NTERARCH and Pennar industries are set to grow at a good pace for next many quarters to come. Pennar does PEB for US markets as well where margins are very high

While Inter is delivering 50% growth in north India by the end of Q2 PENNAR has also commissioned a plant in Raibareli UP. Both Inter and Pennar are expected to deliver very good earnings growth for next 6-8 quarters.

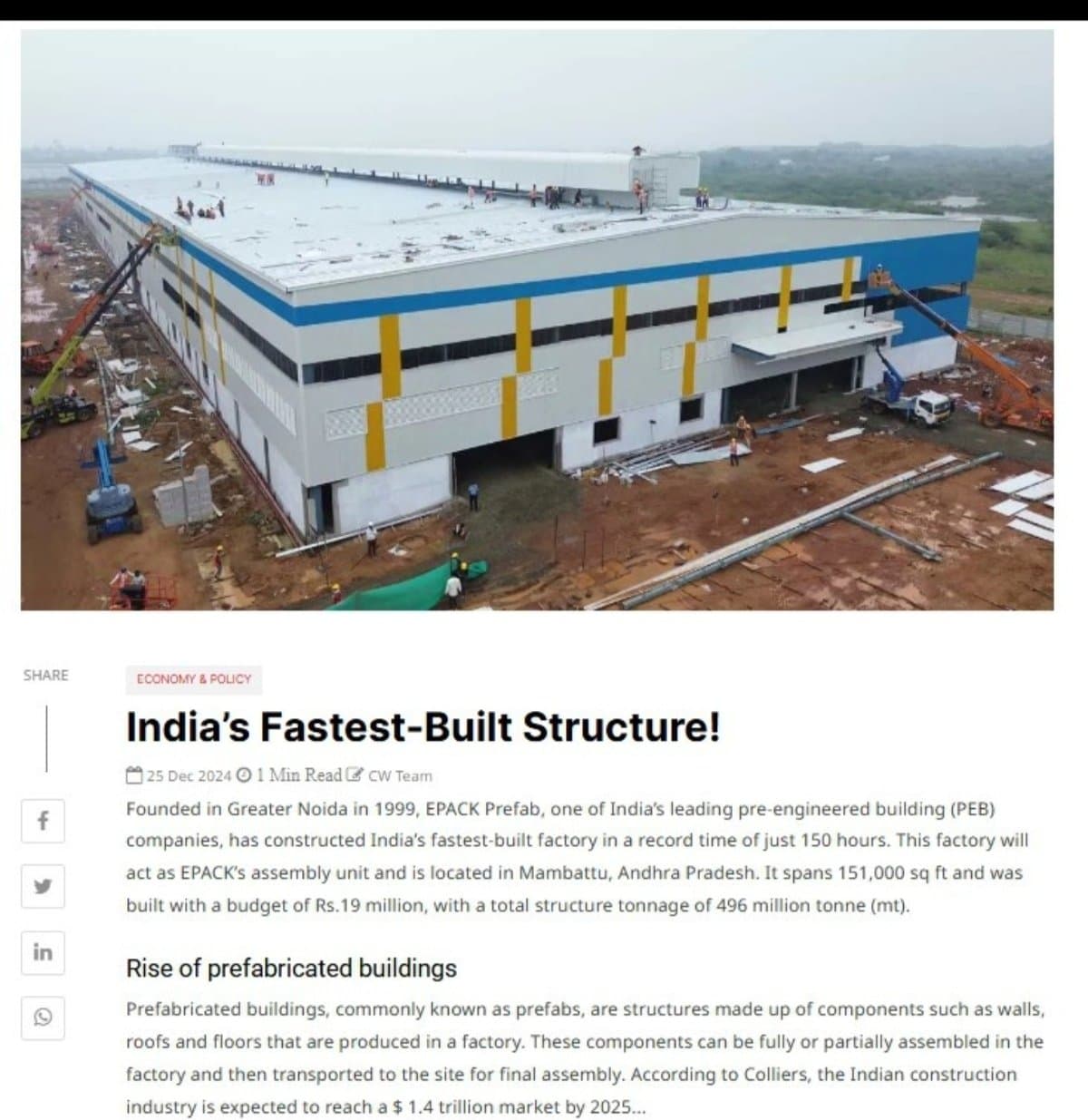

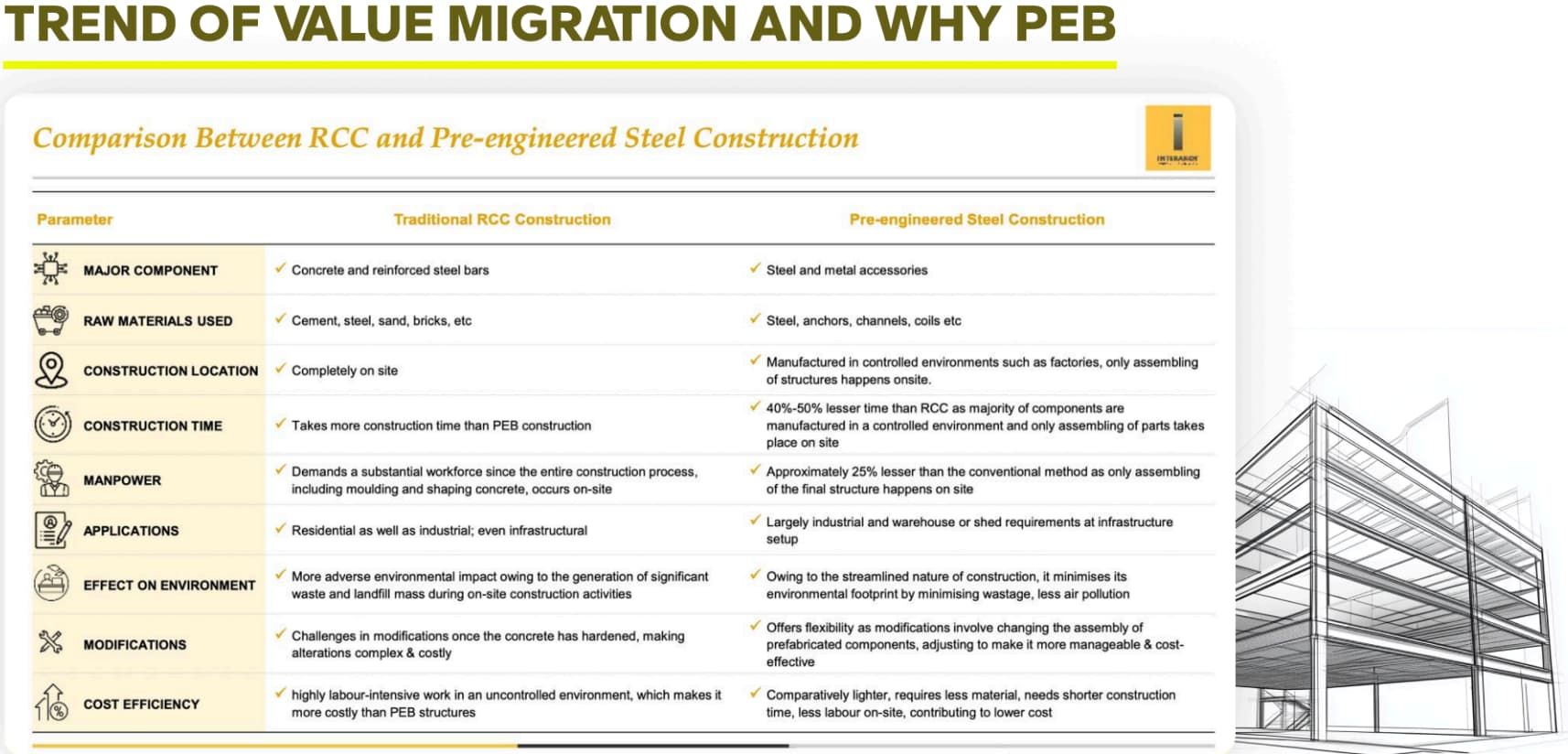

Shows the benefits of Adoption of PEB. Capex done at fast pace. With the time and man hours it takes for approvals - PEB can be a cost efficient way to increase turnaround and capacity bump up

