Hi, I’m not able to figure out what does permanent magnets contribute in the whole chain of smart electricity meters. In the smart meters, there is board etched with circuits which are done at the stage of preparing the PCB.

I watched this video: How It's Made: Smart Electric Meters - YouTube . I think this more or less captures the manufacturing of Smart meters. I can visualize where the magnets would have been used in old meters but can someone point where it is being used in smart meteres?

1 Like

“Shivalik Bimetalis our supplier and we use their material and we make assemblies which are customized as to customer requirements from the Shunts.

Shunt assembly that we supply for energy meters, generally realization is higher in the export market.”

Above comments from Concall clarifies that they buy the shunts and make “assemblies” based on customer requirements. Making modules might require wire harness, PCB etc.

2 Likes

I am yet to watch the video but on a broad level, smart electric meters will have current sensors made of shunts. “shunts” assemblies are from permanent magnets.

Permanent magnet name might be misleading as only 50% of their business involves “magnets” in the literal sense. Rest is shunt assemblies

"Sharad Taparia: Hiperm is 50%, Shunt is 30%. " (from the concall notes)

2 Likes

Current thoughts:

- The growth expectation for Permanent magnets is to come out of developing new products for EV space by 2 fronts- automobiles and smart meters.

- Company wc cycle has increased quite a bit in the last couple of years, but it has shown decent roe, roce and ebitda margins.

- Gas meters are about to fade off completely. There are things on supposed hold with the company, delay in land acquisition, a lot of growth opportunities are in EV development.

- NdFeB market, where the JV is being explored is expected to grow by 6.33% CAGR.

- It seems it is difficult to onboard new customers, so increase of wallet share in legacy customers has done well for the year.

- Valuation wise the company isnt the cheapest, with 40 PE, there is no debt on the books.

- Company had stagnated profits from 2019-2022, and same with sales. This was due to gas meters seeing a sudden reduction in demand and that affected its sales. Used to be 18% of sales in FY20.

- The company can potentially improve its WC cycle and gross margins by becoming a module manufacturer from just a component supplier, however this will likely take a few years to materialise.

- The company from last concall’s visibility sees a 20-25% rev growth, giving us a potential 223 crs rev, giving us a potential 35-37 crs in PAT.

- Company needs very little capex, Current products are expected to continue with their takeoff, and there is an optionality available with ongoing R&D of 200+ products which have a potential to bear fruit.

Disclosure: Not invested but tracking

7 Likes

Can anyone tell why is the share price falling?

Any bad news or just PE correction?

To me it just seems a regular correction. There is no negative news in public domain. After moving up almost 4.5 times in a year these corrections are very normal. The story still seems very strong and should play out in next couple of years.

Regards,

Raj

Disc: Holding for last couple of years. Have reduced a bit only in recent runup.

2 Likes

I’m sharing two links to videos that will help the community understand the opportunity in Permanent Magnets.

The crux is that going forward they will be used extensively and due to rarity the prices are going to rise.

Their arrangement with Quadrant will be positive development for future growth of company.

There will be increased requirement of recycling which will again use magnetic separators.

Learn and grow😊

4 Likes

Here’s a nice dashboard to monitor implementation of smart meters -

I had attended the 2023 AGM of Permanent Magnets held through VC. Some of the running notes of the AGM are given below. Pls not there can be some discrepancies in my notes as these were taken in a hurry during AGM only.

PML has also made contribution to ISRO’s space program - Chandrayan for parts related to space navigation.

• Growth during FY23 attributed to company’s products in automotive and electric meter segments. Added new customers in EV space and increased business with existing customers. Expanded client base including large companies.

• Focus on long term growth and sustainability of the company. Importance of diversification to mitigate the impact of product life cycle. Adding new areas and forward integrating. In non current sense categories, migrating from magnets to motor parts. Become preferred partner for customers. Increase pipeline for future products. Pipeline looks good. Developing more management bandwidth. Honing skills of our employees including client visit and product development. Promise to be innovative, flexible and focused. Business outlook is positive.

