Looks like it is the same, Since there is no other such large Carry forwardable loss to my knowledge

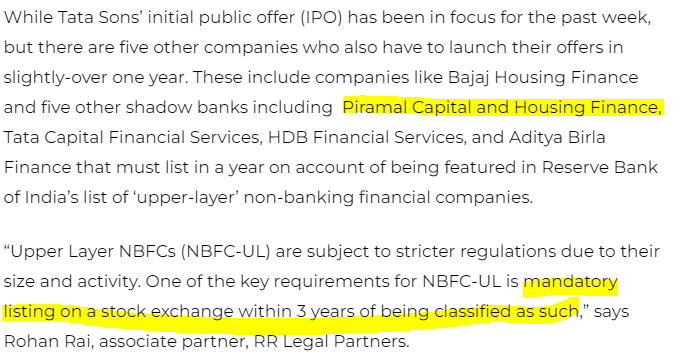

Looks like Piramal Capital and Housing Finance need to list by Next year. I do not think they have ever mentioned about this in PEL con call so far.

By the way Baja Housing Finance is getting to ready for IPO sometime this year with valuation of around $10 billion as per NDTV Profit

1 Like

May be a good news in desguise. HFCs can have different investor class, hope they will be able to raise money from market or sell Asset backed securities on house.

My Question is:

How do we value “carry forward losses” when calculating

intrinsic value of a company?

Terrible results. Company keeps springing new provisions. Best case book value will remain same for 12-24 months as losses on running down legacy book will equal profits from new biz.

Long story if you have patience as still available at discount to book

2 Likes

- Growth business shall be 100% off lending business- which means Wholesale 1.0 will be completely run down, and all lending revenue will be based on the growth business.

- Smaller legacy businesses shall aid in the cost of funds.

- SR reduced by Q1- Cash realisation of 1400

- AIF- 340 cr cash realised plus interpretation of AIF circular- write back of 1600 cr

Approx 3000 cr of provision run down

- 1400 of markdown of fair value markdown on non-earning assets

- Large stage 2/3 - 1000 cr settlement of account by taking settlement

- Provisioning buffer of 700 cr for future provisioning

-

Adjusted this against a similar amount from a one-off gain. This is beneficial to PEL in the long run and for the lender.

-

Wholesale 1.0 down from 44k to 14k cr- Book down by 30k, but credit costs 9000 cr in the last two years. lGD (Loss Given Default) is 30%. In the future, LGD could work on the remaining book- It is up to individuals to estimate it.

-

First, low-hanging fruits are disposed of. The last part is very difficult and risky. The most problematic fruits are left behind.

-

For PEL- Some of the large assets are out. A large account has gone out this quarter.

-

Retail growth will be slower going forward as compared to Fy24.

-

Run down is adjusted against undervalued or no valued assets. Hence, we thought of doing a run down by taking haircuts. One net basis net worth remains the same at the same time, taking a run down.

My view

Fee income—I’m not sure what is propelling fee income. Is it retail or wholesale 2.0 lending? How sustainable is this?

Another set of accelerated run down for wholesale 1.0. This term refers to the gradual reduction of a particular type of lending. They have mentioned this many times. As far as I understand (please feel free to correct), they have made similar statements at the start of FY24, in Fy23 and every year in the last 2/3 year. There is nothing conservative about their provisioning. IN Q3-24, they said we were done with provisioning and within 3 months, came up with 3000cr of write down. Based on the call, it looks like another set of 4 to 5000 cr provisioning is remaining (assuming 30% LGD on 14k wholesale AUM)

INR 67 bond (My limited understanding)- which is converted to cash 1/3rd per year. This is a kind of dividend but in a different format. They have reduced the dividend amount from Rs 33 to Rs 10. I am still figuring out why there is such a drastic reduction in dividends, but they are distributing the money to shareholders in a different format. For example, INR 67 bonds will be converted to cash 1/3 - INR 22 per year INR 10 dividend, which means around INR 32 dividend for FY24 and possibly for the next 2/3 years.

PEL has done a massive amount of bad lending in the last 5/6 years. Shareholders have paid a massive price for earlier management (confident but stupid, which massively increased wholesale lending at 25/30 CAGR before COVID). They will not acknowledge it openly, but the results from the last 2/3 years make it very obvious. They have buried their bad practices under the hood of DHFL, but they come every few quarters with accelerated wholesale provisions with a promise that they are reaching the end of the tunnel. The only silver lining is Wholesale1.0 is reducing much faster, so hopefully, they could recoup some of their losses.

INR 10k losses assets. Looks like PEL is unlikely to pay any taxes for the next 3/4 years even if they report 2500 cr PAT every year. This will help return ratio improve faster going forward.

Note: invested

11 Likes

Posting queries sent to PEL IR. Will post reply. If anyone knows answers to any these questions, please help

Please help me with the following queries:

-

Page 10 of presentation : Legacy loan book 14572 cr, existing provisions 2516cr against it

- Is 14572 written down value on books after 2516 cr provisions.

