https://unifiedportal-epfo.epfindia.gov.in/publicPortal/no-auth/misReport/home/loadEstSearchHome

2 Likes

that rating report had already mentioned that a 35 cr capex is in the works,60% funds via loans & rest via internal accruals.

2 Likes

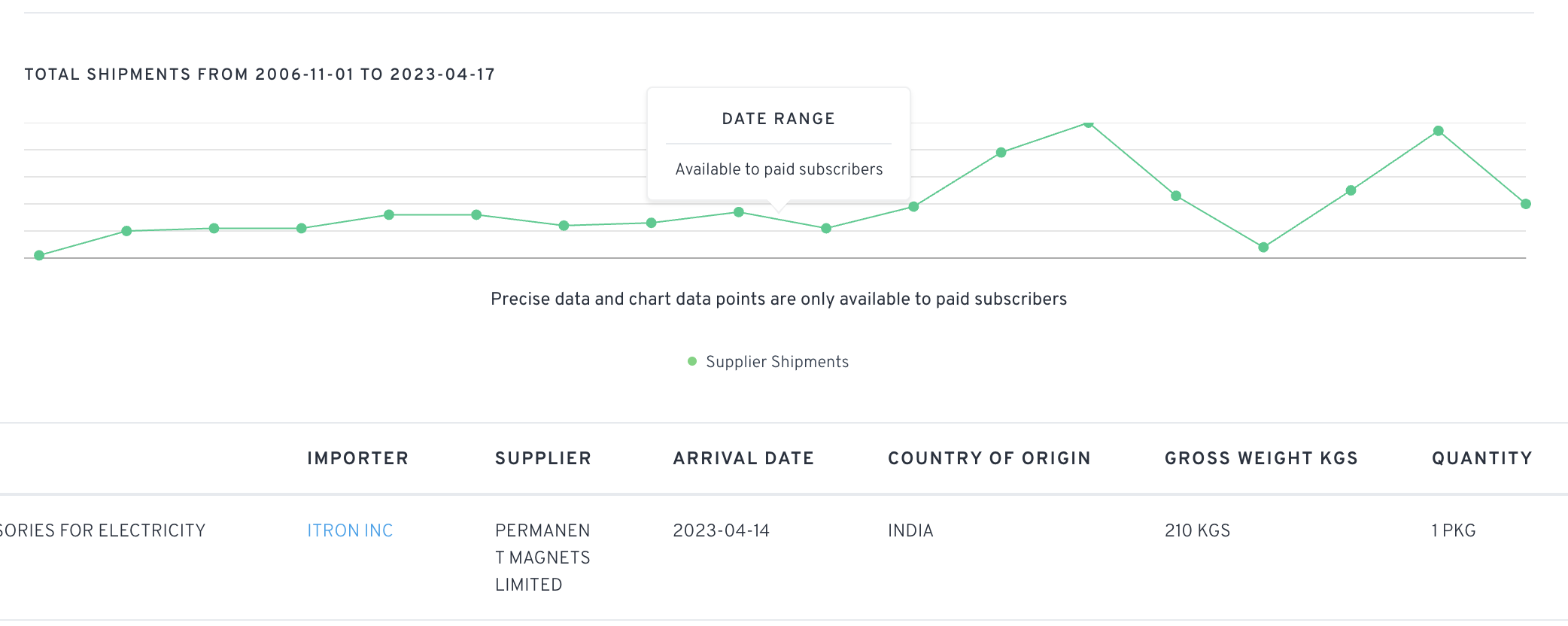

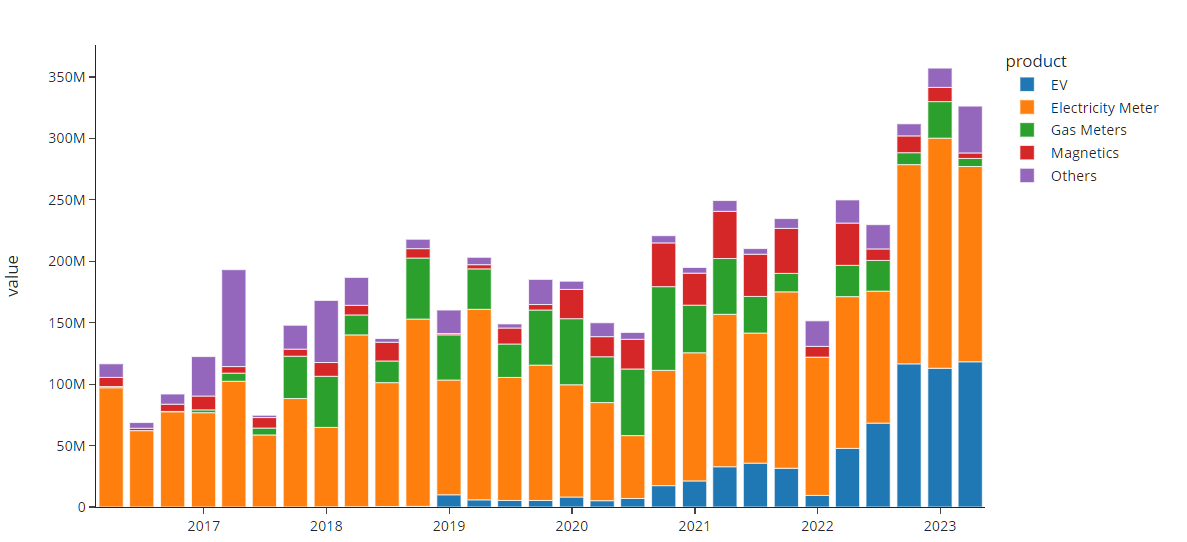

That is the total number of shipments exported to Itron till date. [253 containers & 894483Kgs which is sum total weights of all shipments to Itron]. Latest shipment is of 210Kgs.

Nevertheless, company has already exported as much as ~50% of 2022’s volume (# of shipments) in 2023 already. Below is the trend. Each datapoint in the graph correspond to a calendar year.

9 Likes

From where do you get the employee code for entering in epf portal

1 Like

a few questions from my side:

- When did the Taparias take over this company? Are they related to the family that owns Supreme Industries?

- Have you people noticed the queries raised by @dd1474 here Permanent Magnets - #5 by dd1474

2 Likes

Hi @dd1474

This is regarding the Borivali land, I quote from your reply “there is no benefit to the minority shareholders despite the land being developed”. Are you sure that land had been developed? Can we see the development on the google maps? I tried to locate it but could not pin-point the location of the land.

If you could share the google location of the land and we see the development at the location. We can always question the management why money has not accrued to the company?

