Some basic notes from the recent conf call (Discl - decently long here from much lower levels and def biased)

Indian banks and NBFC’s are strong and need to be growing faster for Bharat to grow.

Q2 Perf in line with management guidance and expectations.

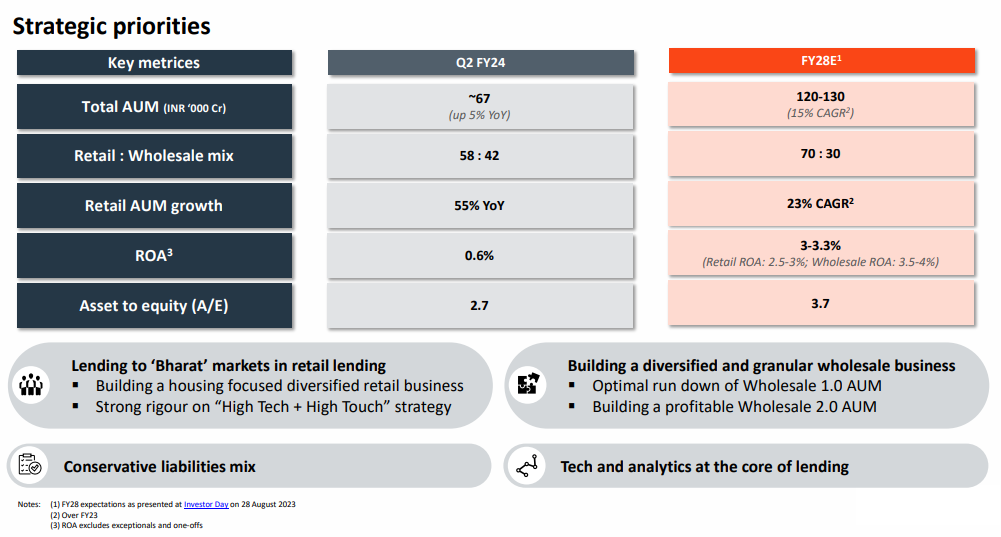

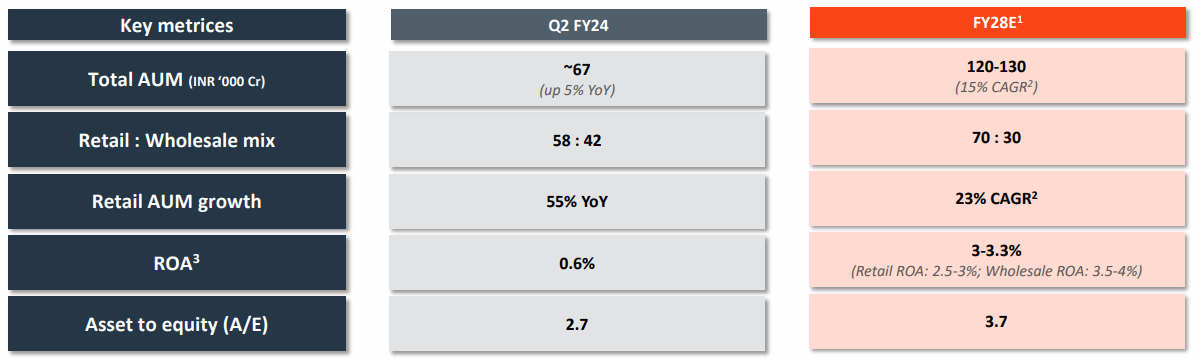

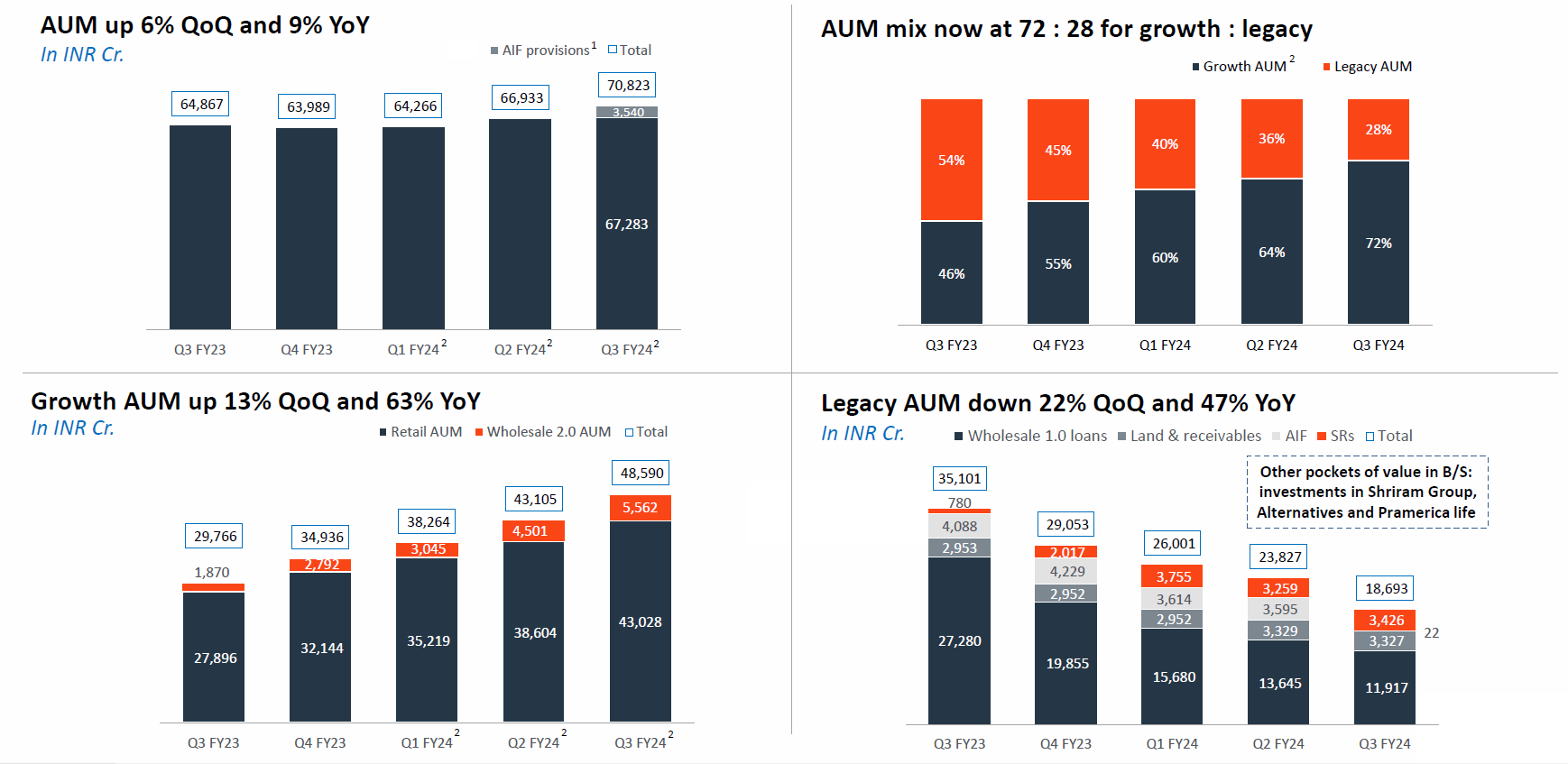

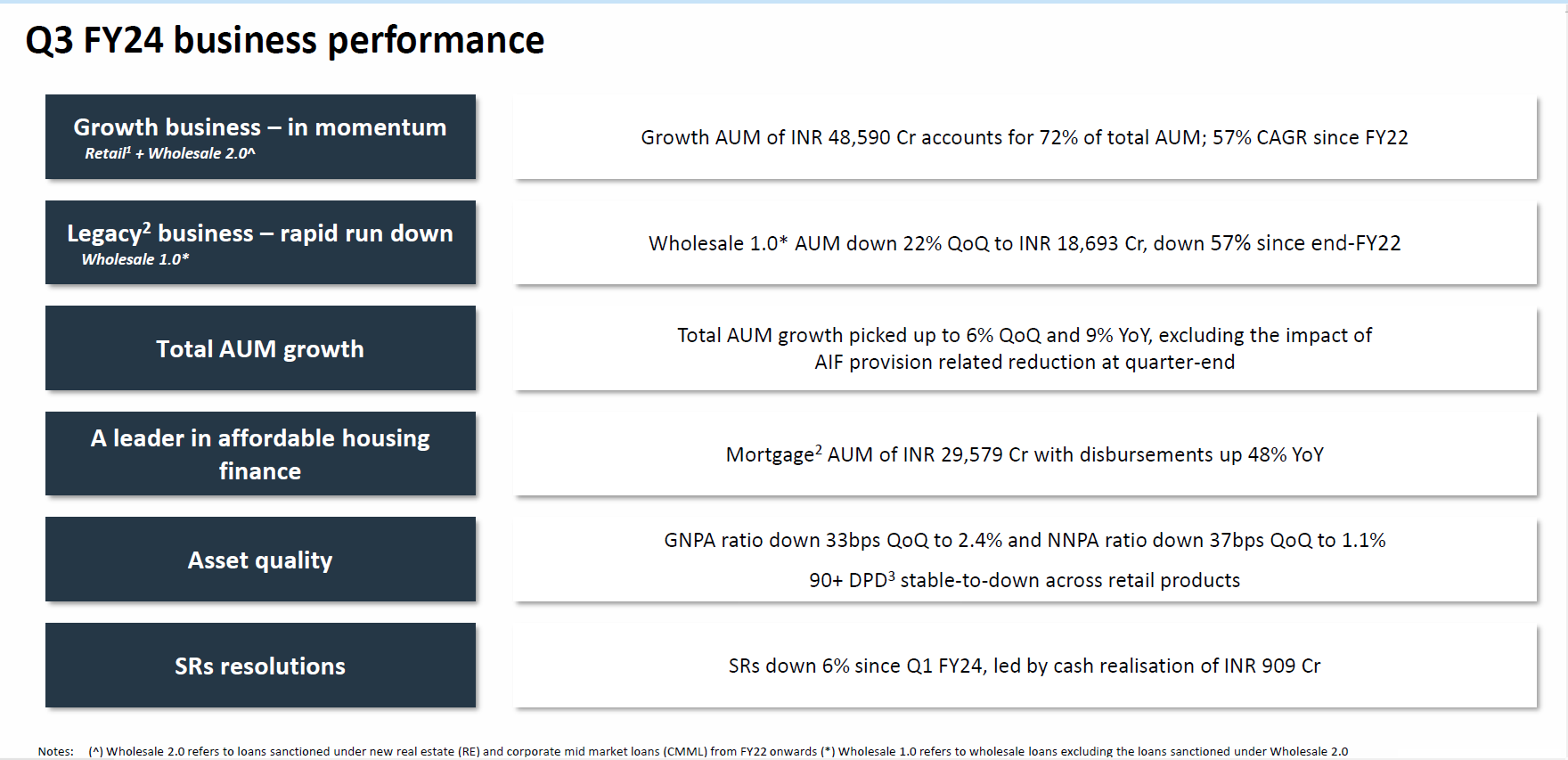

AUM up 5% YoY & up 4% QoQ (a metric I am watching and expecting to grow) apprx 67K Cr -

AUM Stable and growing despite massive changes in underlying book…

Improved Retail : Wholesale mix now at 58:42 (vs 33:67 at end-FY22)

Wholesale 1.0(Legacy) AUM reduced by 33% YoY

GNPA’s down QoQ

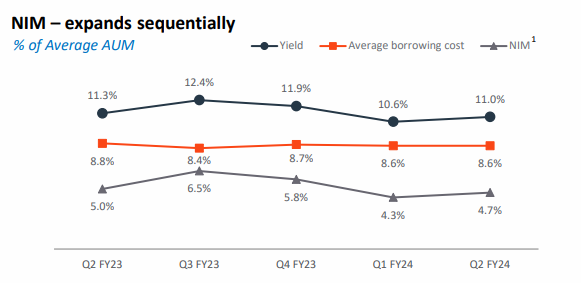

NIM Expansion - Modest

Housing loan sweet spot - INR 18 lacs

Housing disbursements grew by 309% YoY - 60% LTV - 11.2% Yield - 90+ Day Delinquency 0.4%

3.6 Mm Customers - 1.1 Mm Active

23% of retail is Unsecured. De-growing unsecured thru tighter credit standards.

