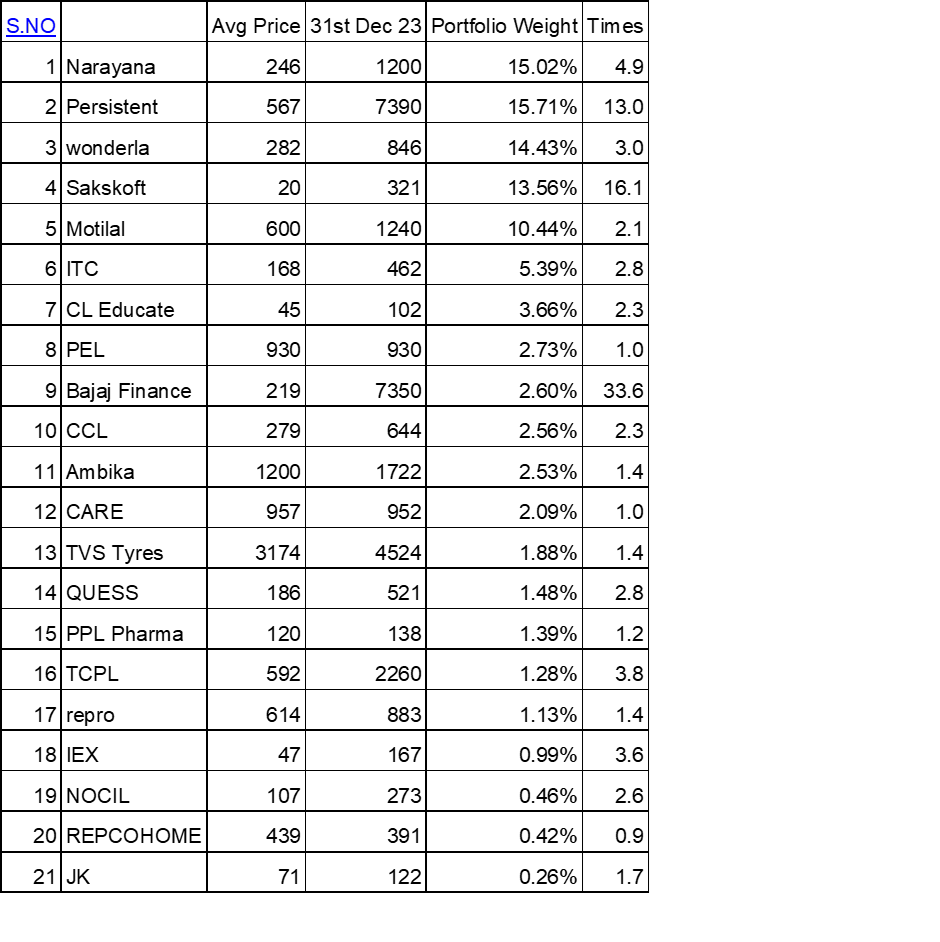

Hello happy to share my Portfolio. 95 % of my net worth is stocks. 5% in Bank and I have one house which I don’t count in my net worth.

Spend 9 years in Investing and started allocating more and more to stocks as I gained confidence. On Dec 31st my stock returns were 25 % XIRR plus Dividends. I don’t sell very often hence my portfolio turnover is very very low. I designed it in such a way that I don’t have to hunt for new ideas as i am working and work takes a lot of time. You can blame me for being buy-and-hold. There is no right way to earn good returns but yes there are things to avoid. I have never over paid learned deeply by studying warren and when i did in 2018 have paid a price for good business have suffered.

I am sharing this for educational purposes. I am not an advisor etc. I see lot of people doing direct investing without proper training and playing with derivatives. Please take time to understand till that time put in SIP NIFTY 500 investing monthly.

Amit ji, great to see an XIRR of 25% over such a long period of 9 years. Pl.it would be helpful if you could share your rational for picking these stocks and also how you retain and maintain the stamina for holding the stocks over such a long time period especially when their are steep market falls like 38% down in Covid time. Lastly what is your exit strategy? Your inputs would be highly guiding for an ammeter investors like us.

