Update:

https://twitter.com/RNTata2000/status/1258791391867494401?s=20

1 Like

1 Like

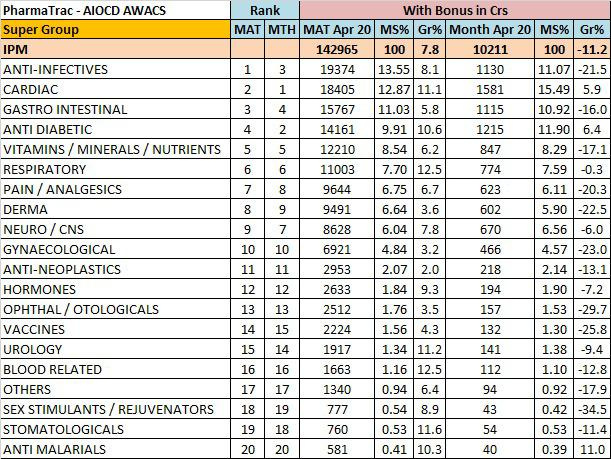

April month Indian pharma:

source:https://twitter.com/anupsoans/status/1260422071210868737?s=20

Overall IPM growth down by 11%.

As expected most of the segments had significant negative growth during April as most of OPDs/clinics were shut,elective surgeries postponed resulting in reduced medicine consumption.

Only Cardiac and Anti-diabetes segments have shown positive growth of 5.9% and 6.4%.

Anti-malarials 11% growth mostly due to HCQ.

Things may get better slightly for the month of May as most state Govts allowed elective procedures and routine OPDs started.

Found this very informative:

Essential summary of the blog:

No structural changes for easing of pricing pressures in the US market, no specialty pharma traction, no biosimilar traction, extreme competition in the India (and RoW) markets building up – so, why is everyone excited about pharma?

4 Likes

COVID-19 Impact On Pharma Sector & Future Of Indian Generics Industry | Global Dialogues

2 Likes

Thanks for the link but this post really seems more like a rant. Its incorrect to simply look at the pharma industry as one. I will try and give my perspective on Indian pharma.

During the recent downturn (starting in 2015), there were four large factors which impacted large generic companies.

- Consolidation of distributors into 3 main companies controlling more than 80% of US market resulting in loss of pricing power for large Indian pharma companies as most Indian companies do not have their own frontend

- Stricter FDA compliance with FDA setting up their offices in India. This was because more than 40% of drugs in US (by volume) come from India

- Implementation of GDUFA in 2012-13 with FDA’s focus on faster approvals to smaller generic companies to reduce generic drug pricing. This resulted in delays in approval for large generic pharma companies at the cost of smaller companies which were just getting into US. Net beneficiaries were smaller pharma companies like Alembic.

- The opioid crisis in US which took the sheen away from large acquisitions from Indian generic companies (eg: Lupin acquisition of GAVIS which made money by selling opioid drugs)

- The large generic pharma companies were trading at very rich valuations reflecting a lot of optimism

I divide Indian pharma companies into the following categories:

- Pure Generic companies: With faster ANDA approvals, the price erosion has increased to such an extent that the incremental ROE has gone below 10%. This is the cyclical aspect of the generic business and depends on the number of drugs going off-patent in a given year. The lowest cost producer and the most efficient player will win this battle. In the 2010s, companies like Lupin and Sun gained a lot by milking this market. Now, its Alembic and Ajanta Pharma winning this game because of their smaller exposure to US market. In a few years, Alembic and Ajanta will land up in a similar position as Sun/Lupin if they do not invest in their specialty drug pipeline.

- Specialty/hard-to-make drugs: The large companies (Sun/Lupin/Reddy) have invested a lot in this business. Returns are yet to come making it hard to estimate the ROCE of this business. On the face of it, it looks better than the pure generic business. Smaller companies like Natco feature here with them making most of their money from 1 to 2 specialty drugs.

-

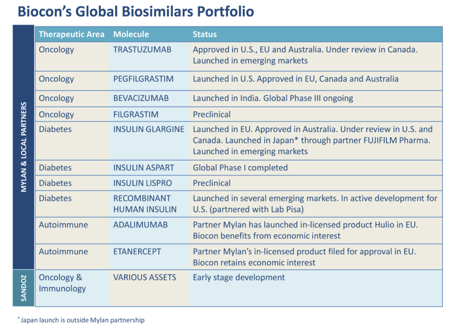

Biosimilars: There is only one company (Biocon) with a sizeable biosimilar pipeline. You can see their pipeline below (taken from FY19 AR). They have commercialized two molecules so far for the US market and EBITDA margins are >30% reflecting low price erosion. Lupin has a pipeline of 2 drugs (ethanercept, pegfilgrastim). Dr. Reddy has 2 drugs (pegfilgrastim, adalimumab), however Biocon has a time edge on both these drugs.

