I asked the same questions several months ago. Never received an answer from anyone. Finally after lots of studying, I finally did, it’s hidden in their business verticals. That’s why they are super hungry for pharma opportunities.

2 Likes

Companies usually do capex which starts to generate revenue afterwards. However those capex will cause increase depreciation cost. Additionally that will also cause increase in other expenses also like salary or any increase in fixed cost. However once those new capex asset will start to generate revenue the profit will increase disproportionately. this is called operating leverage. it will also cause rise in roce this is what happened with laurus labs in fy21. it’s like a 2 way sword. if revenue decreases profit will decrease even faster. same things is happening with laurus in last 3 quarters.

8 Likes

Thankyou @vibhor_vaish @Souresh_Pal for your detailed explanations!

So the way I see it is that ROCE has decreased over the years due to increase in capital employed (high capex + FY20 QIP) without a proportionate increase in EBIT. Is that the right interpretation? Similar story with asset turnover which has been decreasing over the past 4 years.

Yes you can say so. In the last concall they told that for next few quarters they can increase the revenue without doing much capex. And they can increase the revenue further by doing brownfield capex (this is just expanding the capacity of an existing plant and this takes less money compared to setting up a new plant which is called Greenfield capex).

3 Likes

Also, one important reason is for low ROCE is, they did a QIP of 2000 crore which they wanted to use for acquisition of a pharma asset. The Ind-swift attempt didn’t work out and they are still sitting on this cash pile. That can partly explain the lower ROCE too

4 Likes

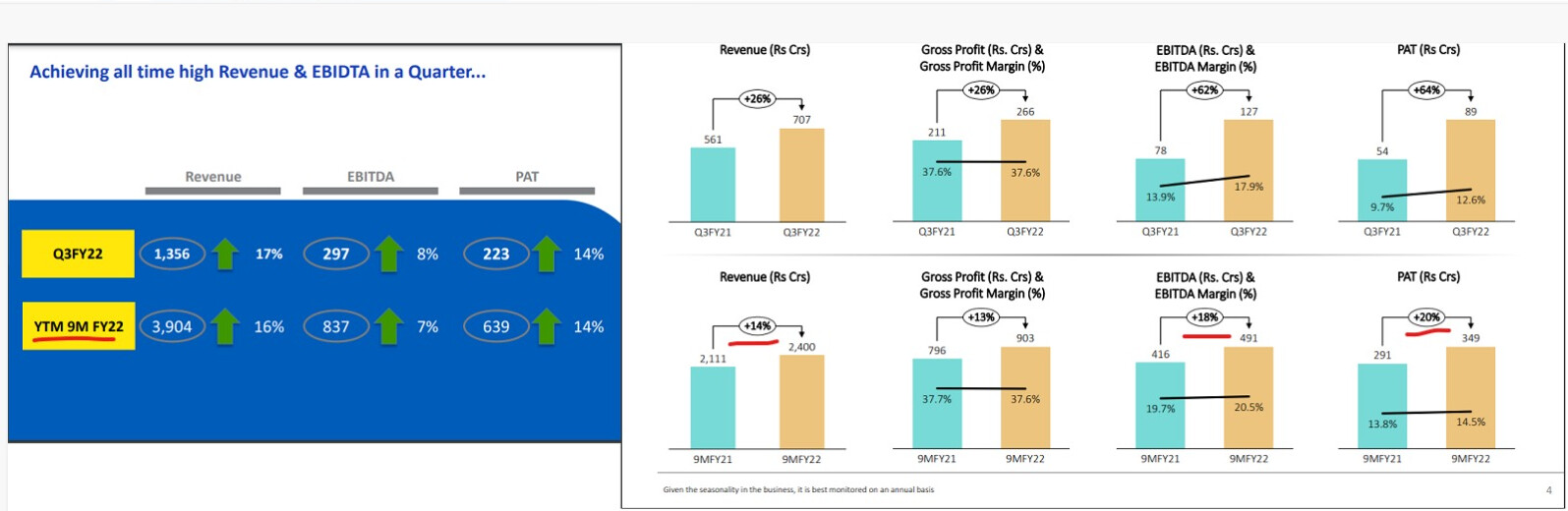

PI industry Q3 results and press release:

Q3 revenue increased by 17% to 1356Cr, EBITDA up by 8% to 297Cr, PAT up by 14% to 223Cr

Q3 exports growth of 19% and domestic segment growth of 8% on a high base.