This one was by e pack but Pennar is doing almost the same thing and that too on US Soil which makes it a larger TAM

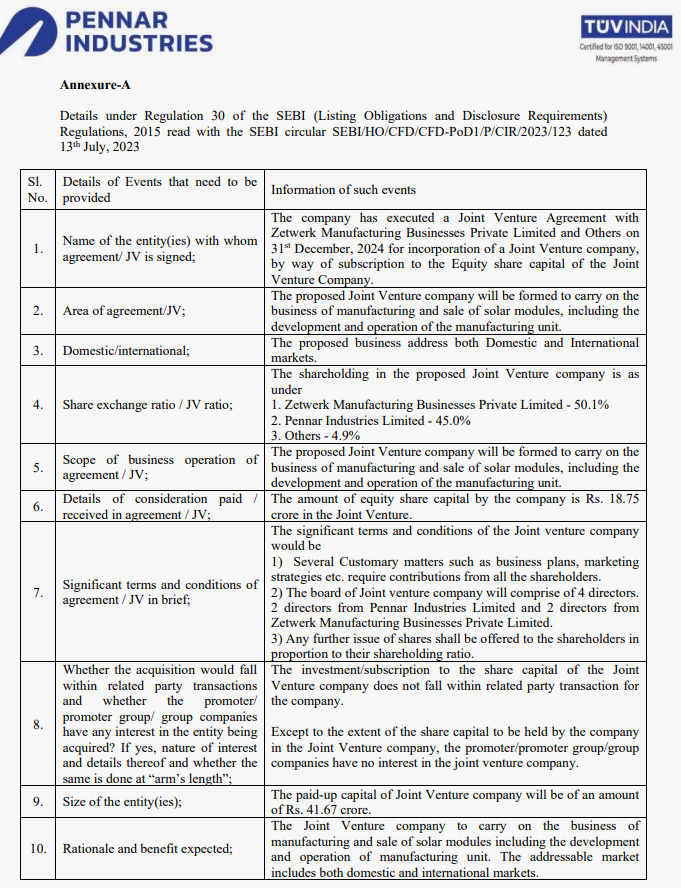

Pennar Ind to form JV with Zetwerk Mfg & others for mfg & sale of solar modules

Pennar Industries Limited (PIL) is a leading engineering building company headquartered in Hyderabad. It has presence in India, US and France and offers a dive portfolio to six key sectors - infrastructure, automotive, railways, construction, general manufacturing, white goods and solar.

PlL has 13 manufacturing facilities in India, in the states of Telangana, Tamil Nadu, U.P., Maharashtra and 3 facilities outside.

They cater to all the B2X segments.

In B2B sector, supplies to automotive and industrial OEMs.

In B2C, it supplies to dealers, sub-dealers and retailers.

In B2G, they serve railways (no direct to government)

They have 2 main sources of revenue -

Diversified Engineering

Contributed 52.43% to the total turnover with over 1000 precision engineering products.

Business Activity includes Railways-Wagons, Steel, Solar Module Mounting solutions, Industrial Boilers & Heaters, Chemicals & Fuel Additives, solar panels, precision tubes, BIW, hydraulics and auto components

Custom Designed Building Solutions & Auxiliaries

Contributed 47.57% to the revenue

Business Activity includes Pre-engineered Buildings, construction equipment and Engineering Services