- API manufacturers: This is a scale business and the lowest cost manufacturer will always win. China is way ahead of India in this and is the lowest cost provider of bulk APIs. In the Indian context, Divis is the only Indian company with a large market share in certain APIs. There are other smaller players like Granules.

- Contract research: This is like the IT of the pharma sector where research is outsourced from innovator companies to India because of labor cost arbitrage. This is a reasonably predictable business with Syngene being the market leader. Other companies like Suven also get sizeable revenue from this segment.

- Indian pharma: This is a high ROCE business with limited growth prospects. Its mostly a branded drugs game, where branding gives pricing power to companies (eg: Zydus, Cadila, Sun, etc.). However every few years there is pressure from government to reduce drug prices (eg: categorizing drugs into National List of Essential Medicines). Large generic pharma companies like Sun, Lupin, Cipla now derive about a third of their revenue from this segment and use this cash to invest for growth in foreign markets. MNC companies also operate in this space. Its a reasonably predictable business.

I will love to get into more detailed discussion about the specialty/biosimilar pipelines of listed Indian companies as that can be a large value driver.

Some additional resources:

The thread on biocon is a treasure trove for learning about biosimilars (link)

Disclosure: Invested in Ajanta, Lupin, Natco, Divis, Biocon

48 Likes

The Future of Healthcare, Pharma, and Allied Industries (HPA) Punch: Day 2 Panel Discussion

https://www.youtube.com/watch?v=WyYr7bmIti4

Link to the summary:

9 Likes

In this post, I tried to cover the sector. It is not very specific but covers broadly what are the workings of the Indian Pharma industry and where we are at (and what to do)

VP is a “higher audience” - this is meant for beginners to Pharma and Investing. Plus it also includes a basic investing checklist / framework.

8 Likes

This is a lovely video describing the industry positioning of different players in the contract research and manufacturing part of the pharma industry, I cannot recommend it enough!

4 Likes

sharing an old report worth reading

https://www.iqvia.com/-/media/iqvia/pdfs/asia-pacific/india/winning-in-the-indian-pharmaceutical-market.pdf