• Have more than 2000 customers across all the product categories. For more product lines energy and automotive, we have 125 customers. Most of the cos are MNCs. These companies have plant across the world. Few are domestic companies.

• Automotive – exports vs domestic and how will the mix be going forward? 85% is exports and rest domestic.

• Froward integration? We were in the component business and trying to get into assembly business. Many of these capabilities we have set up in house. Sometimes we do get complex and different capabilities. In that case, we outsource.

• Earlier collaborations were for magnets. Newer collaborations are different. Maglab collaboration is for development and marketing.

• Quadrant collaboration? Currently signed MOU with them. Don’t have other agreement. Looking at opportunity to manufacture neodymium magnets with the, in India.

• Regarding the capacity, most of the products that we manufacture are customized designed. Don’t have common capacity across products. For each product, set up capacities. Capacity is modular and can increase it. Capacity isn’t a constrain.

• Capex – setting up lines as per demand from customers. Capex has been increasing. This capex – new factory and land acquisition & machinery for new projects. New plant and factory – capex – 20 – 25 crore spread out for 2 – 2.5 years. Machinery capex will be about 10 crore. Growth constraint is not capex or capacity. It is pipeline of products and project execution of customers and us.

• Outlook for 5 years? Lot of opportunities. We have done better than what we had predicted. Keep adding capabilities to the company and growth will be exponential. Market is unlimited. Diversifying to reduce risk. Heat treatment can lead to more capabilities apart from automotive and smart meters.

• Cash conversion cycle increase is due to higher inventory and higher receivables. Lead time of RM higher and hence maintain higher inventory. For receivables, we are working on that. Last year it was higher and we will optimize that. Cash conversion cycle should improve.

• Competitors also make customized products. They don’t have the range or capabilities we have.

• Our ticket size might be lower than our competitors? It will be similar to what they are doing.

• Sales team? We generally have business leaders. They just don’t do sales. Lot of technical discussions go into our sales discussion. They are techno commercial guys. Multiple years of training they need to go through.

• Other applications which can become big? Alloy business is a good opportunities. Capability related opportunities are our target. Service for heat treatment. Totally unrelated to automotive or meter business.

• Designers make a choice of which technology to use for current sensing. Many criteria they use. For Hall Effect sensors, they see how much sensing is needed. Based on cost and these criteria, they decide. In hall effect, these are nickel alloys, shunts are copper based and current transformers have polymorphous ribbon strips.

• New enquiries received? Approximately in last 3 years we have received more than 1000 project request. 150 plus actual prototypes we must have given. About 40 – 50 have converted to supplies. Many are in pipeline.

• Gross profit doesn’t depend on employees. For 100 crore project or 2 crore project, same employees will handle.

• Borivali property? Have entered into JDA with the builder. Builder is stuck. He will soon start the project. Now we are hopeful it will start soon.

• Have to do lot of designing and prototyping with customers. Mumbai has lot of talent available for these kind of projects. For our kind of products, this is a good area to be in.

• Maglab acquired by CTS. How will it impact or benefit us? Possibility is very good. CTS is a bigger company. Many new enquiries we can get from CTS. Mostly automotive applications they are focused on.

• Modules? What kind of projects we are doing? Number of projects we are working on in modules? FY23 commercialization? Very few sales from modules. Many of the modules are still in pipeline. Customers are testing those. In future, we expect modules to be more. Even modules has more components? Are we in early on stage of modules or bigger projects? Mix of both. Few modules were we do quite a bit of work and few modules where it is entire assembly. Comfort of customers is important. Mostly in automotive segment. Some of them are in smart meters – 1 2 projects. Good and healthy pipeline of modules – good opportunity size we are looking at.

• Energy smart meters in India? We have forecast from customers. Big opportunity but there are issues of margins on some of these projects. Cut throat competition. Imports there too. All these we have to decide. But opportunity is big. We are looking at relays, shunts, CTs, assemblies with terminal, bus bar with terminals etc – all our target areas. Contribution in each meter depends on customers. 20 – 50 per meter. For some customers we are doing 200 – 300 per meter also. Indigenization of components? Government will lay down some regulations related to imports, quality level etc. Some guidelines form government will come. People are free to import also for existing orders currently.