Management Goals -

120K Aum by FY28 - 15% CAGR

Retail ROA: 2.5-3%; Wholesale ROA: 3.5-4%

Plan to expand to 500-600 branches

Legacy

Stage 1 (Loans/NCDs)1 AUM of INR 17,381 Cr with an average yield of 12%

Long Bias Assumptions -

Management gets to 50% of target

Cost to Income continues trending down

NIM’s continue trending higher.

Cost of borrowing moderates further.

RR is tilted towards a significant re-rating if, big if, they can grow AUM to 90K within the next 3 years by FY27.

Discl. Long and biased

5 Likes

Thanks for sharing it!

Does the management set any outlook for ROE?

1 Like

Not shared in particular. But as a marker to follow, it’s current circa 6%. I’d be looking for that to improve. But overall it’s the ROA improvements will allow us to evaluate further development of the narrative.

IMO the new RBI risk weights will be a drag on PEL as I understand. Even though PEL has been actively managing exposure. Views invited…

Largely the guidance if for ROA and Leverage for FY28…if you factor in both, we can see an implied guidance of ROE in the range of 11.1-12.2%

3 Likes

Thanks for sharing this. PEL has around 20% unsecured book in the retail segment and that may get impacted. However, they may not face issues in retail mortgage loans. Not sure where the wholesale portfolio sits here.

Also being an NBFC they may have to pay higher rates in their debt financing which they have got from banks. However, considering the fact that they have one of the lowest D/E among NBFCs they are better placed in this category

3 Likes

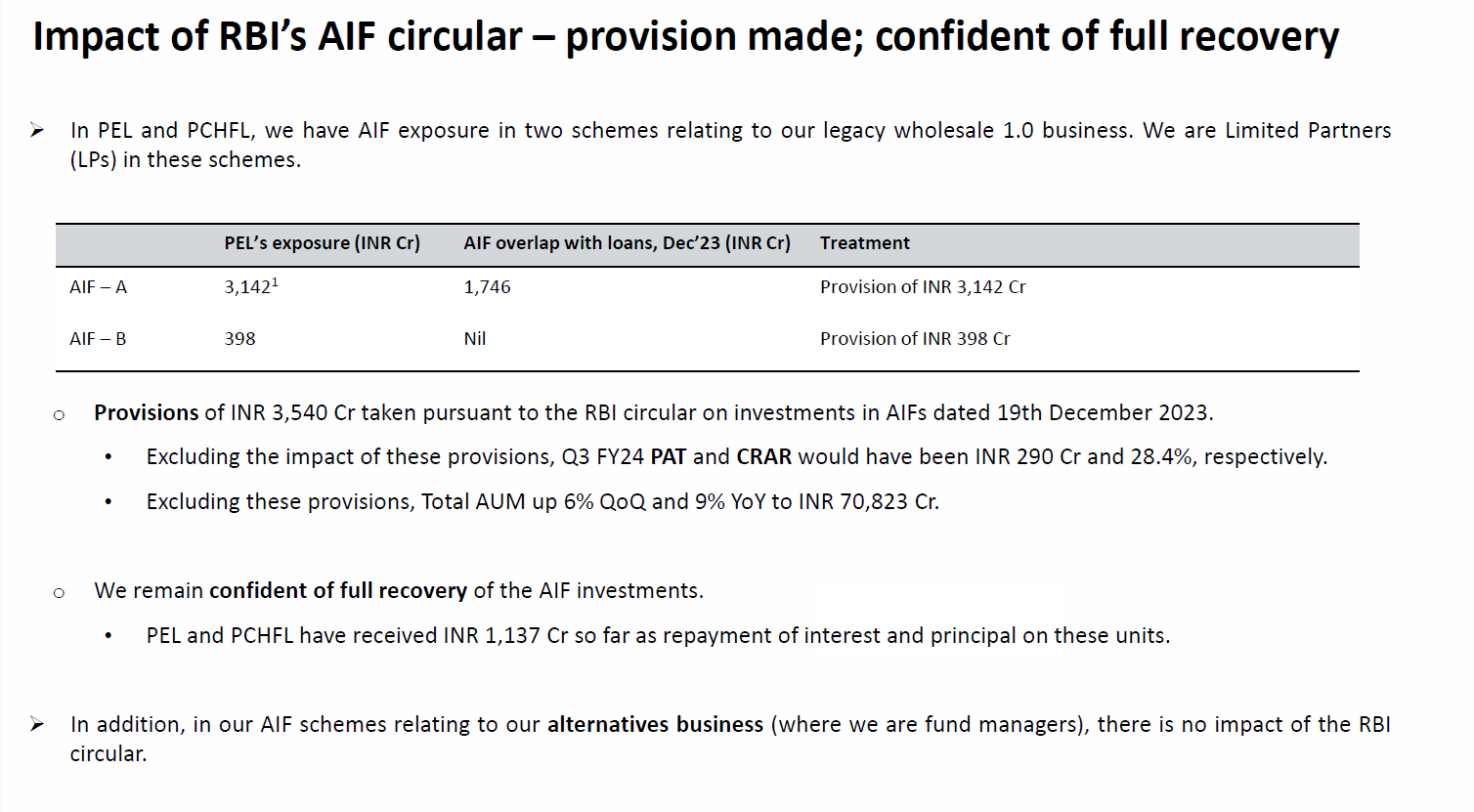

PEL set to Provision 3164 crores

136ba0a5-62c1-48c7-be58-8f1dd2fa2c60.pdf (302.5 KB)

In the midst of concerns about the circumvention of regulations by alternative investment funds (AIFs), the RBI issued an advisory on Tuesday to banks and financial companies to curb the evergreening of loans and misuse of the AIF route.