Regards

1 Like

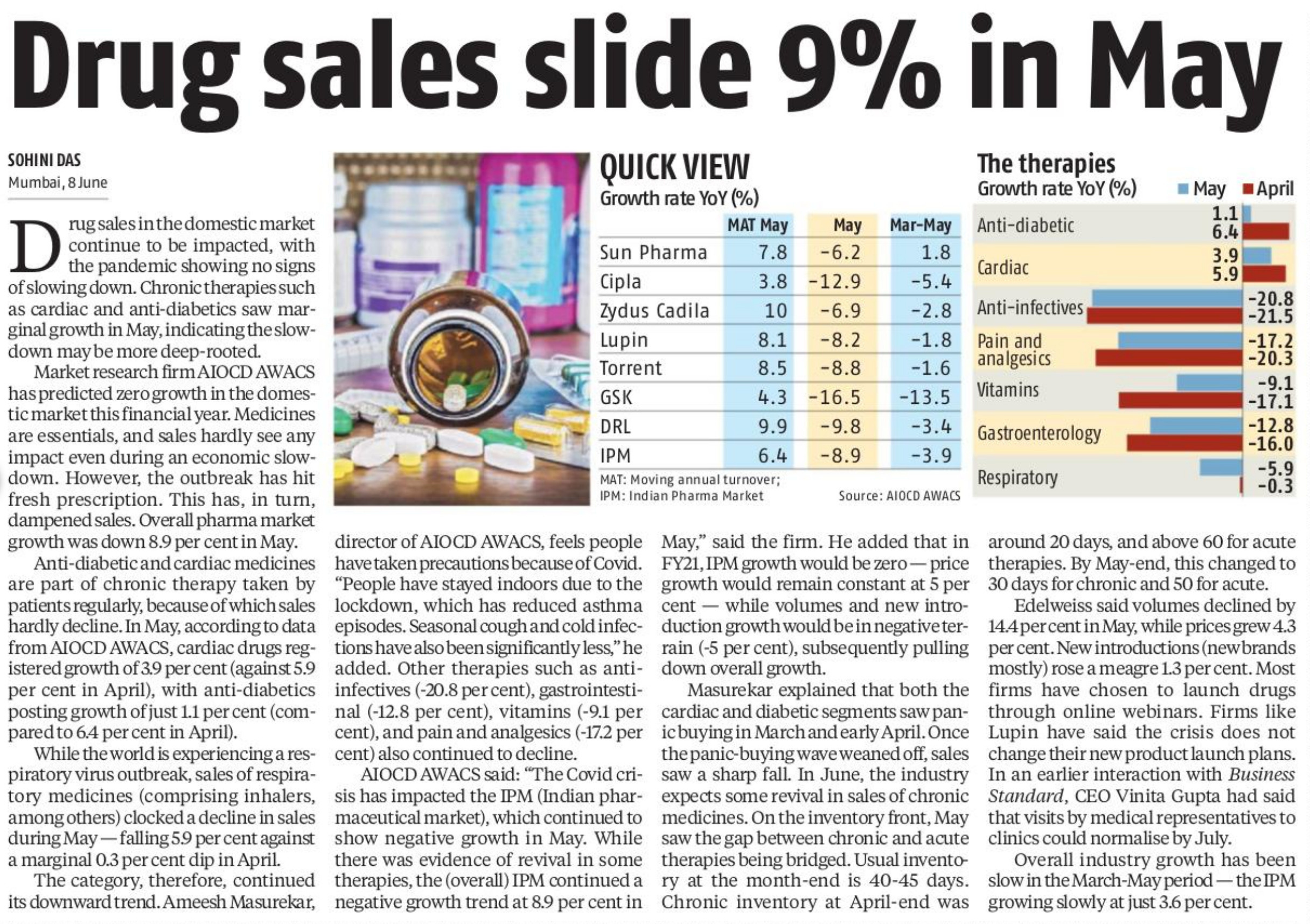

Indian Pharma Industry’s June sales report.

Some encouraging signs here.

2 Likes

Hi guys…

I have been on this forum for a long time now. I have generally been investing in consumer facing FMCG, Consumer durables, private sector banks etc.

Off late, I have started investing in Pharma.( this was a move, that I forced onto myself as my ability to quantify risks in the COVID disrupted world wrt financial institutions went for a toss )

I have been trying to learn about various aspects of Pharma business.

I have a few querries that I want to ask you since you have been active in this space for quite some time now.

Most querries are wrt generic players.

So…here I go -

Lets say…most branded formulation / generic players ( like Ajanta, Alkem, Cipla etc )…make 100s of formulations. However, their in house manufacturing of APIs is very limited, as it is cumbersome, capital and labour intensive. They also outsource a number of their formulations. ( correct me if I am wrong ).

Does that mean that these companies are just front end Marketing companies with added compliance and quality control issues with drug regulators???

How and why is it that a single formulation plant churns out so many different formulations??? Is the process of churning out a formualtion from an API so easy ???

How is it that some companies dont have the capacity to readily manufacture a formulation, but still gets a USFDA approval??? ( correct me if I am wrong ) And later they decide weather to launch a drug or not depending on the amount of juice in the opportunity.

Compliance issues aside ( which is an entry barrier of sorts ) , what else separates these companies from rampant competition ???

China, over the last 20 yrs became an API powerhouse. What stopped them from becoming a generic powerhouse ???

If we do not get the API industry back to India ( atleast to some extent ), and suppose there was no global backlash against China due COVID, isnt it a fair assumption that they would have turned the tables on us on formulations also ( over a perioiod of time ).

Except for front end marketting, what separates generic players ???

India is a branded generic mkt. However, if India were to become a pure generic mkt, wont the Industry loose most of its pricing power ???

Although, I have made small investments in a lot of generic companies ( so that I get serious and study hard ), these questions keep coming to my mind.

Basically, what will make the Indian generic players to churn out descent profits in the future ??? ( not counting complex generics, biosimilars here …sepecially for the midcap guys )

It will be great to hear from guys you about some or all of these.

Trust me…it will of great help.

Thanks in advance.

Regards,

Ranvir Dehal

5 Likes

@hitesh2710 @ananth @spatel @ankitgupta could you please throw light on the following how to capture these

While framing the valuation IMO retail investor don’t put risk premium which may happen or may not it is the claim on the company from the retail purchasers or bulk purchasers of the drugs .

Second Retail investors usually impressed by the patents hold by the company but it is common in the pharma sector but in order to defend the patents companies has to fight lots of legal battles.How much risk premium one thought on this ?

Third Opportunity size and capacity size matter a lot yet sometimes govt put cap on the pricing of end retail drug which put pressure on the manufacturer and in the supply chain to compress the margins and sometimes kill the monopoly position of any establish brand .

