I have found this concall transcript . In this pdf search for pharma word and you will get the info

1 Like

Pharma CDMO is difficult compared to Agri CDMO. I have read PI Industries con calls right from FY17 onwards & they have been discussing opportunities in Pharma way before they did the QIP itself. They have been trying to venture into Pharma CDMO for almost 6-7 years now.

Now, in a TV interview to discuss Q2FY23 results, Mayank Singal hinted that something concrete will definitely come up by Q3FY23 on the Pharma acquisition side. However, still there is nothing concrete on that side.

I do acknowledge that QIP proceeds is lying idle which is depressing the ROE, ROCE numbers, however we can appreciate that they haven’t used the proceeds funding any lower margin business & are still waiting for the right inorganic opportunity in the Pharma side. Also, they have been doing some smaller projects organically.

With the track record of the management execution, something good should come up in next 2 quarters is what I believe.

Disc - Invested & Biased.

7 Likes

PI Industries makes acquisitions

PI Industries acquisition.pdf (635.5 KB)

in API and CDMO space

11 Likes

The purchase consideration will be paid in cash and funded from the completed Qualified Institutional Placement (QIP) proceeds and internal accruals. ![]()

Both acquisitions are expected to be earnings accretive with immediate effect.

1 Like

How much amount they are paying in total for these acquisitions? I think QIP proceeds were 2000 crores. And is there any chance that it may get cancelled like last time?

The total is around 925 crores.