• Market share increase in one of the project with a customers? It was export business mostly. Increased the market share – till the end of life cycle of product – 5 years or more.

• Growth will depends on the pipeline of products. Last year growth was the conversion of pipeline of earlier years. Some will come this year. Working on pipeline of products for FY25 – FY26 also.

• Automotive product range? From 5 – 200 per component. Depends on material. Nickel alloys are expensive while steel automotive is cheaper.

• 50% of tier 1 automotive components manufacturer are our customers. How are we tapping these large opportunity? These customers are giants compared to us. Have so many plants and different products. They want to manufacture in India. 50% of these tier 1 customers are in initial stages. As we go along, they give more and more opportunities.

• Quadrant opportunity? How did we land? Product is permanent magnet only. Magnets is a complex technology. Have capability in it. We are ahead of other companies in terms of learning. We have been in touch with them for many years.

• China opportunity? Related to automotive. Main customers are in Europe or US. Their assemblies are in China. It is increasing and it will depend on customers.

• Bank deposit increase? Collateral against working capital facility. Las year working capital borrowing was less than 1 year. Last year it was 6.8 crore. This year its 7.6 crore.

• Customer added in FY23 and plans for addition in FY24? We have added few new customers this year. This year once they get added – MNCs with plant worldwide. Opportunities across their plants. This year growth will come from projects added 2 years back and scale up happening now. Process take 1 – 2 years. This year’s growth is efforts done in the past. Customers added last year will start adding revenue from next year or FY26. Growth will come from new customers.

• Most of the capabilities for mechanical and electrical parts are there in – house. PCB we wont do. If we know that we don’t have capability, we outsource. Reduce outsourcing to reduce cost.

• Most customer prefer most things from one place. If parts are inhouse we can improve quality better. Do look at payback period to bring in new products.

• Movement to modules from components – impact on margins? Generally, more complex the product, margins are better. Module margins will be better. Share inhouse working of products with customers. Moving more and more towards more complex products. Higher margins there.

• FY25 – movement towards modules will come in revenue? Some of them will come in FY25. Each project is different.

• Neodymium magnet opportunity? Big opportunity in India only. EV opportunities are huge. Want to target exports also. Spread project portfolio across many segments.

• Quadrant looking at alternate source of magnets? What made them choose us? This is bigger project than existing size. Demand is quite high in these project. Not a simple project. Don’t want to do simple products. Any timeline we are looking at? Within one year we will have something in hand. Background agreements started despite not signing JV.

• New plant timelines? Part of land we have acquired and rest we will acquire. Waiting to complete the land acquisition. Wont hamper our growth. Can lease one more premises. 2 years we can build the product.

• Touch 240 – 250 crore this year? Cant give you a number for this year. Uncertainties with product approval and implementation on time. 250 crore then next step is 500 crore. How early it can happen, depends on many factors. Existing pipeline, global scenario. Energy meter bullish, EV bullish. Strategy to work and increase our number of projects.

• Key risks we are looking at? We know that. Tesla is our customer. Magnet constitute just 10% of our business. Despite people moving away from rare earth magnets. Difficult as they make motors very efficient. Don’t see that as threat to our business. We are in product related to our areas. Don’t see threat to our business. Risks? Certain external risks and internal risks as well. External risks – we are susceptible to it. Exchange rates, metal prices, global economy etc. metal prices back to back arrangements. In 2010, we had customers which stopped our supplies.

• Our business is long term one. Cant look at it on quarter to quarter basis. Compare periods of 2 – 3 years. Profits and sales depend on customer demand and product mix. Product mix sometimes is different. Pipeline is good. For future, we can expect good growth.

• Reduced debtors in Q1.

• Earlier we were product based company – magnets. Now we are capability focused company. Main reason for profitability now.

• Pipeline is quite big. Right now are at stage of getting data on how much conversion we do. We have a system in place for that. More and more predictable in future.