RBI restricted banks, NBFCs and HFCs from investing in units of AIFs that have downstream investment either directly or indirectly in a debtor firm where the lender had exposure anytime during the prior 12 months. Investment by the lender in subordinated units of AIF with a priority/structured distribution model shall be subject to full deduction from the lender’s capital.

2 Likes

The #1 most important quality you want in a lending business are honest promoters. This company has that. On top of it, they’ve recruited top management and acquired India’s erstwhile 2nd largest NBFC for a steal. Top it off with their current valuation, and this is an easy buy for me.

Disc: invested

1 Like

With falling interest scenario for next 2 -3 years and retail focus by PEL, seems a doubler in 2-3 year timeframe. Waiting for funds to add early next year. Expecting some opportunity post this quarter results as management taking more than required provision for AIF exposure. Technically AIF portfolios seem to have more stringent deployment criteria and I don’t expect any abnormal NPA on that account.

IBHL exposure from 110 levels have made me look into NBFC below BV and PEL story should unfold mid of next year post election and start of interest rate downward revisions.

Disclosure-Invested from 700 levels and views are biased

2 Likes

Yes, Indiabull housing was in a special situation because of their promoters and other chunky repayments. Mr Ganga managed the situation well but market took down the stock price to 0.3 times of Book Value. I kept building position as I was sure on the long term story .I will not sell this stock in coming 3-5 years as I still feel it will double from these levels in that period. I am not putting fresh money now and watching story unfold with each passing quarter.

Co lending model has significantly derisked the company and they are building strong retail book. I expect them to start showing AUM growth from Q1 2024 and that would take it to its BV around 384 in 2 years time.

My views are personal and should not be considered as any advise as I can be and have been wrong many a times.

1 Like

Interesting. I’m having another look at their Q2 investor presentation, and some not so great things in there:

NIM is down 180bps from peak

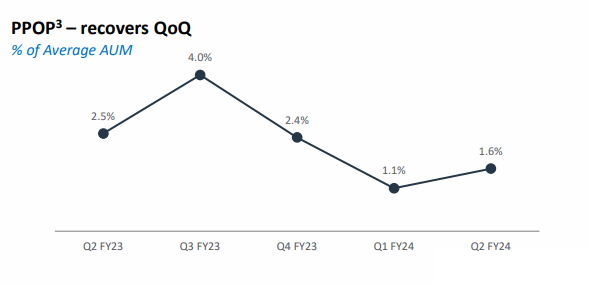

PPOP down 240bps from peak

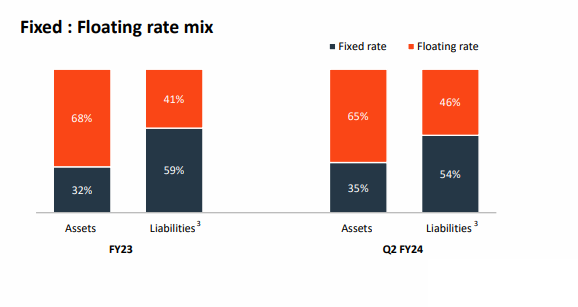

And to your point about a lower interest rate environment being beneficial for them is likely not true as well, due to the split between fixed and floating on assets v/s liabilities

This might explain some of why the market is so hesitant on PEL. The story they’re projecting with FY28 guidance still seems like a distant dream at the moment:

