the results don’t seem to look very good. Were it not for the gains made from sale of shares in Shriram, PEL would have made losses in this quarter. Good amount of write-offs in this quarter as well. Interest income is down, but it is understandable as wholesale book is being wound down. Management has admitted to deferred tax assets worth more than Rs 4000 cr which is a positive. Views invited.

1 Like

Ajay Piramal interview on BQ Prime for Q1FY24.

Buyback review:

Buyback price = 1250/share. So, 25% returns if bought at the price of 1000/share.

Record date: 25 Aug 2023.

So necessarily buy PEL at 1k, than participate in buyback for clean 25% profit.

Any downsides I am missing?

1 Like

Buyback profit will depends on acceptance ratio and the share price after buyback.

1 Like

| Name | Piramal Enterprises |

|---|---|

| Special Situation Type | BuyBack |

| Special Situation SubType | Tender |

| Total Shares | 238,663,700 |

| CMP | 1,014 |

| SS Price | 1,250 |

| SS Shares | 14,000,000 |

| Promoter Shares | 103,780,693 |

| Promoter participating | No |

| Non-Promoter Shares | 134,883,007 |

| Probable Acceptance Ratio | 10.38% |

So with Promoter not participating the probable acceptance ratio is ~10%, it might go a few points higher if non-promoter also not participate, but the numbers are slim. Even if 50% non-promoters do not submit (highly unlikely), the ratio goes to ~20% acceptance.

1 Like

As per June share holding pattern, small share holders hold 29,090,762 shares and with 15% reservation for them, 21 lac shares may be bought from them which gives a minimum acceptance ratio of 7.22%. From my past experience with the buyback of Hinduja global and Wipro, I expect the acceptance ratio to be upwards of 20%. Promoters not participating is not going to help the small share holders. It will help the non-promoter share holders holding shares valued more than Rs 2 lacs. As per my understandin, only if this category of investors tender less than 85% of the total buyback shares (85% of 14 lac shares), it will get allocated to the small share holders.

Disc: Invested around 750 level as it was trading 0.6 times book. Post buyback announcement, have bought more in multiple accounts to take advantage of potential arbitrage in the buyback.

3 Likes

about 25 per cent of the shares tendered by retail investors is likely to be accepted during the buyback. price to book value is now 0.79. at buyback price it will be around 1. dividend yield is also 3 per cent at present. peers are trading at far higher price to book valuations.

IMHO the risk is that the stock could rise quickly after the buyback offer concludes and investors who want to do a trade may not be able to get back into the stock after the proceeds of buyback are credited to their accounts. One option would be to buy 60-70 per cent of the quantity tendered for the buyback immediately after the record date.

the latest concall has given me some confidence that the company will do well in the coming quarters and the Piramals are using the buyback to increase their stake in the company.

In the medium term, the Piramals may even sell out to Reliance.

dis: holding. still undecided on whether to participate in the buyback.

1 Like

…On the Andheri land topic…the management continues to provide no updates whatsoever, but maintains a stance that there is “enormous embedded value”…however, they dont offer any timelines, plans, strategy to monetise the same. Till that time, the mkt value will not price this in I guess.

Disc: Invested

what is size of andheri land ?

One way I think of this- at a 1% div yield PEL becomes dead money or trends lower imo. Trade around it if you have that skill. I’m happy to hold on and see what Mr. Piramal does.

was 6.7 mn sq.ft…refer to their May 2021 call

This is certainly an earnest possibility imo…JioFin could be a useful vehicle to extend reach? The customer data sharing synergy towards lending and offering financial services could be huge.