1 Like

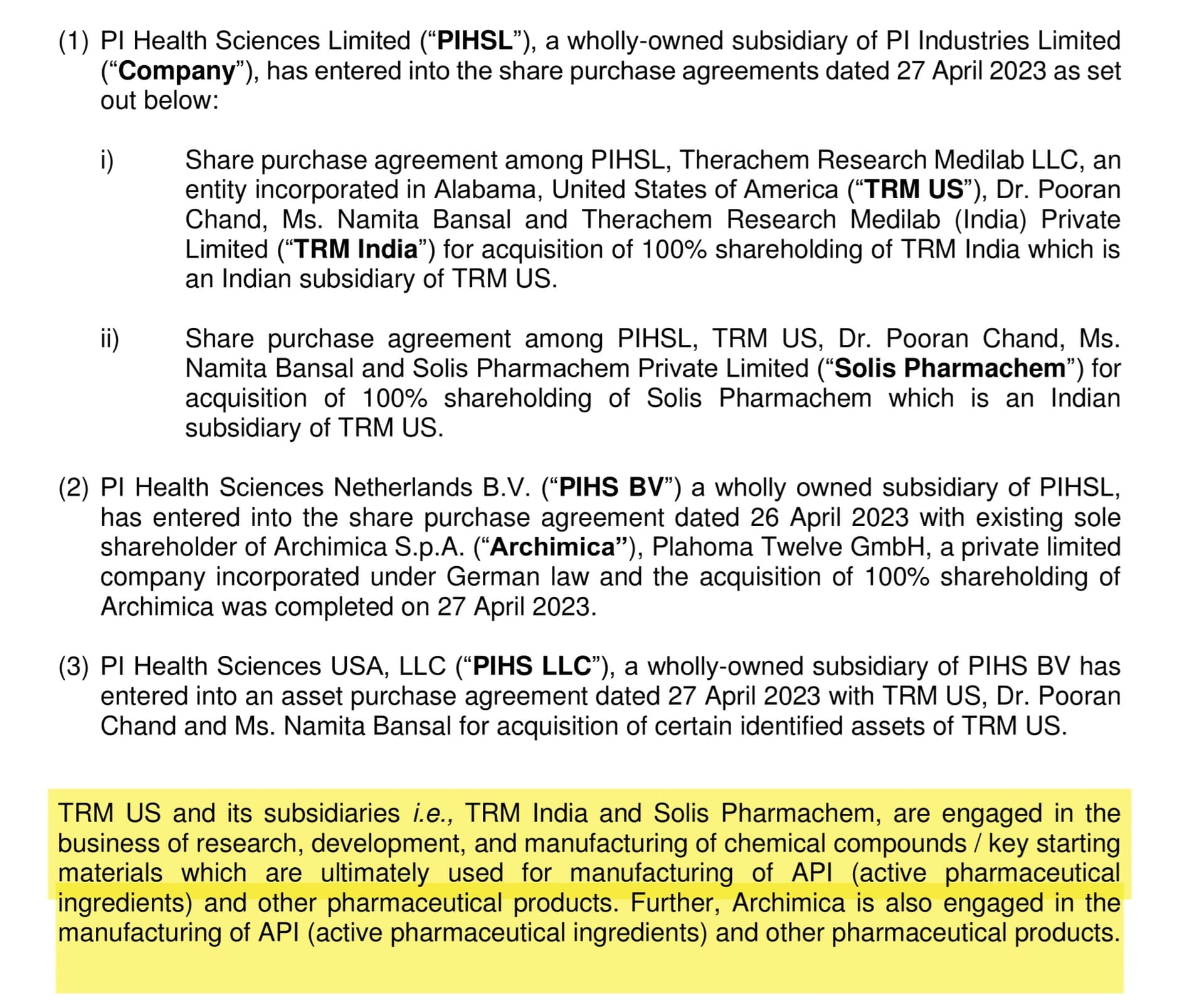

Some notes on recently acquired cos

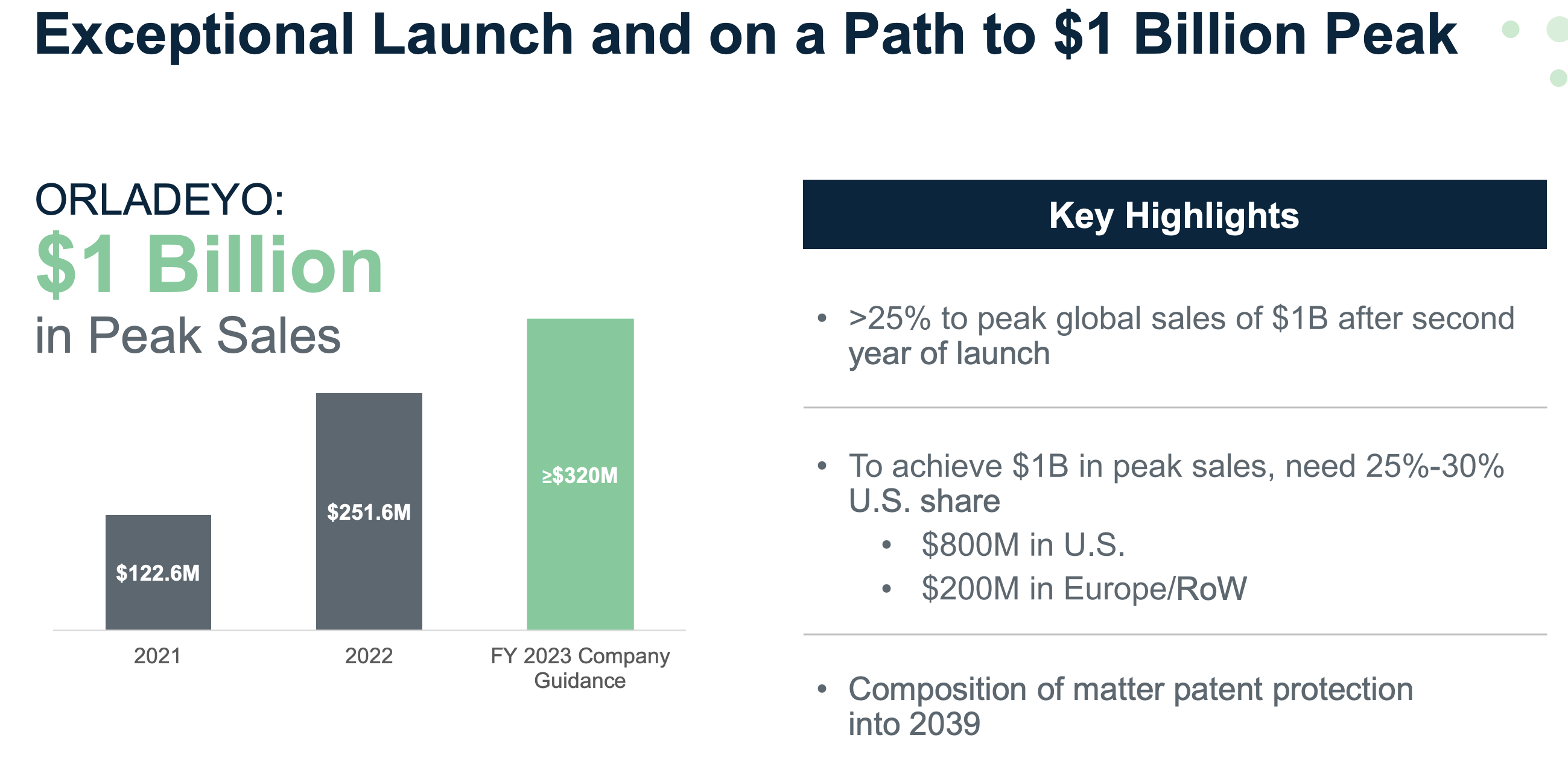

Therachem research medilab: is an intermediate supplier, specializing in phenol, pyridine and benzene based intermediates. Their large customers are Biocryst Pharmaceuticals (NASDAQ: BCRX) and Cambrex Karlskoga (based out of Sweden).

Biocryst Pharma has one commercialized molecule called ORLADEYO (berotralstat) which is scaling up rapidly. I think Therachem provides a couple of intermediates for this molecule.

A very nice presentation on the co. from the JP Morgan summit.