The above gives me some pause for sure

4 Likes

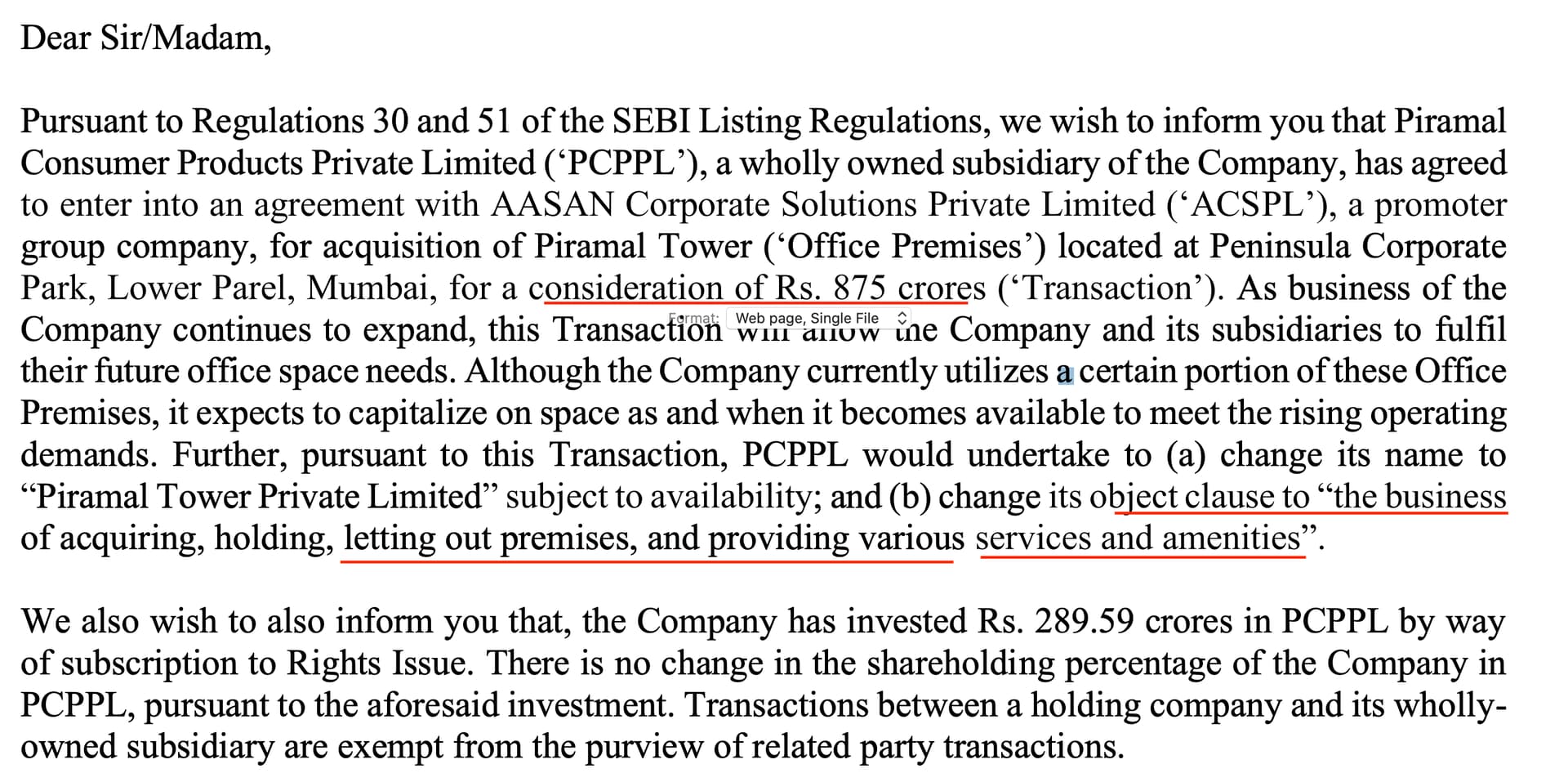

PEL is buying additional assets for 875 cr.

I wonder why are they spending so much money?

Also based on the description are they entering into commercial rental market?

They can take the tower on lease and invest the money in lending to increase the book, they might be facing challenges in growing the book so investing capital in non core assets and avoiding asset light business. Investment in AIF and now need to make provision of huge amount is also not good sign.

2 Likes

In my view, this is done to keep book value stable. real estate value will not go down or up and they need to take provisions of this 3400 cr. But these related party transactions are always not good unless we know it was done fairly.

I have been adding from a low of 500 and have faith in management although rationally I should have exited. DHFL acquisition was done at very low valuations. If management gets it right it will erase many of their sins. BFSI is all about management and the culture you build. Growth is easy in this Industry.

Anyone working in Pirmal finance can DM me Please.

Dis: I am invested in PEL since 2017 3 % of the India portfolio you can find here , so i am heavily biased

2 Likes

Do we know how much PEL actually made from its Shriram investments done close to 10 years back in total ? I think they cashed out Shriram transport stake earlier. Do they still hold stake in other Shriram companies?

Was it a prudent allocation of the money ? Can anyone shed some light on it.

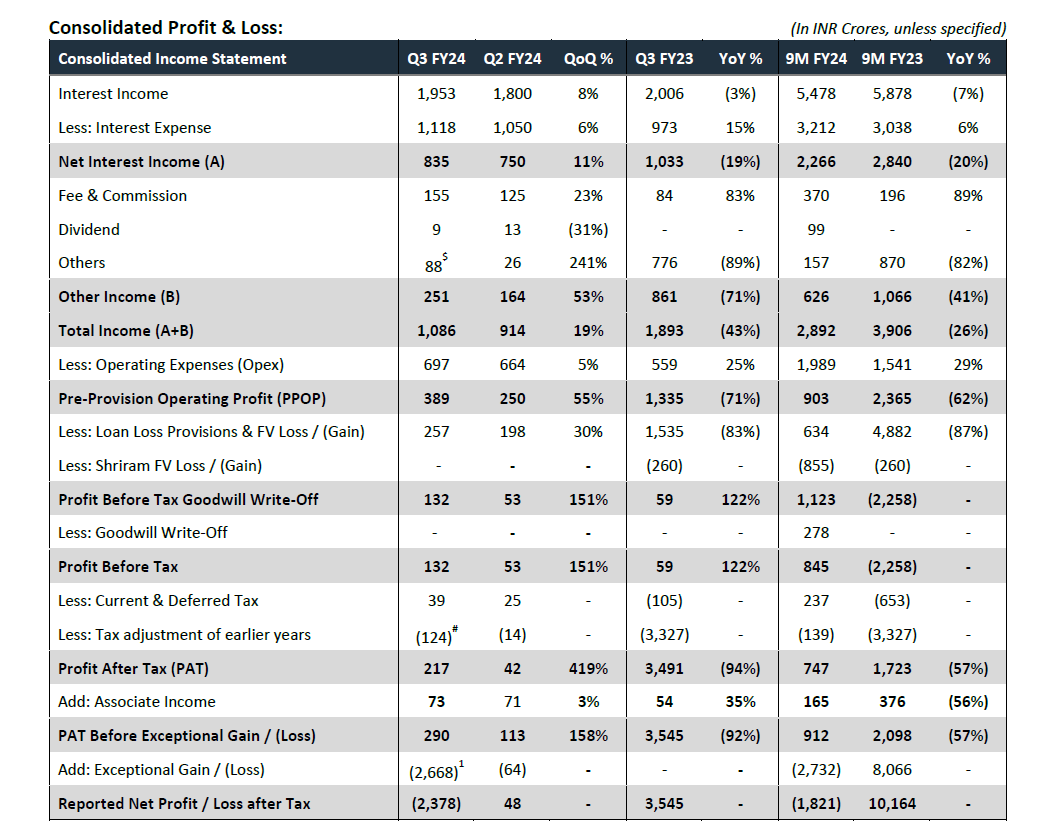

Highlights of Piramal Enterprises Q32024 result -

Prima Facie does not look exciting but if you look deeper, there is a lot of positivity and resilience. Obviously long playout story but seems like narrative and promises made since last few years remain intact.

- Reported Net Loss of INR 2,378 Cr (vs PAT of INR 48 Cr in Q2 FY24) after the impact of AIF provision. AIF provision, on post tax basis, is 2668 Crores.