Thanks

Gaurav Agarwal

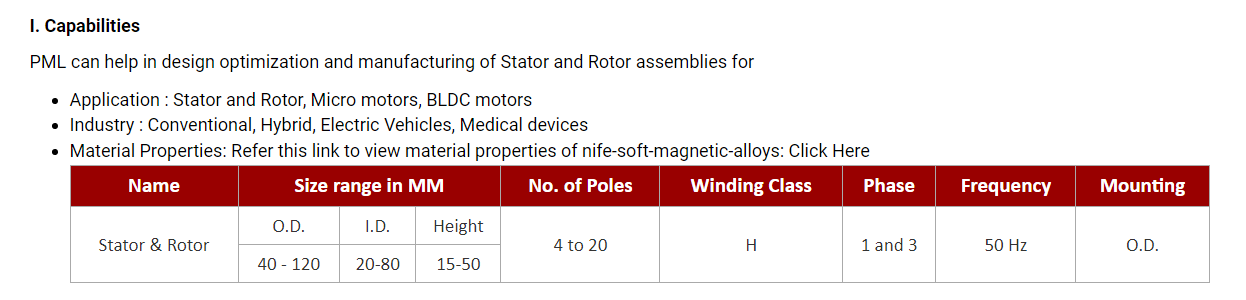

Something interesting is cooking in PML. Thanks to @phreakv6 that I had noticed this in their website. I will try to evaluate the products that are exciting me the most.

BLDC Motors

Source : Rotor & Stator Assemblies for BLDC Motors – Permanent Magnets Ltd

The specifications for the BLDC motors are very well defined. The project seems like it is in advanced stage with all the simulations and specifications displayed. The BLDC motor is also developed for a very niche application as we can see from the specifications. My hunch would be that PML has concrete requirement for a 2W OEM for development / manufacturing of BLDC motors.

Compared to a BLDC used in fans, they are more complex and we would need a Motor control unit ( MCU ) to control the phases. These components will need precise calibration so that the user does not feel jerks.

Please note this BLDC motor is not a hub motor which the current i-cube uses, the stator is the outer ring and the rotor is the inner ring (simply put: the inner ring rotates and the outer ring stays static)

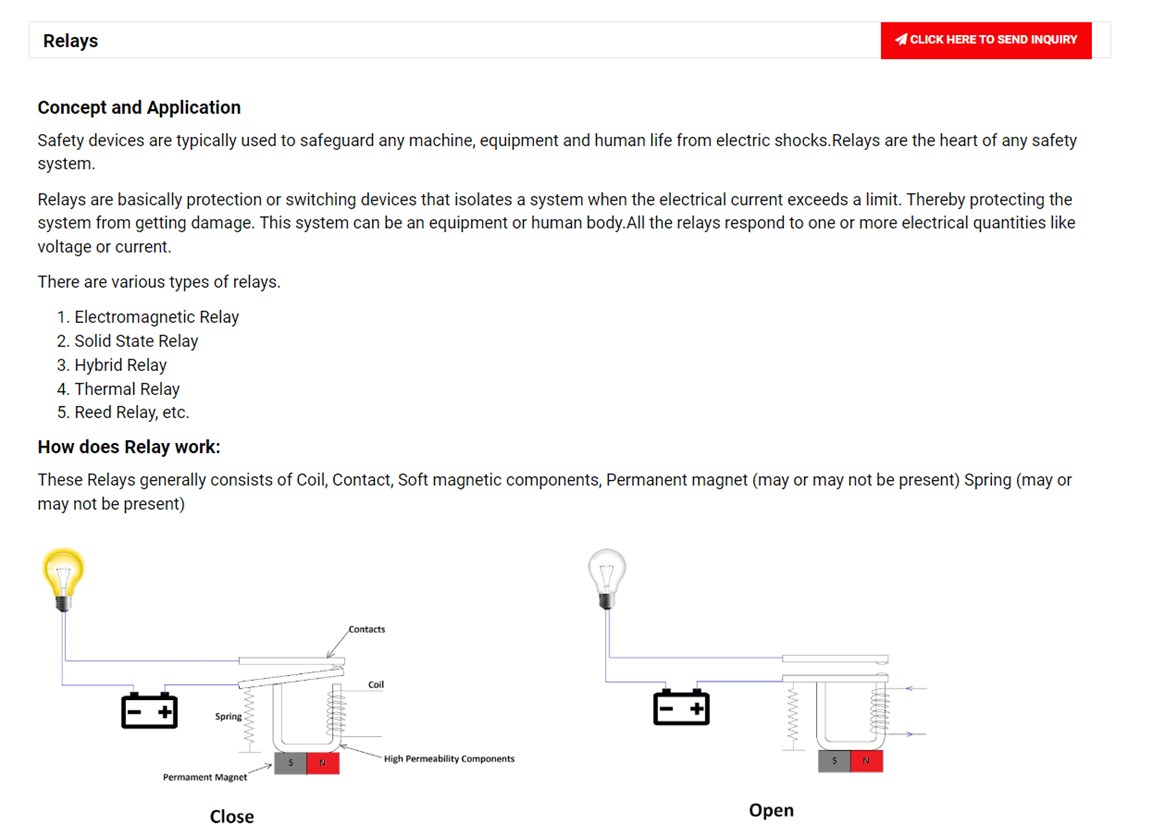

Relays

They have also come out with mechanical relays. Currently there are not much info on it and it does not seem like an automotive relay component. However, every EV will have a relay (also called as contactor, switches) which will disconnect the Battery from the rest of the powertrain. I would not be surprised if they come out with mechanical relays for automotive application soon.

Shunt Sensor Module

I think most of us know how important is a shunt sensor in the context of an EV. I see that the company has a direction.