On a 9M basis, the domestic segment de-grew by 3% due to the unfavorable kharif season.

Good Rabi season helping recovery.

Margins are impacted due to rise in input costs, lower export incentives, fuel expense, shipping cost.

Raising input costs has been passed on partially by increasing selling price both in CSM export and domestic segment. Full impact to be reflected in coming quarters.

Total capex for 9MFY22 : Rs 228 Cr.

Maintained higher inventory of Rs.1,355 Cr to avert supply chain disruptions and meet supply schedules.

Global CSM segment:

4 new molecules commercialized, 3 more planned in Q4.

>40 products at different stages of scale up

R&D pipeline has >20% non agrichem products.

32 new enquiries,>35% from non agrichem space.

Order book of 1.4Bn

1 multipurpose plant commissioned in Q3.

New chemistry building block commissioned in Q3.

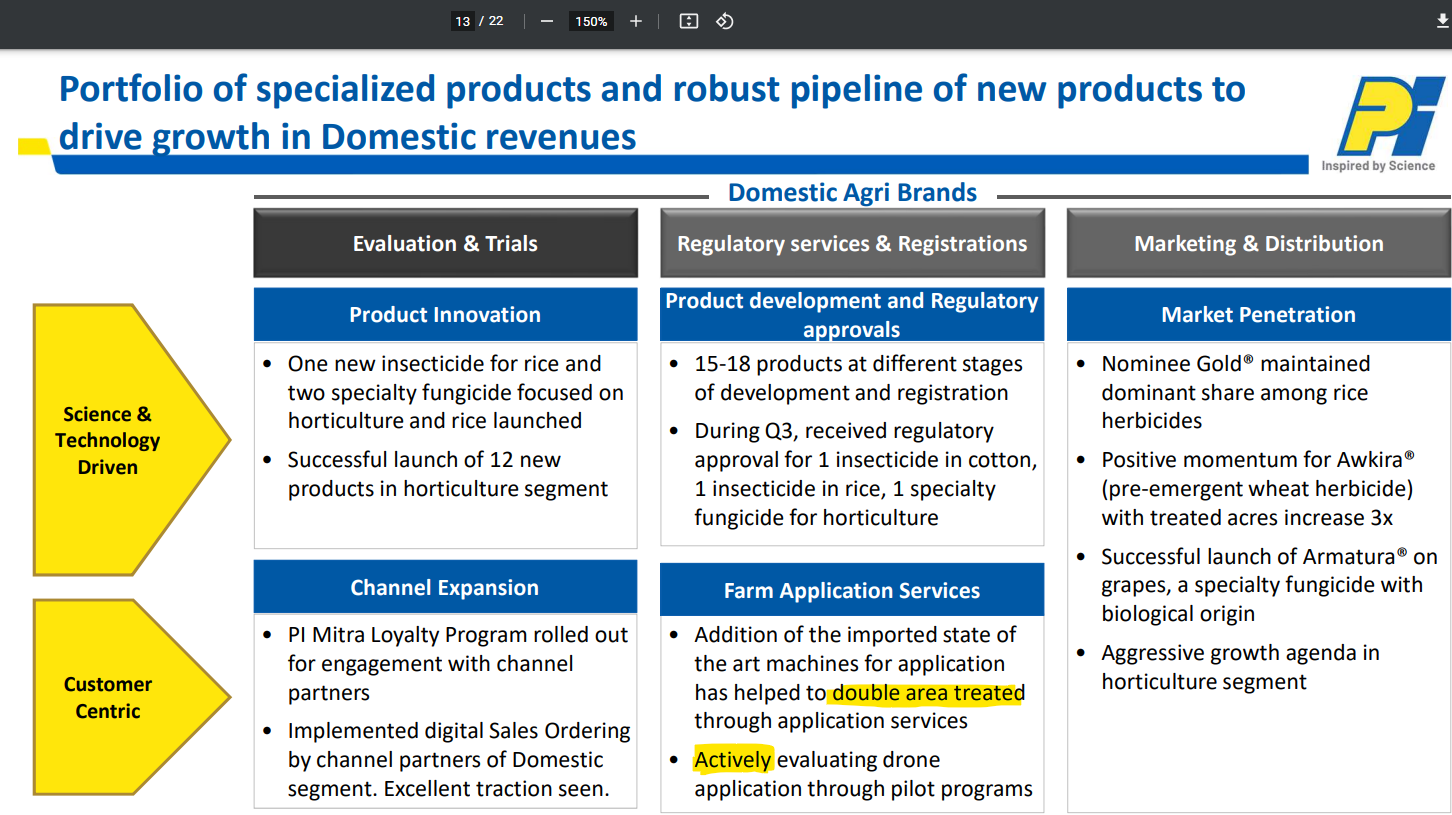

Domestic segment:

One new insecticide and 2 fungicides launched.

12 new products launched in the horticulture segment.

Received regulatory approval for 1 insecticide in rice,1insecticide in cotton and 1 fungicide in horticulture.

15-18 products at different stages of development.

Recent launches like Awkira,PB knot, Armatura are getting good traction.

Maintained original guidance of >15% revenue growth.