Noteworthy slide attached - Provisions of INR 3540 Cr taken pursuant to the RBI circular on investments in AIFs dated. Management is confident of full recovery of AIFs - have received INR 1137 Cr so far as repayment of interest and principal on these units.

-

Growth Book AUM

Retail AUM grew 54% YoY

Mortgage AUM grew 27% YoY - contributing 72% to Retail AUM.

-

Growth Book Disbursements

Quarterly disbursements grew 50% YoY

Mortgage disbursements grew 48% YoY

-

Wholesale 2.0 AUM grew 24% QoQ

-

Wholesale 1.0 AUM reduced 47% YoY to INR 18,693 Cr and management is continuing to guide rapid rundown of legacy book over coming quarters also

-

GNPA ratio down 33bps QoQ to 2.4%

NNPA ratio down 37bps QoQ to 1.1%

-

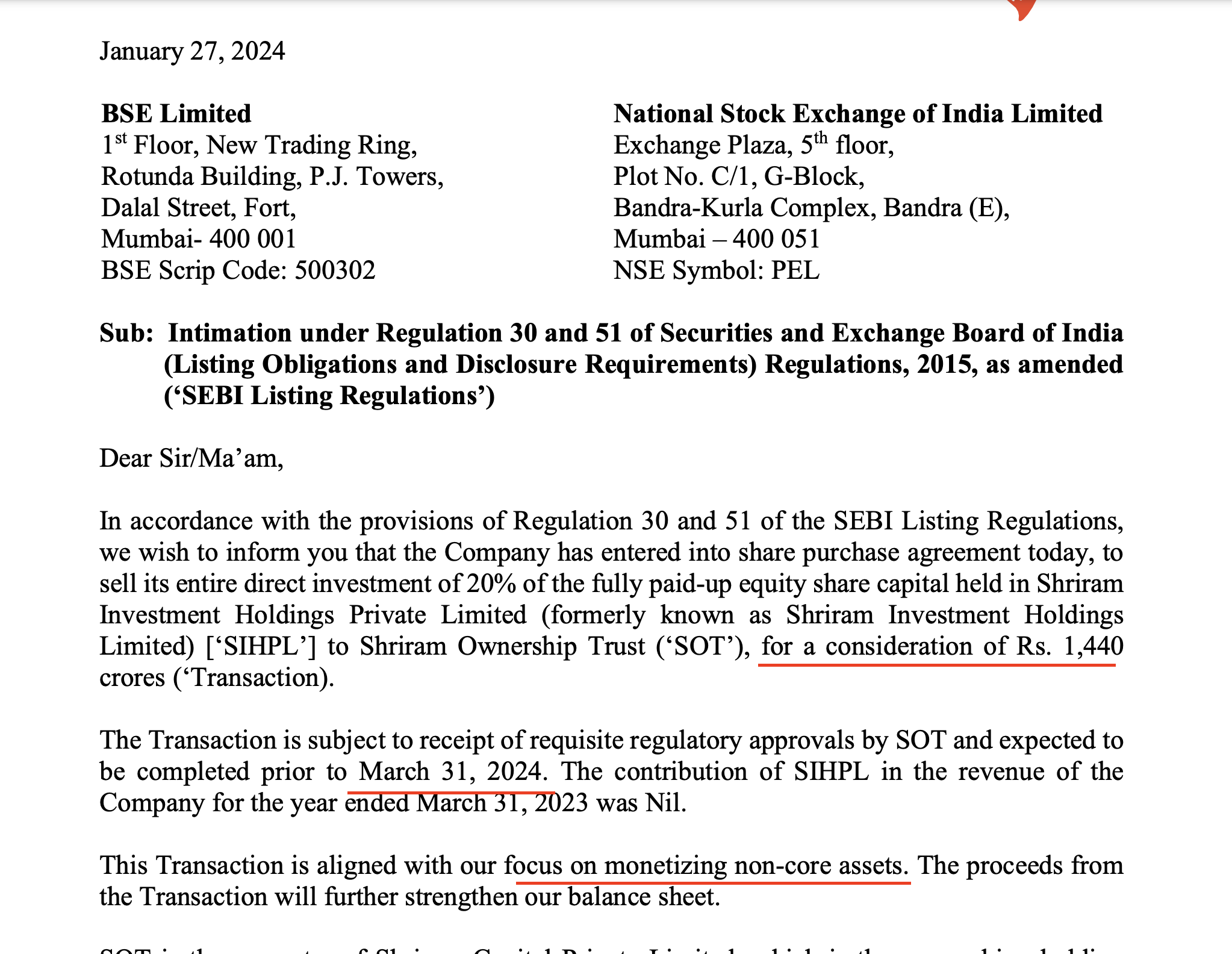

Net worth stood at INR 26,376 Cr with capital adequacy ratio at 24.3% on consolidated balance sheet. Announced sale of INR 1,440 Cr from Shriram investments (carrying value of INR 569 Cr) - expect

closure in Q4 FY24; the proceeds from the transaction will further strengthen balance sheet

-

Wholesale stage 2 3 assets are down 54 YoY to INR 4 721 Cr with PCR of 32 unchanged QoQ

-

OpEx is gradually moderating - reduced from 6.5% to 5.6% in last four quarters. Long term goal of 3-4%

-

ALM is well-matched with positive gaps across all buckets. Strong positive in a competitive environment.