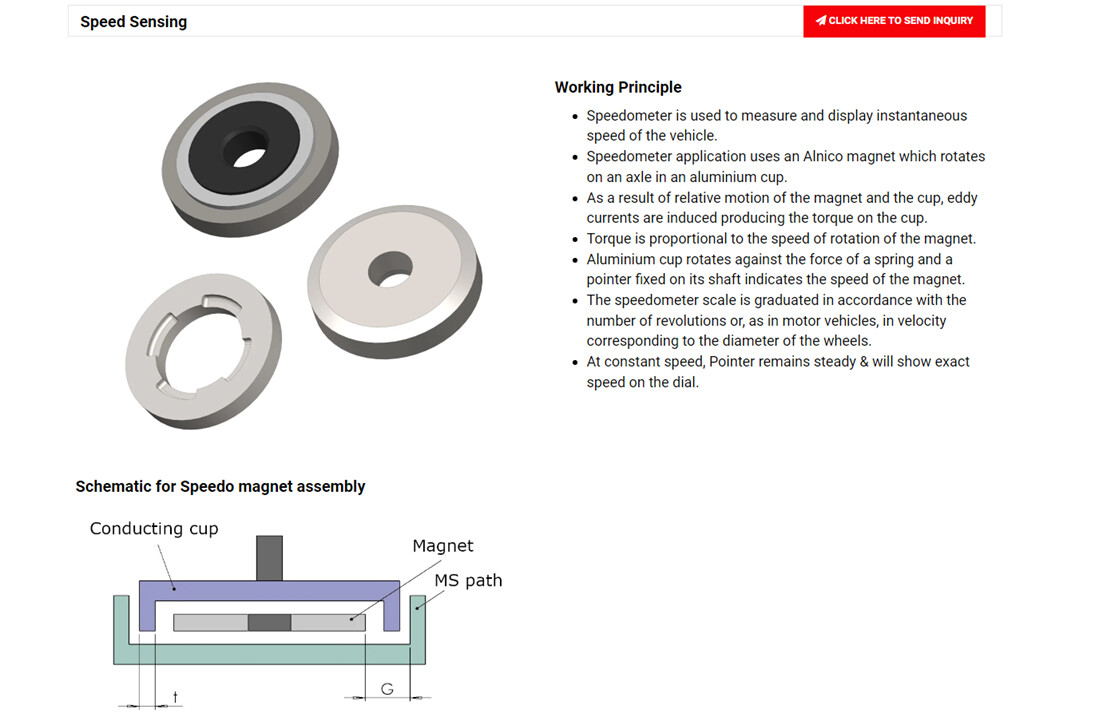

Speed Sensing

This is used to understand the speed of the vehicle. They are used in many places in a vehicle ( crank, wheels. gearbox etc. ) . In the context of 4 wheeler EV, I guess the most appropriate location will be in the 4 wheels if the vehicle has active safety enabled (anti skid, ESP etc.). Also they might be used in the out put shaft of the motor as a monitoring device. This item is also EV agnostic in my opinion

disc: Not invested. discovered this story late and currently tracking.

25 Likes

Information dump that might useful for people trying to understand the business

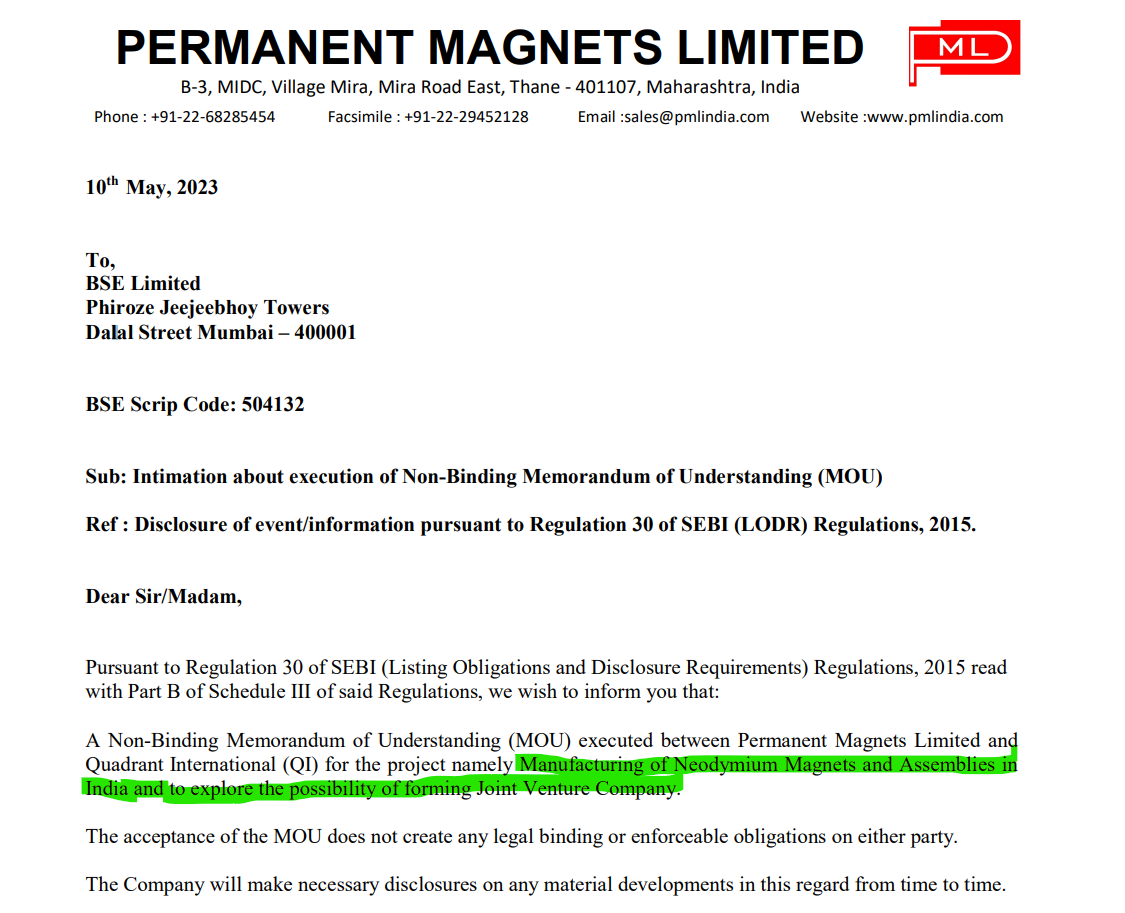

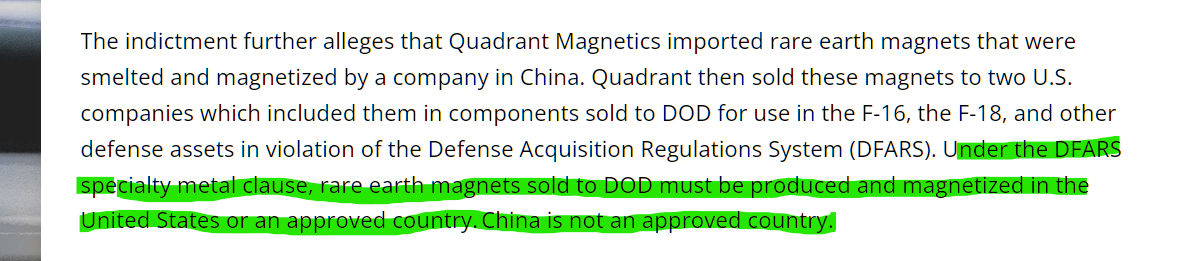

- Taken from today’s notification. This can be an interesting JV if it goes through.

Quadrant seems to be a world leader in magnetics

Even if a fraction of that manufacturing is moved to India, it could be a huge opportunity for PML. PML current imports NdFeB rare earth magnets for its lifters and other appliances it manufactures if am not mistaken. So it could be a good backward integration of a valuable component.

Quadrant seems to be a very good fit for PML in forward components and modules integration as well with its automotive applications. It can all add up so well if this thing works out. I would give the odds for it working out at 5% even if am optimistic.

