It is easy to lose one’s sanity in the current state of the markets where everyday pf moves 3% up or down for no apparent business reasons, purely due to market risk, although the mind tends to make up business issues where there are none. So purely from a business standpoint, just going over last Q results since now all results are out and also future outlook.

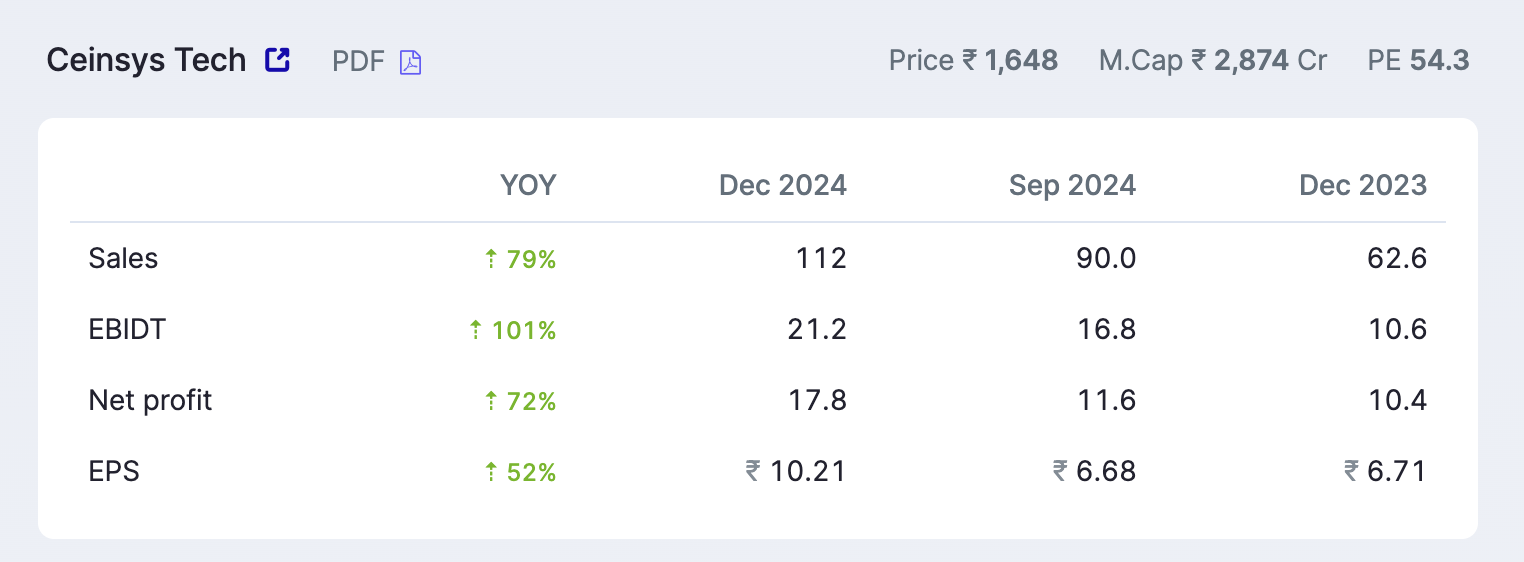

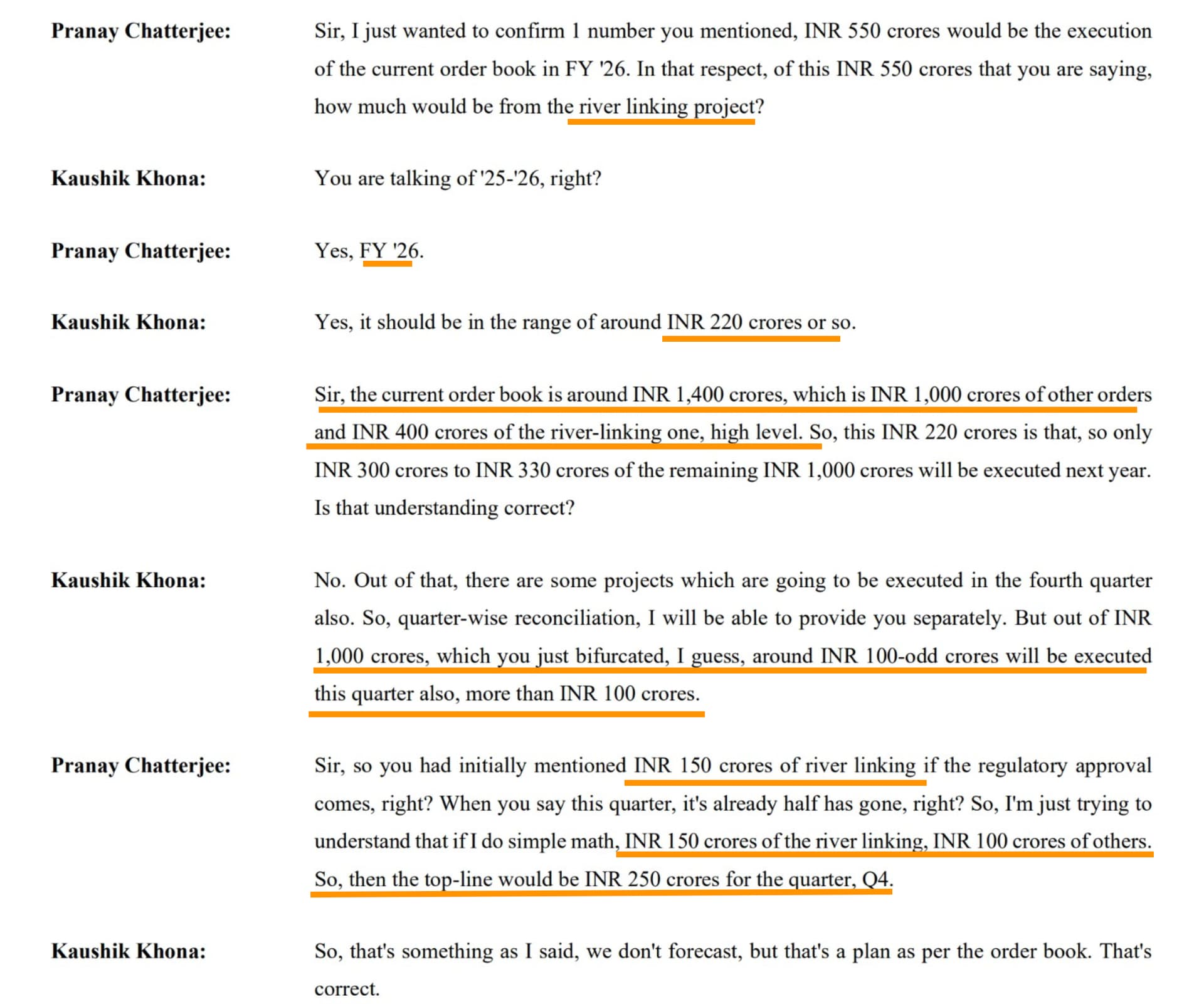

Ceinsys - Finally a big earnings quarter that justifies the order book. But even this is suppressed to a large extent on the consolidated side (by maybe 4-6 Crs) due to higher employee expenses on business which are yet to contribute.

Near future, with the strong order book, Q4 execution might include 150 Cr from river-linking project + 100 Cr of other order book. So Q4 numbers could be anywhere 150-250 Crs though there’s no explicit guidance

Shaily - Pretty strong growth, 6 more customer signups for pen platforms and 2 new business contracts with global retail chains. Shaily UK revenues which are high margin for platform access fee can also grow. Insulin revenues will ramp up from next quarter once they have higher production using the 8 cavity molds instead of the 4 cavity ones which should help operating leverage as well considerably.

Axiscades - Strong growth with good contribution from defence production revenue. There’s good margin expansion in Aerospace business as well from 20% to 24%. Semicon business as well is howering around 24% margins although growth is flat.