- Has the 2516cr already been used to write down book or resides on balance sheet as provisions -

What items contributed to loss of 570 cr in fair value net gain loss in P&L

-

The 729 cr provisions taken is on the legacy book only or across entire book

-

What investment property was written down by 600 cr in this quarter? What changed in one quarter to see such a dramatic fall

-

This quarter writing down 4200 cr of legacy cost us 2400 cr which means provisions were clearly inadequate. It might better to write on legacy book at realisable value in one go than negatively surprising in results every quarter. Just a suggestion

-

Book value has been declining/stable for over 2 years. Is it safe to assume it will resume upward trend only in Fy27 as l foegacy book will be written down @ approx 7000 cr for two years each

-

The Price to Book for PEL is the lowest in the industry. Even PSUs have better Price to Book. Is the management aware of this divergence and trying something to change perceptions

-

The 278 cr goodwill written off, when was this created and what exactly was this asset for.

-

Where does the 10267 cr loss exist on balance sheet for carry forward, if it does exist on balance sheet.

9 Likes

Good points. Because of stupidity in real estate they are suffering. i have been attending calls from last 4 years. The management looked so confident and transparent that we thought piramals will take all the value from real estate but whole industry collapsed. They collapsed with it. Not only realestate all the lending they did was bad including corporate lending to solar parks etc in Adhrapradesh.

4 Likes

Any of these write-downs from their DHFL acquisition? Or are these write-downs on loans issued by Piramal itself?

Got reply from PEL IR

-

Book already written down in balance sheet. 14572 cr is face value pre write down just shown in ppt

-

570 cr pertains to legacy book

-

729 cr is provision across biz not just legacy

-

Cant name assets but revalued reslisable value hence write down

-

Feedback taken

-

Bulk will be done in FY25 only

-

Reducing legacy book faster than planned to improve perception.

-

Not specified yet

-

Not on books

6 Likes

The mgmt of PEL is not at all transparent and investor friendly. They are not cheat/fraud, but their saga of provisions is never ending. Once they were “largely done” with the provisions. Regarding the land also, they showed huge potential, and now they are writing down its value. I guess it could be the land in Andheri for which they never shared what is the progress and what are they doing with it.

I am super disappointed with them. While there is great business opportunity and they are trying to build a profitable business around it, their “cleaning process” is never ending. I hope they deliver the guidance they have given and that creates some wealth.

Disc: Invested

2 Likes

I gave up on them for now. Was heavily invested hoping for legacy woes to be over

1 Like

Great work @startupfundas for keeping us updated. I was sceptical that they would respond, but they did.

It looks like PEL’s write-down sage is never-ending, but the management has a point as well (if you want to believe them).

As per the last call, Jairam mentioned that the company is not evaluated on SOTP, and the market is not giving any value to other unrealised assets. Hence, they are completing writing it off and starting a book fresh. This is again chicken and eggs situation. They are writing down assets, hence the market does not believe it and visa versa too.

Hopefully, it will be majorly over (never say never for PEL) this year. It looks like they will do another 2/3K write-off in Fy25; hence, there is no trigger for the stock for FF25(CMP 820).

3 Likes

In my case i have lost confidence in the books. They kept saying adequately provided and keep providing more. This year showing pockets of value against upcoming write offs was the last straw on camel’s back for me at least.