- Recently came across the last 3 AGM transcripts. I think this helps understand management vision better than even the informative AR. @ankitgupta @ayushmit @desaidhwanil @rohitbalakrish_ have been following this for awhile as can be seen in the transcripts

Incidentally it was @ankitgupta and @rohitbalakrish_ that helped me understand the business late last year after I got excited looking at the AR

-

The land issue queried somewhere in this thread is addressed in multiple AGMs. The land is not developed and the land area is 1,25,000 sqft and PML has a 15% share in it and its value could be 25-30 Cr (I assume this is PML’s interest)

-

This is based on analysis I did on exports data. It is thus not indicative of complete company profile but what the management has been saying in IR/AR adds up in terms of EV contribution (at least in exports)

The split-up has some assumptions built in from my side and could be slightly inaccurate

What is even more interesting is that unlike the electricity meters business which is lumpy from a few large customers, the EV business is very fragmented and the company has at least 45 unique customers it appears to be dealing with.

(Thanks to @Sanjay_Kumar_E for helping out with data and interpretations)

This part of the business should be fairly robust, unlike the gas meter / electricity meter business IMO.

However, this business has several risks if you go through the AGM transcripts. The feel I get is this like a CRO/CDMO business that works based on projects in the pipeline and some of these could turn out to be big opportunities but there’s no way of saying when current products could go obsolete. When some project becomes big, PML becomes the suppliers until the lifetime of the product. But most of these should be micro/small contributions to the topline like in a CRO/CDMO business. The quarter on quarter numbers also could fluctuate just like one! I see so many parallels but please excuse if this is a stretch

The robustness of this business can only be measured by its “pipeline” and which projects are commercialised and how long their contribution will last, just as in a CDMO (I wish management gave us visibility on the pipeline like how a Neuland labs provides visibility on its pipeline and what stages the projects are at). Otherwise, this is a bet on the management to know what they are doing. So far they are doing really well if you go by @GourabPaul 's post above and go through the new website which lists all their products in much great detail. Also, to be able to sit at the table with a giant like Quadrant Magnetics itself is perhaps an achievement

Updated 05/11: Found this. Looks like Quadrant may have a motive for the JV too

Disc: Invested from 550 levels. No recent transactions. I feel the stock is very expensive at current levels and would think ~700 to be fair value

49 Likes

Documenting some readings which I came across while reading about Permanent Magnets.

Quadrant International: History page provides some very good insights on what the company considers it’s historical landmarks. It was established in 1992 with foray into light manufacturing and assembly industry → established it’s centrally located facility in Kentucky in 2001 → opened it’s own manufacturing hub in Hangzhou in 2010 → Foresee group, China becomes a contract manufacturer of Quadrant in 2013 → Opened motor manufacturing lines in Huizhou, China in 2018 → Quadrant opened it’s Australia operation in 2020 → Quadrant opened it’s Germany, Japan and Vietnam centers in 2021.

What am trying to highlight is, Quadrant was majorly focused on US & Chinese operation till 2020 and suddenly they have gone into different geographies such as Australia, Japan, Germany, Vietnam and now a chance of a JV with PML, India ?

What could be driving this change in stance ?

One possible explanation is the demand scenario is so strong that they want to diversify outside of China and US and the normal China+1 theme.

Second possible explanation as shared here

Third is, a major trend towards being self sufficient in rare earth resources (which includes neodymium magnets) which started few years back. Watching these 3 videos gives insights on what and why this trend. The 3rd video from James Litinsky, CEO of MP Materials is a very good one.

tweet from DARPA made on 13th May’23, stressing the importance of reducing overseas supply chain risk for rare earth metals

https://twitter.com/DARPA/status/1657097533745684482?s=20

Indian govt. (Indian Rare Eearth Limited) too opened a permanent magnet manufacturing facility in Vizag just last week, which saw nearly 200 cr. of investment to manufacture 3000kg of Samarium Cobalt permanent magnets.

https://twitter.com/india_projects/status/1656636082585468929?s=20

https://twitter.com/infraAP/status/1657241457252765696?s=20

Going to the Foresee Group site, one get’s a sense of the mind boggling size and scale of this company & industry. Foresee employs 600+ engineers and scientists, 5800+ employees, holds 86 patents, spends 20% on R&D (Same as Quadrant). This has all the characteristics of a high end R&D intensive, design oriented manufacturing industry which is critical for many industries including, defense, aerospace, electronics, EV, etc

Funnily, both Quadrant & Foresee use same picture (one of the pics) of a employee on both their site. Does this kind of tells us that both companies operations were very intertwined and Foresee wasn’t just a “contract manufacturer” ?? > Foresee & Qudrant

PML seems to have huge scope to upscale it’s capabilities & operations over time if they pull off the Quadrant opportunity. It’s up to them now how they grab this.

Given that now PML has announced it’s first ever public con call on 19th, let’s hope it has some good news to share with us. Stock price has shot up in last 2 days since the con call announced.

Disc: No reco. Have some holding, Hoping, if the story is good, there will be multiple chance to scale the position, since it’s not really cheap based on trailing multiples. But overall mcap of just 1000 cr. compared to scale of opportunity, this could be another Shivalik Bimetals?

20 Likes

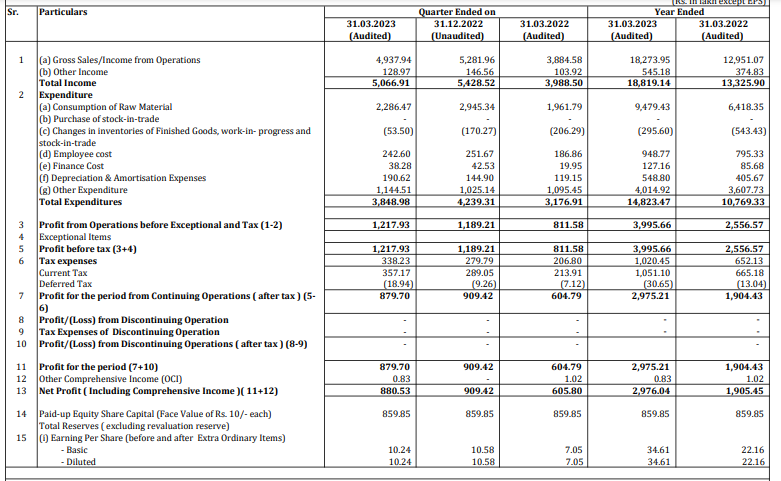

Management expects 20-25% growth next year with similar margins as current year.

1 Like

Notes from concall q4fy23 transcript -

-

Sales from automotive segment was 32% & sales from energy meters 45%

-

35% domestic and 66% exports in automotive.

-

Shivalik bimetal is our supplier, we use their material and we make assemblies which are customised to customer requirements for shunts.

-

Maglab is acquired by another company called CTS.

-

PML has been selected as preferred suppliers to Itron & we getting inquires for other products from them.

-

Smart meter 80% export 20% domestic.

-

We do not have any success from electronic gas meter parts and do not have any visibility.

-

Growth for coming year fy24 we expect about 20% to 25%

-

Hiperm division contribution to sales 50%, shunts 30%.

-

Modules sell was only Rs. 2 cr.

-

Region-wise exports America 29%, Europe 25%, Asia including India 46%, China may be around 10%

Out of 183cr revenue modules are only 2cr which is 1% of revenue. That means the company is not into modules at all and 30% of their sales is from shunts also they are buying shunts from Shivalik. Are they just doing trade of shunts without any value add!

