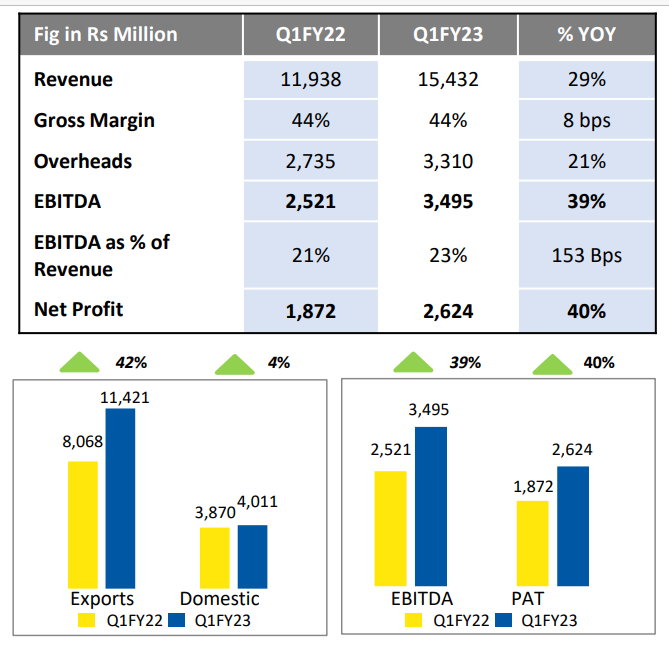

The Q1FY23 result is awesome. All thanks to whooping export growth!!

growth guidance from delivering 18-20% revenue growth to delivering 20%+ revenue growth.

The Q1FY23 result is awesome. All thanks to whooping export growth!!

growth guidance from delivering 18-20% revenue growth to delivering 20%+ revenue growth.

Can you link the source / twitter account. Seems like Exports CSM data was correct.

I’d have given already to some people who were asking for the source. But I don’t remember the name of that twitter account. But that person just got that data from some report. So that person won’t be helpful. It’s the agency that published the report.

Some pointers from the PI Industries Annual Report for FY2021-22:

Financial

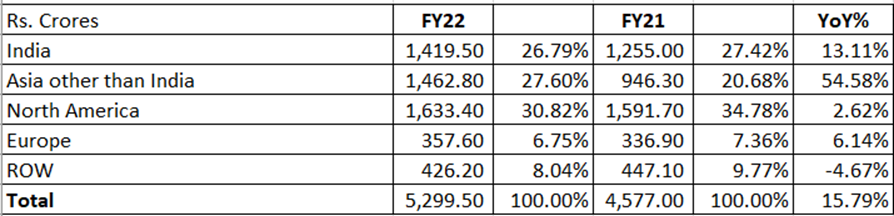

Consolidated Revenue from operations for the year was Rs.5,300 crore and PAT was Rs.844 crore. Revenue growth for the year was 16% and PAT growth was 14%. Operating margins stood steady at 22% while Cash Flow from Operations was down Rs.725 crore to Rs.529 crore, thanks to increased working capital requirements. Free cash stood at more than Rs.2150 crore.

More than 4 % of the income now comes from Subsidiaries. Main operating subsidiary is Jivagro, which houses the company’s horticulture business. Its revenues for the FY22 were Rs.282.1 crore with a PAT of Rs.15.6 crore.

Total CAPEX entailed in FY 2021-22 was Rs.320 crore and assets capitalised during the year were Rs.481 crore. Capital WIP now is just Rs.64 crore which implies much less capex will be incurred in the current year.

Business

Company has five formulation facilities and 15 multipurpose plants under its four manufacturing locations, 400 scientists and researchers and deep symbiotic relationships with over 20 global innovators.

