Interesting points to look at! demand outlook need to be drilled down further

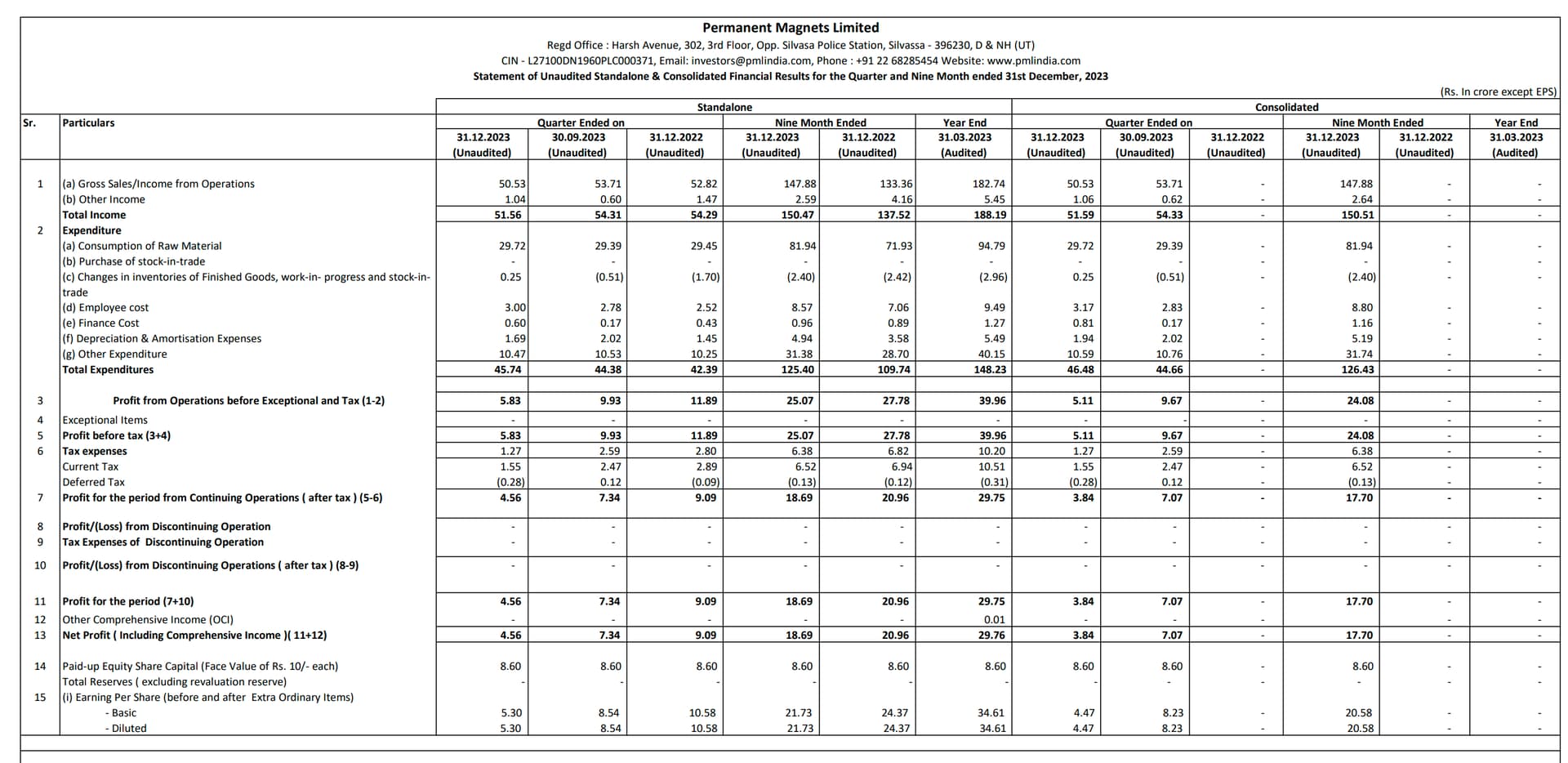

Company is pretty aggressive in revenue recognition. CFO was 11cr but PAT was 30 cr, i.e. CFO/PAT is 39%. This looks like red flag. CFO/PAT in previous years were 19% and 39%.