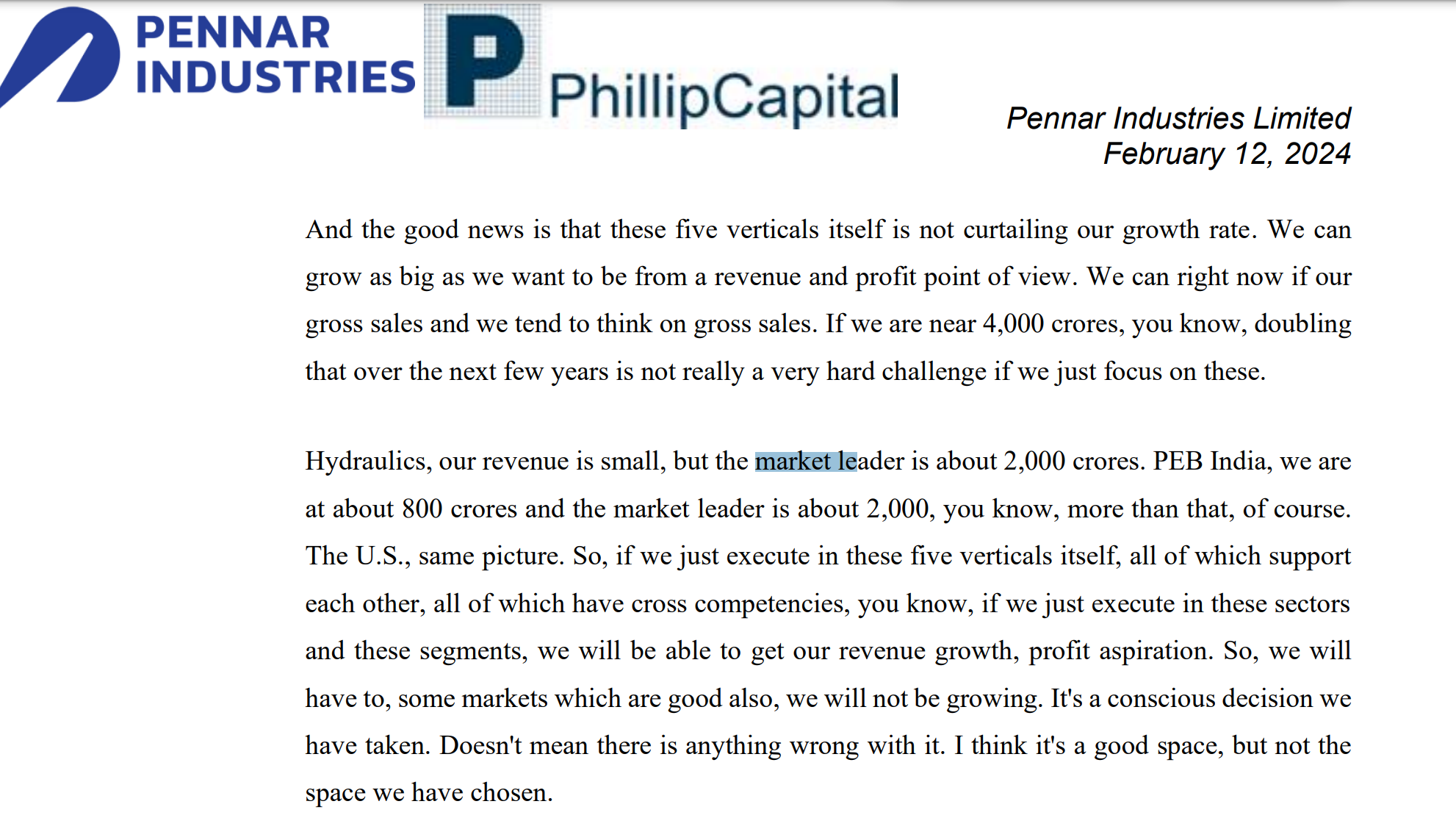

They are strategically shifting from low margin to high margins and to do so, have identified 5 growth verticals:

PB (India)

PEB (US)

Hydraulics

Process Equipment & Boilers

Engineering services

Guidance

Near Term (2-3 years)

Exit lower margin business which contributes 35% of the overall revenue base.

Improving working capital management to 72 days

Aim to reach 7% PBT and PAT margins of 5% and double digit revenue growth.

Long Term

Exceed $1 Billion in Revenue in the next 5 years

As they move away from low margin business, there will be an increase in the EBIDTA margins

Expanding capacity in the key verticals and gaining market share

Products

We can divide their product verticals into commodity and VAP segments

Commodity

Steel products and profiles

Railway components

Value Added Products

Pre-Engineered Buildings (PEBs)

Gross margins for their Indian business is 18% while market leaders have 28-30%

Gross margins in the US is 30% and could move higher

They expect EBIT to be 10% for India and 15% for their US business going forward

Hydraulics

OPM are of around 20%

The revenue is export-oriented

Boilers & Process Equipment

Engineering Services

Operating margin is about 30%–35%

The TAM for the railway products, primarily coach and wagon components and subsystems, is about Rs 2,000 crores. They had 250 crores revenue last year from this vertical however, it’s not a primary growth vertical as it’s highly competitive with limited product development.