Hi @amitverma21, thank you for sharing your portfolio and many congratulations for the great compounding you have been able to achieve.

I would be really interested in knowing your thoughts and process which helped you in identifying multibaggers like Persistent, Bajaj Finance etc very early in their run.

I am also trying to identify some early stage winners but suffer from investing “too less” and hence having lower allocation to these new and exciting ideas.

Would be great to know the rationale and process you follow!

How did I Hold for long periods : I truly believe I am part owner of these businesses and people who make the most money are always business owners ( They are concentrated and have very long holding periods). It is the most difficult habit especially when stock prices are not reflecting the business change. For e.g. it was easy holding Bajaj Finance from 2014 to 2018 while Saksoft nothing happened to stock price for over 4 to 5 years and i bought the business with 5 times Free cash flow . I was buying 40 % ROCE business at 1 time Book.

I buy businesses that have some competitive advantage and have ROE over 20 % and then buy them cheap like when no one is buying them and then hold them. One model I use is to think of business as a growing FD (Owner earnings i-e- Free cash flow yield 1/ FCF ). off course you need to know if business cashflows will increase in the Future.

Most people are buying stocks i am buying partnerships with businesses and hence analysis of business and owner ( your partner ) is most important and then buying them cheaply gives you safety that you will not lose your money.

As I invested in Microcaps and small caps 2018 to 2019 was a bigger fall and more difficult for me than Covid fall. COVID-19 I was an experienced investor and bought truckloads of good companies like Persistent, Wonderla Motilal, Saksoft etc.

Bajaj Finance was beginner’s luck but I bought it 15 times Earnings, it was a play on Indian consumer’s spending and it was like FMCG stock for me. It is also my biggest mistake I did not add as it became expensive due to my framework of not paying. Stock is up 33 times and gives me a dividend yield of 15 %.

Look for high ROCE businesses, see their EBITA margins are constant (which means they have some pricing power), and buy them less than 10 times FCF ( FD is 7 % i.e. 15 times FCF). You will not find many ideas but that’s the whole point. Learning about promoters is not easy but you will know over period of time.

Mudit these are things floated by TV and Mutual funds as they have to come every day and speak. Just plainly ignore large caps and small caps etc etc. See the opportunity size and think about how the business will capture it. I was mostly in small caps or microcaps with the assumption that they have first-generation promoters who are driving business. Microcap does not mean they will grow faster and large cap does not mean they cannot fall 75 %. Look what happened in the US

Performance is not consistent. it is CAGR which will keep changing depending upon the mood of the market. I look at the profit growth of the company to measure my portfolio value rather than stock prices.

Buffet says you should not look at price first (Marketcap) as it distorts your mind but unfortunately, if you do screen that is the first thing that comes to you. The best option is if u heard about good business you pick up annual reports then try to value the company and then go to the screen to check.

Sizing: It has evolved I had 10 %, 5 %, and then 1 % bucket. But I generally stop at 15 %. I believe you should do at least 3 to 4 % because if the stock price climbs with my framework you will get stuck with a 1 % allocation. For the first five years don’t go over 3 % as you can make mistakes, learn, and become concentrated. My largest muli-baggers were all small allocations.

Hi Amit… thanks for sharing… when did you start your investing journey and I am speaking of when you learned from your mistakes and never looked back? You mention 2018 in your post but is that the starting point?

I started investing in 2013 but was small amounts compared to my capital but by 2016 I was putting a large amount of my savings into direct stocks. I have been reading business newspapers since i was in class 11th but in 2014 I found Warren Buffet’s letters and books and then I was spending all my free time reading and analyzing companies. I don’t feel bored and investing is my passion. I don’t care about the results XIRR etc but love the whole process. Investing in the end is very simple but not easy. You learn every day.