https://ir.biocryst.com/static-files/7992d27a-9330-4e12-a634-cfa8152ea6a2

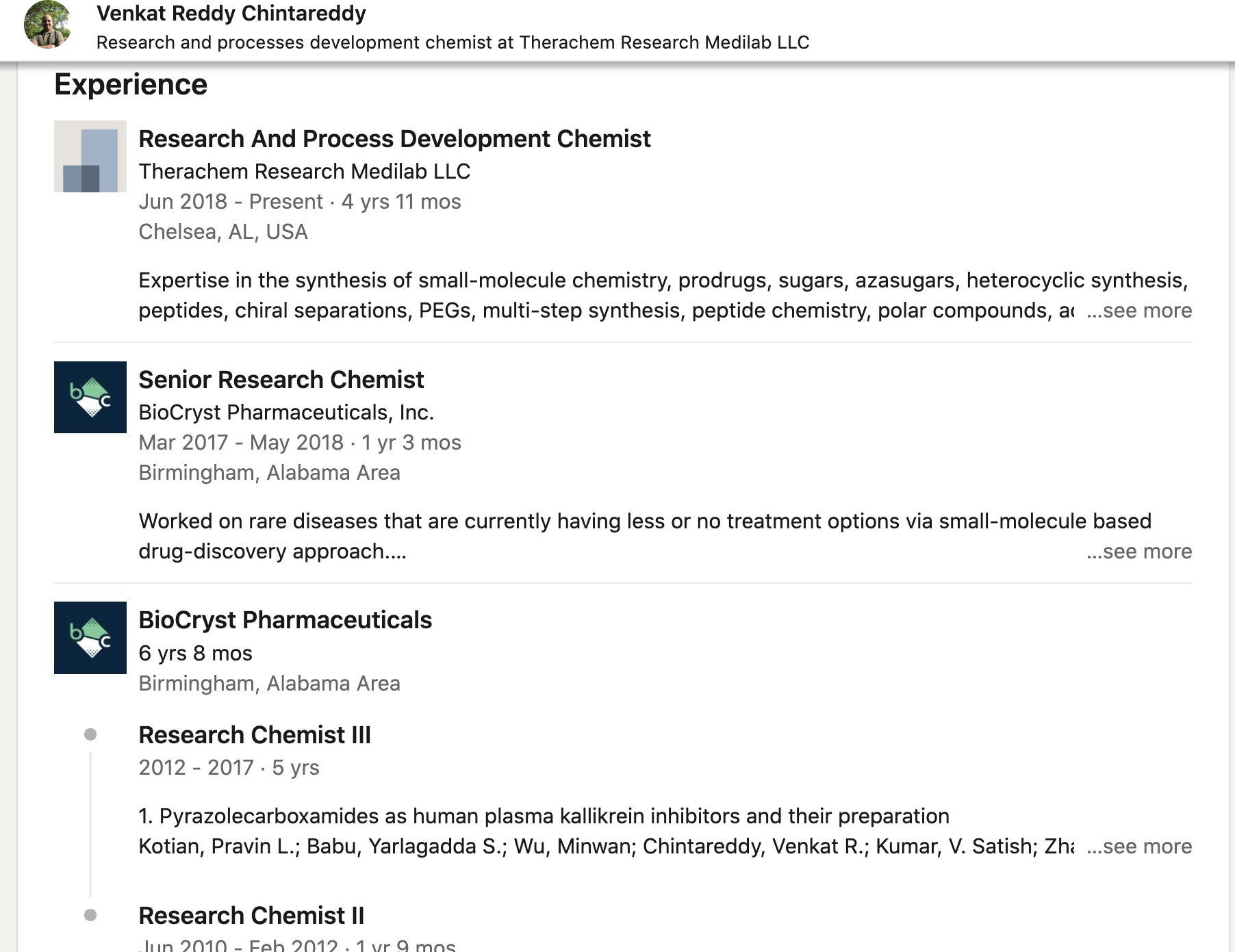

Venkat Reddy is a common link between the Biocryst and Therachem, he used to work in Biocryst and later moved on to Therachem.

Cambrex Karlskoga is a generic API supplier based out of Sweden. Their product basket is available at the link below (looks like generic APIs) and Therachem supplies intermediates to them.