Disclosure -

Invested in small quantity.

7 Likes

Adding few other Imp points from the notes which i have prepared:

-

Revenue Break is same like last year. Hi-Perm : 50%, Shunts : 30%, Magnet Assembly : 20%.

-

More than 50% revenue comes from current sensing.

-

Module sales - 2cr, as per management it is a very small number & it can have a steel increase in coming years.

-

Major competitors are in Europe, China & USA.

-

New technologies developed -

- Casting related. Manufacturing Stator & Rotor of the motor (Heart of the motor).

- High speed stamping.

-

Sales from CT Technology (Current Transformer) - 10 crs (Use Cases : LTCT & Energy Meters)

-

Two projects are going on related to Aerospace, but volumes are very less.

-

No supply in ferrite magnets, only supply of the alnico magnets for now. Generally motors are made of neodymium magnets.

-

PML isn’t supplying any magnet related products to automotive(it is very less), Majority goes into current sensing devices.

-

Capex related to new facility : 10crs Land, 15-20 crs for facility. Total ~30crs.

-

Trying to supply the BMS module as a whole . Currently shunts for EV is less, supplying only to 1 customer (4W segment, Quantity 3000 an year).

-

Price depends on the current carrying capacity of the shunt. Shunt assemblies in E meters can range from 10rs - 100 rs.

-

MOU related:

a). Partering with qudrant wrt neodymium , initial focus would be towards automotive & electronics.

b).Taking process raw material → metal → further processes of assembly. -

Tier 1 companies are supplying assemblies to the OEM’s.

-

There is an option to backward integrate & do EBW and make shunts. But not at the moment, focus is on forward integration.

-

Supply related chain info:

- Shivalik is the supplier & PML makes the assemblies using them.

- Customers give design for the module. PML supplies that to integrator’s.

My thoughts:

- Prices of shunts cannot go too much, PML has other customer in overseas also if shivalik has supply issues. The more forward integration one does on assemblies higher the end realisation. Modules & assemblies also will have higher margins.

- Shivalik again sells the shunts to tier 1 or tier 2 manufacturing companies which again make resistor’s etc. They cannot sell directly to customers or global OEM’s. Whereas PML directly interacts with customers. PML sells to the customer or direct tier 1 integrator.

- For me PML is very much exciting than shivalik right now. Considering so much value add possible in the forward integration.

- As shivalik is anyways manufacturing EBW machines also, PML can also even venture into making of shunts if it is very much required (as stated by management also).

Disc: No investment, just reading more. Will wait for some correction in the current multiple.

15 Likes

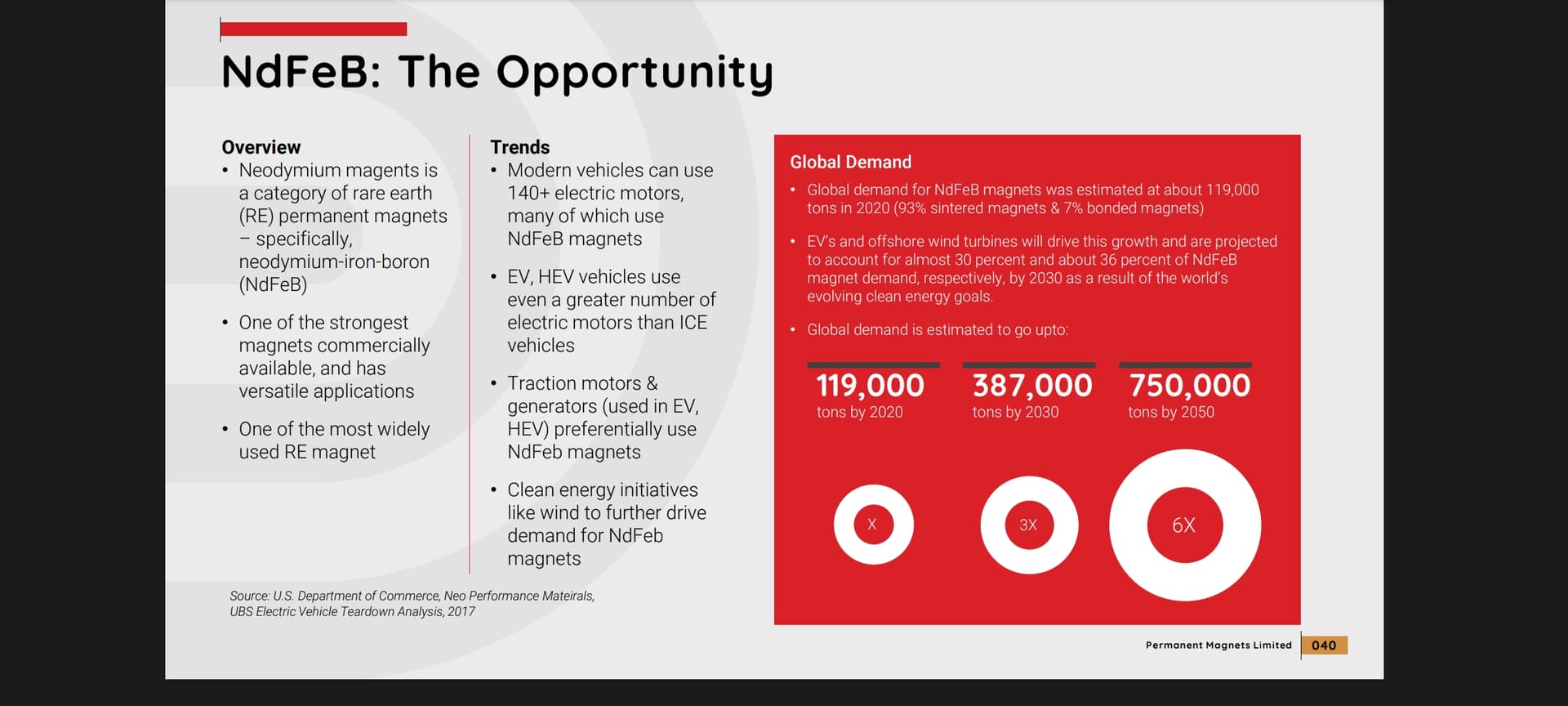

Have spent some time to better understand Neodymium magnets (NdFeb) landscape.