4 Likes

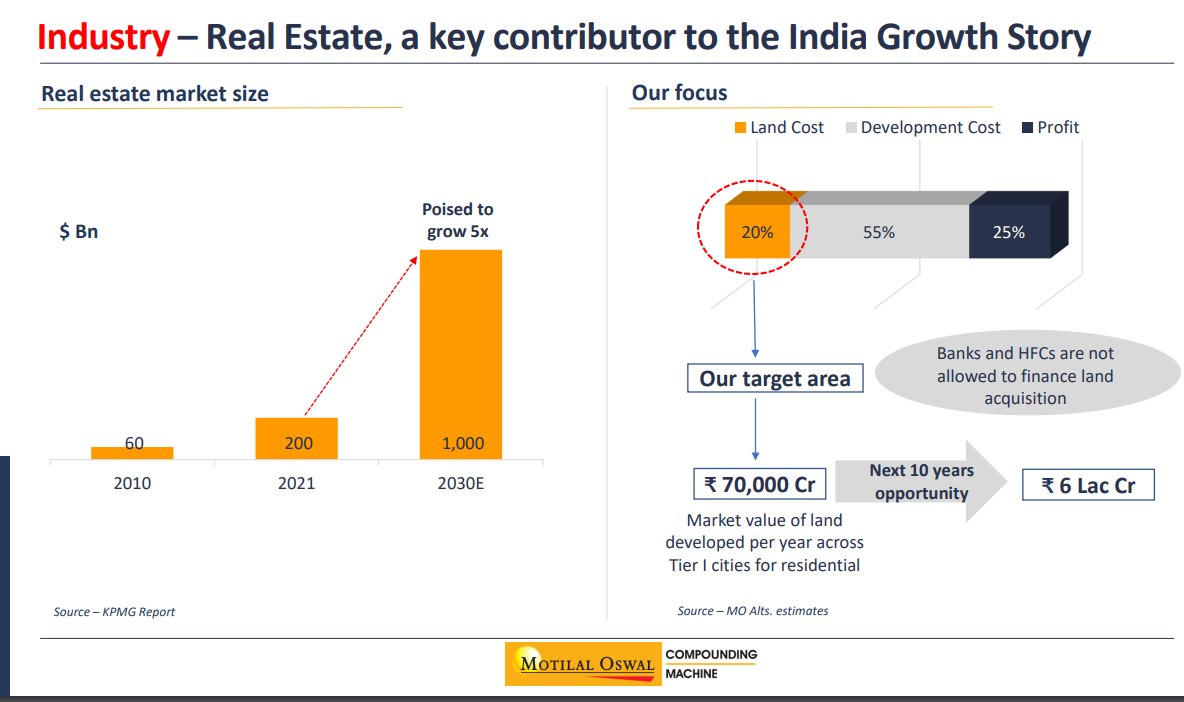

Motilal Oswal has released PPT for one of their analyst meeting. Although the PPT is for MOSL, but some section are relevant to PEL as well. For example below slide which depict the market potential for land funding, which is one of the area for PEL.

The difference is MOSL fund this through AIF funds, but PEL funds them through NBFC route. Currently market is bit worried about land funding as PEL has suffered (and is still suffering), hopefully worst is behind for PEL.

1 Like

PEL has iterated in the last few calls regarding its compliance to the housing finance company and discussion with NHB/RBI regarding the same. They have shown intent of retaining that… If that is the case I doubt they can get into Land financing as they can’t have a subsidiary in housing finance while the parent (NBFC) doing land finance.

2 Likes

Q3-FY 24 Con call notes and some other notes

Although a major portion of the notes is from the Q3 call, I have added some more references to understand things better, for example, Deferred Tax asset or Andheri land.

General

-

Added 93 Branches in the last 12 months

-

Productivity of branches in 1 to 2-year vintage is 2X 6-12 months vintage

-

Target Openex to Asset ratio of 3.5 to 4.0%

-

Today, its Opex to asset ratio is 5.6 (5.8 last quarter)

-

Wholesale AUM (excluding non-yielding assets, SR, Land Receivable assets, DHFL Book) 11,197 cr. Aiming to bring this down to zero in next few quarters

-

Wholesale SR reduced due to cash realisation of 909 cr since Q1-24

-

Shriram’s life (14.9% stake) and general insurance (13.3% stake) business is on the book at 1709 cr

-

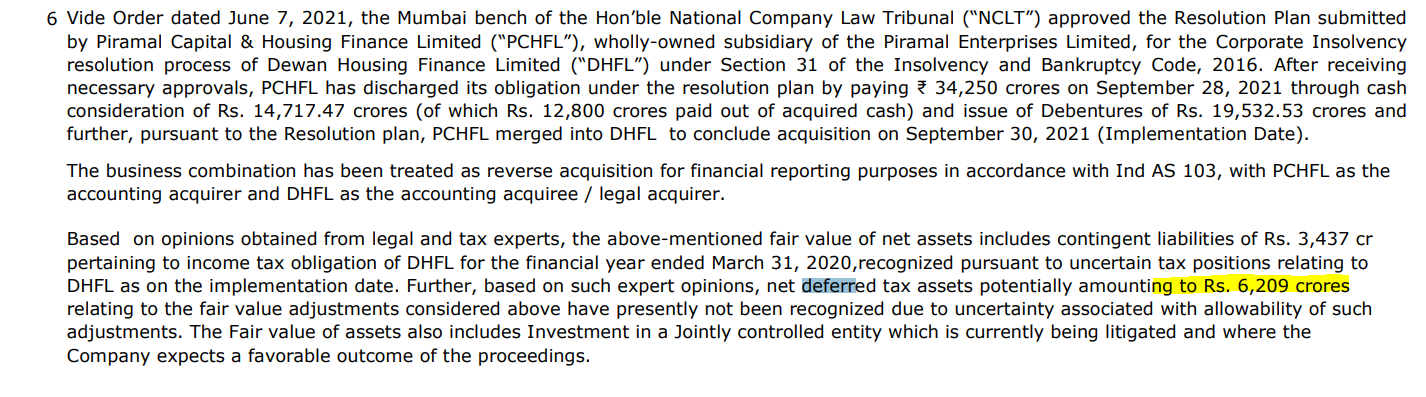

Deferred Tax Asset timeline in Q4 with tax authority. We should hear in the Q4 result. As per this link it was 6209 cr in June 2022.