Mistakes are only known after 5 years and you keep making new ones. So in the 2017 bull run, i invested money in some cheap companies but the good thing was I had put small amounts like Poddar Housing and Sintex. so learned the lesson that useless business no matter how cheap you buy will give you zero even in the long term.

this is the problem in churning portfolio reinvestment risk if you end up in a company like Poddar or Yes Bank, your result will be very bad. anything multiplied by zero is Zero (even if you 100X).

It is easier to say what not to do than what is good.

for me, the protection of capital is my first job as 95% of my worth is in stocks. I will still make mistakes but should not be out of greed.

Thank you for your response… yes… you learn a lot from your mistakes and of course position sizing is an important element of being able to sleep peacefully in most days without having to open charts or other websites…

Persistent systems Very good numbers was planning to trim but they still growing better than other companies. Vaulation wise currently 30 % more expensive then my calcualtion. ROCE is 33 % very good dont have equivalent investments in India. Dividend yield 9 % and growing. This can be viewed as withrawing money each year. You should add to your companies as they peform did not do on this one. Hopefully will learn.

To analyze your company performance you should look at normalized ROCE or ROE to understand if company is still worth staying. An simple FD of 6 % will still show your profits increase by 6 % each year but it is not good investment.

As Mr Kedia says Investment is process of regrets if you sell you will regret and buy something you may regret. Lets see

Added HDFC Bank for tracking position at 1 %. Dividends money invested in HDFC bank. ROE of 16 % available at 2.5 times book. So 8 % Bond and they can grow EPS at 15 % and next year PE HDFC Bank is available at 14 times forward earnings. It is easy to 2x to 3x in the next 5 years. EPS doubles and then maybe multiple expands 50 %.

Although management is guiding over the next 10 years they can reduce the cost to income from 40 % to 30 % which means they grow profits even higher.

I would like to more less than 2 times book or less than 1200.

To find the reasonable or conservative value of a company you can think of it like a Bond (Debt) so if you buy something at 2 times book doing 16 % ROE means you are buying an 8 % bond. This assumes the company does not grow its earnings and secondly company is so good that its earnings will not drop (the market usually has a lot of trust with some history) so some large funds can think they are getting this cheap vs debt funds and if the earnings grow it will be plus. So this is the minimum value a company should trade at, off course in the short-term market can do anything but if you are buying like this or lower you will not lose money in the long term but have a big upside if the company performs as multiple will expand and earnings will also grow.

You will not get many opportunities like this but you don’t need many as you don’t have to sell, patience is the key

Hi @amitverma21, thanks for sharing this. Its a new perspective to look at from numbers point of view.

Just wanted to check, do you use this criteria for high growth (real or expected) companies as well? Such as Varun Beverages, Kaynes etc in today’s times. Because usually these companies trade at higher Book Value and hence the yield would always be lower in the higher growth phase

I am a bit conservative in factoring in large growth expectations. Book value for most companies is not the right measure as the value of services companies or technology companies lies in intangibles like quality of people, management, brand, etc. Having said that how the company is performing is always measured in terms of ROE or ROCE which is again measured against book value. According to Buffet, you should track ROE every year to know if the company is good or bad not only earnings growth.

I learned from Buffet that this is the model he uses to assess even brands like he bought Kraft Heinz for example Kraft Heinz was a 120 % ROE business then you can pay 10 times the book value it becomes a 12 % return for you.

Everyone says BFSI company’s Book value is the right measure but I do look at Book value for even services companies.

So I am not great at paying high multiples as I need to be very sure high growth will sustain for 10 years. All my mistakes were paying fair value to companies in 2017 but some people can identify Varun or Kaynes and ride the whole journey.

Your returns will equal to ROCE over long period of time if Multiples remain same

In 2024

In My international portfolio added more to Prosus - Listed in Europe it is a play on Chinese Tencent, PDD almost all tech companies in China. It is available at 6 times earnings

Added to Piramal Enterprises - Added Dividend money and sold J&K and South Indian bank as PEL looks better. PEL has not delivered for the last 5 years but looks ok from risk and reward.