(Disclosure: Invested from lower levels. Not a buy or sell recommendation. I have trimmed my allocation a bit due to valuations in past few months. Still remains one of the Top 5 allocations for me)

41 Likes

can they achieve 500 cr in 3 years?

If the Quadrant MoU starts contributing 500 Cr revenue will come even sooner

1 Like

Did they talk more about the opportunity size in smart meters in numbers?

Using AI in any way to improve their efficiency ?

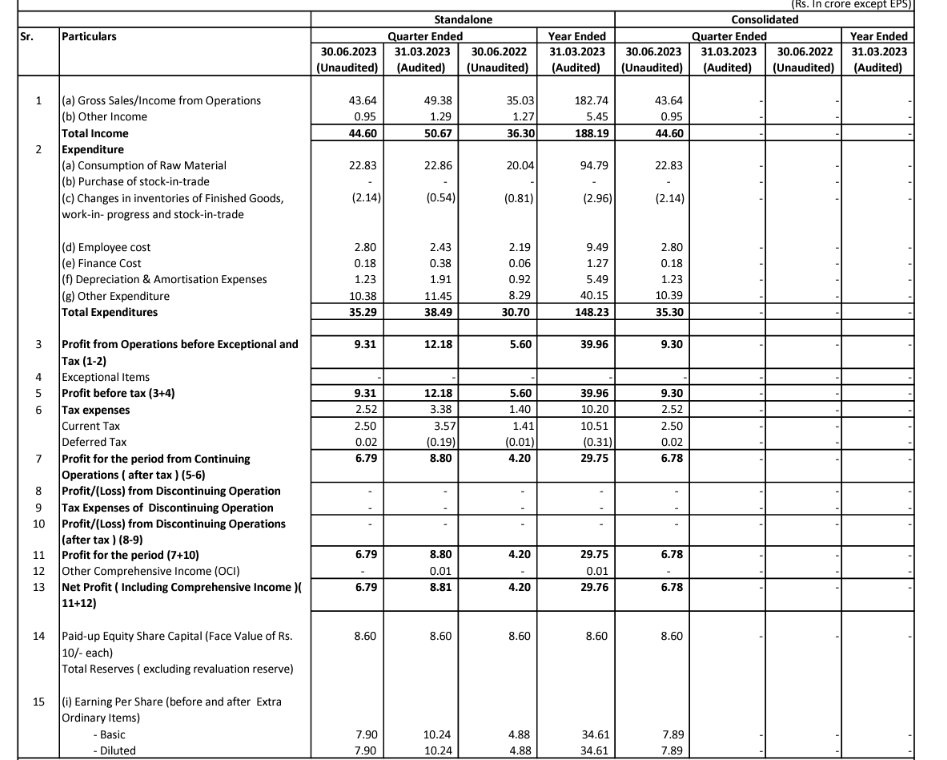

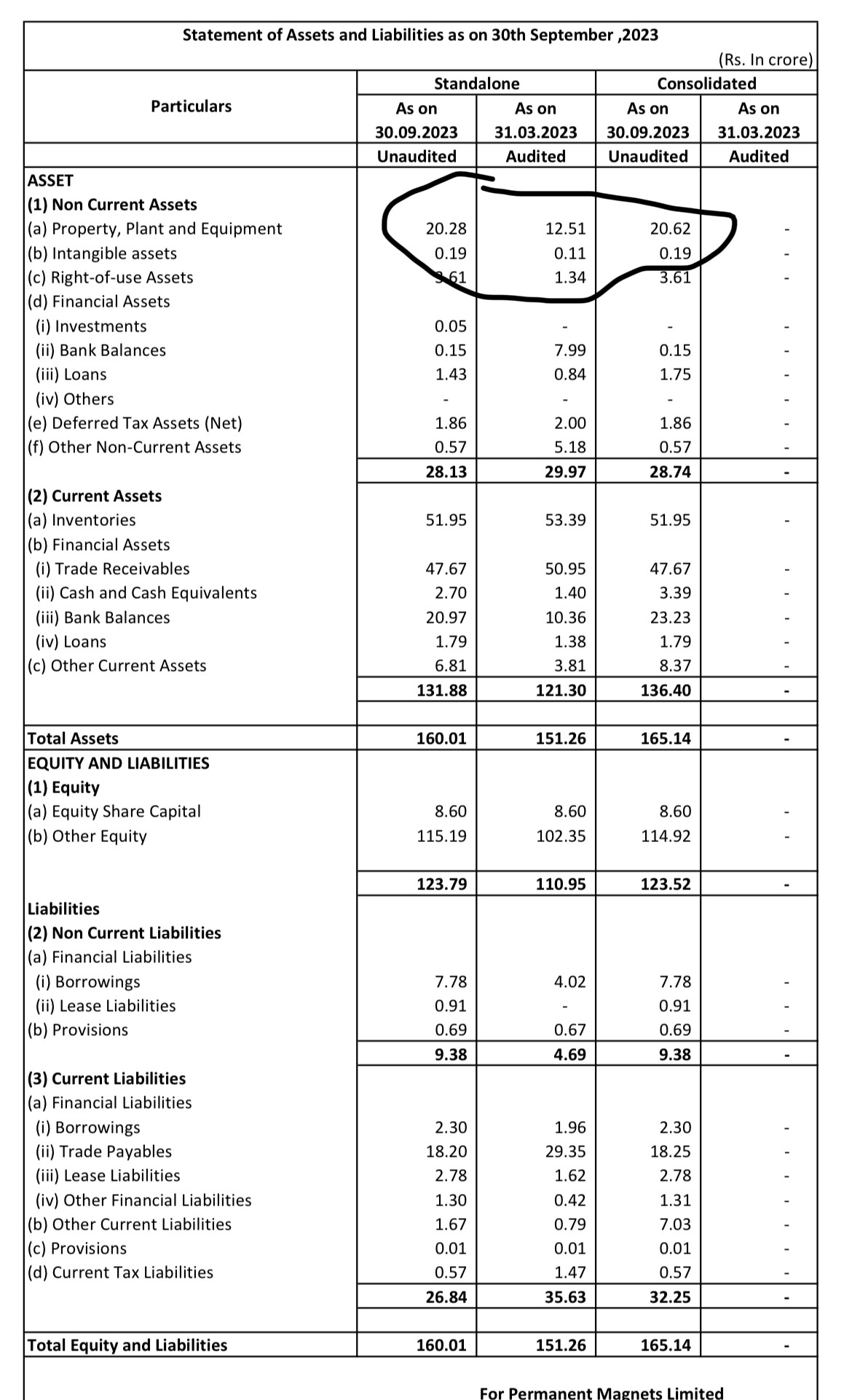

Permanent Magnets posted muted results. However, the figure of property, plants and machinery has jumped from 12.51 crores as on 31.03.2023 to 20.28 crores as on 30.09.2023, which might be indicator of things to come. Would be interesting to see the commentary in concall scheduled on 10.11.2023.

5 Likes

Well pointed out, the Quadrant business will take some time to turn profitable and hence affect the margins in near turn, but it has the potential to give explosive growth, considering the demand and shortage of magnets.

Good thing is that revenue growth has not been impacted.