Dis: Invested in both

1 Like

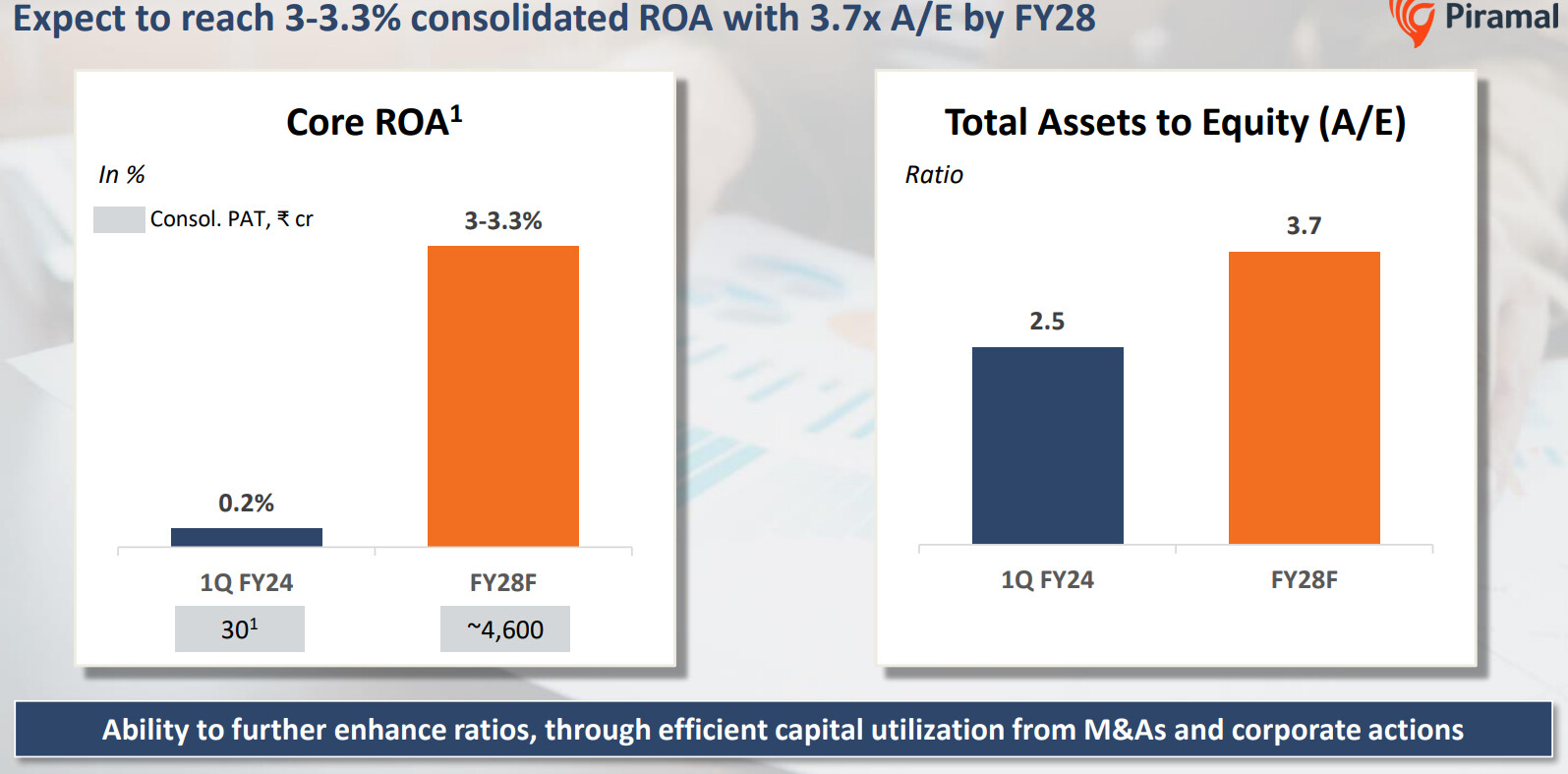

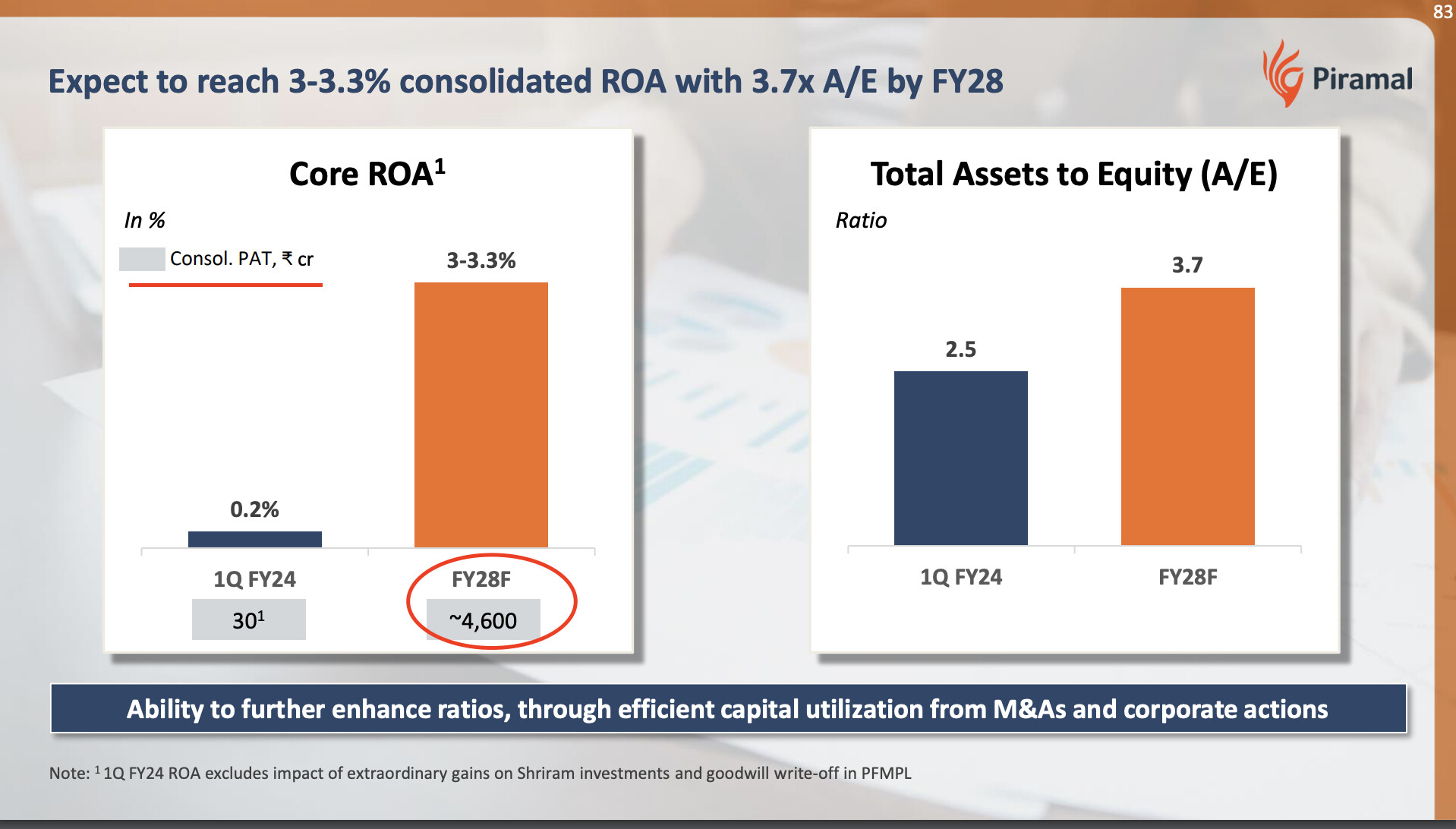

PEL published investor day PPT. It is very detailed and provide their aspiration for FY28.

Key Takeaways:

-

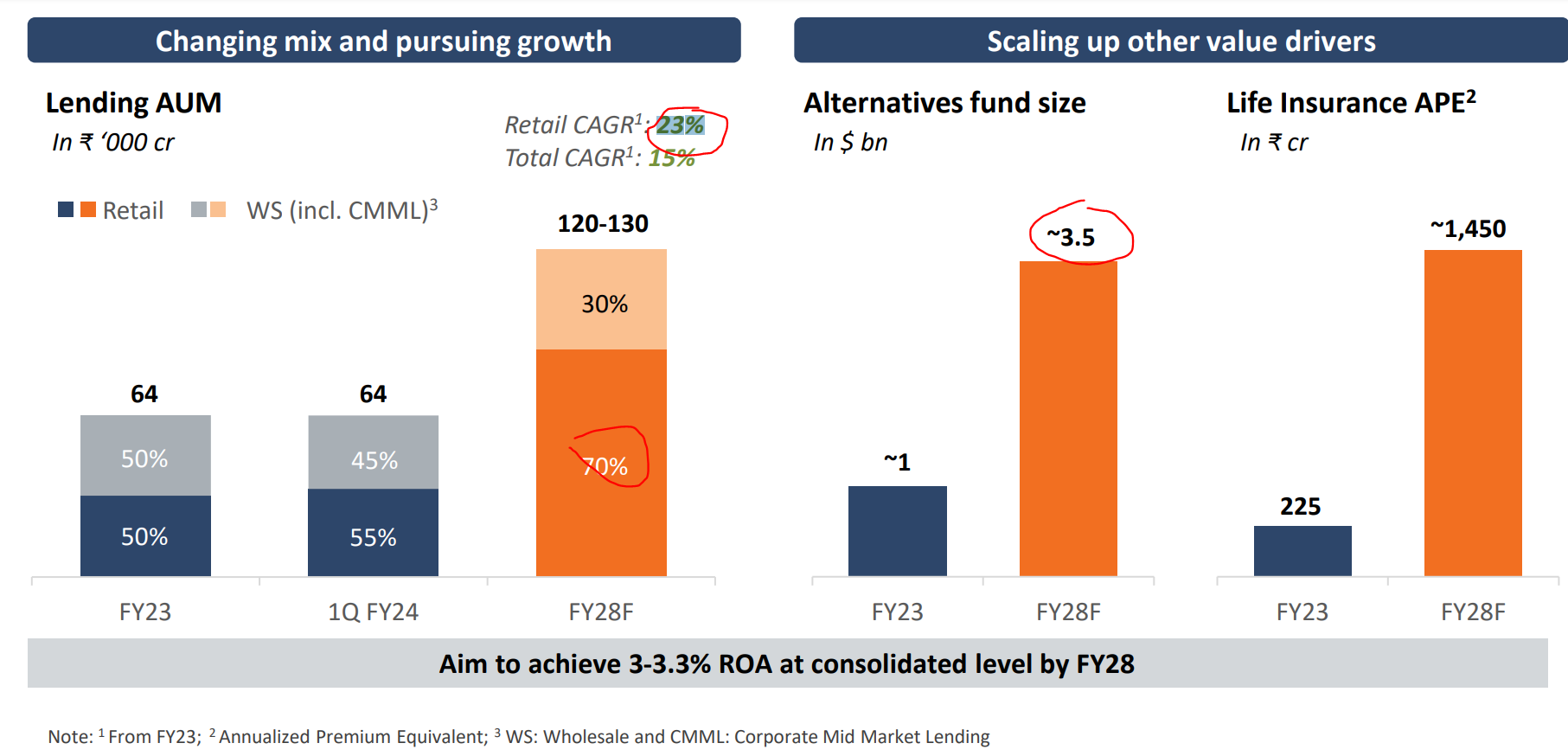

AUM growth outlook: Based on recent performance, they are cautious about retail growth. Although the base was small, now they have invested in technology and opened up many branches, which can be a positive surprise going forward.