Q4 defence revenues should be even higher as its the seasonally big quarter. There’s a big drag in non-core EBITDA to the tune of 7 Cr (3 Cr profit vs 4 Cr loss) which when it compensates can help the core segments shine even better. I am also hopefully some actions are taken on the non-core segment soon which will augment the balance sheet and also improve the PnL

Blue Jet Healthcare - The thesis for investing is here, here and here. The preliminary signs are that the Q4 PAT of 99 Cr should be the base on which there could be 10-15% growth which could yield a 500 Cr PAT that’s more than double TTM PAT (and 3x FY24)

Wockhardt - Nice to see it become PAT +ve although its on the back of forex gains. Though there’s no concall here for future outlook, the management has guided for a 20% growth in the near future. I have covered the zaynich trial results here. It is quite optimistic and would be great if they can file NDA and get the drug to market soon.

Genesys results are very good as well and among other businesses I track closely Garware, though its not a great quarter, the management has reaffirmed its growth outlook. Holmarc being a SME has nothing to show for this Q (They declare every 6 months)

Other than this, we can indulge in macro and scare ourselves to death based on what prices are saying, but its helps to be optimistic

After being 17% down 2 weeks back and almost recovering it all in just 3-4 sessions, am now 12% down so far in this round of cuts. Its not terrible by any means but feels so purely because of the volatility.

Disc: Invested in all mentioned names