TL;DR version:

-

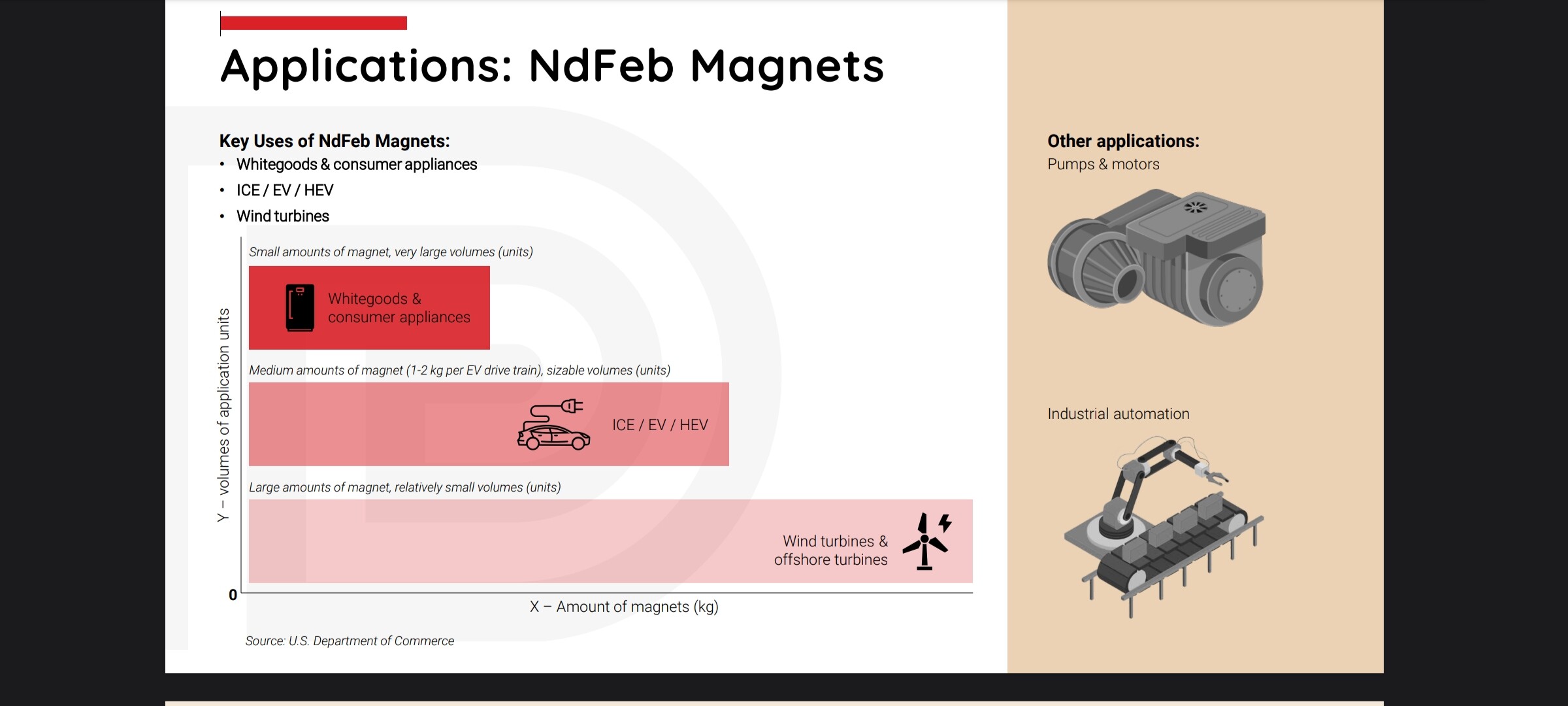

Neodymium magnets (NdFeb) are critical in defence applications (ship propulsion systems, guided missile actuators) and high precision industrial applications (electric vehicles, rotors for wind turbines) as they are the strongest permanent magnets commercially available and improve the efficiency of electrical machines making them essential in high-temperature applications.

-

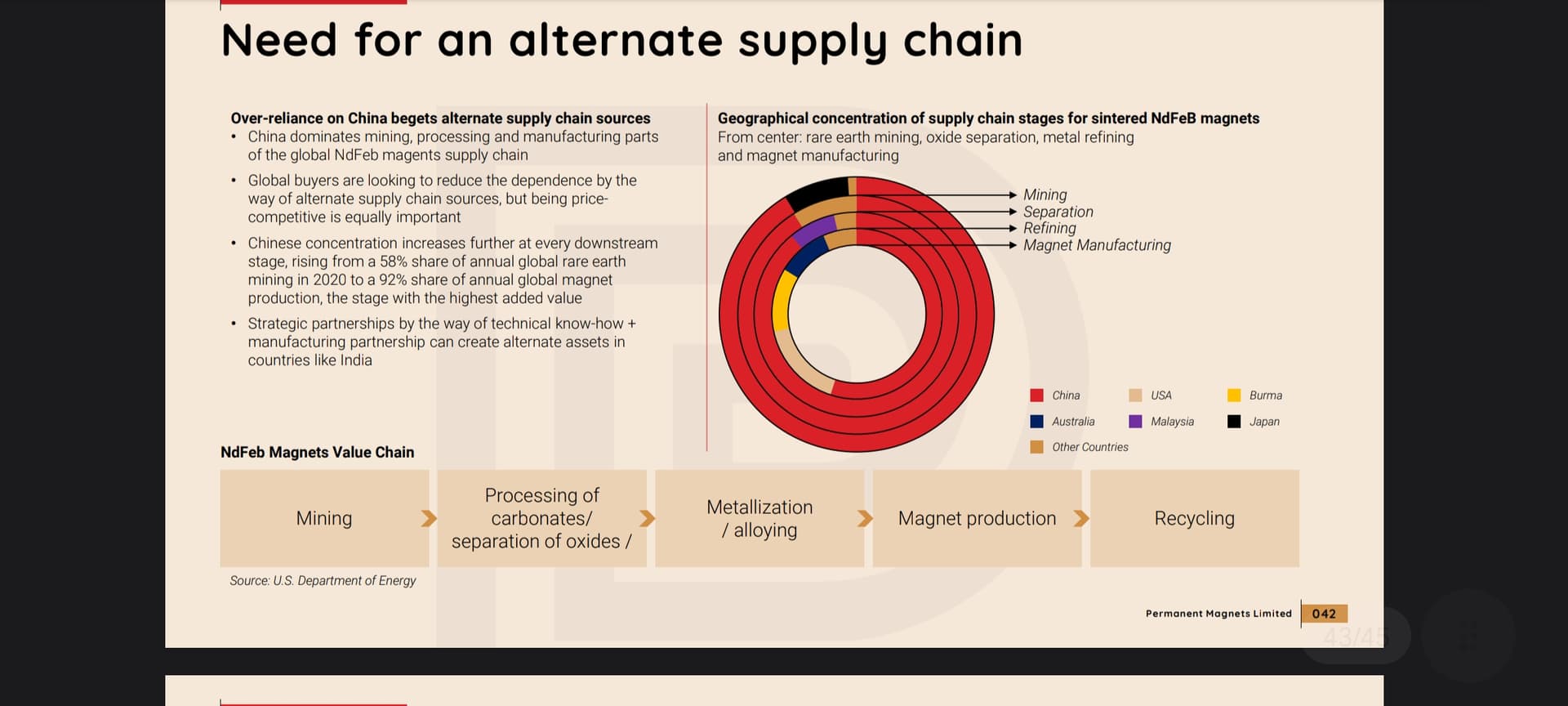

Demand for NdFeb magnet is expected to increase exponentially in coming years. > 3x in next 7 Years. However, US has almost negligible domestic capacity and is mostly dependent on imports. China is holding a dominant position globally - not only in end product (NdFeb magnet) but entire value chain.