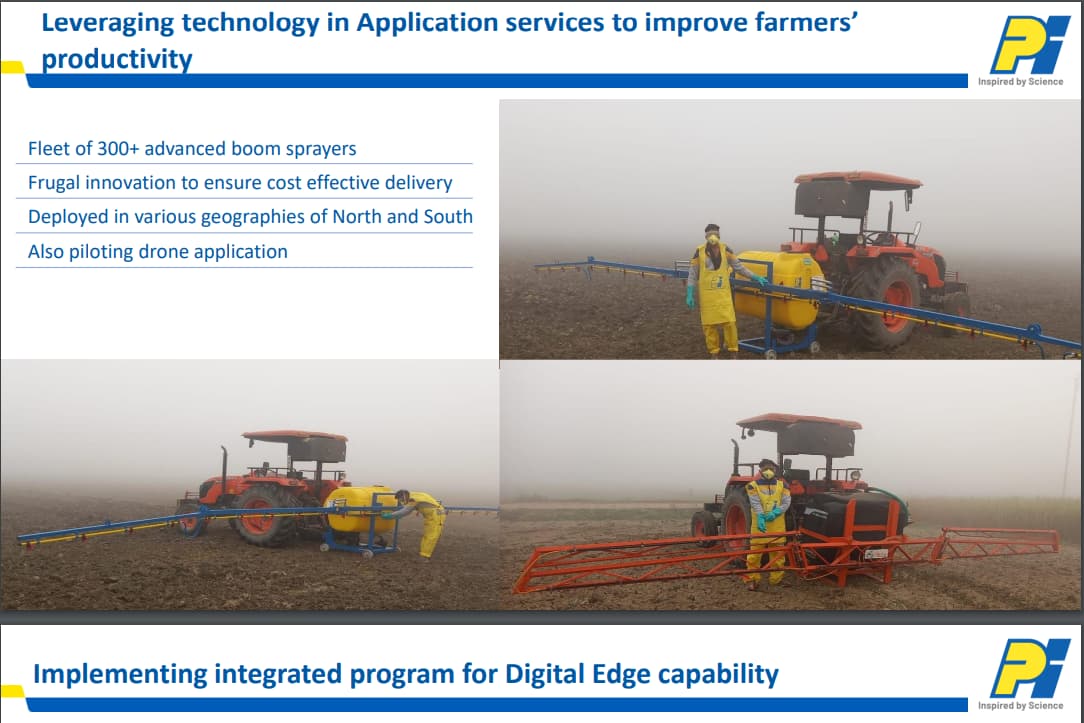

Piloted a drone application. Last year, company made a successful foray into electronics chemicals.

During the year, 2 additional Multi-Purpose Plants (MPPs) were fully commissioned. 2 new Electronic Chemicals were launched marking the company’s foray into this niche specialized field offering promising potential in future.

In CSM exports, the 9 new molecules commercialized were the highest in a single year. The company has also operationalized “Flow-Chemistry” at pilot level and also successfully commissioned manufacturing facility for MMH and established Azide chemistry at a commercial scale.

In domestic agri brands, PI received 3 regulatory approvals during the year, which also included the first product to receive MRL exemption in India.

Horticulture portfolio under Jivagro saw launch of 13 specialised brands at a go. This, by far, was the highest number of brand launches in a single year.

During the year, the R&D team worked upon more than 40 products at different development stages and pipeline has more than 20% non ag-chem products. PI crossed the milestone of having filed more than 130+ patents. Total R&D expenditure as a percentage of revenue was 2.71%.

The Company commissioned a pharma lab at Udaipur (Rajasthan) and is also working on technology scale up of novel catalysts, enzyme technology and green chemistry (ecoscale).

The company incorporated one wholly owned subsidiary having its registered office in the State of Rajasthan for carrying out pharma activities namely – PI Health Sciences Limited.

During the year under review, Isagro (Asia) Agrochemicals Private Limited business other than B2C got merged with PI Industries Limited

Regulatory delays in securing the approval for new products delayed many of the new launches during the year and has some impact on the business for the year.

Accounting

The Board declared an interim dividend of Rs. 3/- per equity share in February 2022. In addition, a final dividend of Rs. 3/- per equity share is recommended.

Promoter remuneration for Mr. Mayank Singhal is Rs.16.50 crore and Rs.29 lacs for Mr. Arvind Singhal. This is 2 % of the Consolidated PAT.

