Q2 concall

CSM story

- CSM engine - 24% YoY growth, product mix now heavy on CSM( kissing distance of 1000 cr qtrly run rate, 70%+ of mix - not far away used to be at 50% type), ** driving GM expansion**

- CSM growth prospects and capacities - 6 molecules commercialized in last year - due to process and yeild innovation brownfield expansion continues to serve without higher Capex - from here also they can increase asset turn ratio to 2.4 - 2.5 range. Lot of room for brownfield expansion in current plants ( land available and effluent discharge mgmt allows to continue expansion)

- Street concerns about low Capex intensity and CSM growth trajectory - given increasing asset turnover, 300 cr Capex can deliver 2.4X+ - thus can continue to add 700-800 cr+ organically( translates to 15% -20% type guidance, CSM they have visibility of 20%+ growth)

- CSM order book reduction from $1.5B to $1.4B - Given input volatility don’t want to overcommit for long term hence some conservative approach.

CSM Agchem growth to be be 20%+ and continue to improve margin profile due to higher share in mix - Order book+ new commercial molecules scaling, innovation aggression and move up value chain with new molecules and 100+ patents, ability to pass on price hikes is visible. This engine contribute 70% revenue and has legs to grow

India Agchem

- Jivagro and Agchem- H1 flat for various supply chain issues and extended rains affecting key geo, expect H2 to pick up with Rabi, new launches in herbicide doing well. Share of biz is reducing ( as %) - likely to grow in line with industry or slightly above. Herbicides 3x areas compared to last year - happy with progress.

New growth engines

- Electronic chemical - long term contract in works, new area with huge potential. Small volume high value, Japan geo to start with, chemical OEM for now and slowly move to Auto OEM

Pharma

-

20% revenue from pharma vertical in 4 years - ambition intact!!( They are at 5000 cr rev in FY22, FY 26 can do 12K-13K cr - at 20% Pharma will be 2500 cr+ - tall claim but doable with Organic + Inorganic

-

Organic in pharma continues, several intermediate at pilot as well as commercial for non GMP. Capex? - how much organic - use our plant, add MPP - part of normal Capex 300 cr, currently 75 cr Capex for pharma - med to long term 1.5 to 1.75X of investment assets turn.

-

Pharma Inorganic- GMP facility via inorganic path - several opportunities in mkt - Shorter period we can use outsourcing

-

Pharma - supply side is fine - How customer acquisition will happen - technology identified, intermediate regulatory in progress, Inorganic path to get access to customers

-

Why Generics in pharma as opposed to innovator part( as is case for Agchrm) - pharma start with Generics/cdmo approach. Agchem took 2 decades to be where we are in value chain , pharma we have technology but expedite with generic to get access to customers + Asset and eventually move up value chain. We will be Technology based generic player( process innovation- cost leadership, environmental aspects such as ESG) - not me too. Patented molecules eventually.

-

Ind-swift lessons learned- value system should be non compromisable, due diligence to be strong, timing - working on yesterday due basis.

-

2500 cr+ cash - ready to deploy to acquire pharma asset and deliver 1.5X to 1.75X in next 1-2 years, eventually improving 2x+ as they move up value chain

-

Org structure is now aligned to next 5+ year roadmap.

While there is setbacks on Ind-swift deal, mgmt is aggressive in acquisition closure - Given target is generics CDMO - plenty of opportunities.infact recent pharma correction and headwinds may augur well.

Can we see three major verticals per below in next 4 years ?

- Chemical CSM( Agro and fine chem/Electronic chem) - currently at 4000 cr+ , growth at 20% plus - getting to 8000 cr size with high margins - a solid compunder

- Agchem India- currently at 1500 cr, at 15% growth, going to 2500 cr - decent margins and some seasonality

- Pharma - FY 23 - 1000 cr rev- Organic + Generics CDMO to start with at 20%+ margins and 20% growth CAGR , moving up the innovation value chain and a Mini Divi’s in making given their R&D and tech capabilities - 2500 cr+ biz by FY 26.

FY 26 onwards - 13- 14K Cr revenue growing at 15-20% CAGR, 20%+ EBDITA with consistency, CSM chem a steady cash cow and pharma biz value chain on improving trajectory, India Agchem a smaller but steady play. Add this with capable mgmt and lean balance sheet. Don’t see any reasons as to why mktcap can’t go from 41K cr to 80K cr+ conservatively.

Building blocks and execution capabilities +credentials are in place, probability high that they can and they will, stock is below 200 DMA post deal fall out, may stay sideways till pharma asset is fully secured.