-

Dependence on China leaves U.S. firms and U.S. allies vulnerable to Chinese coercion that could have a negative impact on national defence and the preservation of domestic critical infrastructure, such as transportation and energy.

-

All of the above factors converging together to force US policy shift and desperation to make US self-dependent (as much possible) on NdFeb magnet production eco-system.

Global Demand Mapping:

-

Total global demand for NdFeB magnets is expected to grow dramatically over the next decade, increasing from 119,000 tons in 2020 to 387,000 tons by 2030 and over 750,000 tons by 2050 in a net zero carbon emission scenario.

-

USA estimated total demand at about 16,100 tons in 2020. Which is projected to increase under a high growth scenario to 37,000 tons in 2030. Specifically for US, Electric vehicles and offshore wind turbines will drive this growth and are projected to account for almost 30 percent and about 36 percent of NdFeB magnet demand, respectively, by 2030.

-

Accelerated shift towards electric vehicle – USA is expected to have > 50% of all new vehicles sold be electric by 2030. NdFeB magnets are used in electric synchronous traction motors for propulsion systems in battery and hybrid electric vehicles. Each electric vehicle motor typically requires 1-2 kg of permanent magnet material

-

Offshore wind turbine generation - As part of clean energy objectives, US has set out a goal of deploying 30 gigawatts (30,000 megawatts) of offshore wind power by 2030 (from current capacity of 42 Megawatt). Within wind turbines, NdFeB magnets are used in permanent magnet synchronous generators (PMSG), also referred to as direct drive generators. The size of the permanent magnet is typically 2.7-3.2 tonnes per MW of wind turbine capacity

-

-

The United States directly imported about 7,500 tons of sintered NdFeB magnets in 2021. – 75% of this from China while rest 9%, 5% percent, and 4% coming from Japan, the Philippines, and Germany, respectively.

-

Direct imports of NdFeB magnets represent only a portion of U.S. consumption and the majority of U.S. demand is in the form of imported products with the magnets embedded in them.

Supply Side Equation across Production value chain:

Global supply landscape across NdFeb value chain:

Step 1: mixed rare earth element mining

-

The top upstream producers of rare earth minerals in 2021 were China (60%), the United States (15 %), Burma (9% percent), Australia (8%) and Thailand 3%) with smaller amounts coming from Madagascar, Russia, India, and Brazil. The largest single source of REs in the world is the Bayan Obo mine in China

-

In US, MP Materials and Chemours has rare earth mining operations. Some estimates suggests that total rare earth oxide production from Mountain Pass mine California was 26,000 tonnes/year in 2019, and MP materials reported producing 38,500 tonnes/year in 2020.

Step 2: Rare earth elements carbonates and Oxides processing

-

China 89% while Malaysia comprises 7% percent of the market for rare earth oxide separation (due entirely to the Australian firm Lynas Rare Earths operations in Malaysia), Estonia accounts for 1%.

-

In US, MP Materials produces primarily light RE elements, such as Nd and Pr, from the Mountain Pass mine in California. They currently send the concentrate to China for separation of rare earth oxides, but have raised funding (including through an award under the DPA Title III program) to finish rebuilding their domestic separation processing facilities, originally built by Molycorp, with the goal to begin production in 2022. If it processes all of its current production of concentrates, this could represent about 12% of current global rare earth production. MP Materials has also stated its intentions to establish a complete domestic supply chain from mining through magnet production.

-

Also, Lynas is planning a separation facility in Texas through its subsidiary Lynas USA LLC, with support from the DPA Title III program, which would be able to separate both light and heavy REs. With the addition of the light rare earth processing facility, it was estimated that, between its plants in Texas and Malaysia, Lynas would be able to produce about 25% of the world’s separated rare earth oxide

-

USA Rare Earths, which owns the Round Top deposit in Texas, has reportedly made progress in developing a separation facility in Colorado.

Step 3: Reduction of rare earth oxides into metals

- China holds 90% market share. Outside of China, production of metals is fragmented between Estonia, Laos, Thailand, the United Kingdom, Vietnam, and other countries, with no country having more than three percent of the market

Step 4: Alloying of rare earth metals and Magnet Manufacturing:

-

China market share of 92%. Japan is the second largest alloy and magnet producer (seven percent in 2020), and its firms produce metals, alloys, and magnets in Japan, Southeast Asia, and China.

-

Outside of China, major manufacturers of alloys and powders include Hitachi Metals (a Japanese company being purchased by U.S. investment company Bain Capital), Shin-Etsu Chemical (Japan), TDK (Japan), Vacuumschmelze (a German company owned by U.S. private equity firm Apollo) and its subsidiary Neorem (Finland), Neo Performance Materials (Canada), Less Common Metals (UK), and possibly Magneti (Slovenia). Shin Etsu produces magnets in Vietnam via Shin Etsu Magnetic Materials Vietnam; and Neo Performance Materials (formerly Magnequench) produces powders for bonded magnets in China and Thailand.

-

In US, lone domestic producer, Urban Mining Company (now called Noveon), manufactures sintered NdFeB magnets from recycled material and has received funding from the DPA Title III program

Patent/Know-how challenges:

-

NdFeB magnets were concurrently invented in 1983 by General Motors in the United States and by Sumitomo in Japan. The Sumitomo intellectual property passed to Hitachi, which has an extensive NdFeB magnet-related patent portfolio of over 600 patents, including about one hundred U.S. patents

-

Many U.S. companies noted that Hitachi has repeatedly declined to offer licenses to U.S. companies. Hitachi granted licenses to eight Chinese firms as early as 2013, which facilitated Chinese firms’ entrance in to the sintered NdFeB magnet market.

-

Hitachi has also defended its intellectual property rights in U.S. courts. In 2012, Hitachi filed a complaint with the United States International Trade Commission (U.S. ITC) against 29 manufacturers and importers of sintered rare earth magnets

-

Some industry representatives also expressed hope that the acquisition of Hitachi’s magnets business by Bain Capital may change Hitachi’s willingness to license the patents to potential market entrants

-

In contrast, Noveon relies on new proprietary technology to process recycled magnets and produce new material and is therefore unaffected by Hitachi’s reluctance to license its patents

Efforts to revive US domestic industry:

-

Proposal to establish a tax credit for domestic manufacturing of rare earth elements, NdFeB magnets, and NdFeB magnet substitutes.

-

The bipartisan legislation would establish a $20 per kilogram tax credit for rare earth magnets manufactured in the United States, and an enhanced $30 per kilogram credit for magnets manufactured in the United States for which all the component materials are produced domestically.