Have completely exited from their water treatment business as there is a very low entry barrier and low growth and scaling opportunity.

They expect the PEB (US) to be their fastest growing business.

Body in White is a slow growth product and hence not their core focus.

Their low margin business achieve PBT margins of 2-3%

They have established a production facility in Hyderabad for catering to aerospace markets.

Geography

Export accounted for 7% of the revenue.

Commissioned a PEB plant in Rae Bareilly to tap into the North and Eastern markets and expanding capacity in the West India.

Establishing a new plant in US focusing on metal buildings and high-rise structures.

Scaling their global presence - in the US, European and Australian markets, to increase export contributions.

Subsidiary

North America

Pennar Global Inc. (PGI): providing engineering services and marketing Pennar Products across the USA.

Pennar Global Metals, LLC: Step down subsidiary

Ascent Buildings, LLC: Step down subsidiary, focused on PEBs and plays a significant part in PILs growth

Europe

Pennar GmbH: Based in Germany, spearheads the company’s expansion in the European market, provides engineering services to European clients

Cadnum SARL: A step-down subsidiary which is located in France and it Engineering and precision company

India

Enertech Pennar Defense and Engineering Systems Private Limited: Focuses on the defense and aerospace industries within India

Pennar Metals Private Limited

Clients

Have over 500 customers across various industries with no single customer contributing more than 10% to the company’s revenue.

Over 50% of the PEB order book comes from repeat customers.

In the U.S. market, their competitors (Nucor and Cornerstone) for metal building companies are also customers for engineering services.

Their CEO in the U.S. is Kimbell, who previously built Cornerstone into a successful brand.

The BIW division’s main customer is Stellantis, a $300 billion company. It takes a lot of time for them to acquire business in this segment and they are working to add three more blue chip automotive component manufacturers.

Raw Material

The raw material cost is the major cost component and accounted for 60-65% of total cost of sales.

They use steel (Steel strips) as a primary raw material in its manufacturing processes and 55-60% of the total raw material consumption.

Steel price fluctuation will have an impact on the companies revenues and margins

Capex

Rae Bareilly plant which should reach max capacity by September 24, will increase the production capacity by 25%-30% with a revenue growth potential of 300 crores. It will start contributing to revenue from Q3 FY25

They are nearly doubling capacity in the US throughout FY25.

They expect the boiler plant to double its revenue in FY25

They are expanding capacity in Hydraulics and process equipment and investing capital into our large diameter tube business

For Industry analysis and more detailed deep dive in the PEB industry

Notes

The order book stood at 840 crores as of Q2 FY2 for India and $54 million for US in PEB while for railways it stood at 100 crores.

They expect to execute their PEB orders in 6-8 months however they face capacity constraint especially in the US.

They are witnessing strong order books for PEB, Hydraulics, Boilers and Process Equipment

Exiting lower-margin businesses, including solar, water EPC, and solar MMS and they will either be liquidated or absorbed into other business units

The market leader in hydraulics, Wheels India Ltd in India has annual revenues of approximately 2,000 crore while PIL is very small currently.

They have sub 2% market share in the U.S. in the metal building and PEB space

There are lot of clear indications of margin expansion along with a more diverse product space and International exposure with higher margins. As others have mentioned, need to track the implementation by the management along with how fast are they exiting the low margin business.

I don’t think WIL business is 2K crore in hydraulics segment. As per the annual report FY24, hydraulics generated ~160Crs and management clarified to double this segment in 2 - 3 years as the demand is robust. Below snippet from AR about Sundaram Hydraulics.

Yes that’s there overall revenue. I also had check that they had 150cr from hydraulics however their total revenue is around 2k crores. It could be possible that WIL is not the market leader?