-

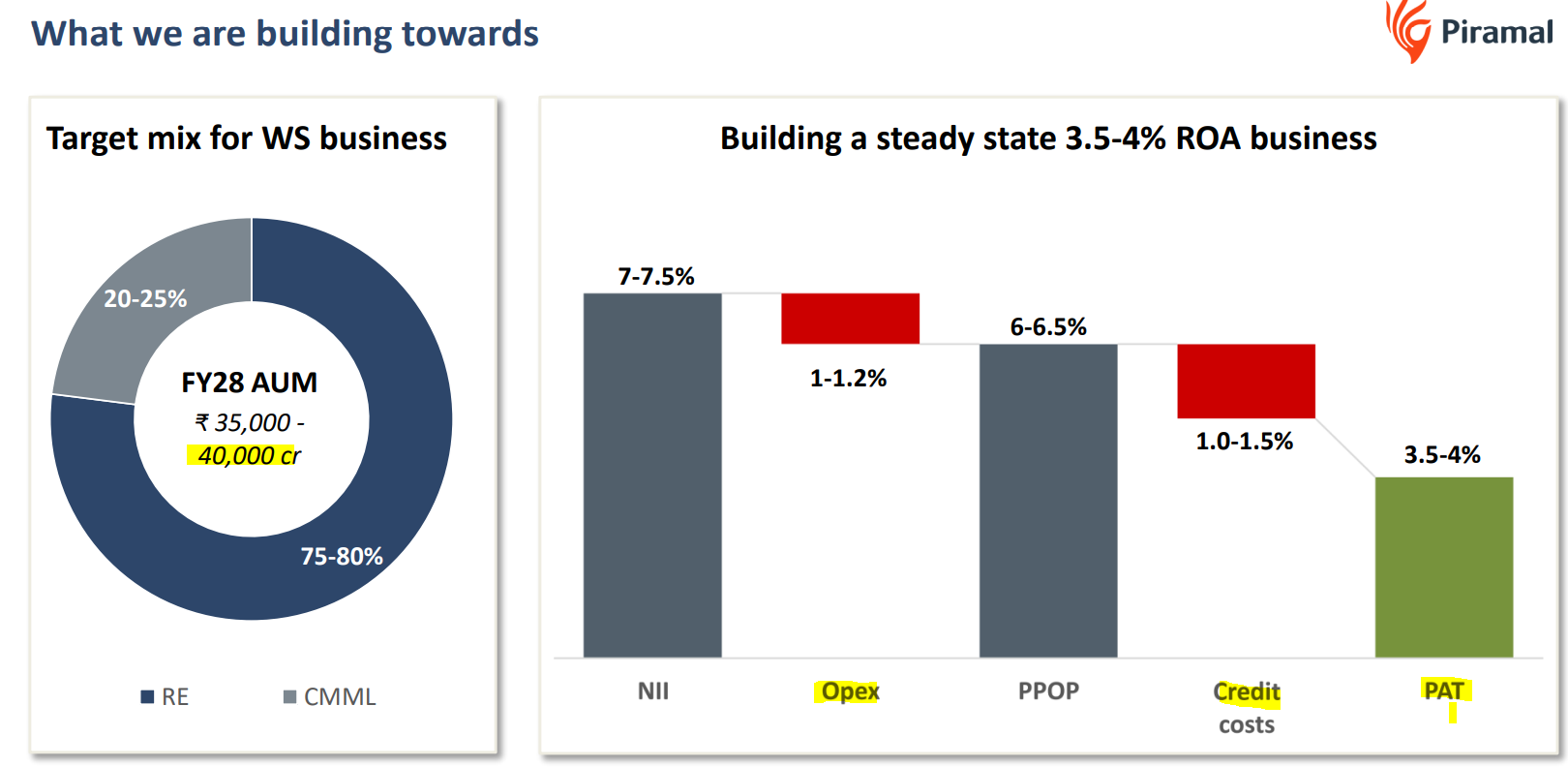

More than tripling Alternative funds size. This shall increase the immediate fee income (in the next 3 years), but it will not have a meaningful impact on carry payment as the carry comes 3-5 years after investment as it is one of the most important parts of alternative returns (Chery on the cake). PEL generally do not say much about this segment. Once it reaches $3 billion, it will be interesting to see how it shapes up.