Discl: invested

13 Likes

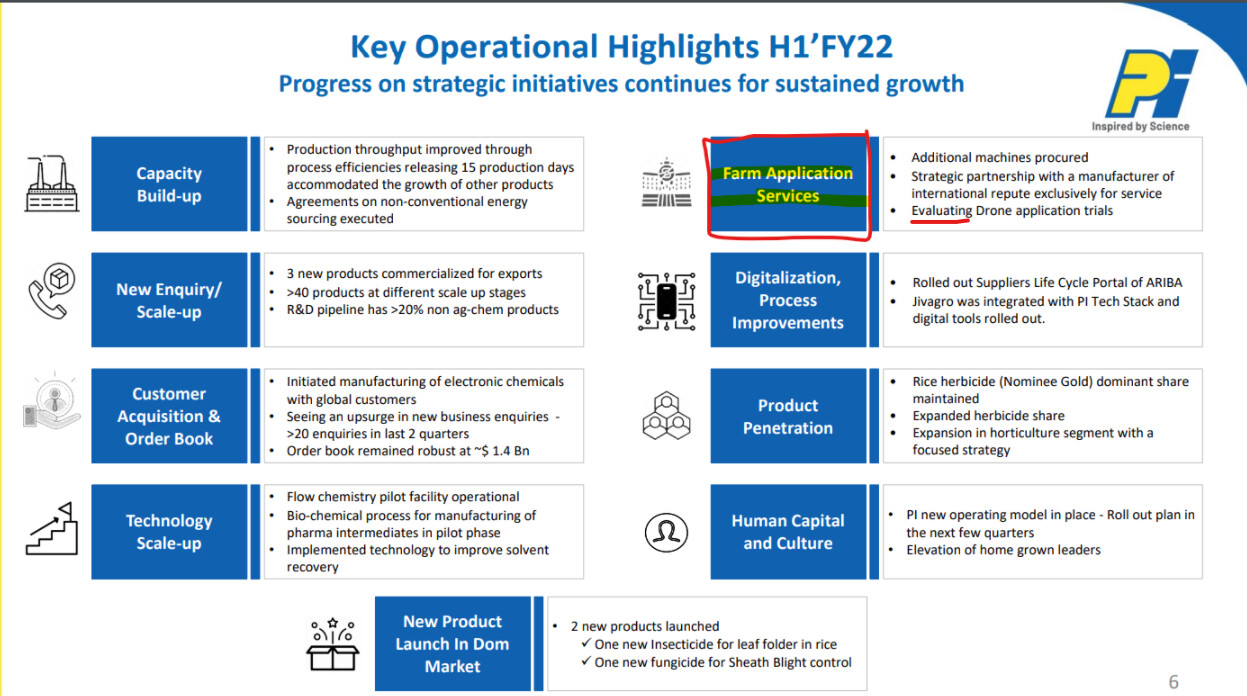

Application Services : How to understand this " Addition of the imported state of the art machines for application has helped to double area treated through application services" ?

Are they evaluating these machineries / equipment ? And if successful they will be launched under PI ? Can someone please help me to understand this ?

There is a slight difference in the wording from Q2 → QA on evaluating drone application

Below is from earlier presentation

3 Likes

Hopefully some acquisition will be in pipeline.

Results are good

New product launch is positive

Q3 Updates

- New CSM unit head - Dr Atul Gupta - earlier COO - https://www.piindustries.com/about-us/about-PI/PI-leadership ( replacement for Mr Rao)

- CSM is quite dominant and becoming heavier in product mix ( 4:1 in q3 from 3:1 in 9 mo basis) - margins improvement not visible in this Qtr despite better product mix but bound to reflect in coming Qtrs.

- 15% guidance seems conservative as already delivered 16% at 9 monnths - Q3 commissioned plants should help bump up, margins should get better as well with prices pass on reflected,