https://www.cambrex.com/drug-substance/generic-apis/product-catalogue/

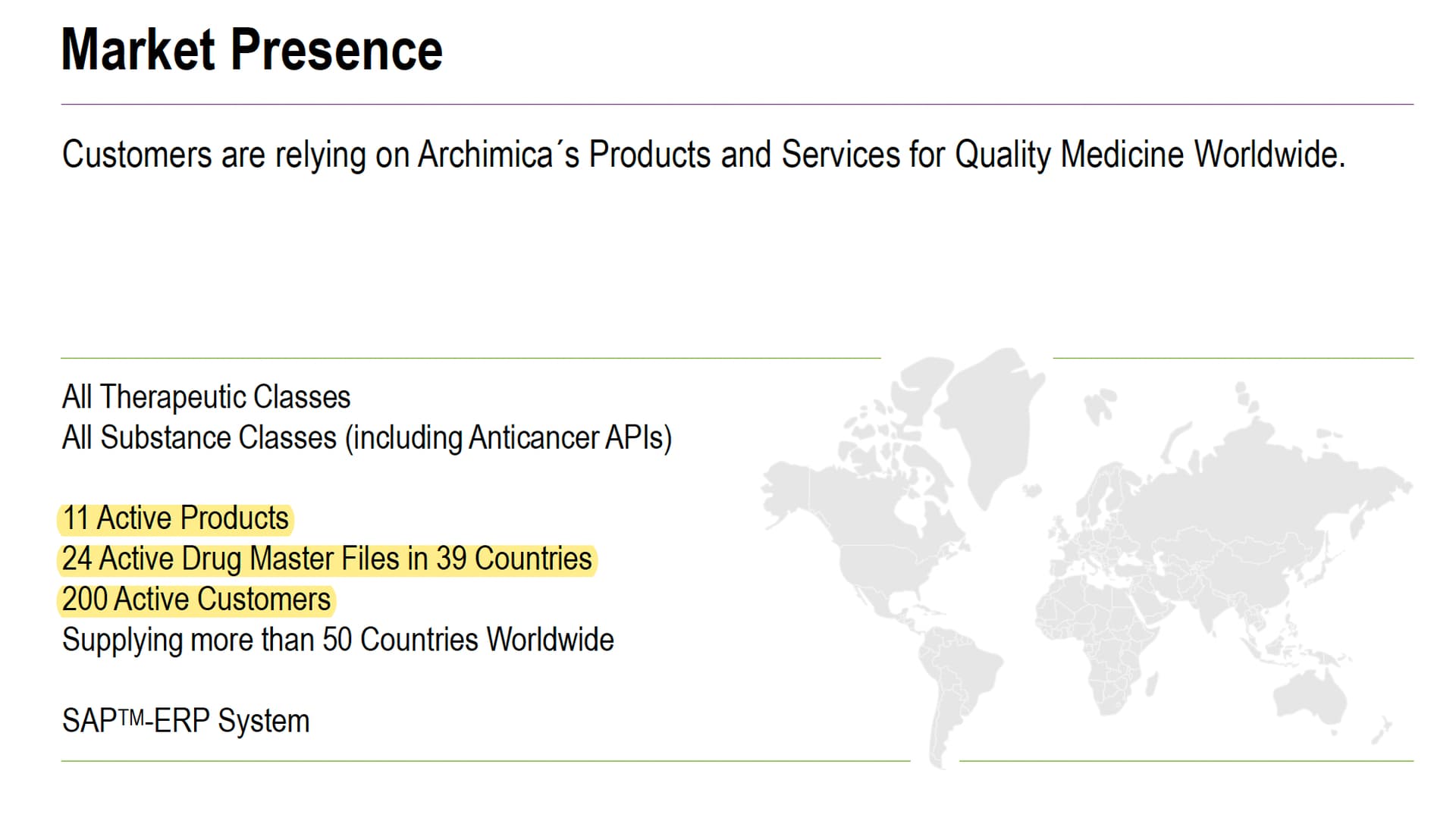

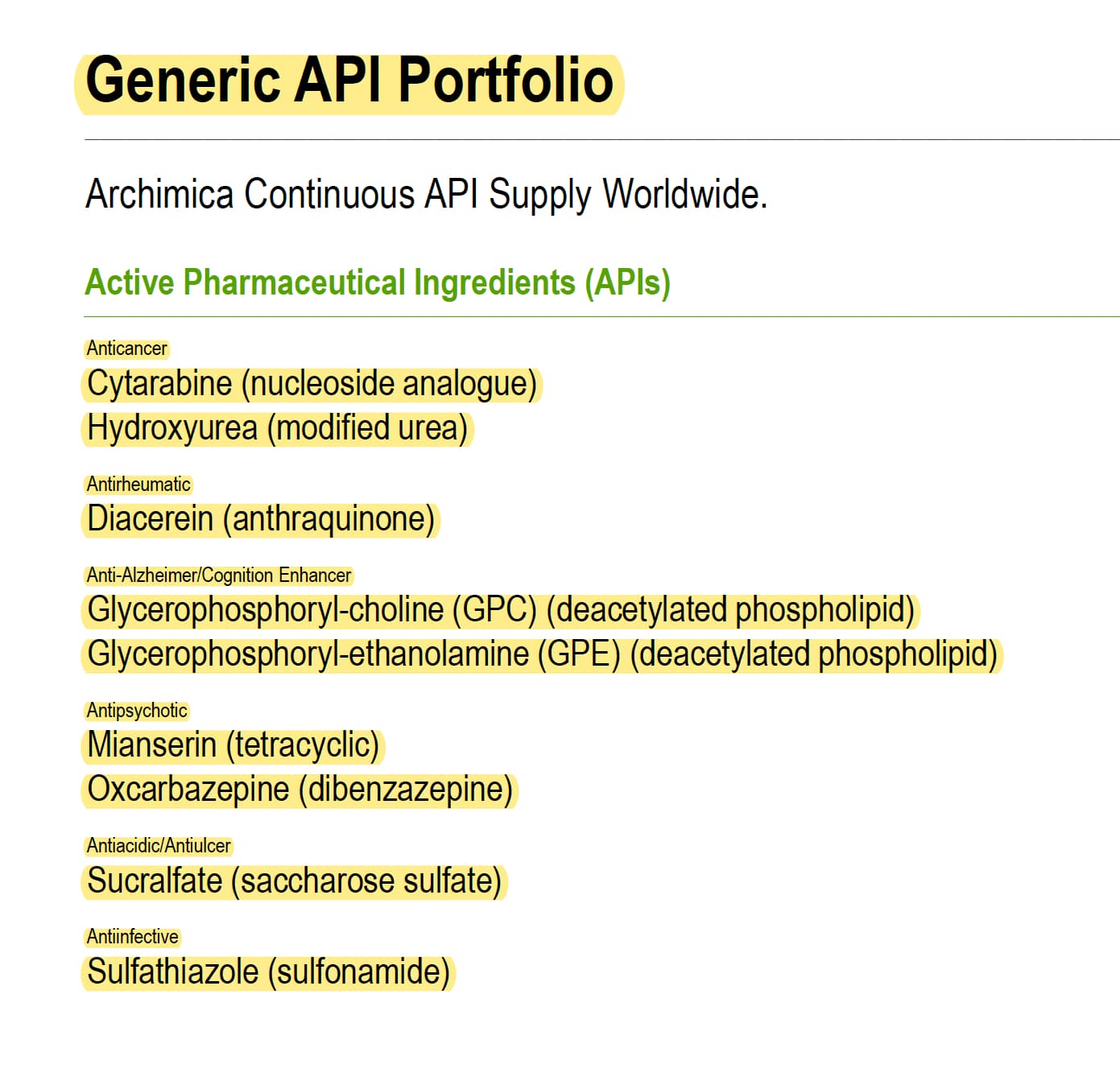

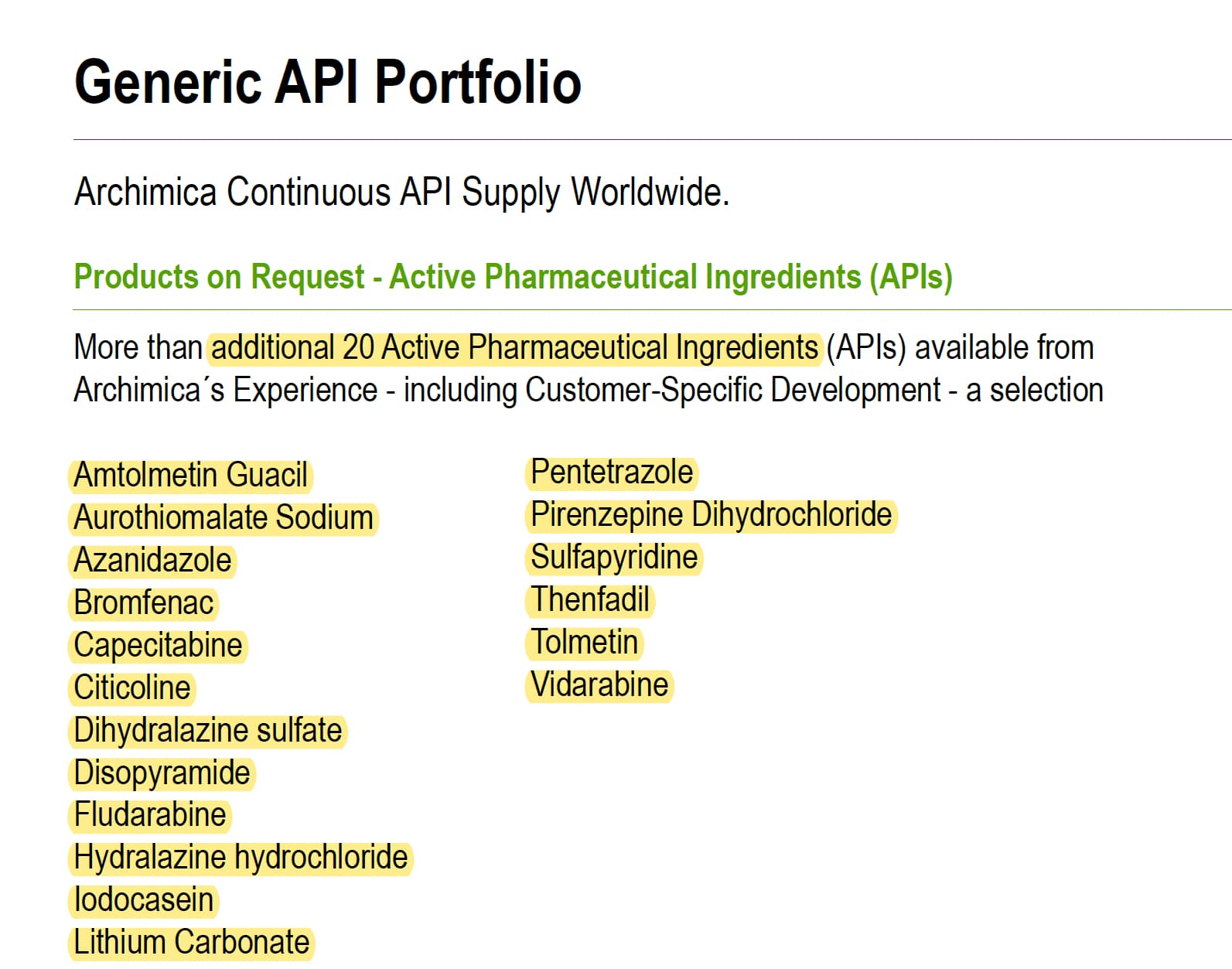

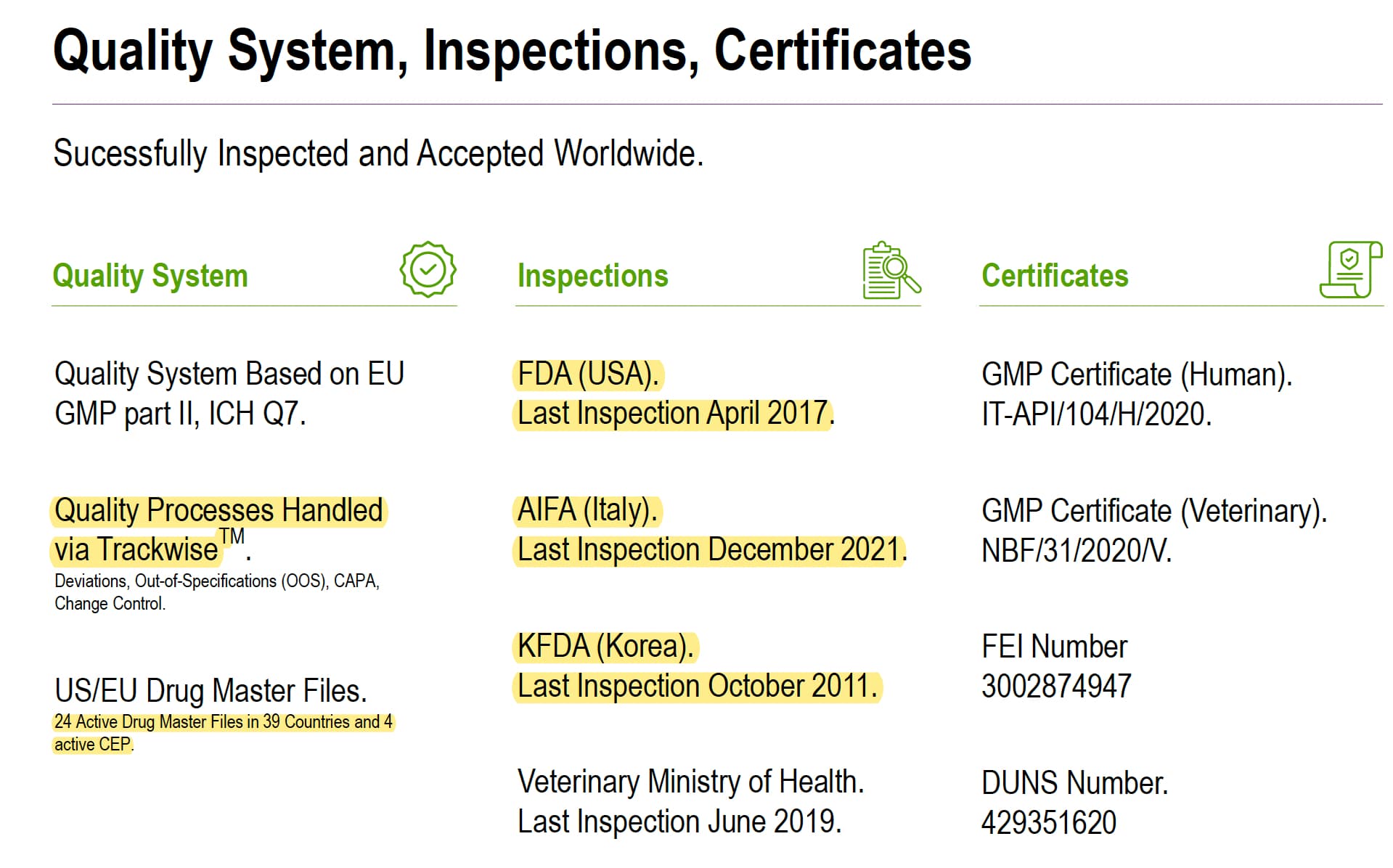

The second acquired co Archimica is a generic API manufacturer, with 24 DMFs, 11 commercialized products and 200 customers.

Company has a history of change in ownership over years.

Product basket

They have certifications from USA, Italy and Korea.

Disclosure: Invested (position size here, no transactions in last-30 days)

32 Likes

What will be estimated turnover for the FY 2023-24 ?