1 Like

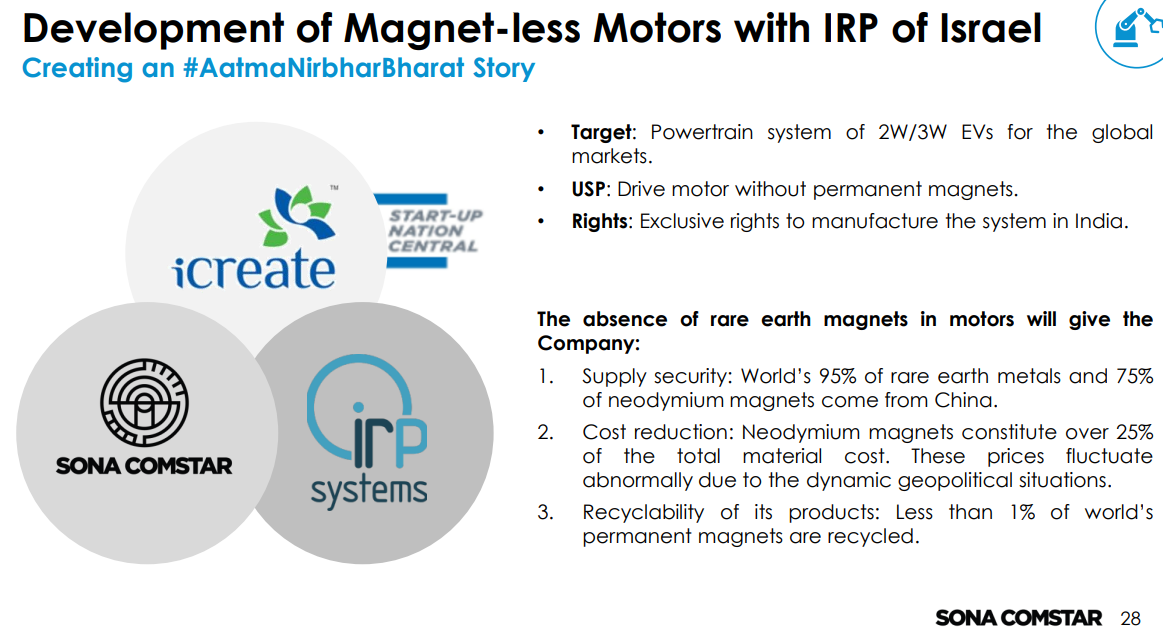

Excerpts from Sona Comstar’s Investor Presentation & Q2 FY24 Concall regarding Magnet-less EV motors:

New developments in Magnet-less EV motors could pose a risk to PML’s neodymium business catering to automobiles, but these developments are nascent. The market for these motors seems very small at the moment and Sona Comstar might have exclusive rights to this technology if it’s commercialized in the future.

5 Likes

Any mention of environmental pollution from mining of rare earth metals used in permanent magents products and impact there off.

Are they doing something to decrease the pollution. Anyone knows or enquired during concall please update

Guys - I really love this forum. Such valuable insights into the company, the opportunity, the potential risks. I’ve learnt a lot reading the VP Forum and I’ve tried to take inspiration from some of the insights mentioned above to write this article - Permanent Magnets - by Siddharth Bothra - Sid's Blog

At a market capitalization of around 1,200 crore - if it can further capture the automotive opportunity + Neodymium opportunity, there should be more room for growth.

Disclosure: I’ve invested a small quantity in this stock to track it more closely

3 Likes

Does anyone know why PAT collapsed so much?

Press release by the company will clarify why PAT collapsed

6 Likes

Thanks, I wish they offered more detail.

@Rudresh Link isnt working anymore. Do you have a copy of this release by company?

Also, anyone tracking order book for Permanent Magnet?