Invested and added in recent dip.

My only Pushback against their Pharma vertical:

-

Take any other company, whether its Navin, Neuland, Laurus etc. It takes time to seed the cdmo business in pharma. Navin took nearly a decade inspite of acquiring Manchester organics early in 2011.

-

Seems journey will start by being a generics focused api player and eventually go towards the higher margin business. One has to taper the expectations of a fast scale up in the latter, given pipeline takes time to scale up and eventually deliver.

-

Acquiring a Pharma asset is to mainly get access to customers. PI has strong relationships within agri but it is yet to be seen whether they can do it in Pharma or not. They scaled up Agri CDMO at a time when other competitors weren’t interested in the business due to various reasons (eg:- Rallis focusing on formulations etc). They might find it challenging to scale Pharma cdmo.

Views: invested and contemplating.

Valid points @Worldlywiseinvestors , adding some more pointers/inferences from management interactions thus far

Does size, capabilities scale , credentials matter and help expedite journey? Neuland and Laurus ( few years back) were relatively smaller when incubating CDMO - it was all organic and thus no of years and yet to show a sizable consistent performance.

Also PI will likely have four phases broadly speaking

-

- BUY asset and transition,

-

- STABILIZE and build/enhance CDMO for generics.

-

- SCALE and cost leadership and marketshare molecule wise

-

- INNOVATION driven value chain unmove with innovators, patented molecule etc

Each of it 1- 2 years depending on execution so yes a journey but given PI has traversed value chain for molecules in Agchem in last decade, with learnings can do in shorter span for pharma(pace to be seen). Once they are past 1&2 stage , has potential to go Divis path given science capabilities.

Also CDMO as sector itself is more fertile now compared to earlier, growing and has tailwinds, believe smart latecomers with size and credentials may benefit from shorter curve IMO.

Agreed, identity will be Generics API for good initial part of journey of few years - lower margin around 20%+ and decent growth , Given it will be a phased approach, which we expect PI to share in due course ( confidence builds up with the fact that they have intermediate under validation and commercial ready - thus Organically in a ready state as soon as asset comes in) - point being team, GTM strategy, molecule are somewhat in place - production asset is what they are after.

This one is tricky definitely as relationships and customer acquisition has no shortcuts - unless there is a way to cross leverage current customer base - which doesn’t seem to be the case though credentials will help.

A logical assumption would be evaluating synergy during acquisition on due diligence of asset ( customer quality, molecule capabilities, cdmo potential of acquired customer base, and so on) - this one is a leap of faith on mgmt track record such as Isagro acquisition turn around etc, though bit shaken at moment given abrupt Indswift deal fall out, hopefully wiser with that.

We will get answers to these in near future, though thesis could be long term, wise to keep an eye on pharma asset play and sector dynamics in short term to revisit if needed.