Discl: Invested and biased

Disc: invested around 3% of PF

5 Likes

PI Industries call on Pharma Acquisition

TRM: 3.57x EV/EBITDA of Mar-22 on base consideration

Archimica: 5.3x EV/EBITDA Dec-22

-

Acquisitions are made through the wholly owned subsidiary of PI Industries, the purchase consideration will be paid in cash from QIP funds. Both acquisitions are expected to be earnings accretive with immediate effect

-

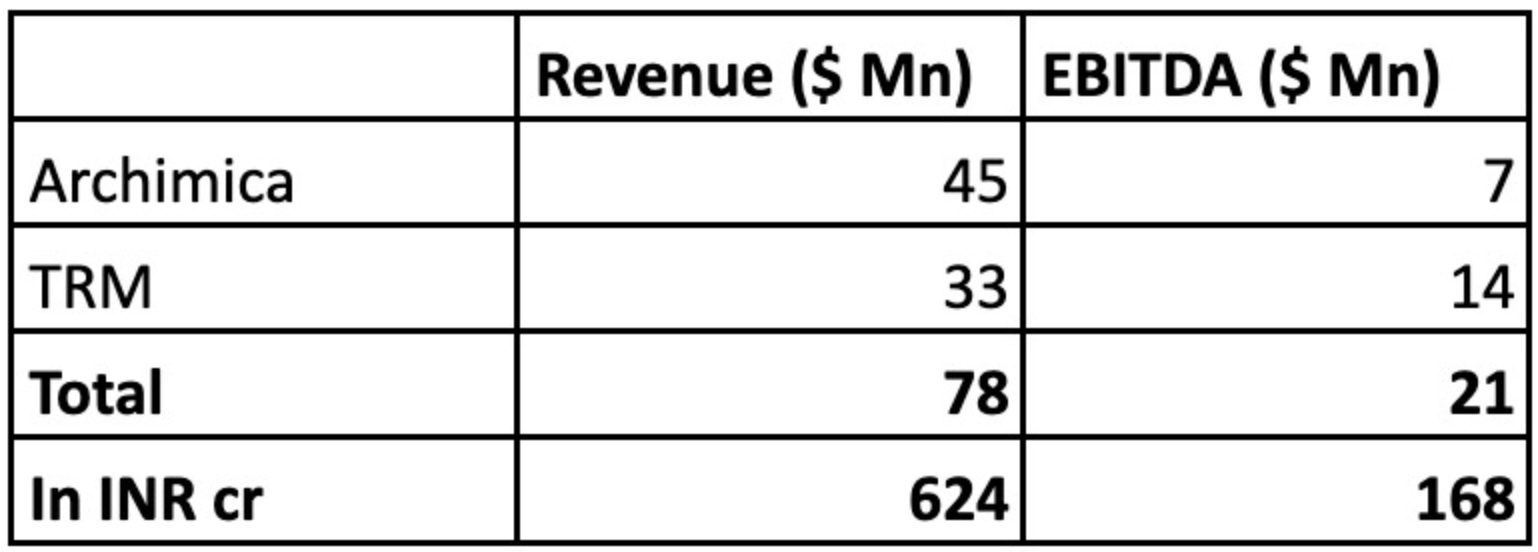

TRM’s R&D team works closely with marquee publicly listed US biotech companies and big pharma companies based in Asia-Pacific in developing their product pipeline. It had consolidated revenue of USD 33 Mn & EBITDA of $14 Mn in FY22.

-

Archimica is an Italy-based, highly reputable small molecule API manufacturer and a CDMO servicing over 60 customers in more than 30 countries. It is certified by USFDA and AIFA among others. Archimica had revenue of $45 Mn with EBITDA of $7 Mn for the year ended 31st December 2022.

-

Acquisition of Archimica is completed on 22-Apr-23; Expect to close the acquisition of TRM by end of May 2023.

-

Archimica has 24 DMF out of which 12 products are currently active; currently 50% capacity is utilised for niche API and 50% is idle on which PI can work on. PI might do some strategic capex based on their understanding of business. In Archimica PI will retain the leadership and team and they will work them to grow the organization.

-

Archimica has more than 60 clients and TRM has 10 clients; TRM is currently working on under patent products only, there are no generic products in TRM. In Archimica they are working on niche API and they are all generic.

-

PI has planned for $10 to 15 Mn capex per annum over next 2 years for the pharma division.

-

During FY22 there was commercialisation of molecules for TRM and hence its revenue grew by more than 2x over the previous year; there are also some fixed term contracts (1 to 3 years) with certain customers.

-

These 2 companies have 3 R&D centers in different countries, so 1 is in the US , another is in Europe and one in India. They have clients for each center as some customers want the development in the US, some want in India and some in Europe; along with that Hyderabad center will be complimentary for all those 3 centers.

-

TRM is working with the customers who are dealing with the biologics, TRM is supplying the building blocks to them.

-

TRM is currently working at 40 to 50% capacity utilisation; so capacity is not a constraint for growth currently.

-

The current focus for these acquisitions is scaling up the revenue rather than focusing on margins. Expecting to more than double the current revenue of these companies in the next 3 to 4 years.

-

Revenue split between CDMO and API - for Archimica it is 20:80; and for TRM 100% is CDMO.