-

There is a huge growth in Life insurance, but it may impact the balance sheet as Life insurance is growing much faster, and it may not be profitable yet due to the huge investment they are making in growth.

Productivity Metrics

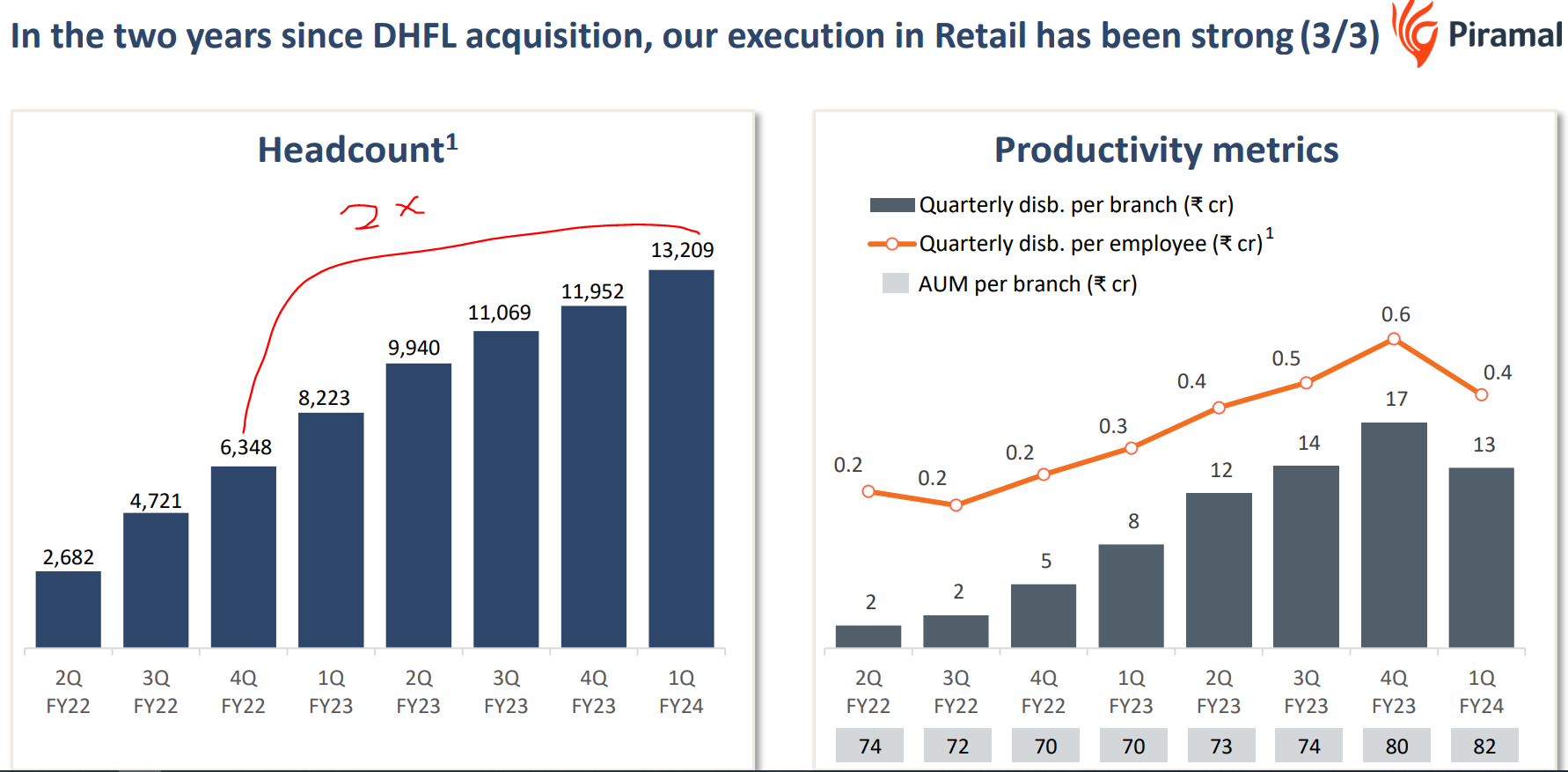

- More than double the number of employees in 5 quarters (well after DHFL acquisition). They have invested huge upfront in building and strengthening the retail front end. The current P&L shows the cost, but not all benefits are realised yet. As they increase the contribution from retail, I think the operating leverage will play out, helping their profitability.