There is an unrealised loss on foreign currency transactions (Net) to the tune of Rs.60 crore in Cash Flow Statement compared to an unrealised gain of Rs.31 crore.

Provision for Bad and Doubtful debts & Advances is made for Rs.22.50 crore. This was Nil last year.

Disputed tax liabilities have increased from Rs.43 crore last year to Rs.106 this year.

There is one customer having revenue of Rs.1743.5 crore including an amount of Rs. 869 crore and Rs.874 crore arising from shipments to United States of America and Japan respectively.

Going ahead

The Annual Report says the company is likely to benefit from the maturing of its new product launches of the recent year.

In addition, the company is planning to launch 5 new products in the domestic markets in FY 2022-23.

Moreover, its focussed approach to horticulture segment through Jivagro coupled with a healthy pipeline of new launches shall support growth in domestic markets in FY 2022-23 and beyond.

With scheduled commercialisation of 7 new molecules and 2 new process innovations, the company is well placed to sustain its growth and profitability trends in FY2022-23.

Order book position continues to stay strong at $1.4 billion with high visibility growth for the next couple of years.

On bio-pesticides, the report says emergence of bio-pesticides is making a splash in the existing crop protection market. However, product features of bio-pesticides are so limited as compared with traditional CPC products that later has not gained popularity.

(Disc: Invested)