-

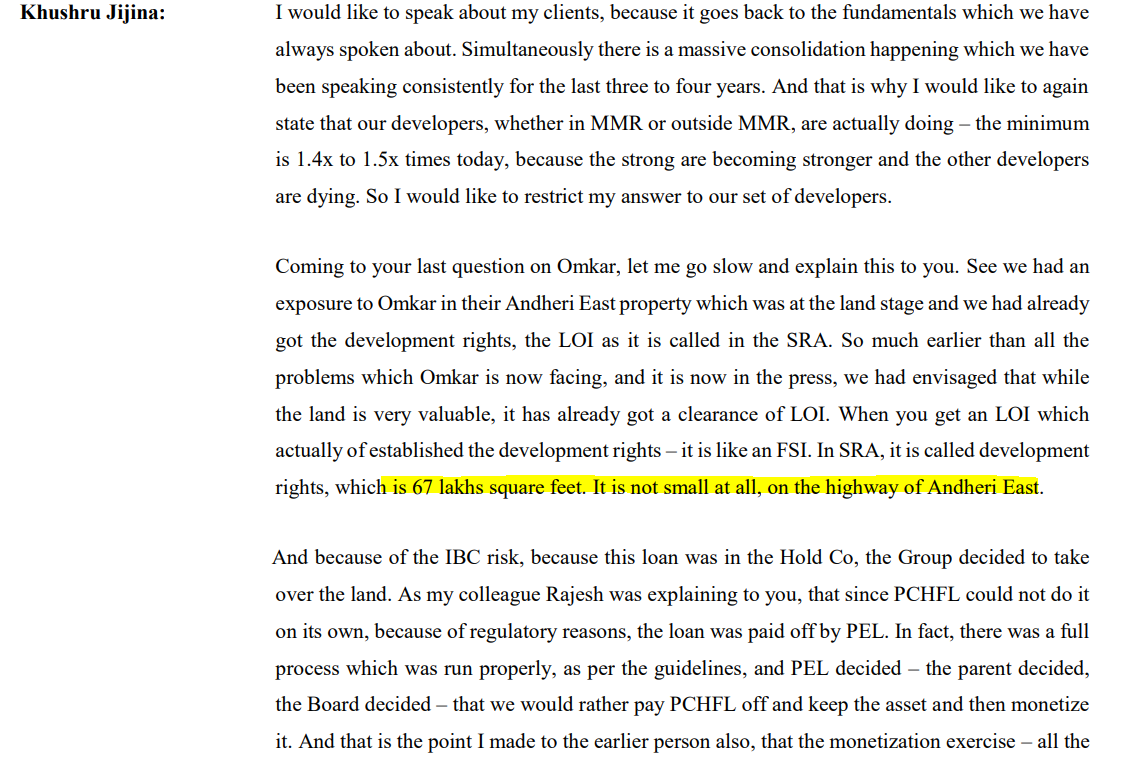

Andheri East Land- 67 lakh square feet on Andheri East Highway. Work in progress for monetisation. It is around 1300 cr on the book as ‘Investment property’. Below snapshot from old con call for reference.

Road to 3% ROA (by FY28 as per Investor Day PPT)

- There things that need to happen

- OpenX need to come down from the current level (5.6%) to around 3%

- Yield plus fees need to go up

- A moderation in the cost of borrowing.

If these things happen, ROA will improve even if credit costs remain in the same range (1.5%)

AIF

- It was formed in 2020 and comprised 35 loans. Of this, 22 loans exited and 13 remaining. Proceeds of this 22 have been used to bring down AIF

- All 13 loans are residential real estate projects. One project is backed by an undeveloped or early-stage land parcel

- earlier, it was 8000 cr. Now it is 3500 cr

- Confident of recovering pretty much everything.

- As per CNBC interview, most of it shall be recovered in the next 6/8 quarter (major shall be recovered in the first 5/6 quarter).

Unsecured Loan

- Total is 10,000 cr. But less than Rs 50,000 loan book is 600 cr( there is a serious strain in Rs 50k and below loan book overall)

- This part of the book is a flywheel kind of business. PEL is originating a bunch of customers, but only a small part of it will be going to become large ticket customers in future

Fintech business

- Done at 14/15% IRR. 90% of this business is protected through FLDG(First Loss Default Guarantee), which means PEL is not taking any credit costs.

- Essentially, it is a 14% IRR business with no opex and no credit cost, so hence, it is profitable.

- Currently, it is done through partnership, but looking forward to doing it internally

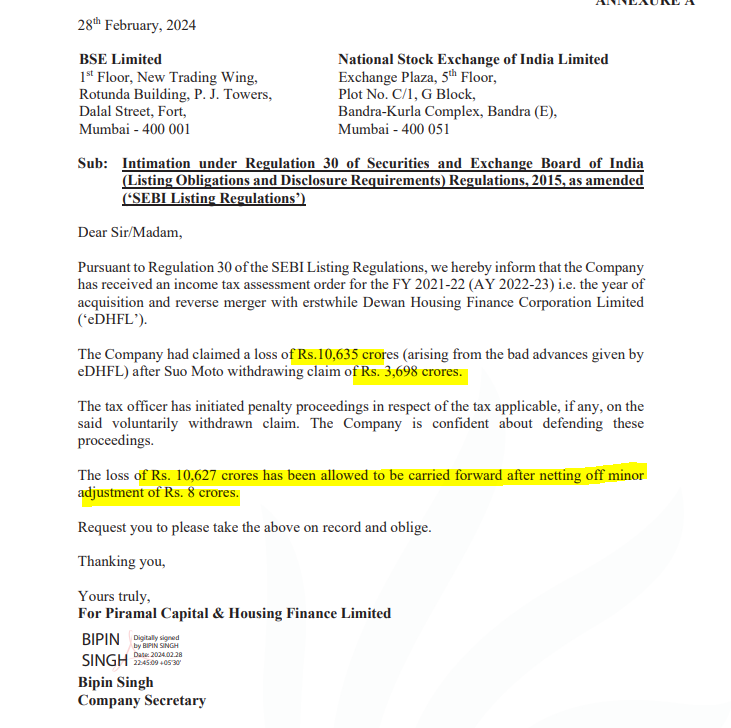

PEL Just reported that they are allowed to carry forward losses of Rs 10627 cr. Not sure it this is same as Deferred Tax asset referred above.

Note: Invested

4 Likes