22 Likes

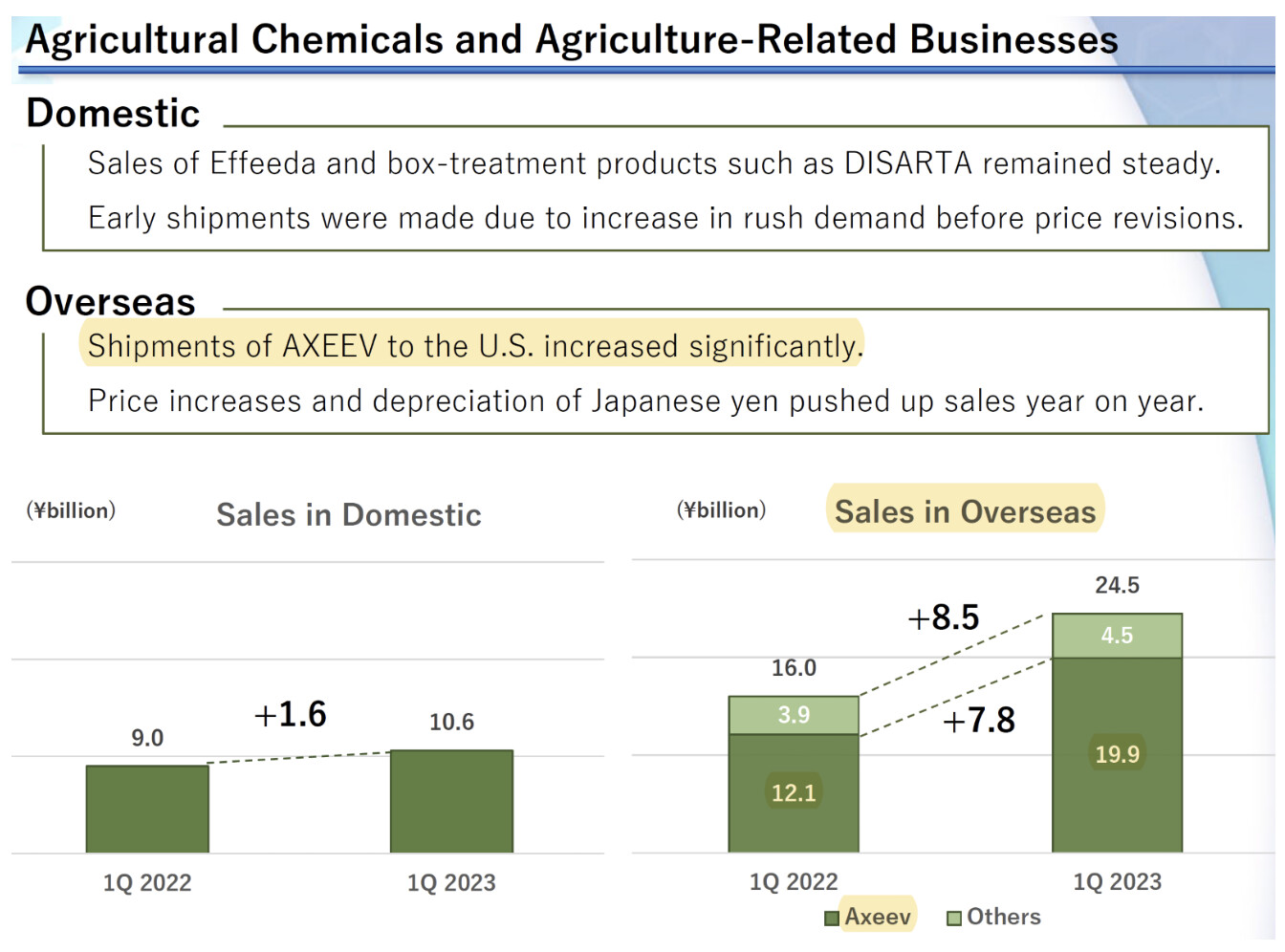

FY23Q4 concall notes

- 26% FY23 export growth: 11% volume + 15% price, currency and product mix

- 12% FY23 domestic growth: 8% volume + 4% price, currency and product mix

- Huge reduction in working capital (from 103 days in FY22 to 79 days in FY23). There won’t be further improvement

- Not witnessing any significant change in demand of innovative products

- Expect 18-20% growth going forward (all driven by volume growth) and improvement in margins in FY24

- Revenue recognition is a mix of revenue booking at time of shipping and revenue booking when customer gets the shipment

- 2% lower gross margin (vs Q3) was due to change in product mix

- Agchem capex: 300 cr. carried forward from FY23 + 600 cr. Expect 900 cr. of capex going forward (time frame not specified). In FY23, did capex of 339 cr. (vs 500 cr. guidance in FY22Q4)

- CSM: 17-18% revenue from products launched in last 4-5 years. This was 16-17% in FY22

- Pharma will contribute 550-600 cr. revenues in FY24 at 15-18% EBITDA margins (depending on when transactions get closed and nos get consolidated with PI)

- Pharma capex: Expect $10-12mn (not yet finalized)

- Kumiai achieved 64% growth in Axeev (pyroxasulfone) in last quarter

Disclosure: Invested (position size here, no transactions in last-30 days)

16 Likes

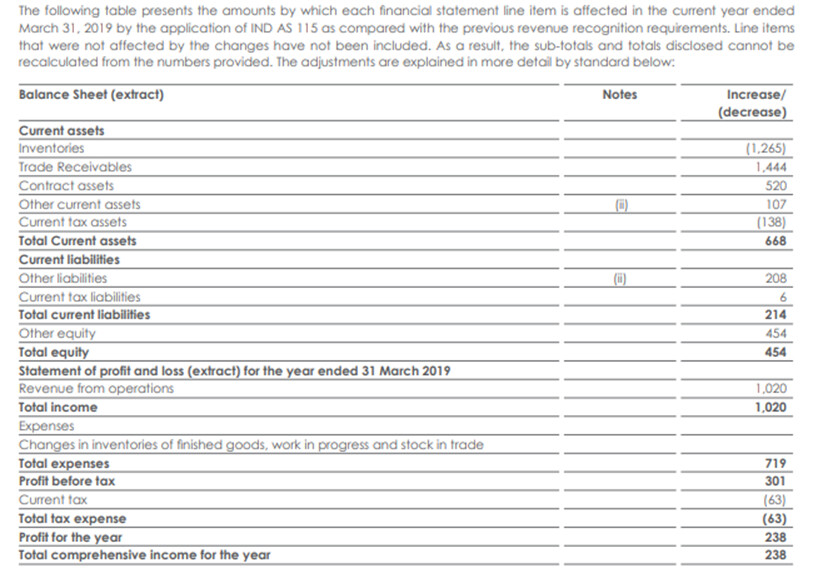

While the rest of the ag-chem sector faces headwinds, the PI juggernaut continues. For the first time, analysts quizzed the management on revenue recognition, as if finding the results too good to be true. It may be noted that w.e.f. 1st April 2018, PI adopted Ind AS 115 for the CSM segment, which allows the company to recognize revenue “over a period of time” as in case of contracts rather than “transfer of control” which is the usual norm for physical goods.