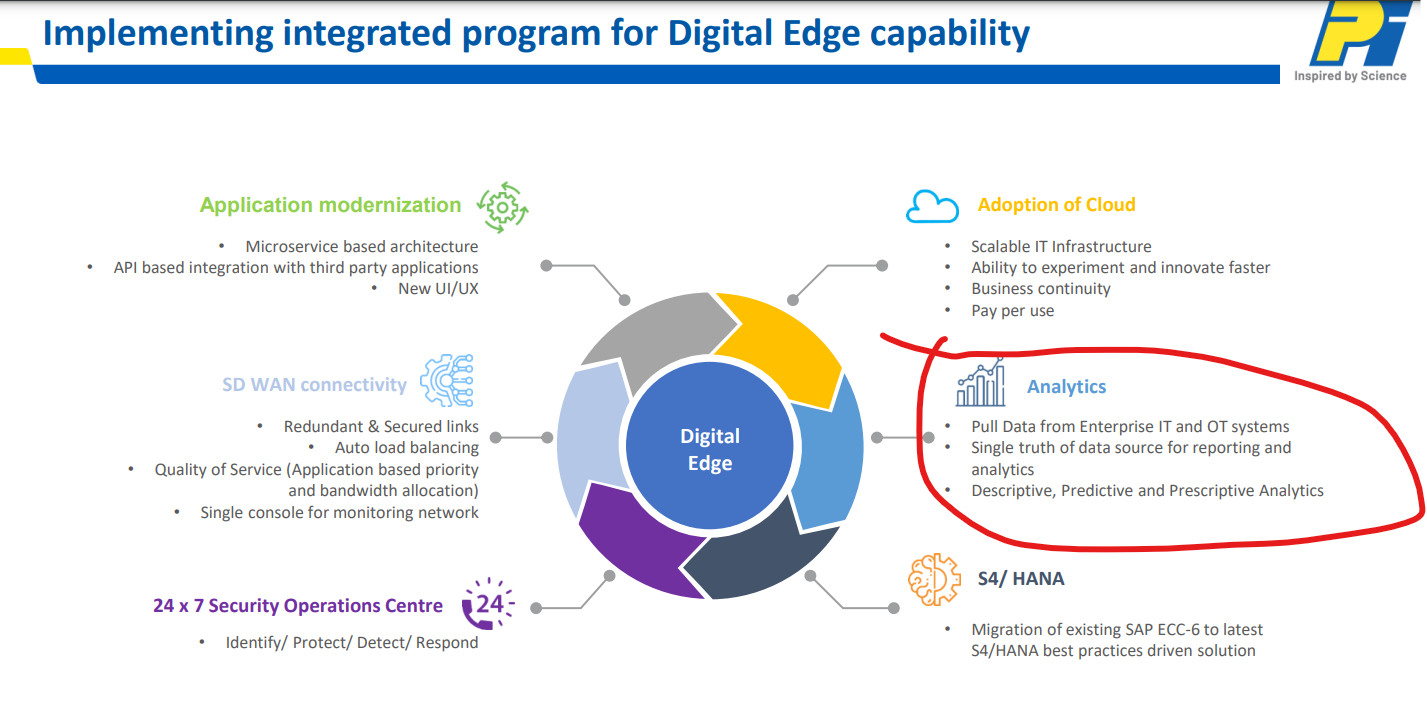

What stunned me in the AR also, the kind of spend , they are doing in IT and Digital

While , I was in another company, they were few of the companies, who enquired and shown interested in Connected Plants , way back in end 2019

On the right path of innovation. IT will cut across industrial domains.

Connected plants is the way to go since reactivity & quick response is essential to maximize the utilization of expensive machinery assets. We have implemented connected plants in most of the manufacturing process which enables us to move from breakdown → predictive → preventive maintenance

Such news are often speculative in nature and many times turn out to be false.

You are right. Priyanka Chigurupati said this is completely untrue and baseless.

Few days back I posted about some big guys came to know about increasing export of PI Industries because they have superior access to information. They are “Sell side”

Now they are claiming similar things for divis labs export degrowth.

https://twitter.com/Ankush__Agrawal/status/1579694923724783616?t=6YOcqz_svECAnhh-Wb4c3A&s=19

Here is a ss of from twitter which posted about it.

Thanks for bringing up. I too read the same thing last quarter and now similar information is being shared for Divis and Laurus.

There is always information edge between institution and retailers. Don’t know if the regulator can do something about it or not.

PI Industries - Capex guidance for FY23 was raised to ~ Rs 700 crore. They are looking to expand their export CSM business by venturing into adjacent segments. They are principally looking to enter pharma intermediates too. Apart from that, PI is looking at manufacturing electronic chemicals.

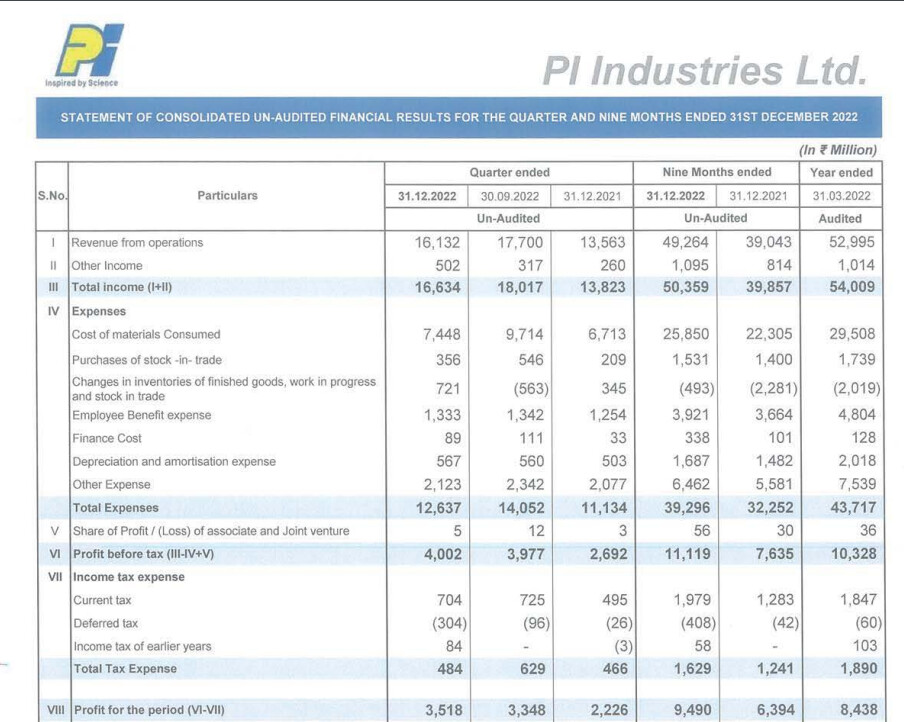

Excellent set of results posted by PI Industries. Management commentary will be crucial to see the growth going forward.