2 Likes

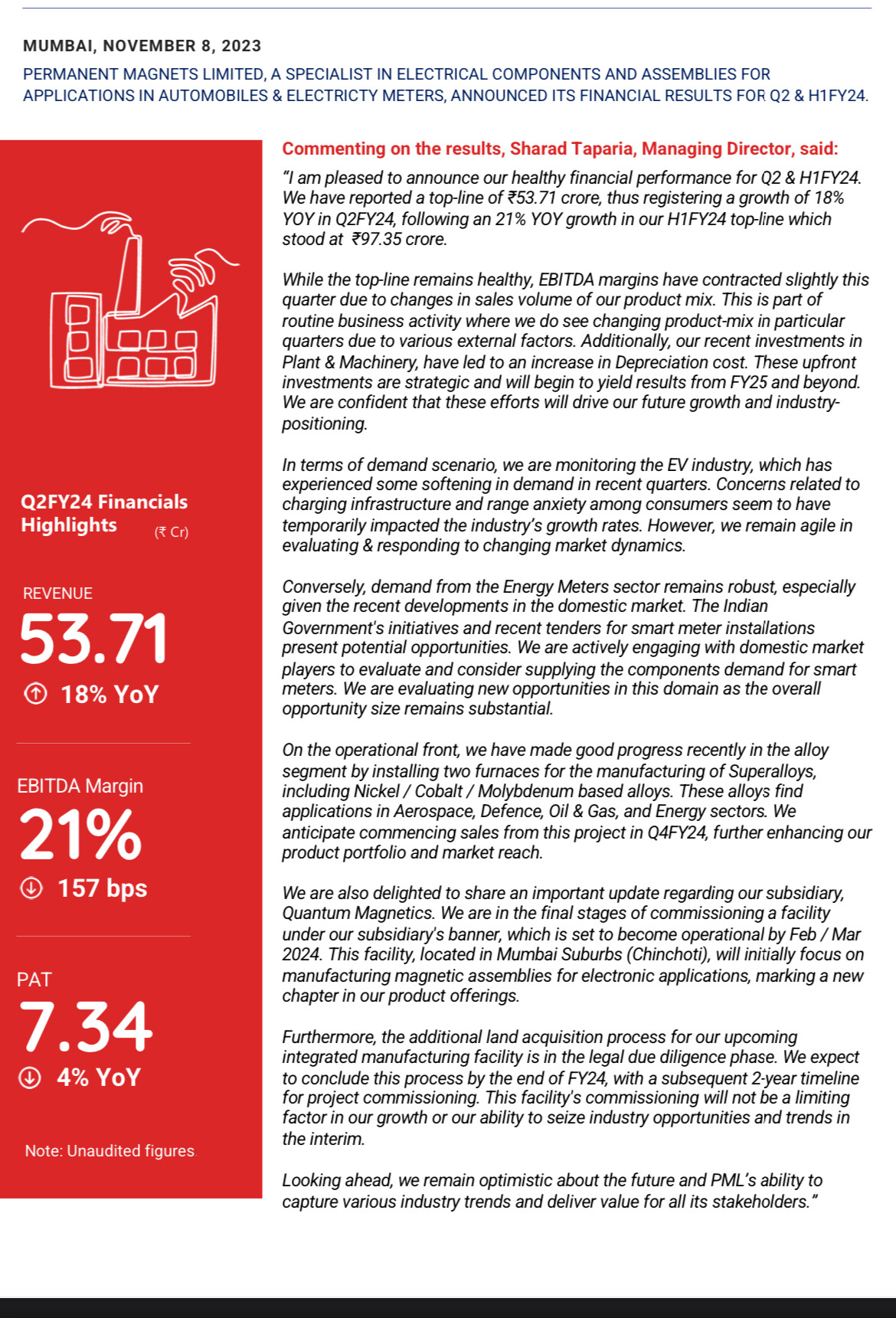

Very interesting and detailed press release by the company covering almost all the crucial points about the current results, capex, haidwinds, strategy and future outlook.

9 Likes

Attended the concall and got the opportunity to ask few questions that were troubling me.

-

Regarding Neodymium supply - since China has restricted exports of critical minerals, the company doesn’t have any supply concerns as we have tie up with IREL for supplies and even the govt wants pvt companies to participate in utilisation of these. We will have multiple sources of supply and not dependent on single source.

-

On Tesla entry into India, the management is positive on getting share of business. Didn’t quantify, nor did I ask.

-

Due to aerospace and drone boom the company is positive on demand scenario and they mentioned that their components were onboard Chandrayan and Aditya L1.

-

E-waste Recycling doesn’t pose any threat to their revenue potential and would in turn improve the availability of supplies to the company.

Other point of interest -

The new business investment is 4 Cr and revenue forecast in FY 25 is 7lin the range of 7 to 15 Cr.

Since the metals involved are in the range of Rs 5000/Kg, once the business takes off, the revenue potential can be huge.

Missed parts of the concall so others can contribute.

11 Likes

Check this in the investors call audio link tab

2 Likes