-

The Department of Defence (DoD) has made several notable awards through the Defence Production Act (DPA) Title III program to firms in the NdFeB magnet value chain. These awards have largely focused on the development of oxide separation and sintered NdFeB magnet production facilities.

-

Eligible U.S. NdFeB magnet industry participants, including NdFeB magnet manufacturers and producers at upstream and downstream steps in the value chain, should be encouraged to apply for loans from the Export-Import Bank of the United States (EXIM). (15 percent or 25 percent depending on firm characteristics)

-

Mandate minimum domestic and ally content requirements for NdFeB magnets used in U.S. Government-owned electric vehicles and offshore wind turbines that power U.S. Government-owned buildings. NdFeB magnets used in these products should be produced domestically or by allies and contain feedstock sourced domestically or from allies.

[worth paying attention to the wordings around “ally content”/"ally countries ]

- Defense Federal Acquisition Regulation Supplement (DFARS) that restricts the use of foreign NdFeB magnets in the military supply chain from 2019

Key US players - Current standing and future outlook:

Key US players in different stages of NdFeb manufacturing process are:

- Noveon (erstwhile Urban Minning Co.)

- MP Materials,

- Quadrant Magnetics, and

- USA Rare Earth

-

Noveon (erstwhile Urban Minning) - ** who Is the only manufacturer of NdFeb today plans to expand production over the next four years.** Noveon’s Texas facility is commercially operational and on-track to produce approximately 2,000 tons of magnets annually by 2024. In July 2020, under DPA Title III, Noveon was provided $28.8 million to develop NdFeB magnet manufacturing, which will begin in 2022 and ramp up thereafter. Noveon later received $0.86 million for an inventory demonstration.

-

MP Materials announced in 2019 that it was spending $200 million to establish a domestic processing and separation facility and announced in February 2022 plans to spend $700 million to establish a vertically integrated NdFeB magnet supply chain in the United States

-

MP Materials (along with Noveon) have received Department of Defense funding. They are looking to develop U.S. capacity in pre-magnet value chain steps, including rare earths mining, rare earth carbonates processing, rare earth oxides separation, metallization, and alloying.

-

MP Materials $35 million under the IBAS program for a heavy rare earth oxide separation facility, on top of a previous $9.6 million commitment in December 2020 to develop light rare earth oxide separation capabilities. MP Materials expects to commence production by the end of 2022.

-

-

Quadrant (Project code name NeoGrass) : Quadrant has announced the construction of a rare earth magnet manufacturing campus in Louisville, KY, under the project name of NeoGrass. Quadrant is investing more than $95M on this multi-year expansion, bringing approximately 200 full-time jobs.

-

TDA Magnetics - In November 2020, DoD also provided $2.3 million in DPA Title III funding to TDA Magnetics for a rare earth element supply chain study.

-

Lynas USA LLC, a subsidiary of Australian mining firm Lynas Rare Earths, received $30.4 million to establish a facility to produce light rare earth oxides, including neodymium. This facility is also expected to produce heavy rare earth oxides such as dysprosium

Based on forecasted NdFeB magnet production, domestic sources could potentially satisfy up to 51 percent of total U.S. demand by 2026. From 2022 to 2026 import penetration could fall to as low as 49 percent as domestic production ramps up

NdFeb Magnet substitute Development efforts:

-

Iron-nitride magnets, made of iron and nitrogen powder, have several attractive qualities and may become a viable alternative to NdFeB magnets.

-

Niron Magnetics is seeking to commercialize iron-nitride magnets as a substitute for NdFeB magnets. Iron-nitride is a high magnetization compound that has been known for many years, but which has yet to be commercialized because of the difficulties involved in manufacturing. In 2021, Niron Magnetics raised $23 million in its latest funding round

In conclusion, rare earth based magnets - specially Neodymium magnets has mission critical application from two critical perspectives: a) Defence and Military equipment’s manufacturing self-reliance, b) Enabling shift from fossil fuels by way of adoption of Electric Vehicles and Wind Power generation. While USA is aggressively strengthening its domestic manufacturing capabilities, its equally important for them to have strong supplier base within allies countries across the global. More so, since most of the end products where NdFeb is used is still manufactured outside of US.

Specifically for Permanent Magnets co., this white space ex-US could be an interesting opportunity. Even, the recent press release and concall etc. are suggesting that the proposed partnership/JV with Quadrant may explore such opportunties.

A world of caution though, specifically for Permanent Magnets co., this is still an evolving story. As of today, they may have some peripheral competencies in metallurgy and different magnet manufacturing however nothing directly related to Rare Earth based magnets manufacturing. Will have to see their placement in value-chain, construct of partnership, value-add potential and scalability scope etc.

Thanks,

Tarun

Disc: Invested

28 Likes

Here is the snapshot from the department of energy report plotting down the different metals on importance to energy vs supply risk graph.

https://twitter.com/big_lithium/status/1665070857293639681?t=kbhdaiBnuv1ErmQ1gnw-LQ&s=19

4 Likes

As we rely quite a bit on the auditor to provide us information, one of the check as part of my due diligence is to dig into auditor’s integrity and their opinions on audit report.

Auditor Integrity

The current auditor is Ramanand & Associates, established in 1998. Was researching to see if they have some legal proceedings. Found this one where they are said to have helped a company (RKDL) siphon off IPO proceedings around 2010-11. They had been fined by SEBI for the same.

You can check Page 122 of the report starting from point 167.

This happened quite a while before and I am not sure if the same people involved in auditing permanent magnets. Am just pointing it for sake of information as we investors rely on auditor to a much greater extent for smallcaps.

Opinions on audit report

As per the opinions on audit report, there are two instances:

Pending case in Bombay High Court:

This doesn’t seem to be much of the issue as the amount in question is just 19 Lakhs.

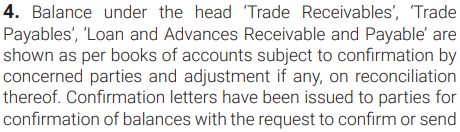

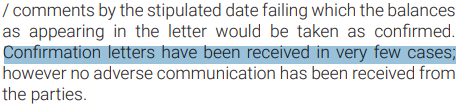

Trade receivables:

As per this the majority of receivables are “unconfirmed” by the parties. There is no provisions for doubtful receivables (not able to find how they would classify something as doubtful either). Historically, the days receivable is trending around 90-100 which provides some relief.

Disc: Invested recently

8 Likes

I attended both the concalls and at present both companies have decided to coexist without cutting down each other. Shivalik supplies the shunts to Permanent Magnets which they are further integrating into value added products.

Shivalik sees Permanent Magnets as a customer instead of a competition.

Disclaimer - Invested in both and very positive on both stories over next few years.

5 Likes

I don’t understand what further integration Permanent Magnet is doing with the shunts supplied by Shivalik? As per concall their modules sales was just 2cr which was 1% of their revenue?

So they are actually not using the shunts in the modules so what kind of value they adding here?

1 Like