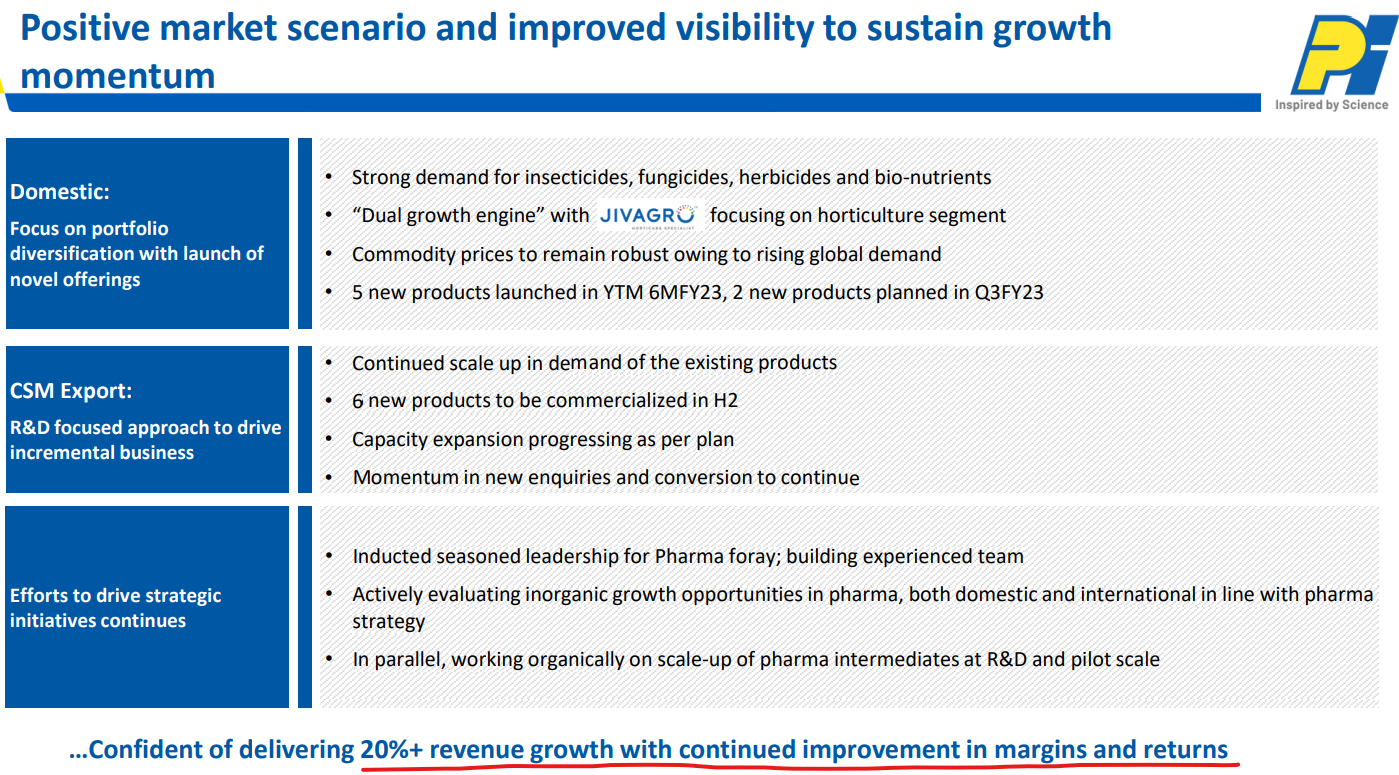

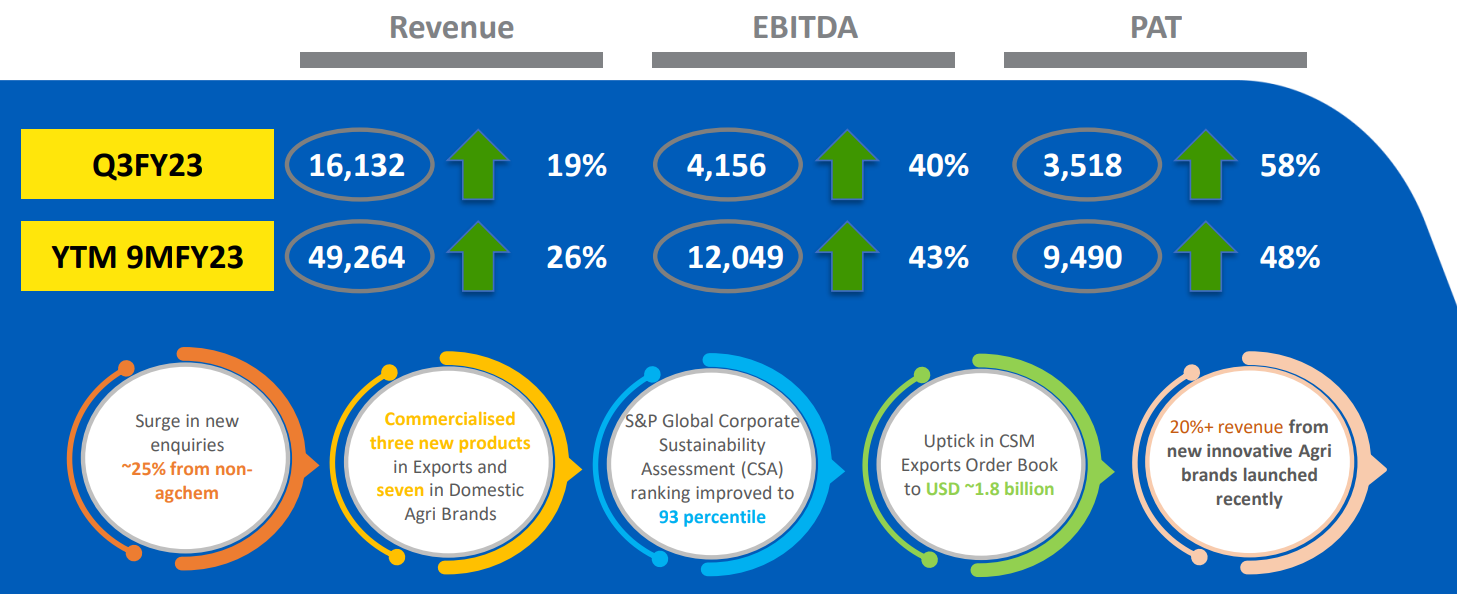

I read the con call transcript for Q3FY23 & below are the notes for the same.

EBITDA margins are at 26%, Gross Margins at 47% & management is confident of maintaining the same at 23-24% going forward. The increase in EBITDA margins are mostly due to favourable product mix wherein 10-12 molecules were commercialized in the last 2.5 years & operation leverage kicking in.

Order book stands at 1.8 USD Bn. Management is confident of delivering 20% growth for the year with continued improvement in margins & returns.

Share of non agricultural enquires rose to 25% of the total. Product mix continues to evolve & management is guiding for higher share of non agri commercialization in the coming years.

Capex guidance for the next year is 800-850 crores (which includes some spillover capex of the current year as well). The ongoing & next year capex should increase capacities by 25-28%.

Currently, 17-18% of revenues are from products that were introduced in the last 3 years. (This is a good data check point to keep in mind)

Currently, there are total of 15 plants out of which 3-4 plants are dedicated and the rest are MPP. Also, 2 new plants are expected to come on stream by FY25.

Overall, the commentary was very bullish with no signs of weakness witnessed for their products. However, the management still guides for 20% growth in future years as well.

Disc : Invested & Biased.

I could not find any update on pharma acquisition, QIP proceeds are sill lying idle in BS invested in Liquid fund resulting in depressed ROCE/ROE. Its almost 10 to 11 quarters since QIP.