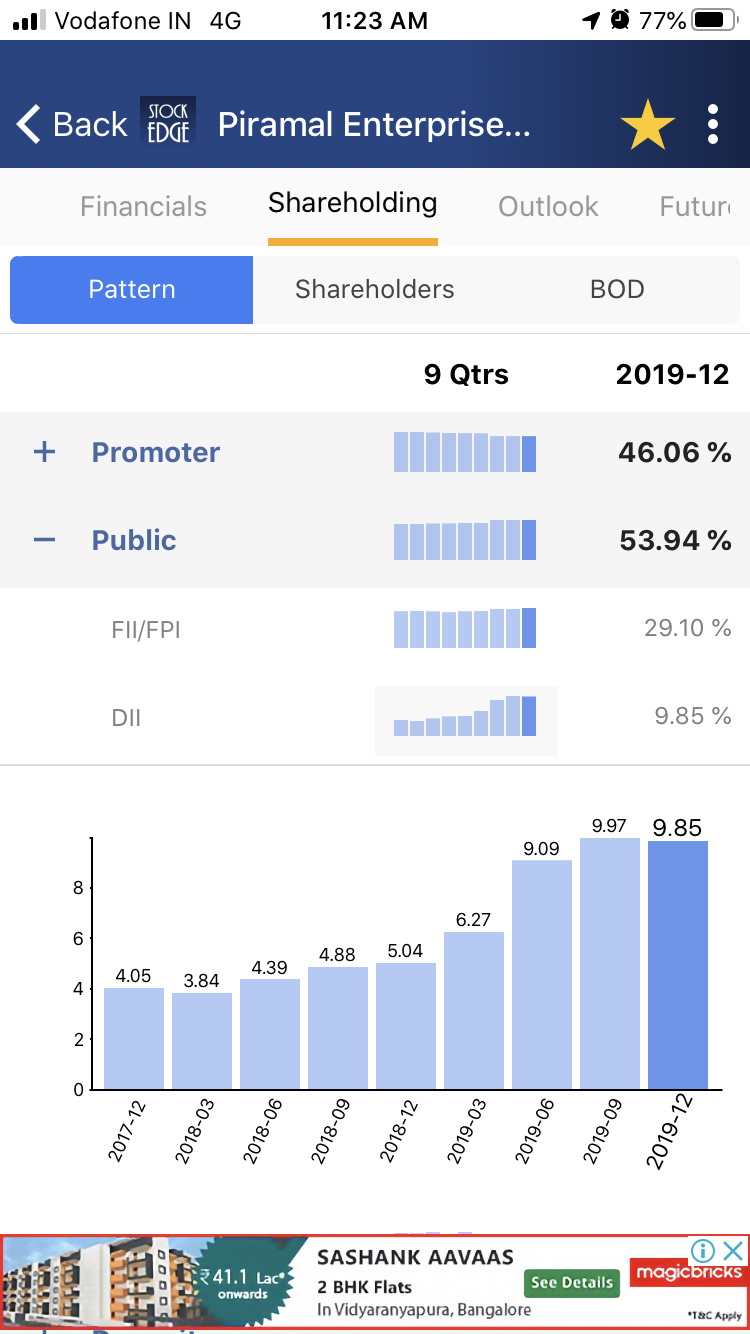

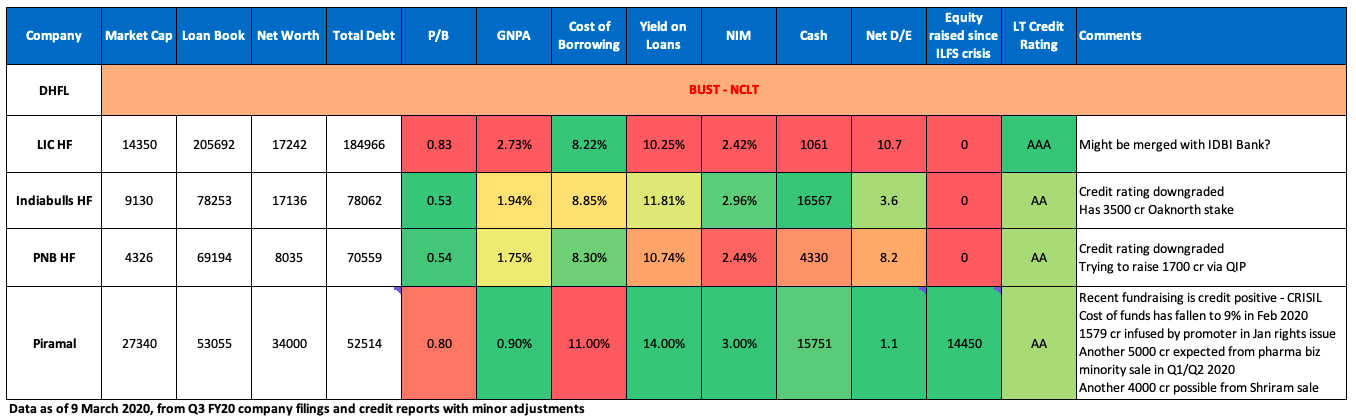

Comparison of the 5 large HFCs (excluding HDFC) I did for learning purpose.

Disc. Tracking position in PEL

8 Likes

His stake sale in Shriram capital is almost done. Should see the announcement soon. That will add further cash in his kitty.

Any inkling about the amount ?

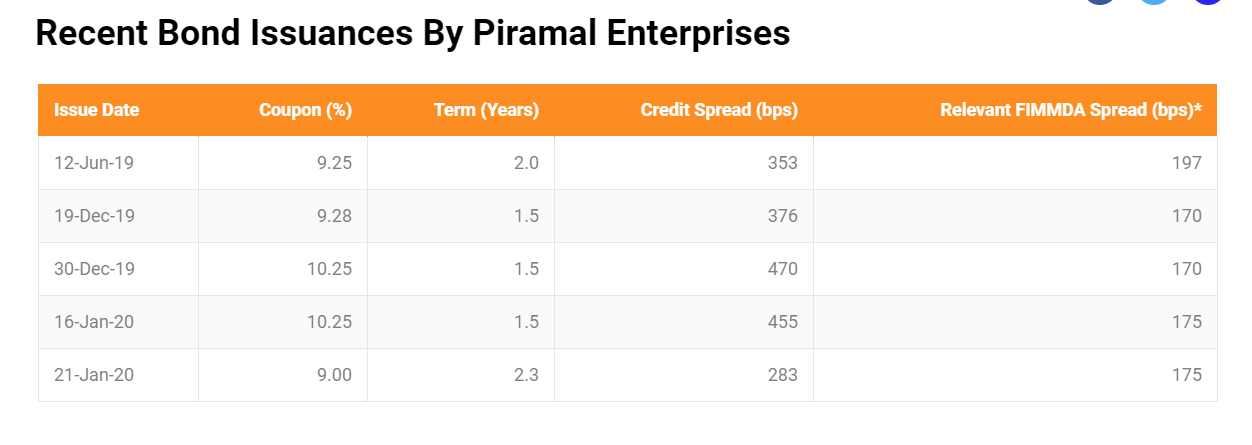

Lodha managed to beat the debt clock on these offshore bonds.

Background:

1 Like