2 Likes

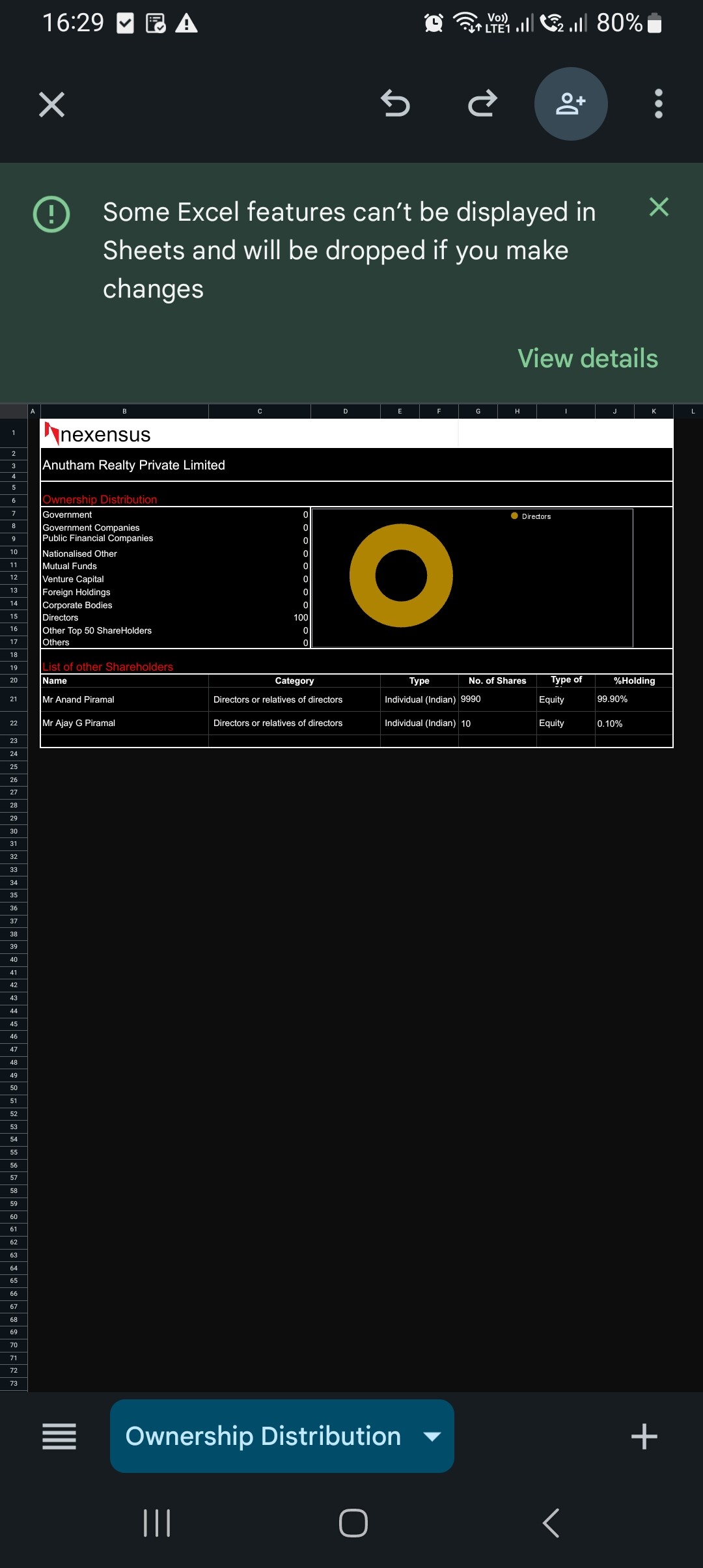

Ownership being transferred to Anand Piramal

Anutham Realty 99.9% owned by Anand Piramal

C673AAA8_D388_4519_990A_C97BE90E4A7F_142542.pdf (2.8 MB)

3 Likes

I am a new investor and have been following the company for about a year. At the cost of sounding optimistic, here is my take on PEL’s legacy book:

As of FY24:

- Gross legacy book: Rs. 14,572 cr

- Provisions: Rs. 2,516 cr

- Net legacy book on balance sheet ~ Rs. 12,000 cr

This implies that if the company recovers < 12K from the legacy book, it will have a negative impact on net worth and vice versa (I am not really hoping for a positive impact from this book).

In Dec 2023, due to an arbitrary RBI circular, AIF was rundown from Rs. 3,540 cr to Rs. 1,067 cr, resulting in a (hopefully) unrealistic loss of ~2500.

[Source: “impacted by net AIF provision of INR 2,473 Cr in FY24” in Q4FY24 presentation].

Gross legacy book (adjusted for AIF) = 14,572 + 2500 ~ Rs. 17,000 cr.

Between FY23 and FY24, gross legacy book value went from ~29K to ~17k, generating liquidity of 10,245 cr. This implies a recovery ratio of ~ 10k/12k ~ 83%.

Digressing slightly, I think the additional provisioning in Q4FY24 was required because, in FY23, this book had provisions of 10% (implying expected recoveries of 90%), whereas the actual recoveries in FY24, as we saw above, were 83%.

Required recovery ratio going forward for a net zero effect on net worth

= net on book / gross

= 12k / 17k

= 70%

If we assume that the AIF will be recovered in full, this ratio will be further down ~ (9.5K/14.5K) ~ 65%. But let’s not make this assumption.

Given the above, I think the legacy book should not have a material negative impact on the company’s net worth going forward. The pockets of value and the stock being available at less than the book value adds additional buffer.

I think what matters much more is the profitability and asset quality of the growth book. In my humble opinion, this is largely unknown at the moment. It is good that the company has started reporting separate profitability numbers for growth and legacy books - this will help in getting a sense of the growth book independently.

2 Likes

Creating two books for investors is not sign of transparency but sign of weakness. Every financial institution who has gone through bad phase will have two books good and bad. They give different names. It on management discretion to call anything legagcy. In short realestate and corporate financing standards were bad they gave loans to solar companies in Andhra and almost all developers collapsed. Luckily lodha survived.if something was to happen to lodha Piramal fiancé would have been history. Lot of us got into Piramal due to investment acumen of Ajay Piramal his ability to make large value deals. Last 5 years have been value destruction. Now it all depends on new team and how they play execute. Although recent uptick in HDFC NPA is worrying and RBI stance on retail loans.

Risk and rewards looks good at this price provided no major NPA ahead. If they are excute this will be 5x in next 3 years. Need scuttlebut with some employees.

Disc: holding from last 6 yrs adding still.

9 Likes

having been invested in the company since 2010… I strongly opine that one of their erstwhile senior mgmt leaders with a rhyming name and a big mouth conned AP… and this led to serious value destruction…

2 Likes

Khushru Jijina had hand in glove with many developers that he financed.