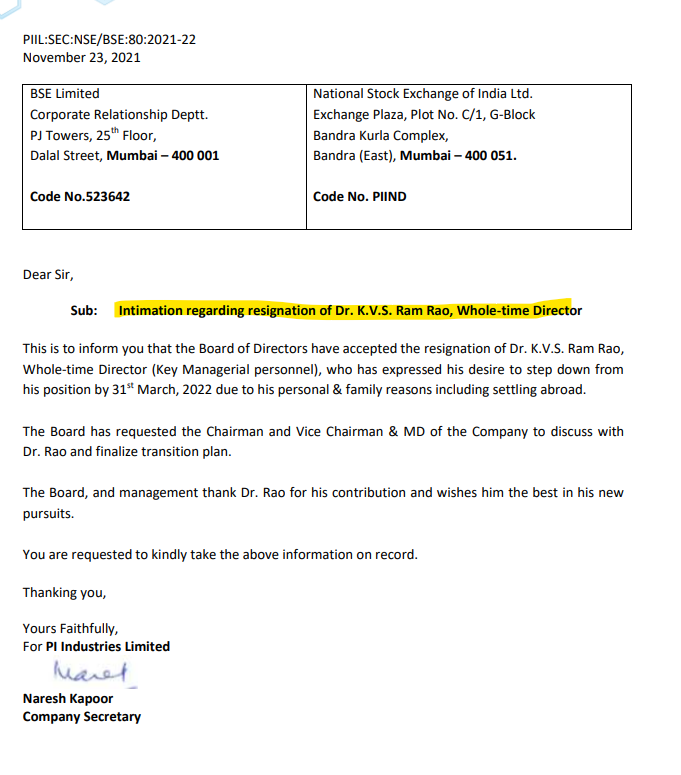

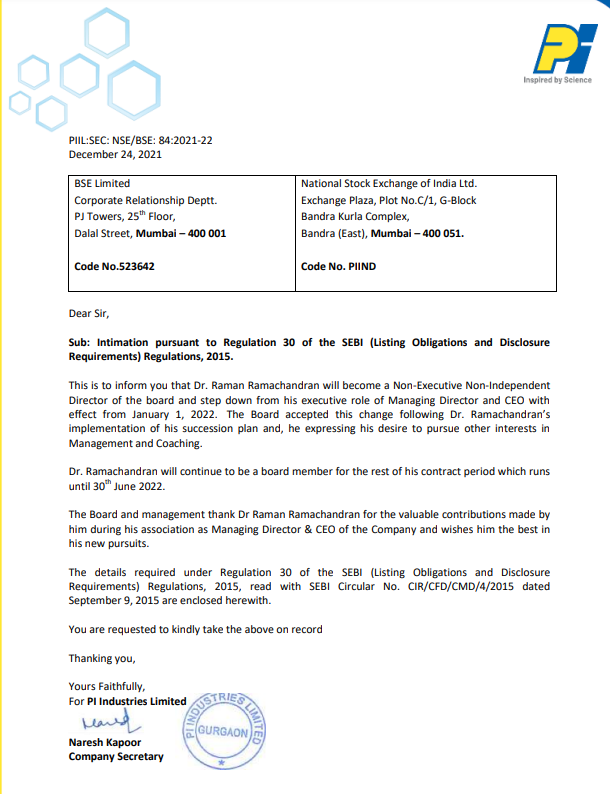

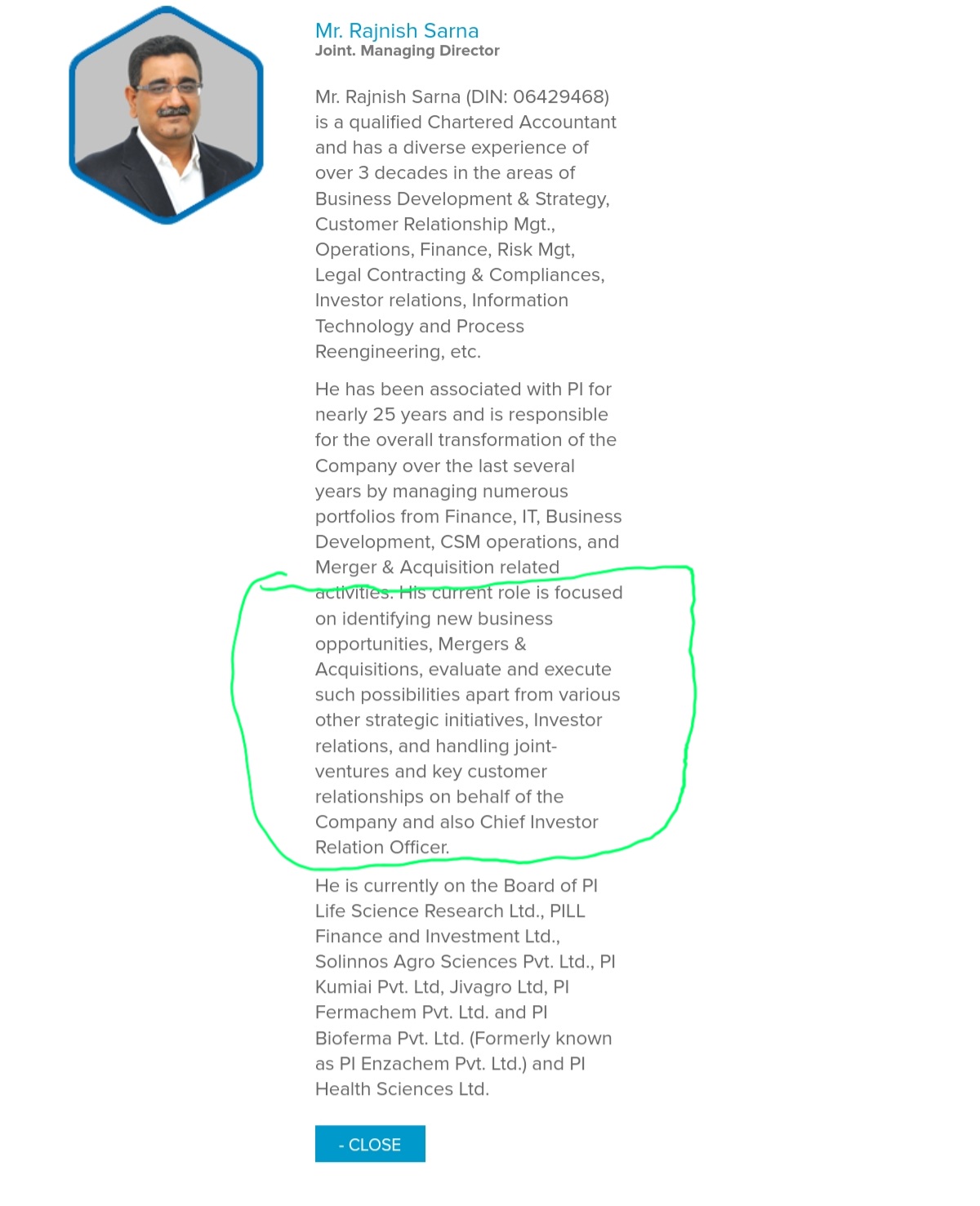

Most likely the case considering he got an elevated role back in May 2021. Attaching a screenshot from his elevation announcement:

Let’s wait and see who takes over him.

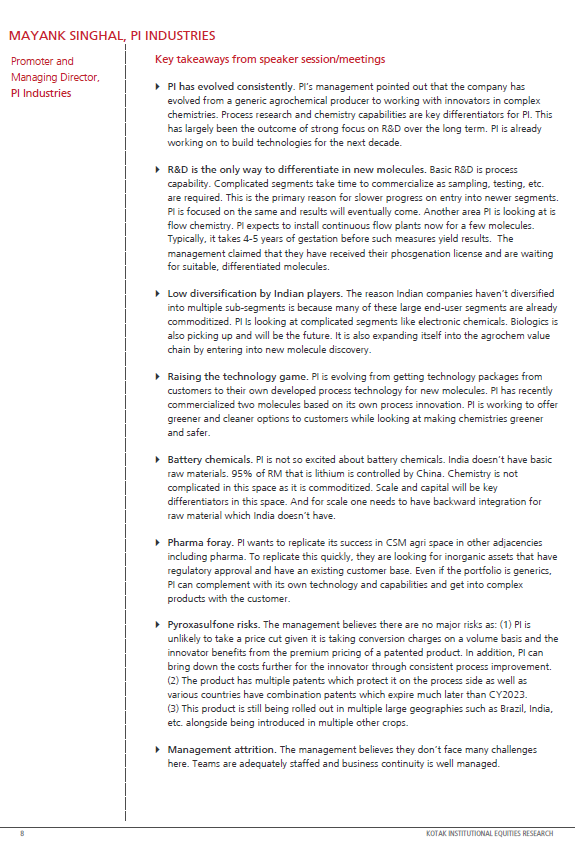

Phosgenation, flow chemistry, electronic chemicals… I see traces of Murali Divi in Mayank Singhal.

In fact, Murali Divi also spoke about electronic chemicals in the recent concall.

I see ever hungry management who realizes the constant innovation needs to keep the gushing flow of cash and appropriate re-investment of it back into business. I guess we should not call it high P/E but premium management fee if that makes any sense.

Why did management decide not to enter formulation contract manufacturing?

Recently PI applied and received the licence for Phosegenation. Only Paushak, Gmdc and Atul are the other players in this hazardous chemistry. Pi expects to launch differentiated molecules using this platform.

Source:- Kotak Daily

My guess would be Jt MD - he is deeply rooted with Mayank and PI, and is driving all growth initiatives as well.

This still leaves the huge Gap of CSM head and upcoming Pharma unit head position ( that’s 75%+ revenues once pharma assets comes on board) - Mr Rao who resigned earlier was designated as Head CSM exports and possibly playing both in a way given his pharma background.

Ideally should be two leadership/CEO positions as CSM and Pharma( Generics to start with) may not be similar skill set given different stages of maturity of each asset.

They have CEO each for both Jivagrao and Agchem biz thus P&L is sorted.

while I read this, 1 Q that came up is “why was he not retained by Pi management ?”

I read somewhere that he is very good.

LIC increases shareholding slightly and becomes >5% shareholder.

Can anyone please explain why the ROCE has fallen continuously over the past few years? From almost 30% in FY17 to 16% in FY21. I am an amateur investor, just wanted to understand whether the ROCE can go back to atleast 25%?