- Asset turns are 2.1X - quite an improvement- should improve further with Q3 commissioned plants - they are delivering 4500 cr on TTM basis with fixed assets of 2200 cr - 2000 cr sitting in cash to deliver similar returns once deployed after Indswift deal setback - once deployed potentially we are looking at 10000 cr revenue runrate and 2500 cr EBDITA - need to hear progress on acquisition plans in con call

- Attrition was called out in control esp at Sr leadership( irony that Mr Rao resigned in same qtr to join Granuels)

- Biggest consistency over many many quarters is CSM order book at $1.4B - doesn’t move at all

Recent underperformance

- Mgmt has been at pharma vertical built up for quite some time now, market has been patient but recent beating suggests its running thin - stock has seen derating from 60PE to 45 PE now which is long term median - one would assume that they lost 18+ months from successfull QIP to deal fall off ( Jul 20 QIP of 2000 cr, July 21 Ind swift acquisition announcement, Nov 21 deal break off) - Quite a long time to conclude a Generics player acquisition - by mgmt own admissions- many out there.

- In contrast Isagro acquisition has been quick , turnaround even quicker and efficient- good capital allocation

More details hopefully in concall, Invested

16 Likes

Has mgmt mentioned any reason for CSM order book staying flat at $1.4 Bn since the past few quarters?

Yes they are keeping it purposefully because of volatile raw material cost situation going on now. Told in q2fy22 concall