Some Key pointers captured from the call on Growth

Segment-Specific Growth Projections:

PEB India and US (Ascent Buildings): PEB sector to be a major growth engine. Both the India and US PEB businesses will grow strongly. Raebareli plant and planned US greenfield capacity expansion are key drivers. Strong order books in both geographies validate the growth potential. Should see qoq growth hereon in PEB revenue.

Body in White: BIW is another significant growth area with good future potential. They expet it becoming a ₹1,000 crore business over the next few years, and current progress already above ₹100 crore marks a good starting point. Customer acquisition (Stellantis, Hyundai, Kia, Maruti etc.).

Diversified Engineering & Custom Building Solutions: These segments are already seeing growth and are expected to continue contributing to the overall revenue expansion.

Tubes (Longer Term & Niche Focus): Growth in the tubes business is approached more cautiously. While they see potential in niche, high-margin segments like large diameter and precision tubing, scaling this business is expected to be a more gradual process. Large diameter tubing, in particular, needs time for CAPEX investments to materialize and contribute significantly to revenue. Hence, tubes are not currently viewed as a primary short-term growth vector, but medium-term.

Engineering Services: Mentioned as a growth vertical, will be driven by outsourcing trends, especially design engineering for US clients.

Hydraulics: Expected to maintain a steady performance but growth narrative is more related to efficient restructuring for better reporting rather than rapid expansion.

4. Geographic Growth - India & US Markets:

India Market (Primarily PEB & Diversified Engineering): India remains a crucial market. Growth in India will be significantly driven by PEB sector and diversified engineering businesses. The Raebareli plant is designed to tap into the growing Indian market for pre-engineered buildings.

US Market (Ascent Buildings/PEB US & Hydraulics): The US market, primarily through Ascent Buildings (PEB) and hydraulics, is a major area for expansion. Strong order book in US PEB signals robust growth. Capacity expansion plans (greenfield plant) are directly targeting the US market.

Margin improvement to 7% in PEB space expected in relatively short-term. Overall company margin improvement to 7% and then 10% targeted over medium-term.

35% of current revenue from de-prioritized businesses; expected to reduce substantially YoY to near zero within 5 years. This is expected to be the key driver for margin improvement and cash generation.

Overall growth guidance is double-digit CAGR growth. PBT margins to reach 7% but no specific timeline commitment.

Valuation:

Growth & Margin: Assume 10% CAGR growth for next 2-3 years (FY27-28). Project 6.5% PBT margin (below 7% guidance).

EPS Projection: FY27 EPS ~ ₹14, FY28 EPS ~ ₹16 under these assumptions.

Current Valuation: Stock at 10-11x forward PE (FY27).

Potential Upside: 15x exit PE by FY27 end → ~20% CAGR return.

High Upside Scenario: If execution strong, ROIC improves, and market awards 20x exit PE → potential to double in 2-3 years.

Question: Is 10x forward PE entry + potential 15-20x exit PE re-rating a reasonable investment calculation?

Overall management seems to be optimistic. Though the capital investment in JV is not big, need to see the quantum of losses JV can have in the initial years. Any big surprise can impact bottom line of Pennar.

See the total investment for them here is 18crores and they are almost hinting that they will sell off their solar epc/arm eventually at profit. They are not providing management bandwidth here to this smallish bet/vertical.

^ This clarification was in depth and almost the very first question addressed in the concall. We can sideline this and focus on things like PEB and US arm for PEB.

Can someone please highlight why we one should choose Pennar over let’s say Interarch or others? What’s the advantage that Pennar has in terms of anything.. Be it geographical, client relation or whatever..

Backward Integration- Manufactures its own steel components, tubes, beams, etc., unlike many PEB players who buy from others. Higher margin and more stability.

In-house Design - Pennar has a dedicated design and engineering team which give customised solution.

Pennar has big clients like L&T, Siemens, GE, Tata Projects, JSW, Indian Railways. Long-term relationships in sectors like railways and infra give it a sticky revenue base.

Manufacturing plants in Telangana, Tamil Nadu, Maharashtra, and Gujarat

US PEB, the base is small but growth opportunity is higher due cost effectiveness. can offer lower price then competitors. Profit margin will also be higher as they make components in Indian and erect them in US.