Therapy leader (e.g Cipla in Respiratory, Alkem and Aristo in Anti-infectives , Sun continues to show fragmented presence with focus on both chronic (Cardiac, Neuro) and acute (Gastro) therapies) Vs Speciality leaders ( intas , Torrent ) first having large volumes and later is having improved margins . Being retail investor how would one formulate his strategy ?

Regards

2 Likes

Mr Sailesh Bhan of Nippon MF…on Indian Pharma’s prospects.

He runs the Nippon India Pharma fund…the oldest Pharma fund in India.

3 Likes

HI,

I was going through the year ending Mar 2020 investor PPT of Sun Pharma…was pleasantly surprised to see that Sun manufactures aprox 300 APIs inhouse.

Now thats some cometitive advantage besides the Formulation knowhow , quality control and regualtory complainces.

The management also indicated that they intend to ramp up the production of 20 APIs per year for captive and third party sales.

Given the API tailwinds…this did sound encouraging.

Also, Sun pharma sells aprox 1900 cr worth of APIs to third parties besides captive consumption.

Another thing that caught my eye was the fact that the PPT refered to API division as the -

ONE OF STRATEGIC IMPORTANCE

I always used to wonder, how can generic pharma continue to keep doing well going fwd…in the face of increased competition and pricing pressures. This kind of backward integration provides some answers to the nagging thought I had.

Off the cuff, I know that DR REDDYs contribution of API sales ( besided captive consumtion ) is even higher. ( will come out with exact numbers shortly ).

Now…this not only improve their backward integration,provide cost leadership in various molecules, also gives them a huge opportunity to play the China to India API shift.

Lets see how it goes.

One request - these are some of my observations. I would love to hear some counter views.

Disc: invested in both.

Views are biased.

Though the outbreak of coronavirus has hit the global economy, the Indian pharma industry’s exports have managed to grow by 10 per cent in dollar terms (22% in Rupee term) during Q1-2021 the first quarter of the current financial year over the previous year as per Pharmexcil.

For the period of April-June 2020, the sector has managed to export pharma products to 206 countries and recorded $2018.21 million as against $1835.5 million in the same period, last year.

It appears drugs like hydroxychloroquine, Remdesivir, Paracetamol, and other respiratory drugs including the respective API makers must have contributed towards the exports…

In spite of the fact that Our Country’s overall exports contracted by 12% in June and we had a trade Surplus which had never happened before during last 18 years . … and Despite disturbed pharma supply chain due to COVID-19 in domestic as well as international markets, it is Amazing that the Pharma sector managed to grow considerably apart from Chemicals / Speciality chemicals which also grew by 19% in dollar terms…

4 Likes

Good news is that India Readies $1.3 Billion Pharma Incentive Scheme; aims to be $120 billion industry!

Modi Govt seems to be walking the talk!

The Govt has announced a PLI (Production Linked Incentive) Scheme, where they have allowed maximum 30% Import for Pharma API/ Intermediates,/ KSM (key starting materials) . The scheme is also valid for speciality chemicals…

Hope a lot of our API makers will get benefitted such as Granules, Aarti drugs, Divi, Jubilant and many others…

It is a pragmatic approach, as it is not possible to expect 0% import from day 1…

It may take 2-3 years to expect to become self reliant…

So, naturally API’s produced by india will be costlier for some time since economies of scale may not permit a lower cost … It would be passed on to the drug maker and then to the consumer…

The end consumer need to pay for the increased cost … May be for few years !

2 Likes

Looks like good news for the API and speciality chemical manufacturers.

However, considering the drugs under NLEM and the price controls on them, wont it be a negetive for the branded formulation players ???

Or…is the Govt gonna extend some relaxations on that front???

Can anyone throw some light here???

It will be of great help.

Thanks in advance.

1 Like

Now the Ship has started sailing

Things will Evolve… the Govt is willing to listen… only Pharma industry needs to speak what they need in order to create a self reliant Pharma industry …

Recently Aarti drugs took up with the Govt for imposing anti-dumping duty on imported Ciprofloxacin molecule from China. The Govt promptly investigated and ordered for the same…

Similarly , the Govt has started initiatives which would benefit API’ makers such Bulk drug park, Center Of Excellence, incentives for R&D, common infrastructure management by Govt … Etc etc…

If the Govt wants to make pharm industry self reliant , the country self reliant… They will have to remove all obstacles to make pharma industry a vibrant one which has got tremendous export potential and to become the " Pharmacy of the world" …if required they may bring in changes to NLEM or even introduce some kind of subsidy scheme…

1 Like