1 Like

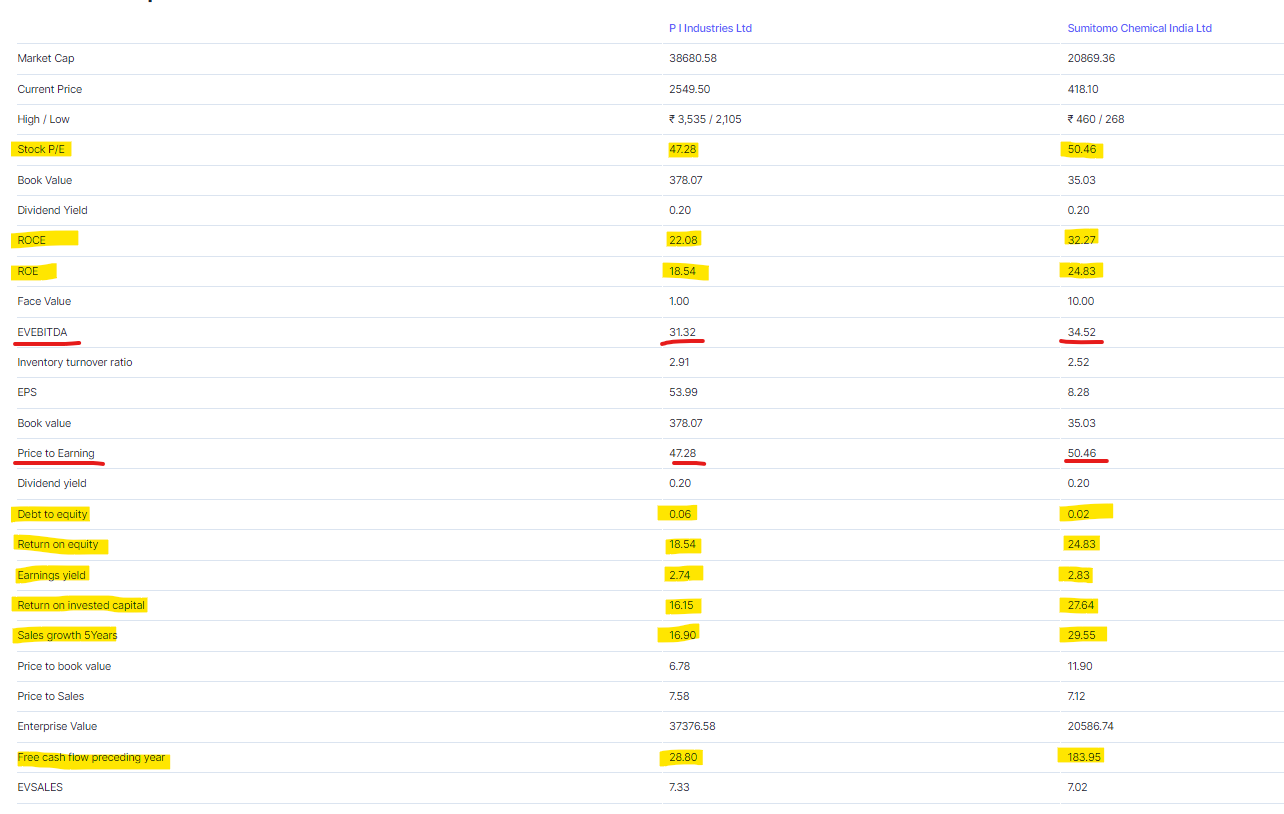

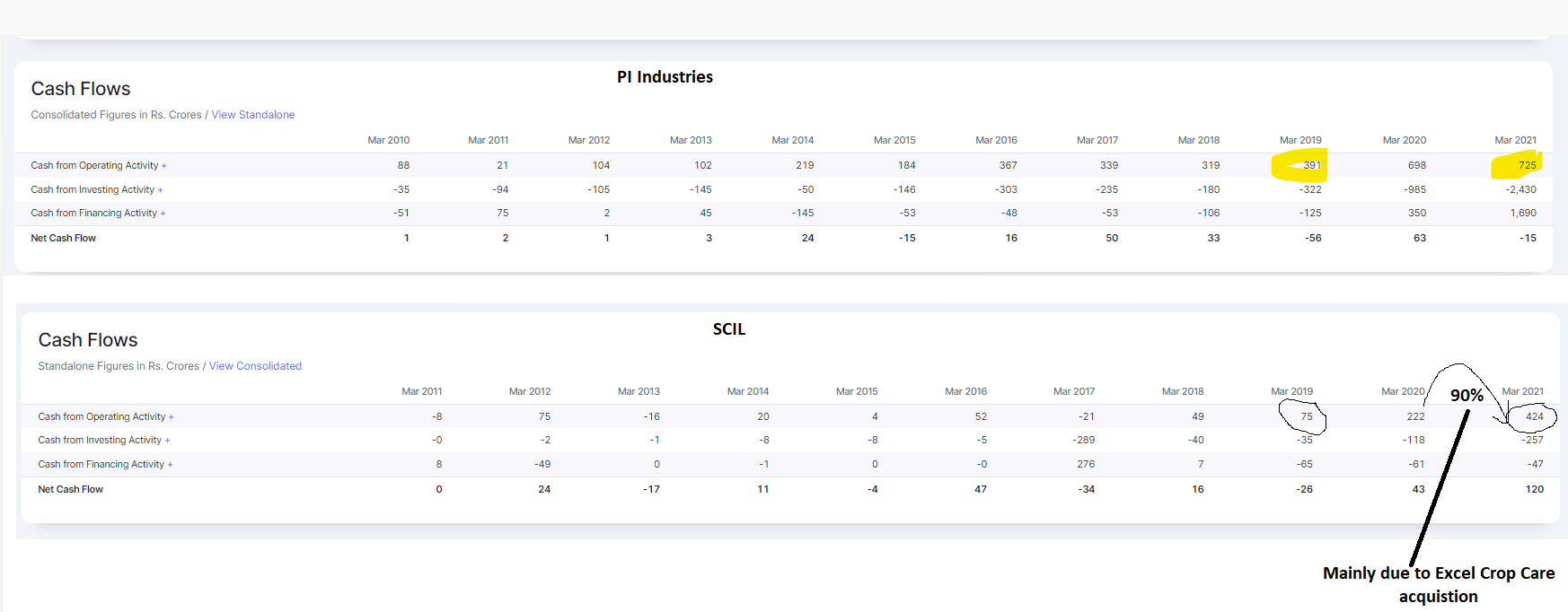

Why market is giving high valuation in terms of PE or EV/EBITDA to Sumitomo ? Where as the later is kind of a commodity play; PI is more focused play ?

PI vs SCIL Cashflows

2 Likes

Another strong set of results, revenue grew by 16%. Margins were impacted due to raw material price inflation (seen across agchem players). Here are my short notes from their concall.

- Gross margin impacted due to higher commodity prices and lower export incentives (the impact will be even more visible in Q4) despite favorable product mix

- 9MFY22 :New client addition: 8, new CSM product launches: 4 (3 planned in Q4)

- Have maintained higher inventory to avoid supply chain problems, managed to satisfy 98% of customer needs

- Focus is on improving flow chemistry processes to enhance capital efficiency of the business (basically become more capital light thus higher ROCE)

Disclosure: Invested (position size here)

6 Likes

My two cents:

- Sumitomo – Japanese parentage, less capital intensive than PI therefore higher ROE & ROCE, less floating stock due to 75% promoter holding, smaller size so faster growth prospects, more scalable business than PI.

- PI strengths – moat business model so less downside, less cyclical risk.