Key takeaways from Q4FY24 earnings call transcript:

Financial Performance: The company reported a 9% increase in total income for the quarter and full year. However, profitability margins declined due to changes in the product mix, particularly from slower EV customer business.

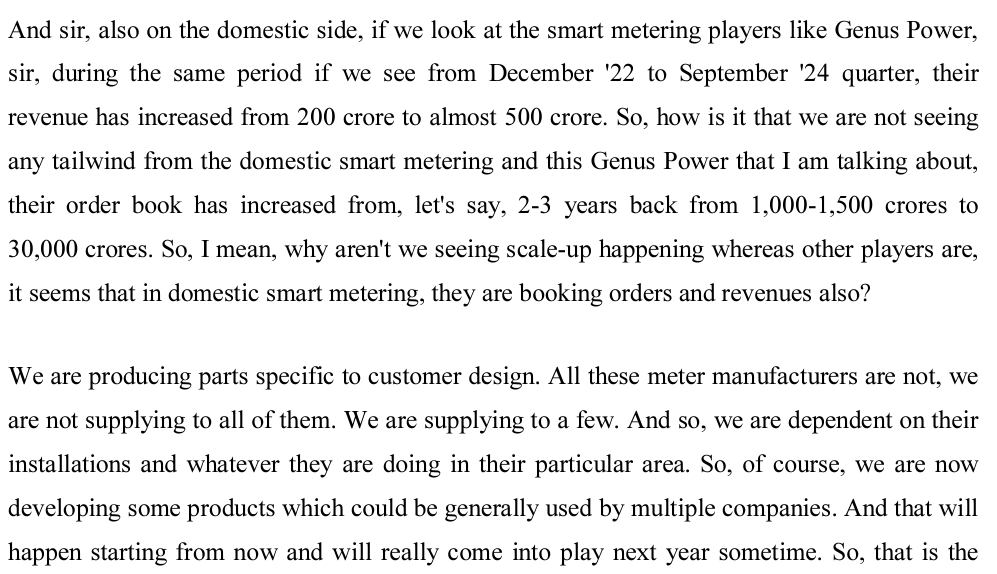

Smart Meters Market: There is a significant opportunity in the domestic smart meters market, driven by government policy. Out of a target of 250 million meters, only 11 million have been installed. The company is expanding its product offerings in this segment.

Alloys Facility: The new alloys facility commenced in Q4, focusing on products with quicker scale-up and longevity. The company is in advanced talks with prospective customers in oil, gas, and aerospace for commercial supplies.

Quantum Magnetics: Revenue from quantum magnetics is expected to scale in the coming years, starting with components and assemblies made from rare earth magnets, with further backward integration planned.

6 Likes

@ankitgupta Are you still invested in Permanent Magnets. Do you have any views on the company?

Do you think FY25 numbers will be flattish?

Hi Venkatesh,

I trimmed a bit around 1400 - 1500 (40% of my original position sold) due to valuations but continue to hold the rest. I track the company as I used to do earlier only. I think EV segment has slowed down quite a bit and we arent sure when the revival will come. However, there are other three segments which are expected to do well for them - alloys, domestic meter segment (which they earlier weren’t sure on the scale up) and the JV with Quadrant to manufacture and assemble Neodymium Magnets. Revenue scale up will happen with all these segments despite EV slowdown. However, margins might be lower than what they used to do. These three segments provide them a good opportunity to scale up considerably.

7 Likes

Very relevant question asked by a participant in latest investor call. reply is not very convincing.I feel smart meter was a huge tailwind not being exploited by the company, Ev trend is also in danger of being missed out. What is forum’s view?

Disc: small tracking position in co, thinking of whether to exit or stay on.

5 Likes

Any idea about the sudden change of direction of the stock price? Searching news channels, but no info.

Disc: Invested

On 25 Dec 25 - Company has acquired an additional parcel of land measuring 127.20 Gunthas. This land is situated in the village of Juchandra, under the jurisdiction of the Vasai-Virar Municipal Corporation, District Palghar. Any update from Ananta Capital meeting on 10 th Jan what are their plans ?

1 Like