(Extract from Annual Report for FY2018-19)

Essentially, what this change does is it allows the company to book revenue as soon as goods are produced without waiting for shipment. This is perfectly legitimate though more aggressive (thanks to @zygo23554 for pointing this out and explaining neatly here. This change resulted in a Rs.23.8 crore increase in profit that year, but does not affect the YoY growth thereafter. So long as PI does not face any reversal of sales due to customer’s refusal to lift goods that have already been produced, this will have to be considered okay.

22 Likes

Hi @Worldlywiseinvestors , you mentioned that due to stocking issue in 2016-2019 , things went temporarily wrong . Can you please tell what went wrong with PI Ind at that time ? Is it due to GST?

Destocking which took place during that time + the end customers I.e. the innovators went through the cycle of M&A. This created a lot of uncertainty which impacted the growth rates for end manufacturers like Pi, Srf and Deccan.

Seeing similar destocking in generics Agro. Can it move over to innovator agrochemical molecules. Always possible as most of the industries are cyclical.

9 Likes

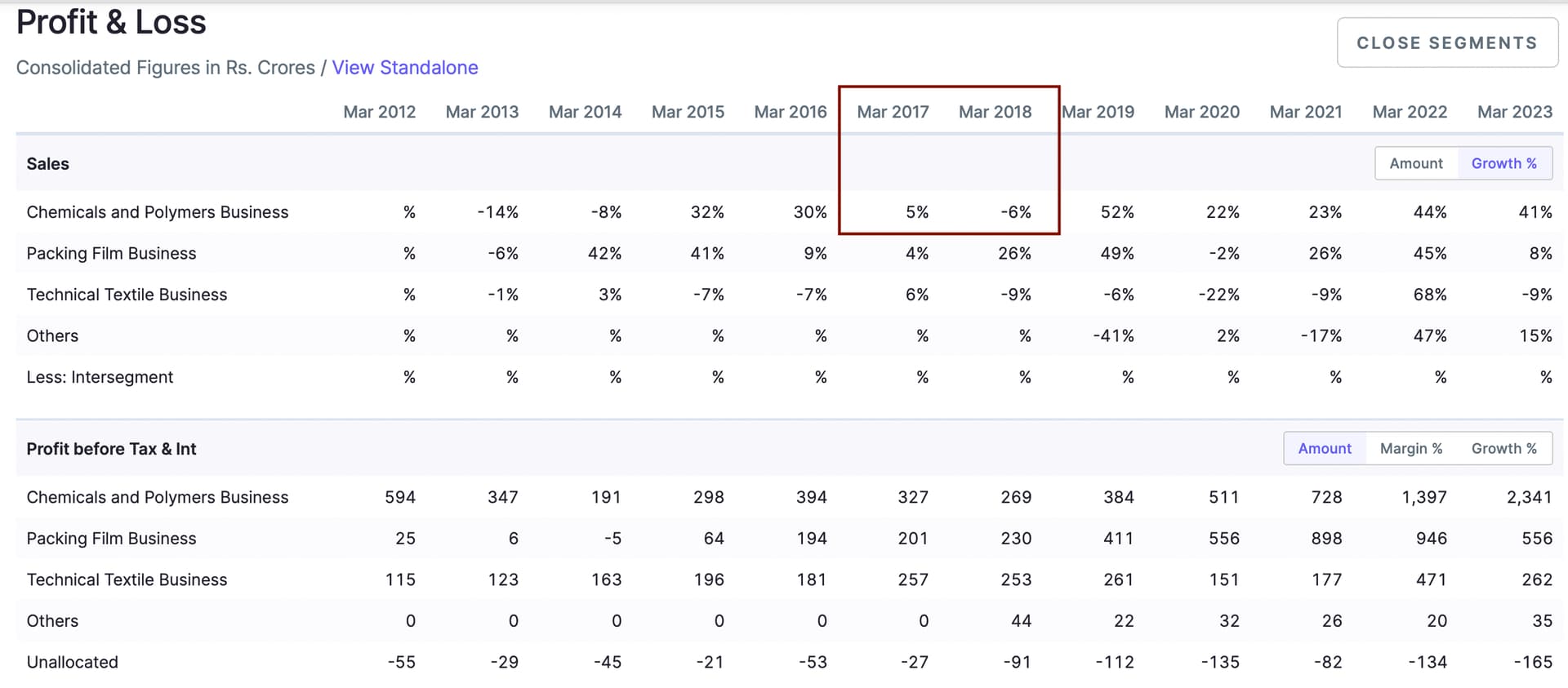

Check PI’s growth rate in that period:-

Check SRF’s Growth rate during that period in chemical division:-

17 Likes

The Annual Report is out and I see this -

PI aims for 18-20 percent revenue growth with a focus on R&D, new product launches, and capacity expansion.

PI Industries is diversifying its business through strategic acquisitions in the Pharmaceutical and CDMO (Contract Development and Manufacturing Organization) sectors.

The company has set specific sustainability objectives to achieve by the year 2025. They plan to increase their use of renewable energy to 20% of their total energy consumption and reduce specific CO2 emissions, hazardous waste disposal, and freshwater consumption by 25%.

To navigate the uncertain economic environment, the company will maintain strict but practical financial controls. They will persistently focus on optimizing costs and reducing waste. Additionally, effective risk management is a top priority for the company, and they will work to strengthen their internal processes to meet best practices across various functions.

8 Likes

This is usual rhetoric that all companies give about green energy, saving costs, risk management, financial controls etc…What is value addition here to P.I. story?

3 Likes

Right. There have excellent script writers available in the market and I have heard most of the companies outsource that. ![]()