9 Likes

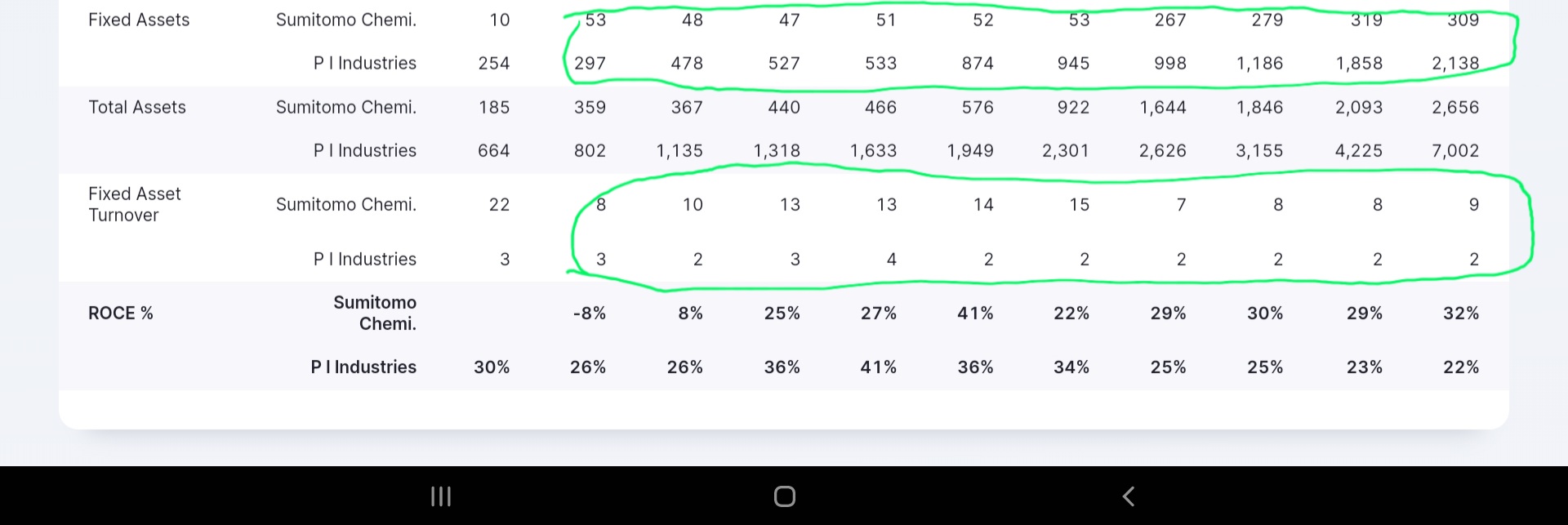

Interesting observation @Rafi_Syed , in addition to what @Chandragupta articulated, one additional data point stands out in favor of Sumitomo. Below diagram shows fixed asset turns ratio

Asset turn of Sumitomo is unheard of and likely to do something with parent and India entity arrangements( folks following biz can comment more)… What this essentially means that it needs fraction of assets compared to PI to generate similar revenues, though it is not fair to compare pure Agchem to CSM+Agchem. Even in pure play Agchem comparison such as India pesticides Sumitomo asset turns are way higher.

Q3 PI concall there were discussions on focus on asset turn ratios and RoCE improvements. Mfg setup Asset turns is a key efficiency lever, though looking at in isolation won’t do full justice.

6 Likes

Formulation or distribution companies in agro generally have a higher asset turnover but more volatile margins and sales. Just check Dhanuka agri

4 Likes

All purely domestic facing formulations agchem companies make these kind of asset turns, it has nothing to do with being an MNC. This is because formulations in agchem means mixing active ingredients in a given proportion (basically diluting the concentrate to relevant levels). This doesn’t require fancy machinery and can be easily done at very low capex. A correct comparison is Dhanuka Agri which does similar fixed asset turns (10x+).

The problem with domestic market is growth, its hard to grow beyond a given level. You can read my detailed post about this where I compare all agchem companies and different business models that exist.

22 Likes

Q3 concall

Core biz - CSM - Almost reaching 80% revenue share

-

Near future margin expansion on back of input cost price rise pass on with lag as well product mix in favor of high margin CSM

-

Med term margins expansion on back of Asset turns improvement, moderated by continuing capex

-

Threat of patent expiry of molecules on PI - Mgmt believes it should not matter as such given this( gentrification)will take 3-4 years to play out , PI will continue to have labor arbitrage and cost leadership innovation to mitigate impact.