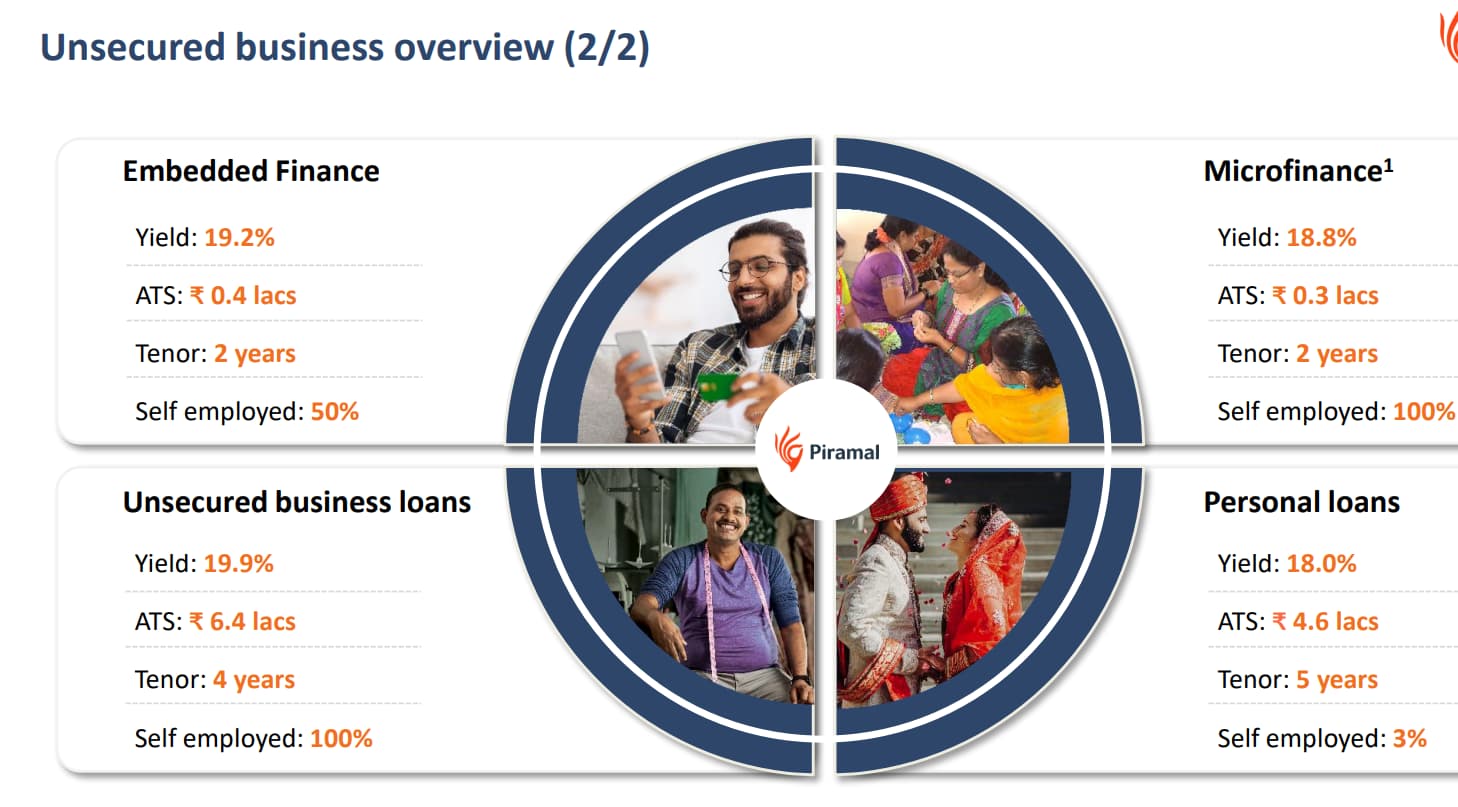

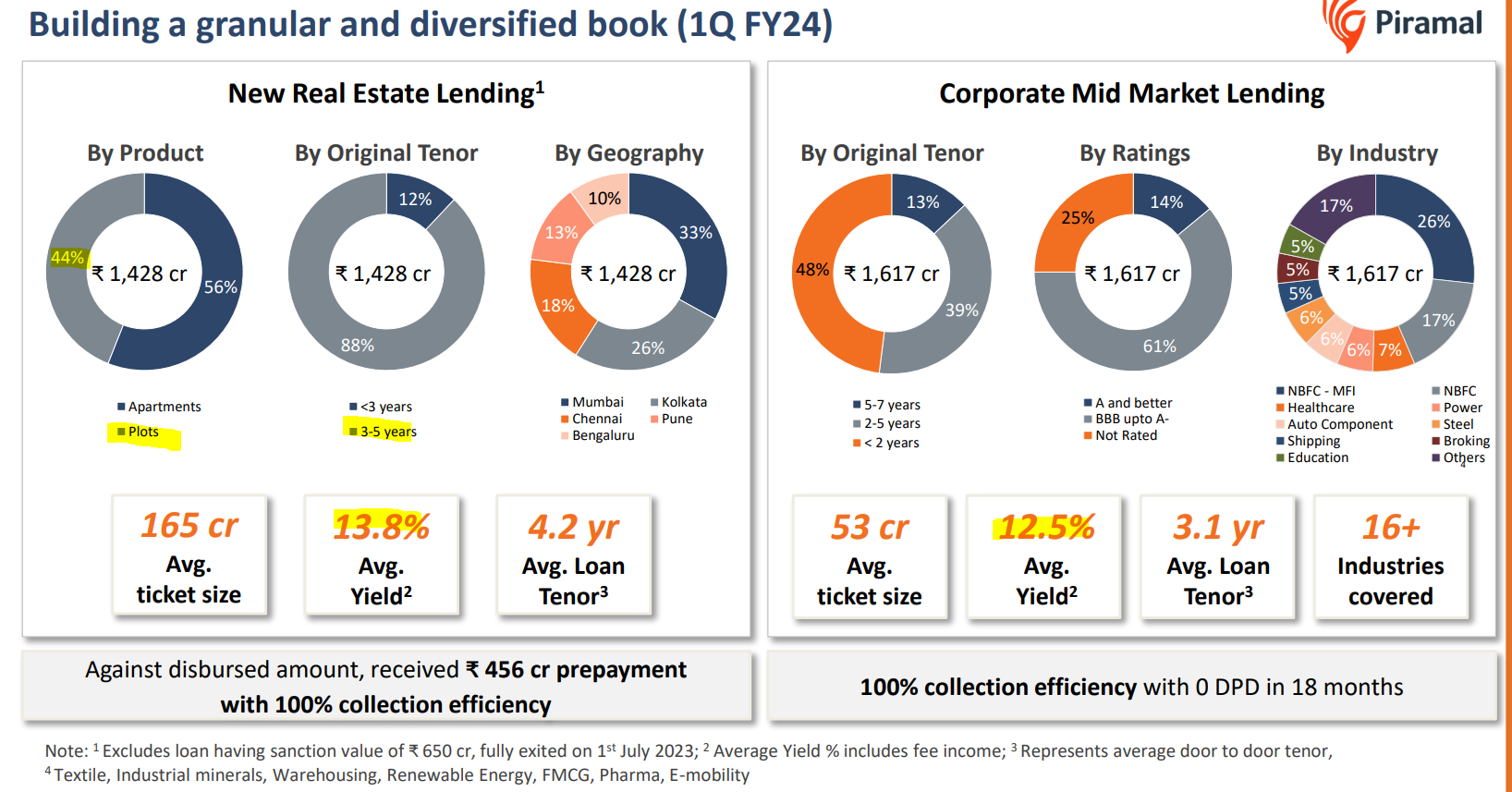

3- Unsecured

- I think this could be the bone of contention. They have ramped up disbursement massively- 40X in 7 quarters. Although the yields are much better, PEL’s records in managing the risk-adjusted return are bad.

-

During 2018/19, they were thumping their chest and saying a lot of things about the quality and how they monitor of their portfolio. They even said that RBI had applauded their portfolio tracking. Fast forward 4 years, they have lost all (or most of) profit due to bad loans.

-

So I would personally not read too much into it now. It is concerning that they are ramping up risky segments very fast, which his fraught with risk. They had difficulty managing secured lending to real estate developers (2X security for the loan), but still made massive provisions how this unsecured fear is a thing to watch. I hope they manage this well after learning a thing or two from Wholesale 1.0 debacle.

FY28 Aspiration breakdown

-

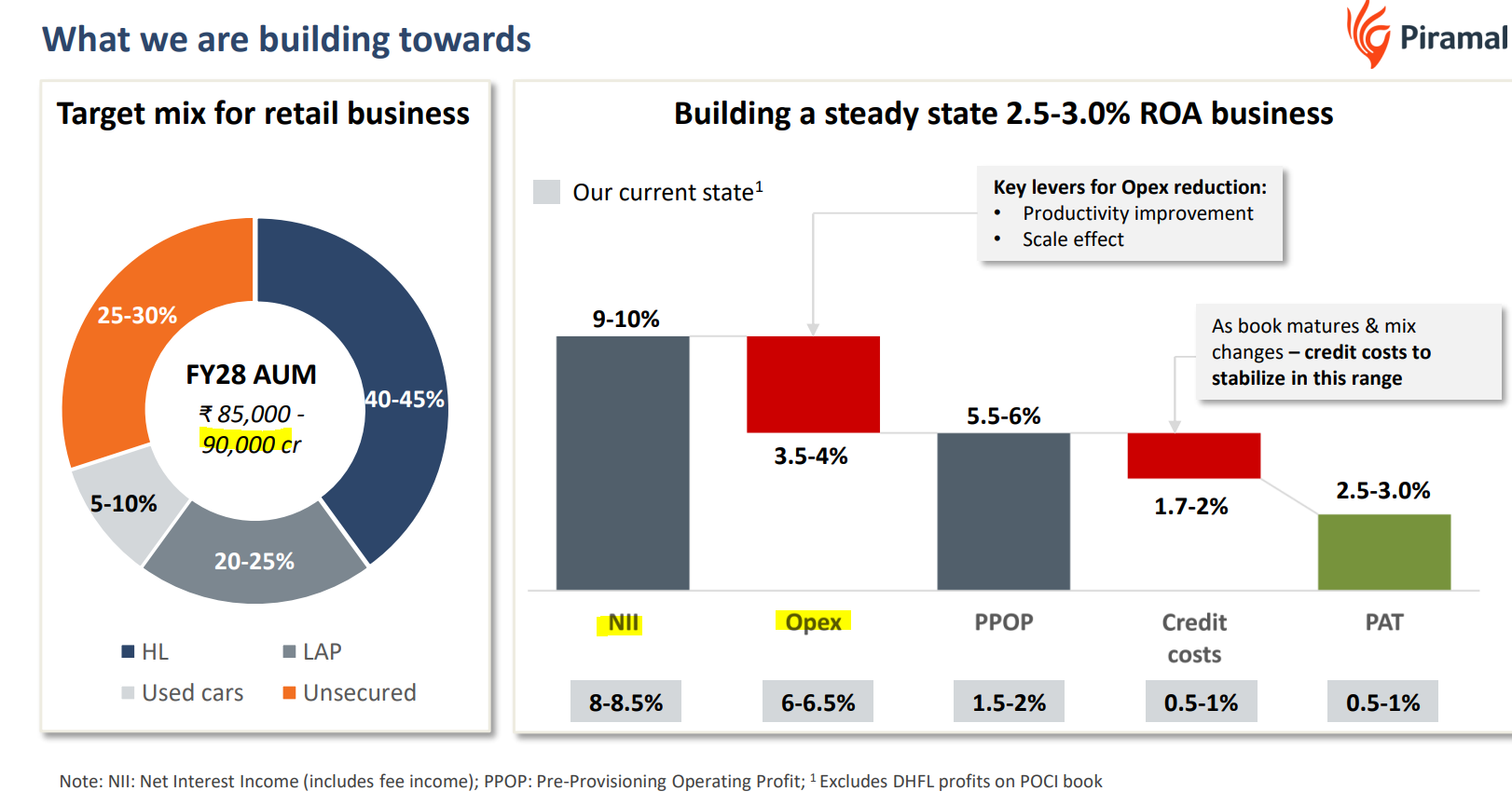

This is one of the most important slides and provides a glide path for the portfolio. Retail AUM target is 90,000cr (Fy23 is ???).

-

The improvement in ROA is likely to come from Opex reduction or operating leverage play along with NIM improvement.

New Wholesale

Large exposure to land purchase. Even if they manage it well, the market will not like it and is not likely to give a high valuation to this part. So even though it may be more profitable than retail, but if one goes by their own record, the wholesale profitability can disappear in a flash. Hopefully, PEL is lucky second time, and I hope that it fares better than the wholesale 1

…this shall lead to PAT of 4500 cr by FY28

Overall good read and they are providing PEL’s aspiration. I think PEL will need 2/3 quarters to clear the book before they start reporting better numbers.

Note- Long term invested

5 Likes

is there chance PEL to sell insurance business to Jio finance as they had strong plans and capital to invest for long term to build insurance business.

Very good analysis. Piramal was always good in making presentations and providing long winded explanations during concalls (mainly by Mr. Jijina) …the problem is with their execution. Street is concerned about lack of transparency in the past and their reluctance to accept (and apologize) their multiple mistakes :- ![]()

They need to start showing consistent results before market can trust them. They need to let their results speak for themselves, then only the stock can regain its past glory.

6 Likes

Piramal are looking to raise $1 billion for their resurgent fund.

3 Likes

How to tender shares if I have Zerodha and Axis Direct account?

I know about Zerodha… go to Zerodha Console - under one of the tabs, there is Corporate Actions, where you can place bid

2 Likes

Source Link: BSEINDIA

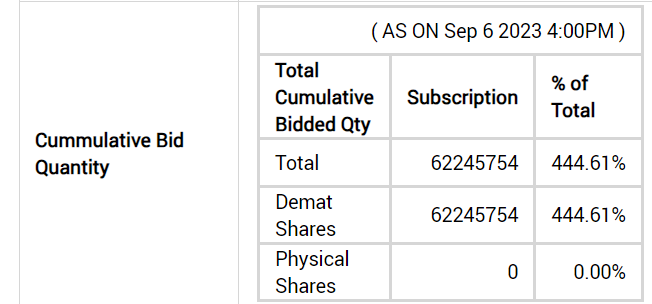

Seems Acceptance will be atleast around 22.5% for most holders, if they have submitted more than their entitlement.

Synopsis

“The Piramal Group has sold its bad loans worth ₹531 crore to Omkara Asset Reconstruction Co., including properties like a JW Marriott hotel and a Crowne Plaza unit. The deal was done at a premium, resulting in a profit of over ₹700 crore for Piramal. The loans were initially sold to Omkara ARC in a structured deal, with 15% paid in cash and the rest issued as security receipts.”

Read more at:

3 Likes