-

Strong commercial molecules pipeline build over FY 21 and 22 - true impact is seen with a gestational period of 3+ years - I.e. FY 24 onwards

-

Healthy Enquiries growth continues, 8 customers added

-

Mgmt continues to emphasize on moving up the value chain - demand side on innovation and drive future commercial pipeline - mgmt believes that innovative molecules will always be driven by relationships, credentials, capabilities ( thus was in response to competetitive landscape) - so far growth number suggests they are leaders but good to keep any eye on peers trying similar path( Bharat rasayan etc)

-

Supply side innovation focus with measurable outcomes was visible e.g.

-

Tech - No of digital tech intervention across life cycle, employee learning,

-

Chemistry - flow chemistry - helping throughput and thus asset turns increase, better safety, quality control, Plant capacity optimization ( called out 15% type increase in capacities)

-

process - continues yeild improvements, Solvent recovery and so on <

-

Another unspoken element was continuity of biz impact post departure of Mr Rao, and leadership churn( though Bharat shah from ASK raised concerns ) - at the end of day an organization driven by processes and systems is not dependent on individuals - good to see it playing out so far

-

98% Customer deliveries on time , this metric not many companies share publicly- something that strengths PI position in customer base for future

-

Capex will be needed in addition to sweating current assets better

Net net this sticky, predictable & consistent cashflow, pricing power driven, healthy pipeline of recently commercialized molecules - looks steady engine for continued double digit growth trajectory.

AgChem- formulations- domestic

- Awkira doing good

- Muted Qtr but expect pick up

- PBNot - a new community driven solution is being rolled out - takes time for adoption but scale will be good

This is a competitive landscape and a smaller pie on overall mix, may continue growth inline/better than industry

Future growth areas

- Organic efforts on Pharma intermediate at best can get to three digits( 100-150cr) in near future per Mayank, he is very clear that Inorganic is the only way to scale here - given FDA approved plants, relationships, size where one can scale meaningfully is needed.

- There are two school of thoughts for PI Pharma vertical ambitions and also influenced by industry dynamics

-

Not a cake walk and will take years - inability to close transactions inn1 year+ post QIP, Mr Rao moving out( only guy in leadership with deep pharma background), very highly competitive industry landscape leading to sub optimal results vis a vis current CSM - agchem biz, no Right to win type situation given whole credentials and cust relationships to be seen, CDMO scaling is a patient game and has its own lumpy character and so on. Folks here will likely wait and watch execution success and already trimmed/exited considering opportunity cost.

-

Faith in PI execution given credentials and capabilities - Mgmt has ventured in uncharted territory in past and desigend its own CSM - agchem innovation partnership success over years - none in industry peers could do it yet at similar scale, Intent with aggression & funding is in place, Capital allocation history of past( Isagro) speaks for itself where turn around was swift, Once bitten twice shy - Indswift fall off will make mgmt better prepared and cautious to make it right this time, process and chemistry capabilities are proven and thus Pharma supply side is well covered( mfg, quality, compliance, ESG…), optimist breed here is staying put, will find current levels attractive and will add as execution builds.

Based on which camp one finds oneself is imp to understand and position, ride is going to be volatile as mkt expectation will be like a bolt on with smooth outcomes in few quarters where as reality is likely going to be multi phase - transition +stabilization + scaling- atleast 2-3+ years affair post acquisition.

Stock has taken a beating since Nov deal fall off and current valuations are inline with 5 year median of core biz, in a way good as expectation are reset, current Fixed asset base equivalent cash chest( together 4500 cr) is available and mgmt has every intent to deploy it, with a conservative asset turn of 2-2.5 range we are looking at a likely possibility of 10000 cr+ revenue in few years.

Charts at monthly support

Invested

16 Likes

Refer to Page 17, the initial comment by Rajnish Sarna - “if you are looking at CSM per se across

the verticals it would be substantially high; $30 billion to $40 billion, but if you are

talking only about the Ag Chem may be $4 billion to $5 billion around that.”

3 Likes

The total CSM market is huge but their capability in other non Ag chem CSM verticals will take some time to be proven. Does anyone know the current market share of PI Ind in the Ag chem CSM market only?

3 Likes